The future of biosensing wearables

For full access to this report and all of our research, become a Rock Health partner—email partnerships@rockhealth.com.

2014 has been a year marked with pessimism about the future of biosensing wearables. Put simply: we’re not buying it. After spending over a year looking at the space—including evaluating 100+ startups for investment, watching venture trends, and working with giants from both in and outside of healthcare—we know interest has never been greater. However, excitement shouldn’t be mistaken for impact. We expect biosensing wearables will need to leverage their consumer learnings and evolve into highly functional and accurate devices in order to gain adoption in the industry.

The opportunity here is not to be underestimated. A long tail of evolved biosensing wearables, enabled through platforms, has the potential to improve health outcomes and lower costs. Only time will tell if the reality matches the promise—we’re optimistic.

Landscape

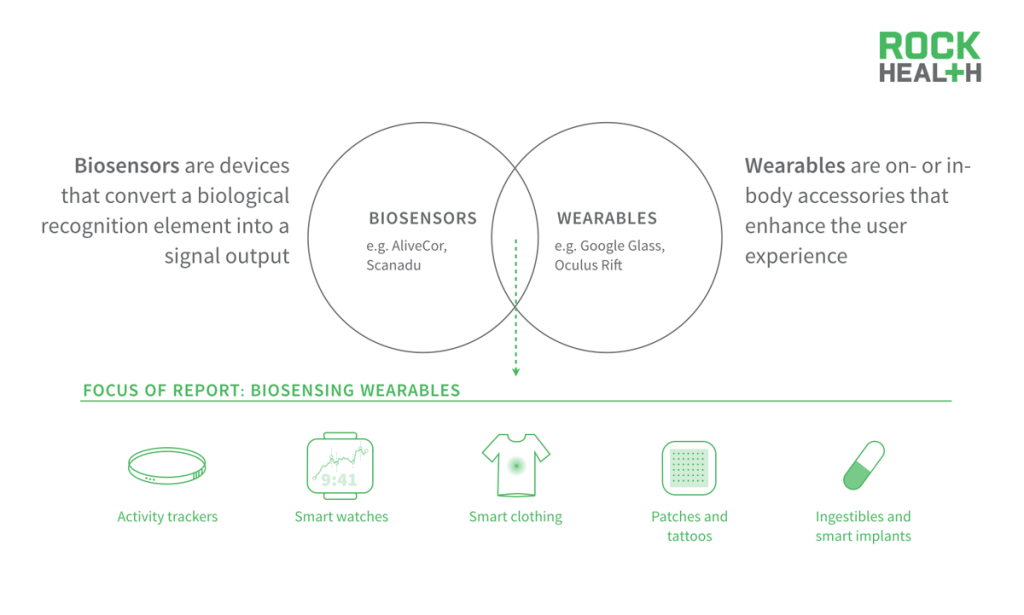

Biosensing wearables allow continuous physiological monitoring in a wide range of form factors.

Today there are an overwhelming number of trending wearables, but not all of them are capable of measuring or telling us something about our health. Similarly, there are plenty of biosensors that measure physiological inputs but do not have a wearable form factor. That’s why biosensing wearables are exciting: they allow for continuous physiological monitoring in a wide range of wearable form factors.

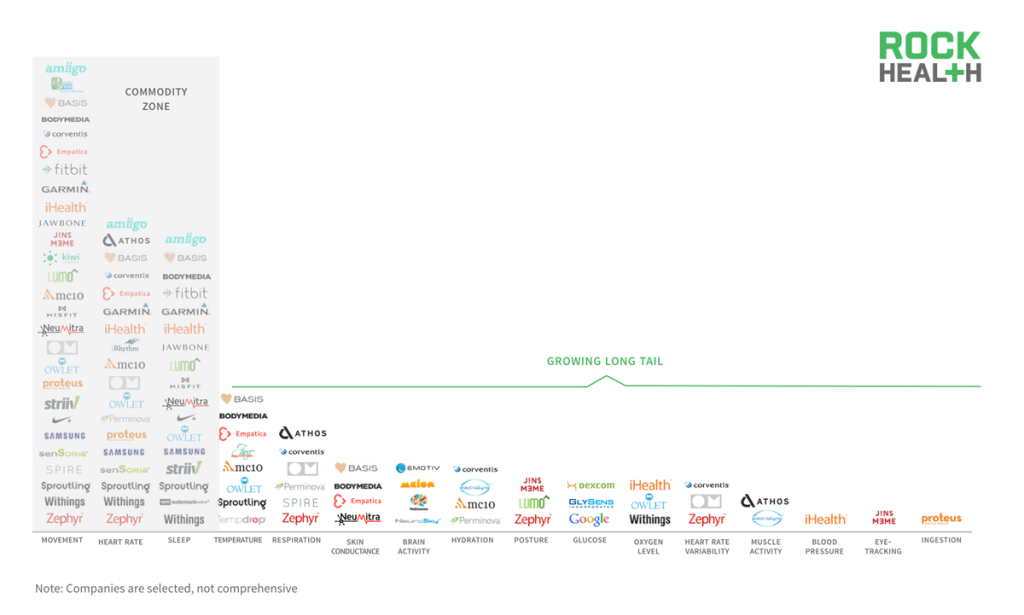

A wide range of products have emerged or are being developed in the category, covering numerous aspects of human physiology.

Source: Rock Health review of marketing for 75+ companies

It’s a crowded market, with an abundance of companies tracking movement, heart rate, and sleep. These physiological metrics have essentially become commoditized features and companies are distinguishing themselves in tracking more novel metrics.

