H1 2023 digital health funding: A Brave New (lower funding) World

At the end of 2022, we noted that digital health was leaving one funding cycle for the next. H1 2023 has firmly rooted us in the beginnings of this new era—with all of its pains and potential. Fewer deals, lower check sizes, and a smaller cohort of sector investors are the new normal.

Though a new status quo has been established, founders, investors, and healthcare innovators are in different stages of acceptance and adjustment. Some startups are avoiding the inevitable (down rounds) by pursuing unlabeled raises. Digital health’s seasoned investors are rushing to crown the next class of household-name startups. And some companies are making the tough decision to sunset their businesses; yet, their assets may live on as tuck-in acquisitions or relaunched products.

The beginning of anything new can feel overwhelming and uncharted, but H1 2023’s funding data is already surfacing signals of what lies ahead for digital health innovation. Read on for a breakdown of the funding numbers and what we see coming up on the horizon.

H1 2023: Firmly rooted in a new market cycle

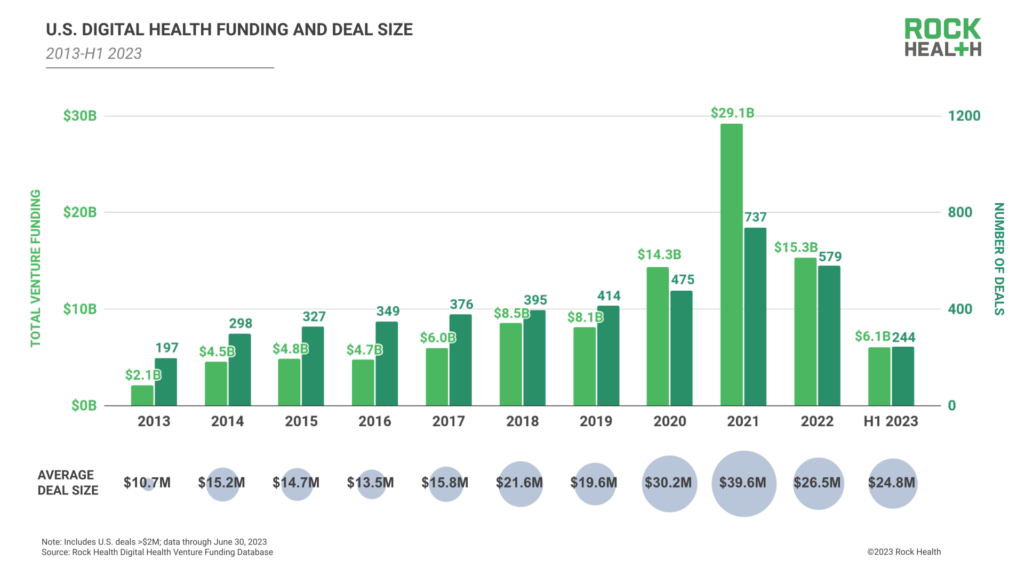

In the first six months of 2023, U.S. digital health startups raised $6.1B across 244 deals, with an average deal size of $24.8M. Compared to Q1 2023 ($3.5B over 131 deals), Q2 registered only $2.5B in funding across 113 deals—joining Q3 and Q4 2022 as recent sub-$3B quarters. Should H2 2023 funding continue at the rate of H1, we’re on track for the lowest funding year since 2019 (a possibility we predicted at the outset of this year).

Alongside lower funding totals, H1 2023 also saw a continued trend of fewer investors participating in digital health deals. 555 investors participated in digital health fundraises in H1 2023, down from 775 in H1 2022 and 832 in H1 2021.1,2 Additionally, 71% of H1 2023’s dealmakers were repeat digital health investors.3 To us, this signals that generalist and crossover investors are moving away from one-off participation, leaving a smaller group of focused digital health investors to lead sector activity

Each of these signals confirms that we are quite firmly rooted in the beginnings of the next funding cycle in digital health—smaller total funding numbers, lower deal volume, and a more concentrated cohort of investors. New beginnings typically come with new challenges, however, and startups are now tasked with acclimating to their new environment.

The startup ride back to reality

While the “writing on the wall” has been clear for the past several quarters, many digital health startups are still navigating a shift from the prior funding environment to the present day. For most founders, the challenge is how to bring in new capital without 1) severely crunching previously-established valuations, and 2) incurring bad PR associated with a down round or a smaller-than-expected lettered raise (e.g., Series B, Series C).

