A whole person view of obesity care: Staying competitive in an evolving market

New weight loss medications are transforming the standard of care in obesity treatment. With an average weight loss of 15% total body weight, a new class of drugs known as GLP-1s (which includes Novo Nordisk’s Wegovy) are targeting the rising incidence of obesity and achieving remarkable results.

While the promise of GLP-1s may be transformative, they’re not a silver bullet. Drug shortages, side effects and weight regain after medication withdrawal, coupled with the overarching complexity of the disease (including nuanced psychological and socioeconomic factors) highlight the importance of a comprehensive and multimodal approach to obesity care. With offerings across virtual care, remote monitoring, and novel testing, digital health provides solutions that can lead to a sustainable standard of obesity care.

These twin innovation cycles of GLP-1 development and digital health innovation for obesity care parallel many dynamics we see in the interplay between medications and digital solutions. As new therapeutics influence the standard of obesity care, we’re tracking the role digital health plays—and what leaders should keep an eye on to maintain a competitive edge as the market evolves.

Medication-assisted weight loss grows as an obesity care market opportunity

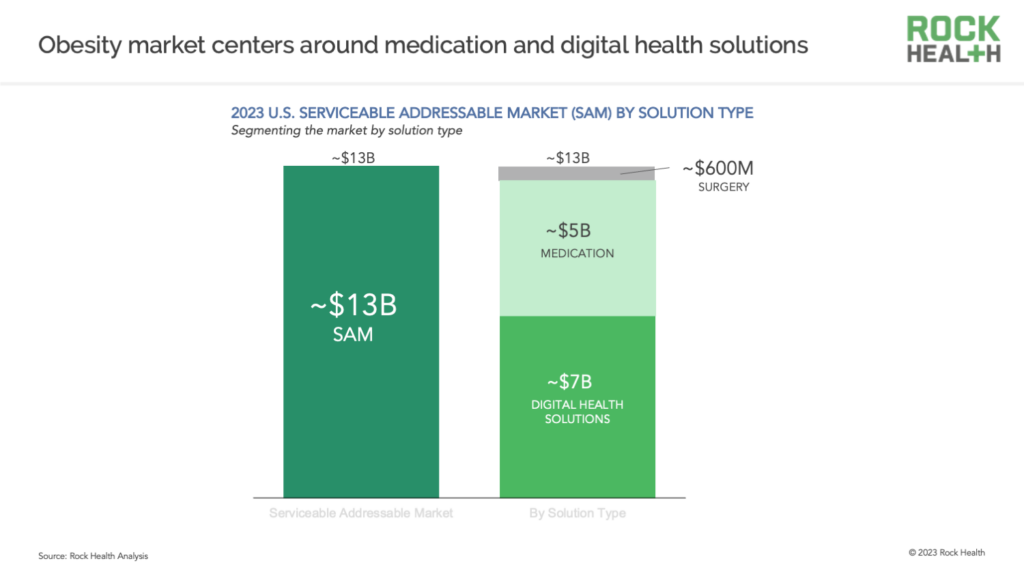

Obesity has been a long-time public health issue, which the AMA declared a disease in 2013. With the introduction of new and emerging obesity medications like semaglutide (Wegovy) and tirzepatide (Mounjaro), major progress is anticipated on substantially treating the disease—and the market opportunity has grown. Inclusive of the new medications, Rock Health estimates that the serviceable obesity care market hovers around $13B in the US. Medication for obesity care makes up a large portion of the market at 40%—and it’s expected to increase as more drugs are approved (beyond the six FDA-approved weight loss drugs) and insurance coverage is expanded. Digital health solutions, which include digital weight management tools focused on disease prevention as well as obesity-focused behavior change tools, make up a burgeoning 55%. While rates of bariatric surgery have increased over the years, it remains a smaller portion of the market at 5%.

Some estimates suggest that the obesity care market may grow to as much as $54B by 2030, assuming access to medication-led treatment expands. Digital solutions with and without a medication component are key to that expansion and play a role in increasing access to scalable and sustainable care.