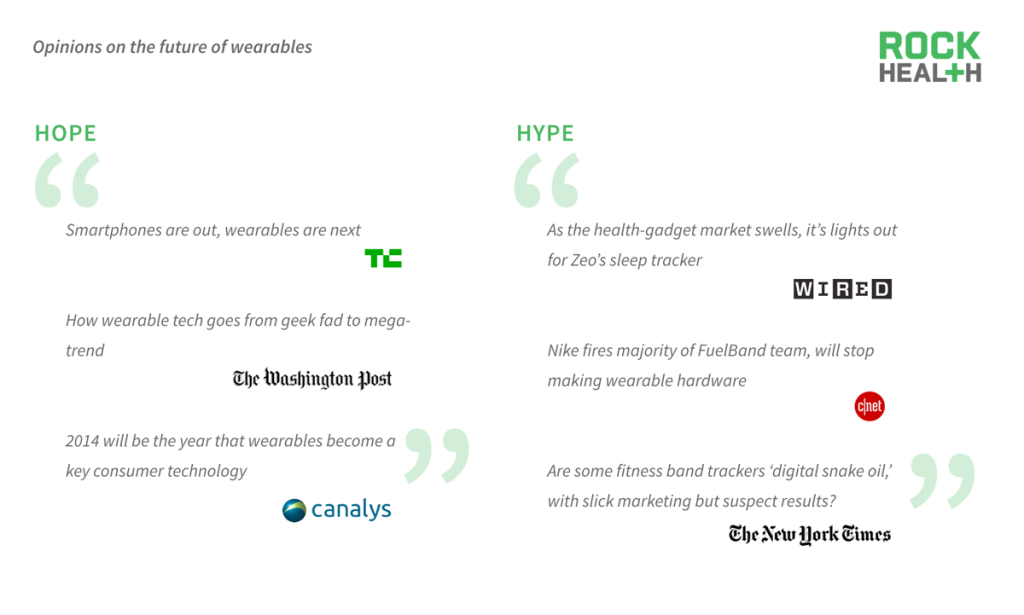

Opinions on the future of the category are decidedly mixed, with a tremendous amount of hype mixed with failure.

Source: News stories, Twitter

While the activity tracker segment has about 1-2% U.S. penetration, wearables overall are expected to grow significantly.

Source: Respective company sites

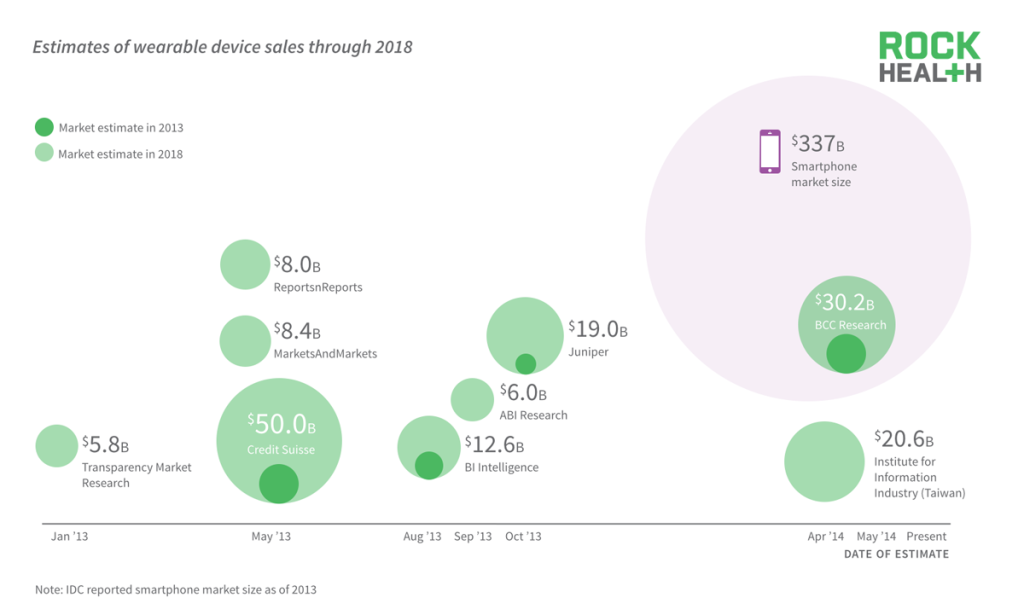

Market analysts are excited about the future of the wearables market, with estimates ranging from $5.8B to $50B. For context the smartphone market is $337B.

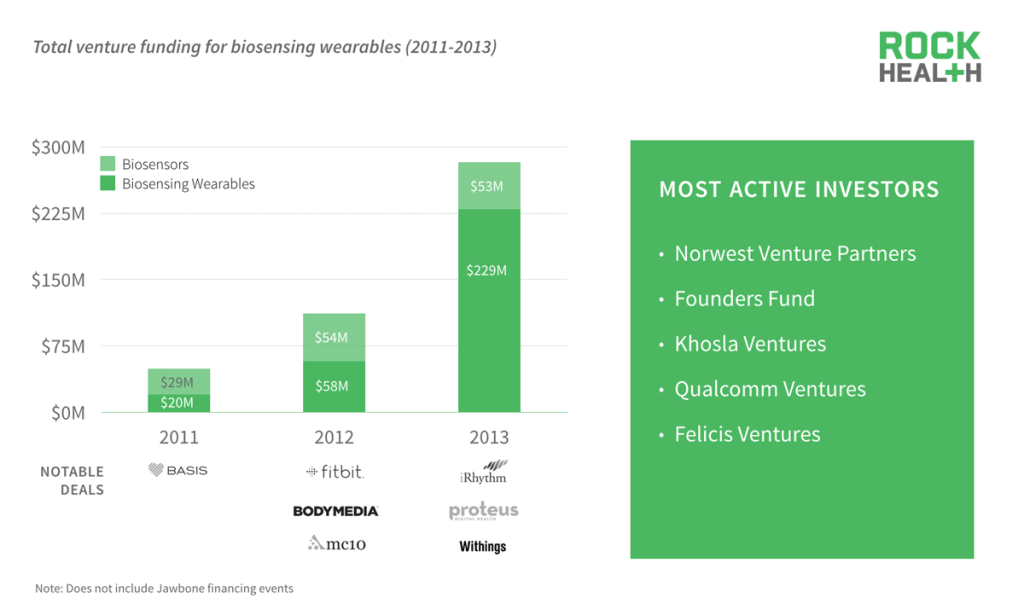

Venture capitalists are also betting on the space, with venture funding up over 5X since 2011.