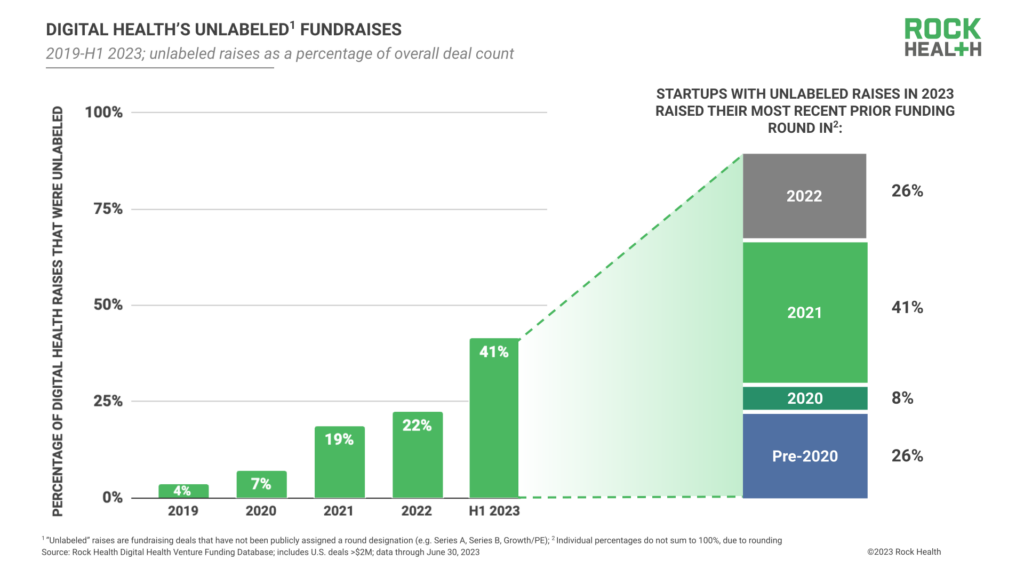

Enter the “unlabeled raise.” To try and delay valuation haircuts, many digital health players have raised capital without publicly attaching labels to weaker rounds. In fact, a staggering 41% of H1 2023’s digital health funding deals (101 of 244) were not publicly labeled with a series or round label. This is the highest proportion of unlabeled raises since we began tracking sector funding in 2011.

Notably, most of H1 2023’s unlabeled deals were raised by startups that had previously raised an early-stage round (12 unlabeled deals were raised by startups that most recently closed their Seed rounds; 14 by startups that most recently closed Series A; and 11 by startups that most recently closed Series B). For many in this cohort, these preceding early-stage rounds were raised in late 2021 or early 2022—aka the tail end of “boom times.” Since Q3 2021, we’ve signaled that startups that raised their early stage rounds in 2021 were likely to be at risk of valuation crunch in the future. Two years later, their growth metrics or commercial traction may not qualify them for a full-fledged labeled fundraise at a markup in today’s environment.

Unlabeled raises are one way for startups to protect their prior valuations while they continue to make progress, but they’re a battlefield tactic, not a long-term strategy. The new funding climate has a low tolerance for 2021-inflated valuations, and startup operators that reset valuations to match sustainable profitability and growth targets now may ultimately be better positioned for success with investors—and possible acquirers—in the long run.

(Some) investors are confident, making big bets in a high stakes market

While some startups are trying to wait out the shifting tides of the market, digital health’s (now smaller) group of active investors is diving in headfirst, doubling down on companies—via mega deal raises—that they see as especially promising.

“In this market, we are seeing true differentiation between the startups that are shining and those that are failing. Cash availability from 2021 to early 2022 may have made that differentiation harder to see, but it was always there.”