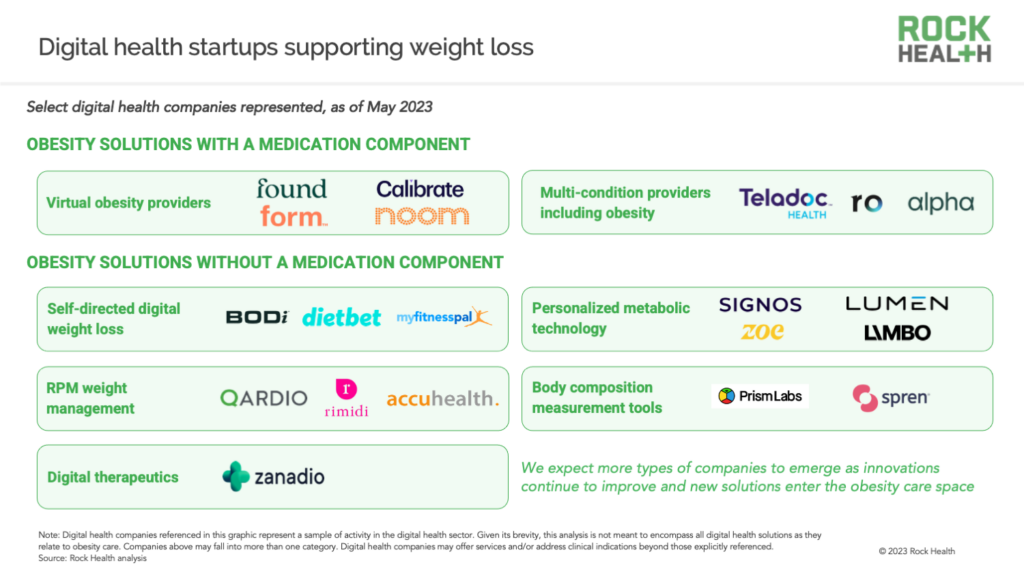

Digital health solutions offering medication-assisted weight loss

Technology can expand access to treatment in a variety of ways, and virtual care players are choosing different strategies to engage with therapeutic innovation in weight loss. Some are expanding beyond their core conditions to launch new obesity-focused programs. For example, companies like Teladoc and Ro are stepping into the ring with new weight loss offerings and prescribing capabilities.

Virtual obesity care solutions primarily rooted in behavior change—like Found, Calibrate, and Noom—are also building on their offerings by adding new prescription service lines.

Digital health solutions addressing obesity without a medication component

Others are thinking about the role non-medication solutions can play in weight management. Many digital solutions focus on behavior change as a means for weight loss. These apps can play a role as a first-line of treatment, or alongside medications to sustain weight loss. These self-directed weight management apps have come a long way, with companies focusing on whole-person health and even self esteem, like BODi, which calls itself the “health esteem platform.” Other apps are tapping into creative ways to support users on their weight loss journeys—like DietBet’s online community weight challenges.

Beyond traditional apps, a growing cohort of companies is focused on a personalized approach to weight management, using metabolic testing and glucose monitoring to inform individual treatment plans. Other companies are incorporating body composition measurements, such as Prism Lab’s (previously Naked Labs) body mapping and Spren’s smart mirror, to target precise care recommendations.

Remote monitoring companies like Qardio and Rimidi are also making strides in the weight management space as well by tracking weight via smart scales and aggregating data to screen for risk factors. These technologies can be used alongside medications to stratify appropriate care and monitor adherence.

"The outcome here is beyond weight loss. Everything you read now is about losing x % of weight. The impact should be measured by reduction in comorbidities and/or improvement in health, together with a reduction in total cost of care.”

Some companies look to offer alternatives to medication

Given the complexity of obesity, not all patients may be eligible or comfortable taking medication—especially given the possible side effects. Plus, the cost of the new weight loss drugs adds further challenges. Even if patients are eligible for the medications, insurers may not cover it.

Many employers and payers already require “step therapy,” a system where patients must start with a cheaper drug first before switching to a higher-cost alternative if necessary. As patients face restrictions on coverage of the expensive new weight loss medications, chronic care companies like Virta and Omada are tapping into the step therapy model to offer behavior change as the first line of treatment, support patients in adopting behavior change while on weight loss medications and even help people stop taking the drugs after a period of time, or avoid GLP-1s completely.

Other digital health companies are also refraining from jumping on the medication bandwagon. In particular, given the success of Zanadio, a smartphone app developed to provide a digital and multimodal treatment for patients diagnosed with obesity, we anticipate a growing segment of digital therapeutics to come to market as payers, providers, and patients look for affordable and sustainable care methods.

As new medications emerge and technology improves, the obesity care market will continue to evolve.

Here’s what you need to maintain your competitive edge

1. Create a comprehensive and personalized approach

Given the complexity of the disease, obesity care requires a comprehensive approach. Research supports a multimodal obesity care plan, which digital health can enable through virtual care, behavior change, and monitoring technologies. Plus, we may see companies bring in genetic variant analyses, real-time metabolic health monitoring, and other personalized testing to further pursue a curated approach to care. Successful companies will combine multiple, personalized treatment modalities and stay engaged with patients as they embark on their care journeys.

2. Design for health equity

For many, the prices of the novel obesity medications are out-of-reach. And the people who need these medications the most will likely have the hardest time accessing them given vast inequities in obesity rates across socioeconomic status and race. Digital solutions have the potential to help bridge the gap on access to obesity care, as virtual care can increase access to a short supply of obesity specialists. However, this doesn’t solve other issues around medication access and cost. As obesity care programs are built and iterated, stakeholders must intentionally design for and account for these barriers to ensure treatment is reaching the patients who need it most.

The novel obesity medications are exactly that—they’re new, and there is still much to learn about long term effects. Capturing real world evidence will be key as researchers track the long term effects for patients. Insights from data captured through remote monitoring and wearables will continue to catapult the industry forward by offering improvements to treatment designs and enabling providers to personalize patient care. And the potential of these medications goes beyond weight loss—studies have already begun to explore the potential for GLP-1 to improve cancer immunology and the impact of semaglutide on heart disease and stroke.

Looking ahead

Staying competitive in the rapidly evolving obesity care market requires a thoughtful digital health strategy—to learn more about navigating the opportunities and challenges, reach out to advisory@rockhealth.com.