Source: Rock Health Funding Database

It’s interesting to note the active investor list ranged from early to late-stage investors, with or without a healthcare focus. Investment theses were diversified from more traditional medical device products to consumer products trying to get sold on Apple shelves.

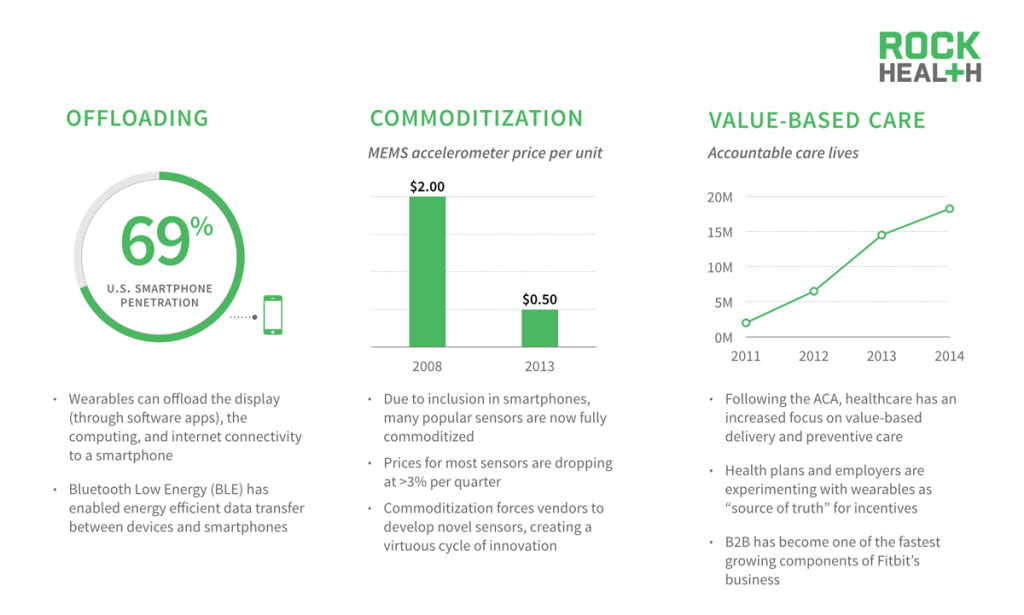

The scale and utility of smartphones, in addition to a dramatic shift in healthcare, has catalyzed the space.

Source: Smartphone penetration from Comscore as of March 2014; MEMS accelerometer pricing from supply chain sources; ACO penetration from Leavitt Partners

Smartphone penetration in the US has reached over 69%. With smartphones in the pockets of most Americans, this has allowed wearable device makers to rely on smartphones for display, computing, and internet connectivity. As smartphone demand grows, many internal sensors have become fully commoditized, significantly driving the price down.

Specifically in the US market, the growing emphasis on value-based delivery and preventative care provides wearables the opportunity to act as “source of truth” for incentives. Enterprise customers are turning to wearables to encourage general wellness, evidenced by the growing importance of Fitbit’s B2B sales.

The ground has to be fertile for the seeds to grow—innovative technology in wearables and biosensors can be both economically- and functionally-sound because it leverages the trillions of dollars that have already gone into that space. Once the technology lines up, utility will come from people knowing how to use the devices. Healthcare is the biggest and most persistent opportunity and will ultimately define the market.

Biosensing wearable products being created today could not have existed even three years ago.

Source: Product and app rendering courtesy of Spire, Inc.

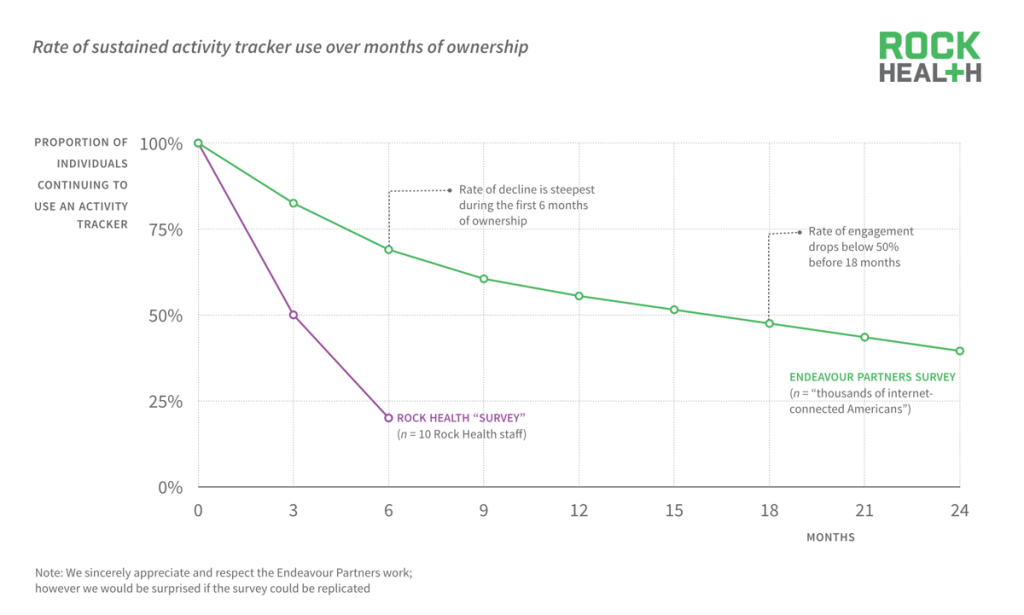

Despite such advancement, wearable products today fail to engage users over meaningful periods of time.