— Alyssa Reisner, Lead Director & Investment Principal, CVS Health Ventures

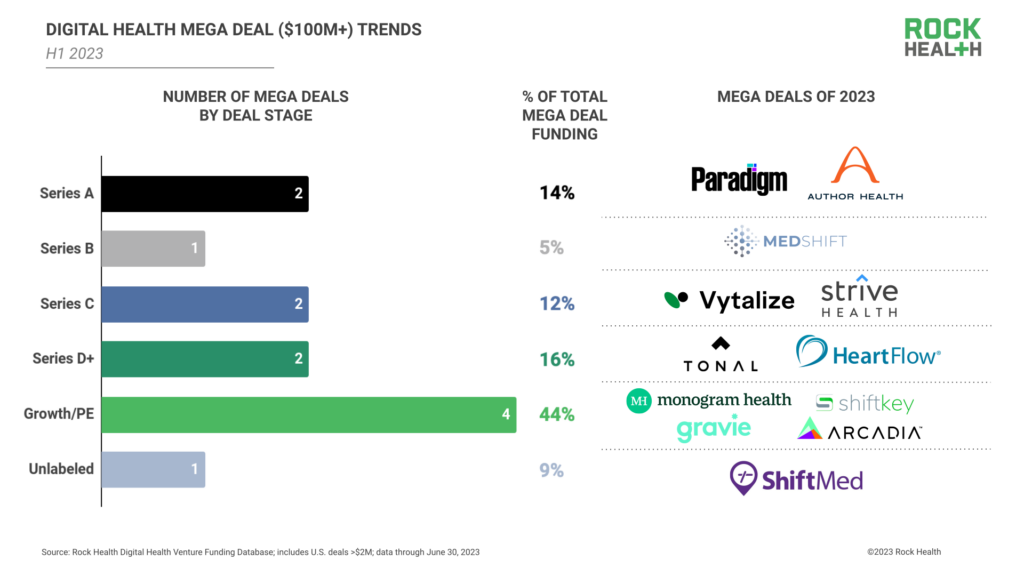

Despite the overall low funding climate, H1 2023 clocked 12 mega deals comprising 37% of total funding dollars—and H1’s mega deals were almost as large as that of prior years. The average mega deal check size came in at a whopping $185M, nearly equal to the average mega deal size in blockbuster-year 2021 ($188M). Notably, these super-sized bets are happening at every deal stage. H1 2023 saw two mega deals at Series A, one at Series B, two at Series C, and six at Series D or higher.4,5 Also notably, many of H1 2023’s mega deals clustered around one of three digital health transformation areas: value-based care enablement (Strive Health; $166M, Arcadia; $125M, Vytalize Health; $100M); non-clinical workflow and practice management (Shiftkey; $300M, ShiftMed; $200M, MedShift; $108M); and at-home care (Author Health; $115M, Monogram Health; $375M).

H1 2023’s cluster of mega deals around promising innovation areas suggests to us that funders are going “all in” on companies that they feel have the right talent, technology, and market positioning to become the next digital health varsity team. And some investors are more involved than just writing checks. Increasingly, funders are incubating companies in hopes of securing a smoother road to product-market fit and commercial traction (clinical trial startup Paradigm was co-incubated by ARCH Venture Partners and General Catalyst, while kidney care player Monogram Health was incubated by Frist Cressey Ventures). Though incubated or co-designed startups aren’t new to 2023, we’re likely to see more of this activity as investors try out creative approaches to minimize risk.

While growing investor confidence is typically a welcome sign for founders, super-sized checks in an otherwise low-deal volume funding climate introduce a certain level of unpredictability into the market. For example, due to mega deals outlier raises, mean deal size exceeded the median by more than $20M across all deal stages in H1 2023. Deal size variability can make future capital availability hard to predict, intensifying uncertainty for investors, startups, and organizational collaborators alike. This irregularity is particularly salient now; the present funding climate is characterized by the highest variability in deal size (as measured by relative standard deviation) since 2018.6

Importantly, these investor-induced fundraising spikes carry the risk of perpetuating circular thinking in investment and innovation. Venture capital investors have historically tried to de-risk their funding activity by making many diversified bets. But today, some firms are managing broader market uncertainty by putting more of their eggs in select baskets—and sometimes participating in shaping those baskets themselves. To the extent that some investors double down with outsized bets on incubated, “de-risked” startups, their investments shift the overall fundraising landscape. This creates a circular pattern in which a few investors’ big bets inform and reinforce the investment market trends they’re betting on. Additionally, investor interest in a preferred class of startups may exacerbate funding challenges for diverse teams, especially first-time or underrepresented founders, as these innovators look to secure capital from a dwindling number of active investors with eyes set elsewhere.

