Q1 2017: Business as usual for digital health

When we started tracking deals in 2011, the newly enacted Affordable Care Act served as a major catalyst for market growth. Entrepreneurs leaped at the opportunity to wedge their new businesses into a changing healthcare landscape, aiming to serve the 30M newly insured Americans. We’ve only tracked digital health in an ACA-world, so we’ve been on the edge of our seats as the new administration vows to repeal this landmark reform.

While we don’t yet know how or when healthcare law will change, we have picked up on at least one externality of the legislative process: providers and health plans are delaying expenditures based on uncertainty.

“Lack of clarity on what is going to happen to ACA and other healthcare policy matters seems to have scared at least some portion of the hospital system customers into a sense of paralysis in terms of making decisions around bringing new HIT solutions.”

– Sam Brasch, Senior Managing Director, Kaiser Permanente Ventures

“We hear from fee-for-service hospitals and employers that they want to understand the regulatory framework before making substantial purchasing decisions.”

– Julie Papanek, Partner, Canaan Partners

However, founders remain cautiously optimistic and feel well positioned to navigate any regulatory changes.

“The most savvy healthcare purchasers know that digital patient engagement is table stakes for any type of environment (fee-for-service or alternative payment models). Providers must connect with and empower the patient to be successful. Our product enables this deep interaction, and we’ve actually seen an acceleration in client uptake rather than the sluggishness some expected under regulatory uncertainty.”

– Leah Sparks, Founder & CEO, Wildflower Health

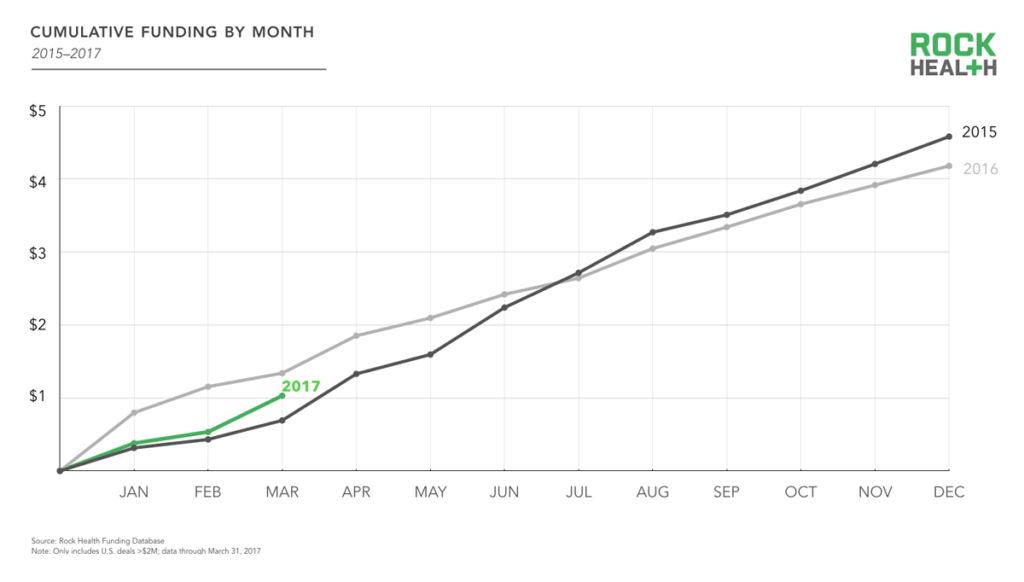

This quarter’s venture activity also reflects this optimism. In Q1, we counted 71 digital health deals totaling over $1B. Despite any regulatory uncertainty, it’s business as usual for digital health funding.

Source: Rock Health Funding Database

(As a reminder, Rock Health reports only US-based digital health deals of $2M or more. What’s not included? Healthcare services companies like Forward and Oscar, biotech/diagnostic companies like Grail or Theranos, and software companies like Zenefits and Reputation.com that are not solely focused on healthcare. We don’t report international companies like German-startup Clue, even though many of their users and funders are US-based. We also don’t include grant or government funding, non-dilutive crowdfunding, or venture deals under $2M. Why? By comprehensively tracking companies within clearly defined parameters, our longitudinal data is more accurate and telling.)