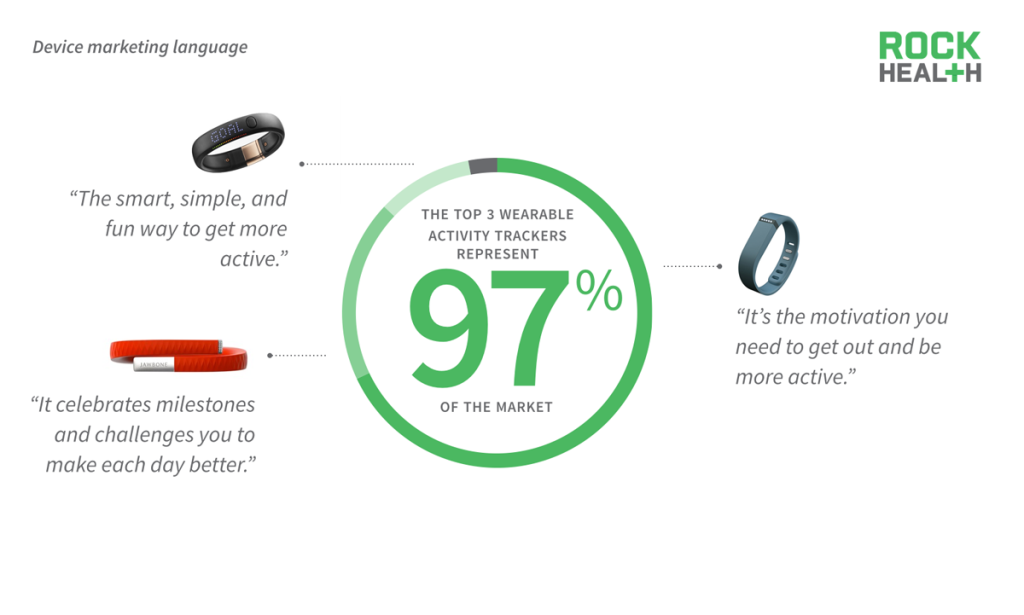

The generic marketing language of most devices leaves use cases to the purchaser’s imagination.

Source: Market share from NPD point-of-sale data (January 2013-January 2014); marketing copy from company websites (May 2014)

Fitbit, Jawbone Up, and Nike Fuelband captured 97% of the market, yet even these dominant market leaders were unable to send clear use case marketing messages.

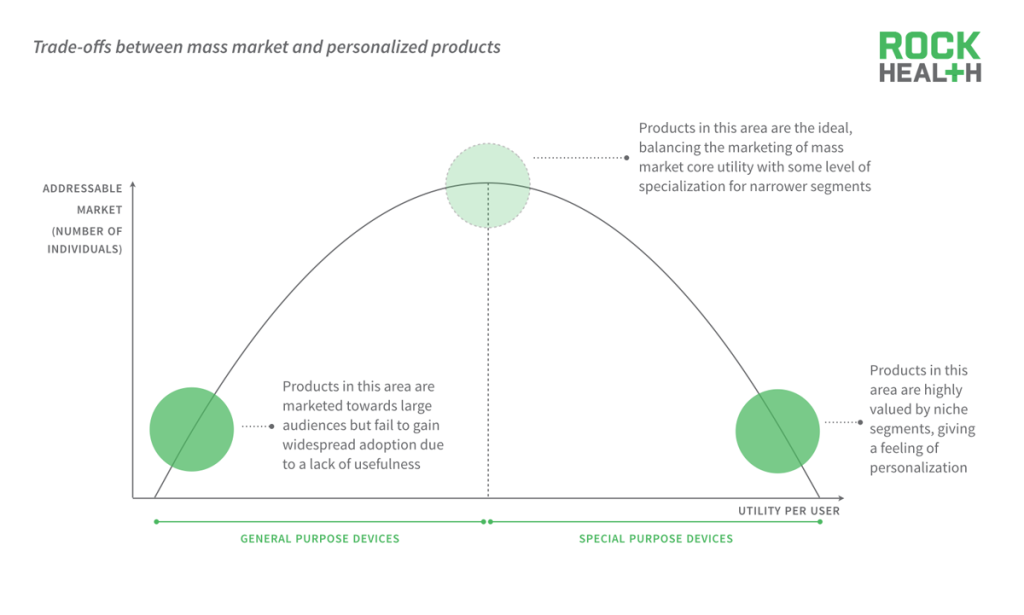

All companies face product marketing challenges when making the trade-off between mass and niche markets.

Biosensing wearables are in a paradoxical product market where there is a constant trade-off between utility and addressable market. Products that are generic, low utility don’t provide enough value to users but products that specialized, high utility are too personalized for the majority of the market. The ideal position would require a decent degree of utility, but not be too specialized, in order to cater to the largest possible market.