What happens next: Startup acquisitions, sunsets, and asset sell-offs

Difficult paths to capital, coupled with a still-frozen IPO market (zero digital health exits so far in 2023), create the right conditions for startups to consider acquisition bids. Anecdotally, we’ve heard that some digital health startups today are rounding up acquisition offers, oftentimes alongside their VC term sheets, in order to put all the options on the table.

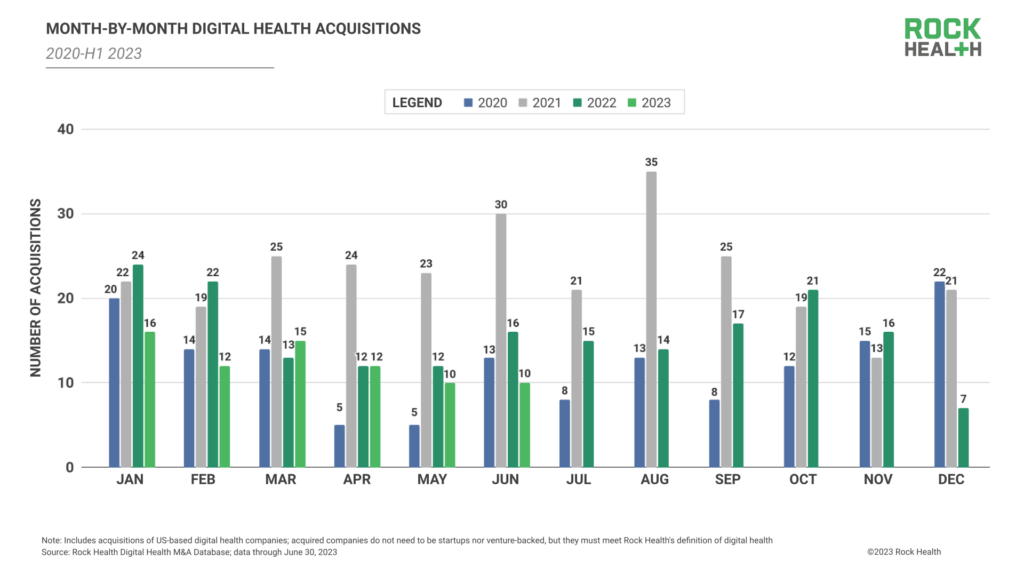

However, H1 2023 averaged just over 12 acquisitions of digital health startups each month, down from more than 15 M&A deals per month in 2022 and 14 M&A deals per month over the past five years. What’s keeping acquisitions low? It’s likely that, similar to H1 2023’s valuation crunch, startup teams are holding out on accepting acquisition offer bids that they see as lower than they might have received just a few quarters ago or even lower than the sum of their previous raises. Another hypothesis is that company acquisitions are happening but aren’t being announced publicly, especially if terms were less-than-ideal for the startup purchased.