“I am surprised that the investment pace hasn’t waned in Q1. Political change has caused policy uncertainty. I would have expected all the turbulence in Washington DC to lead to a slowdown in investment activity.”

– Steve Kraus, Partner, Bessemer Venture Partners

Largest deals

Five deals over $50M were announced in Q1. Investors in these growth rounds were a mix of institutional VCs (KPCB, General Catalyst), corporate VCs (McKesson Ventures, Salesforce Ventures), and growth capital (Warburg Pincus, Goldman Sachs). The companies behind the five largest deals have various users, but not a single product charges the healthcare consumer. PatientsLikeMe, a patient community, monetizes by selling de-identifiable patient data to partner companies. Livongo Health, a B2B2C diabetes management platform, sells only to health plans and employers and not directly to the end user.

Source: Rock Health Funding Database

Themes

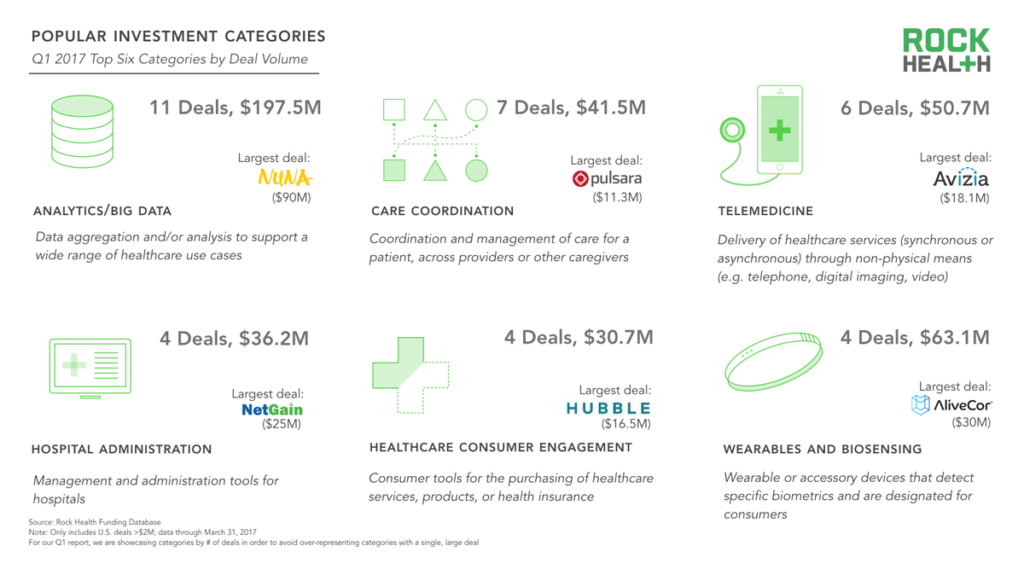

Nearly half of the deals in Q1 fell into six categories (see chart below). With the most dollars and most deals, the analytics and big data category included eleven startups—with Nuna Health bringing in nearly 46% of the total category funding.

Telemedicine, with six deals in Q1 totaling $50.7M, deserves recognition due to recent trends in legislation and reimbursement. Telemedicine reimbursement continues to evolve; in 2005 only 24 states allowed coverage of telemedicine, while in 2017 all 50 states “allow coverage of telemedicine to some degree,” according to a recent report. Legislative telemedicine developments from state to state will influence future investment in this category.

Source: Rock Health Funding Database. Note: For our Q1 report, we are showcasing categories by number of deals in order to avoid over-representing categories with a single, large deal.

M&A

We tracked nearly 20 M&A transactions in Q1, including these two notable acquisitions:

- CoverMyMeds was acquired by McKesson for a whopping $1.1B in cash, plus an additional $275M contingent upon CoverMyMeds’ meeting financial performance goals ending fiscal year 2019. This would make it the fourth largest digital health acquisition on record at nearly $1.4B. The Ohio-based startup was founded just nine years ago, and backed by Francisco Partners in 2014.