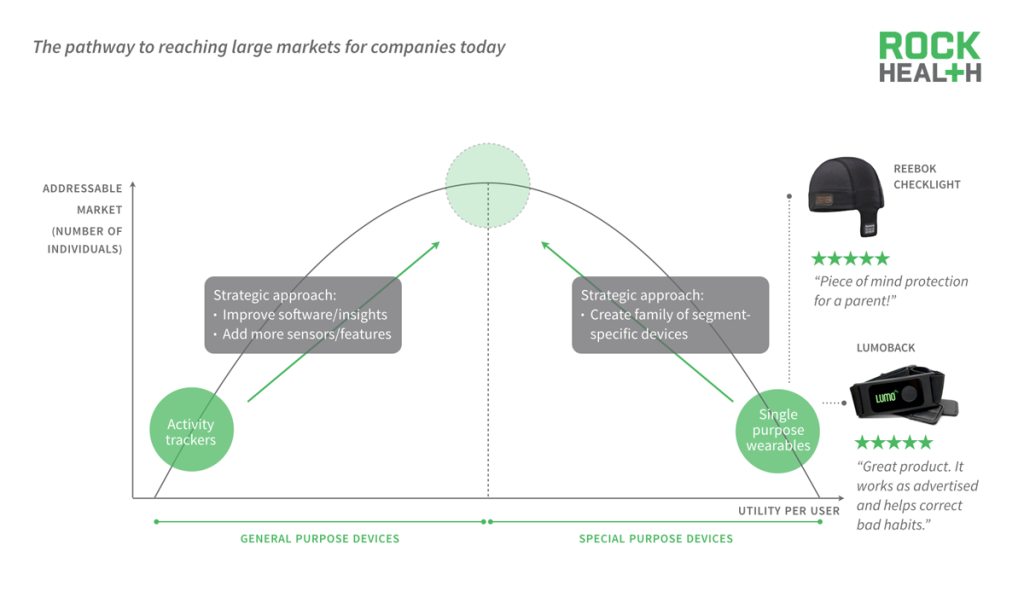

For most activity trackers, the lack of utility and failure of product marketing have made it difficult to scale and meaningfully engage.

Source: Reviews from Amazon.com and Reebok websites

As activity trackers become commoditized, companies have turned to improved software, additional sensors and features to appeal to a larger market audience. On the other hand, biosensing wearables that provided high utility by being single purpose are looking to expand their suite of products to capture more of the market.

Innovation for use case is important. Right now, everyone is just using off-the-shelf technology so they can only go after things that are obvious, like counting steps and heart beats. In order to provide something more meaningful, it’s important to design a product that has a specific utility. Then you can stand behind it and say to somebody, ‘This is how I’m going to help you.’

Axes of Innovation

In order to scale beyond early adopters, biosensing wearables will need to innovate along three axes.

In order to combat low engagement rates and scale beyond early adopters, we identified three axes—functionality, reliability, and convenience—on which companies should innovate in order to provide consumers with high utility. In a world where screens and devices are competing for a consumer’s time, it is crucial for a biosensing wearables to be convenient and seamless. But beyond reducing friction for engagement, if little to no utility is extracted from the biosensing wearable, consumers will continue to leave the devices at the back of their desk drawers. Additionally, increased competition makes data and device reliability more important than ever before. The more accurate and valid the data collection, the greater utility a device can offer. If biosensing wearables can emerge at the intersection of these three axis of innovations, companies will be able to provide high utility to a large market.

Functionality determines a biosensing wearable’s potential utility to an end user, whether a consumer or healthcare professional.

Source: Company website

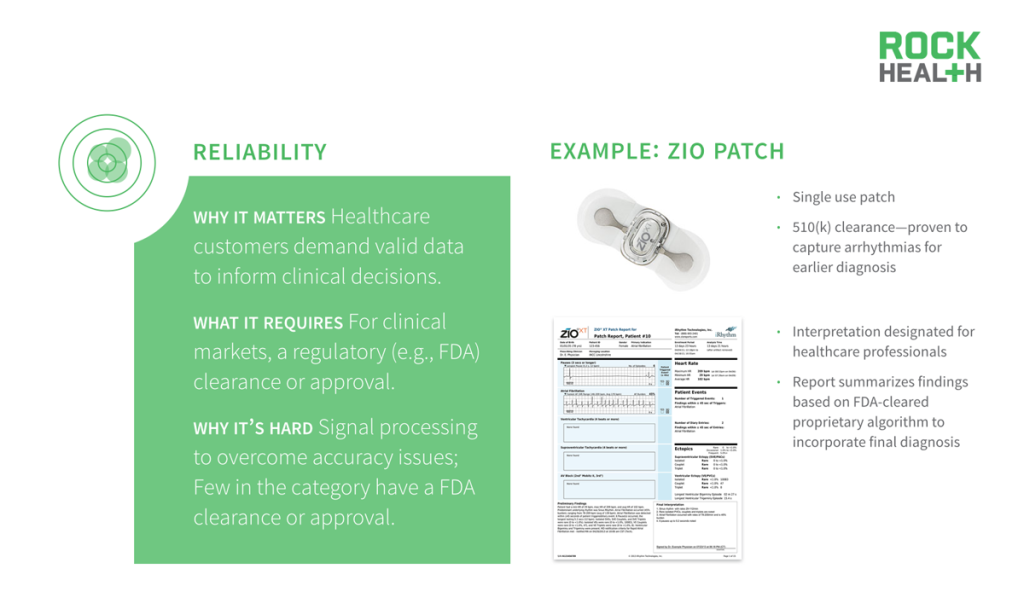

Reliability influences the addressable segments due to the unique constraints of operating in a healthcare environment