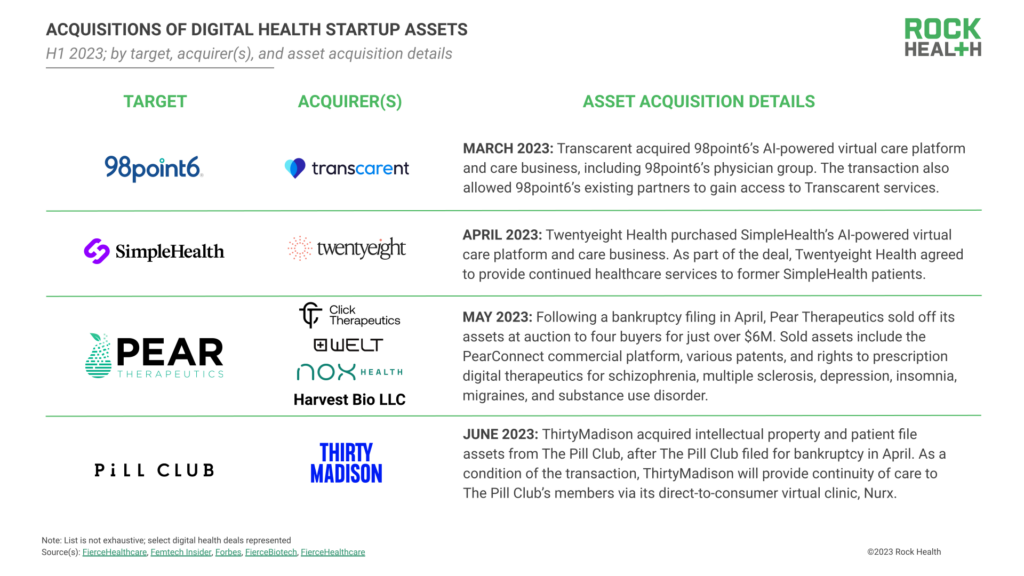

For companies that aren’t offered or interested in a purchase bid, the time may come to sell or sunset the business. Beyond the highly publicized bankruptcy of Pear Therapeutics, this half saw digital health startups including SimpleHealth, The Pill Club (also known for a select time as Favor), Hurdle, and Quil Health close their doors.

Sunsetting is hard for any digital health company—each closure is a difficult, deeply personal experience for those involved. Unfortunately, some of today’s startup attrition directly stems from the prior funding cycle; though 2020–2021’s fundraising climate of cheap money and eager investors sustained a wide range of startup businesses, 2023's climate eliminated any cushion for unsustainable burn rates or unclear paths to profitability. Not to mention, large health systems that signed contracts during the pandemic may be reconsidering or scrapping their arrangements, stripping some players of their most secure revenue sources and throwing cash flow into a tailspin.

Although the curtains may close for some digital health disruptors, other digital health startups are gaining second lives through asset acquisitions and relaunches. Pear’s prescription digital therapeutics (PDT) assets, for example, were distributed to four buyers, ranging from PDT market competitors to life science players to Pear’s former CEO himself. Each of these acquirers is expected to relaunch the purchased assets, either rebranded as standalone products or repackaged with other digital health products. More straightforward asset transfers include Twentyeight Health’s acquisition of SimpleHealth customers in the reproductive care and sexual wellness space, Transcarent’s purchase of 98point6’s AI-powered virtual care platform and care business, and ThirtyMadison’s purchase of the assets of online birth control clinic, The Pill Club (ThirtyMadison will provide continuity of care to The Pill Club’s members via its direct-to-consumer virtual clinic Nurx).

“We are operating in the mindset that the more we bring together complementary companies and capabilities that are bettering the overall care journey for all people, the market will see the value.”

— Snezana Mahon, Chief Operating Officer, Transcarent

Second lives are promising signals in an otherwise mixed-feelings environment. While individual startups may come and go, the intellectual property (IP) they create and the services they deliver to end-users can serve as vital additions to the next crop of startups and change-makers in digital health. For acquirers of folded startup assets, however, a high level of stewardship is required to successfully integrate new IP, services, or customers. With patient and consumer data changing hands and treatment programs hanging in the balance, the stakes have never been higher for seamless integration and continuance of high-value care delivery.

Toward a new world

Though any new environment can be overwhelming—and comes with its fair share of changes—we’re looking forward to the thoughtfulness that startups, investors, and innovators will bring to the table as they adjust from 2021’s funding climate to 2023’s. This reset stands to bring fresh and focused perspectives to digital health product development, partnerships and commercial approaches, as well as team-building. Though challenging, tough times can serve as a much-needed market correction, right-sizing innovator and investor expectations for a more steady and sustainable future.

Tap into insights and strategic guidance for enterprise companies with Rock Health Advisory.

Get in touch with the venture team at Rock Health Capital.

Join us in building a more equitable future at RockHealth.org.

And last but not least, stay plugged into the Rock Health community and all things digital health with the Rock Weekly.

Footnotes

- Participating investors refers to the number of unique investors who participated in at least one $2M+ investment round in a U.S.-based digital health company.

- Participating investor count has declined every half since H1 2021.

- Rock Health defines “repeat investors” as investors who have participated in at least one prior $2M+ investment round in a U.S.-based digital health company.

- These mega early-stage rounds aren’t just happening in the U.S. In June, Europe’s VC market logged its largest ever Seed raise at $113M.

- The stage of ShiftMed’s mega deal was not disclosed.

- H1 2023’s deal values had an RSD of 178% relative to the overall mean deal size ($24.8M). This means that data points (digital health deal sizes) within the sample (H1 2023) tend to be distributed at 178% (1.78x) the value of the mean ($24.8M ± $44.1M).