- Castlight Health acquired employee wellness platform Jiff for all-stock consideration of up to $135M. Jiff previously raised $68M from investors including Venrock, Aberdare Ventures, GE Ventures, Aeris Capital, and Rosemark Capital Group. Venrock was also an early investor in Castlight Health.

Although the following M&A deals reported undisclosed transaction amounts, these four acquisitions earned honorable mention. The locations are also noteworthy, as we see more transactions taking place outside of California.

- higi, a provider of retail health kiosks, acquired EveryMove. EveryMove is a rewards system for healthy behavior based in Seattle, Washington.

- Digital Pharmacist, the newly minted company formed by the RxWiki and TeleManager merger, made its first acquisition this quarter—buying up PocketRx, a mobile app for prescription refills. PocketRx is based in Shreveport, Louisiana and Digital Phamacist is based in Austin, Texas.

- TreatMD, a Miami, Florida-based, bootstrapped telemedicine company, was acquired by site-to-site telemedicine technology group GlobalMed (based in Scottsdale, Arizona).

- Zen Planner, a member management software company for gyms and sports clubs, was acquired by DAXKO (based in Birmingham, Atlanta). With 88 employees and 5,500 customers, Colorado-based Zen Planner was backed by a Series A in 2013 from Mainsail Partners.

Public markets

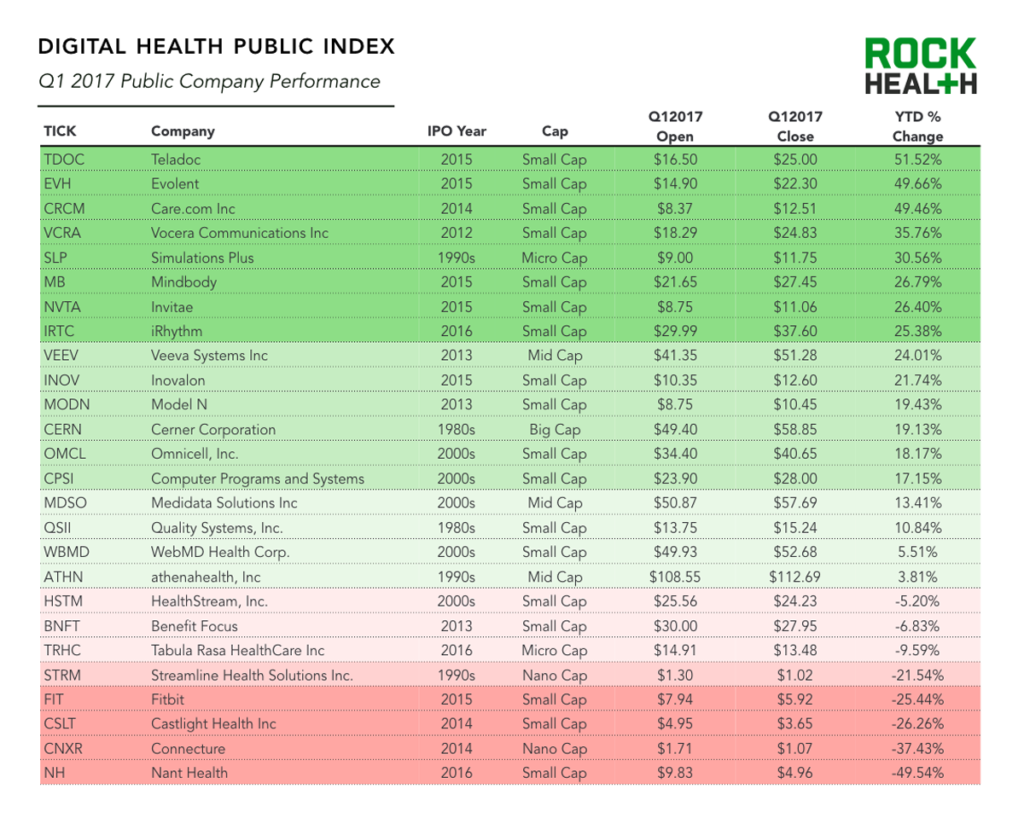

It’s been a strong quarter for the public markets overall, with the S&P 500 and Dow up 5.77% and 4.89%, respectively. The Digital Health Public Index (unweighted) is up 13% since the beginning of the year, with a majority of the companies generating a positive return over the quarter. The biggest digital health stock surge of Q1 was Teladoc, now trading at an all-time high (partly attributed to their March 1st earnings announcement that revenue was up 65.5% YoY).