Source: Company website and FDA

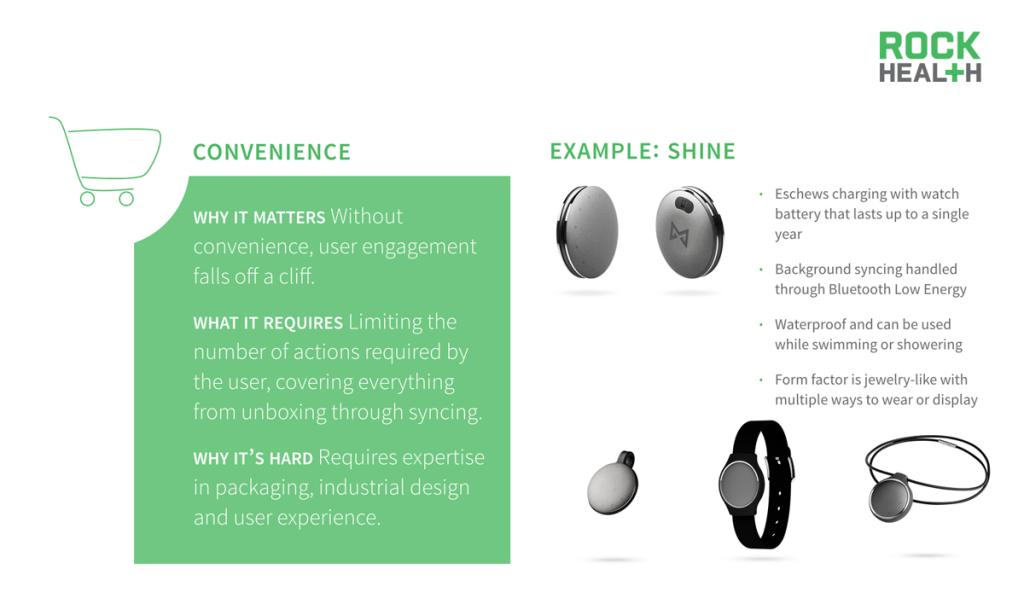

Finally, convenience plays a significant role in engagement with biosensing wearables, particularly at the onset of use.

Source: Company website

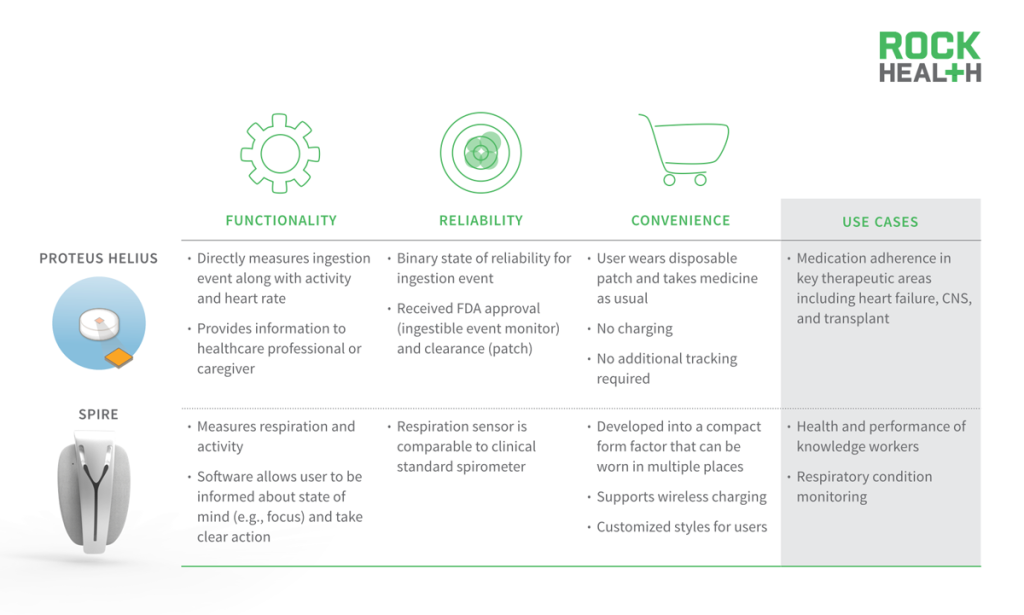

First products from Proteus and Spire demonstrate how innovating along all three axes leads to high utility.

Source: Proteus website; Spire website

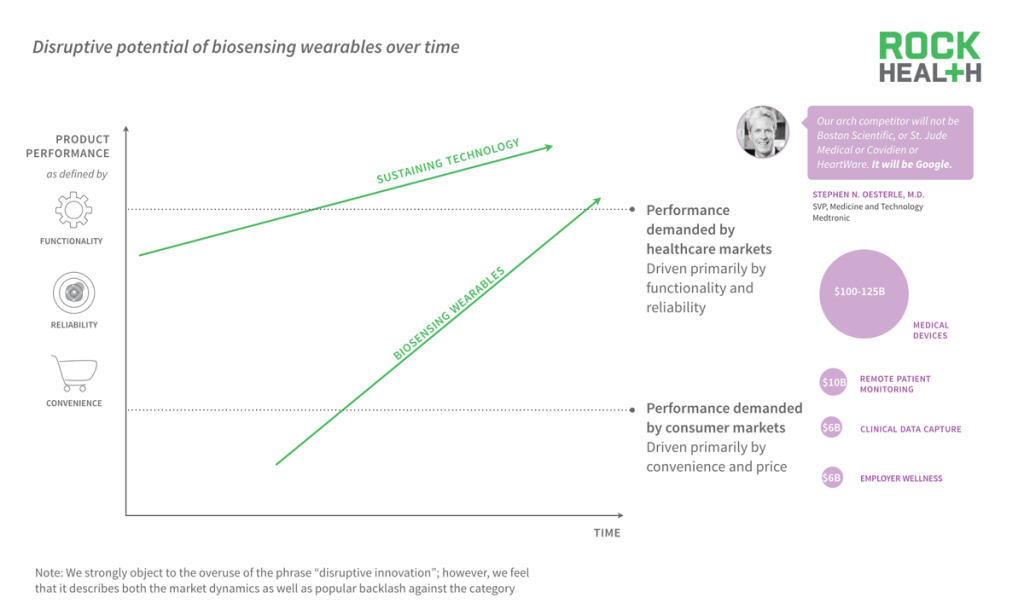

Biosensing wearables that evolve along the three key axes have the potential to disrupt large healthcare markets.

As biosensing wearables advance across all these three axes, there is significant potential to disrupt traditional medical device markets as they pursue sustaining innovation. Today, the medical device companies are able to distinguish their products based on functionality and reliability. The performance demanded by consumer markets initially require lower functionality and reliability, instead focusing on convenience and price. However, as the market becomes more competitive and companies eye the lucrative healthcare markets, they will continue to innovate and eventually create products that meet the demands of the traditional healthcare markets.

AgaMatrix was medical, medical, medical for 7-8 years. What we realized was that we had so much difficulty trying to rapidly update our apps. With Misfit, we thought we would go to the consumer first, test, learn a lot, iterate over and over again, and then hit the healthcare market.

Platforms and business models

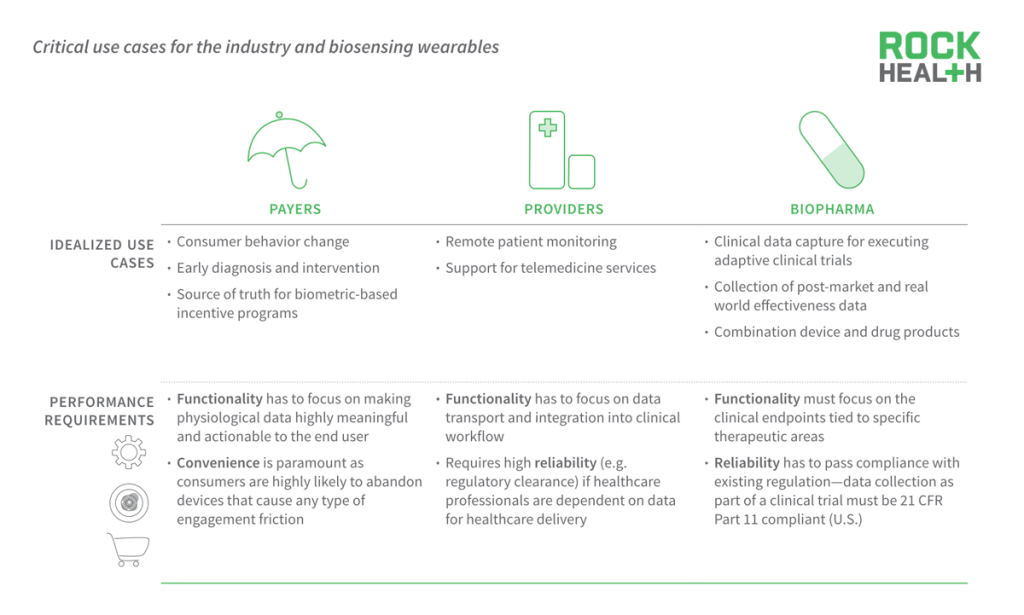

Evolved biosensing wearables will solve significant problems for the healthcare industry.

All industry stakeholders—payers, providers, and biopharma—could greatly benefit from the development of biosensing wearables. There are many use cases for the industry, all of which are aiming to improve outcomes and reduce costs.

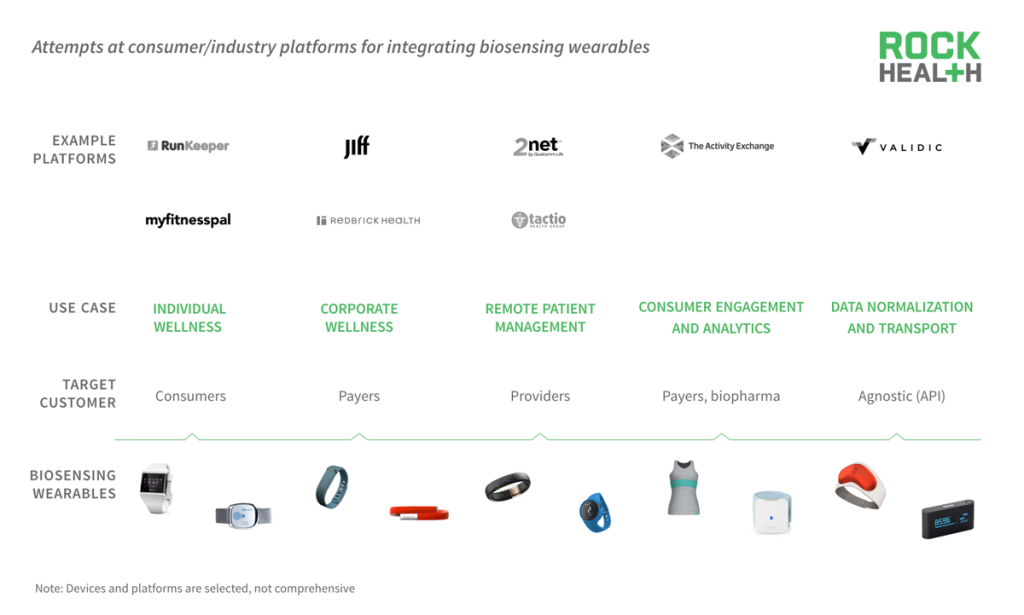

Multiple companies have emerged in an attempt to enable these use cases, although none are close to becoming scaled platforms.