Not all companies in the Digital Health Public Index are enjoying life in the public markets. Fitness wearable darling Fitbit currently trades 25% below its 2017 opening price and 70% below its 2015 IPO price, even though it is expected to sell $1.5B in devices in 2017. But no stock dropped this quarter as drastically as NantHealth, founded and led by physician billionaire Dr. Patrick Soon-Shiong. The stock price fell nearly 50% this quarter, after a STAT news article exposed questionable charitable giving used to bolster NantHealth’s topline.

Source: Rock Health Funding Database

With over 20 digital health companies that have raised $100M+ since 2011, we anticipate that more exits are on the horizon.

New funds

A slew of new digital health-friendly funds were announced in Q1, expanding the pool of capital for investors (and eventually startups) in digital health. We counted at least six new funds with over one billion dollars in capital:

- Venrock (Palo Alto, CA) raised $450M for its eighth fund. They are one of the most prolific digital health investors, with a portfolio including Doctor on Demand, Stride Health, and Virta (which are also Rock Health portfolio companies).

- Lux Capital (New York, NY) raised its fifth fund at $400M. The firm invests in emerging science and technology ventures. Current digital health portfolio companies include Aptible, Kyruus, and Zipdrug.

- New fund! Biomatics Capital (Seattle, WA) launched with $150M to invest in genomics and data-driven healthcare. The firm was started by two former Gates Foundation executives.

- New fund! Section 32 (San Diego, CA) is a $100M healthcare-focused venture fund reportedly being launched by Bill Maris, former CEO of Google Ventures.

- New fund! Spectrum Health (Grand Rapids, MI) is launching a $100M corporate VC arm to invest in technologies, products and services that improve patient health and drive down costs. Spectrum Health is a not-for-profit, integrated, managed care health care organization.

- New fund! Refactor Capital (San Francisco, CA) is a new $50M fund investing in startups tackling problems in “hard but not impossible” industries, like healthcare.

Summary

Business as usual for digital health It’s still early in the year, and deals take months to close (thus are a lagging indicator), but so far we aren’t seeing a downshift in digital health funding due to regulatory uncertainty. So far, 2017 digital health funding is shaping up to be on track with previous years (49% above Q1 2015 and 23% below Q1 2016). We hear that providers and health plans are delaying expenditures based on uncertainty, yet founders remain cautiously optimistic and feel well positioned for what comes next.

Major themes Going forward, healthcare leaders indicate that they will focus on controlling costs, investing in analytics to improve data integration, and increasing patient engagement and utilization of telemedicine. Not surprisingly, the popular investment categories of Q1 align with such ambitions. The top six themes with the most deals per category received nearly half of the $1B+ invested in digital health: analytics and big data, care coordination, telemedicine, hospital administration, healthcare consumer engagement, and wearables and biosensing.

Largest deals The five largest deals of this quarter, making up 41% of total funding, were Alignment Healthcare ($115M), PatientsLikeMe ($100M), Nuna Health ($90M), Evariant ($64M), and Livongo ($53M).

Exit activity Nearly 20 digital health acquisitions occurred this quarter, with two notable deals: CoverMyMeds and Jiff, making headlines for transaction size. Public companies in the Digital Health Public Index overall had a strong run. And with over 20 private digital health companies that have raised over $100M since 2011, more exits are likely in the pipeline.

New digital health-friendly funds At least six new digital health-friendly funds with, cumulatively, over a billion dollars of capital were announced this quarter! Venrock announced its eighth fund at $450M and Lux Capital announced its fifth at $400M. Making their grand entrances on the health scene in Q1 were Biomatics Capital’s $150M fund, Section 32’s $100M fund, Refactor Capital’s $50M fund, and Spectrum Health’s new $100M fund, a not-for-profit corporate VC arm.