Industry players don’t want to make the bet and tie themselves to one wearable device; thus, many companies have emerged to try and become the platform. While a few data aggregators have attempted to become the platform that increases data liquidity, we seem to have simply built more fragmentation on top of the universe of devices. And companies are platform shopping, weakening the scale of any one data transport solution. As a result, these platforms are becoming niche players that serve silos of the industry (i.e., individual wellness, corporate wellness, consumer engagement)

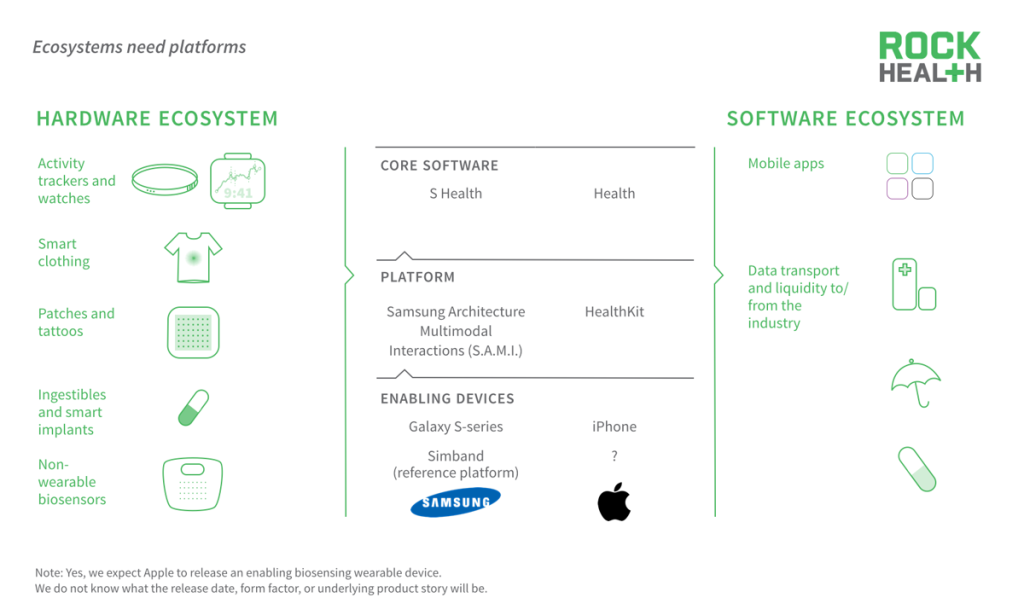

Wearable makers and end customers are both heavily platform shopping, limiting scale and leaving an opening for tech giants.

Currently, most biosensing wearable companies are responsible for both the hardware and software components of their product, which has created a siloed ecosystem. It can be daunting for a startup team to master the entire stack, but with tech giants entering the space, there may be a fix sooner rather than later.

Both Apple and Samsung have announced health platforms designed to capitalize on their existing consumer scale to attract industry players. If there is a successful scaled platform, this can help overcome the current software challenges associated with fragmentation.

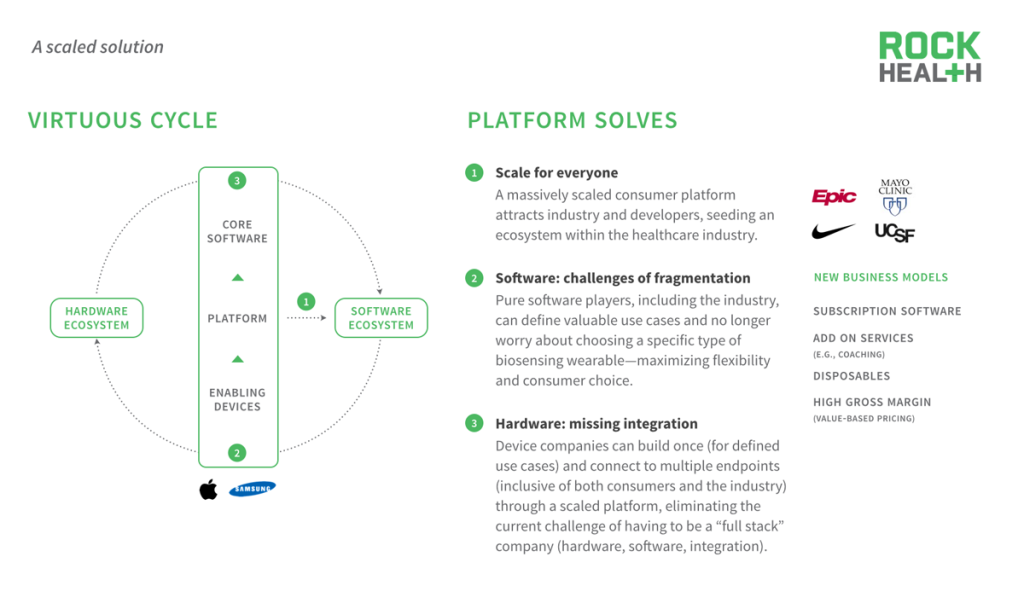

Pure software players could define valuable use cases without worrying about choosing a specific type of biosensing wearable. Similarly, hardware companies could build for a specific use case and be able to connect to multiple endpoints through the scaled platform, thereby eliminating the current challenge of having to be a “full stack” company (owning and being exceptional at hardware, software, and integration).

Starting from a scaled platform could catalyze a virtuous cycle, enabling new business models for wearable companies.

A scaled-platform could catalyze the space in a way that the current data aggregators haven’t been able to. With scale, the platform solves the problem of attracting the industry and developers. This helps software players overcome fragmentation challenges since they can develop and define valuable use cases without having to worry about being tied to a specific wearable. Similarly, device companies can focus on building hardware and leverage scaled-platforms for integration. Scale could enable entire new business models for companies.

We’re at the beginning of a long journey with biosensing wearables.

Characteristics of disruptive businesses, at least in their initial stages, can include: lower gross margins, smaller target markets, and simpler products and services that may not appear as attractive as existing solutions when compared against traditional performance metrics.

Acknowledgements

We are indebted to our industry partners who not only support our work every day but provided invaluable feedback on an early draft of this report.

A number of industry, startup and venture folks also offered their expertise. Special thanks to Aaron Duran, Ingo Elfering, Sridhar Iyengar, Amar Kendale, David O’Reilly, Jonathan Palley, and Sundeep Peechu for their time and insights.

Finally, we are fortunate to work with the most talented (and fun) team in digital health. Thanks to Halle Tecco and Mollie McDowell for reviewing our final drafts and providing edits.