The AI/ML use cases investors are betting on in healthcare

In theory, artificial intelligence and machine learning (AI/ML) can be applied to nearly every process in healthcare. In practice, however, entrepreneurs, enterprise leaders, and investors need to discriminate between incremental improvements and the 10X improvements that will transform the industry.

Media attention has largely centered on the ability of AI/ML to transform how clinical care is delivered through better diagnostics and treatments. But AI/ML is even more quickly transforming the business of healthcare through automation and enhancement of non-clinical, operational functions—such as claims adjudication, patient engagement, scheduling optimization, risk analytics, and documentation.

The extensive set of use cases poses a nearly impossible challenge: to keep track of all AI/ML innovation in healthcare. In order to guide stakeholders toward the most promising applications, we examine venture funding as a proxy for emerging innovation on the belief that (1) investors are betting on what they view as the most promising companies, and (2) venture money functions as an accelerant for the companies funded.

Investment Analysis Methodology

Using the Rock Health Funding Database, which tracks all US digital health venture deals, we tagged companies based on whether AI/ML was central to their business model. We then analyzed all of the digital health companies leveraging AI/ML techniques who received at least one venture funding round (of $2M or more) from January 2011 through December 2017. We were careful to include only companies that clearly relied on AI/ML as a core technology to power their business, and we further vetted the top companies with subject matter experts, including healthcare practitioners, investors, and enterprise leaders.1

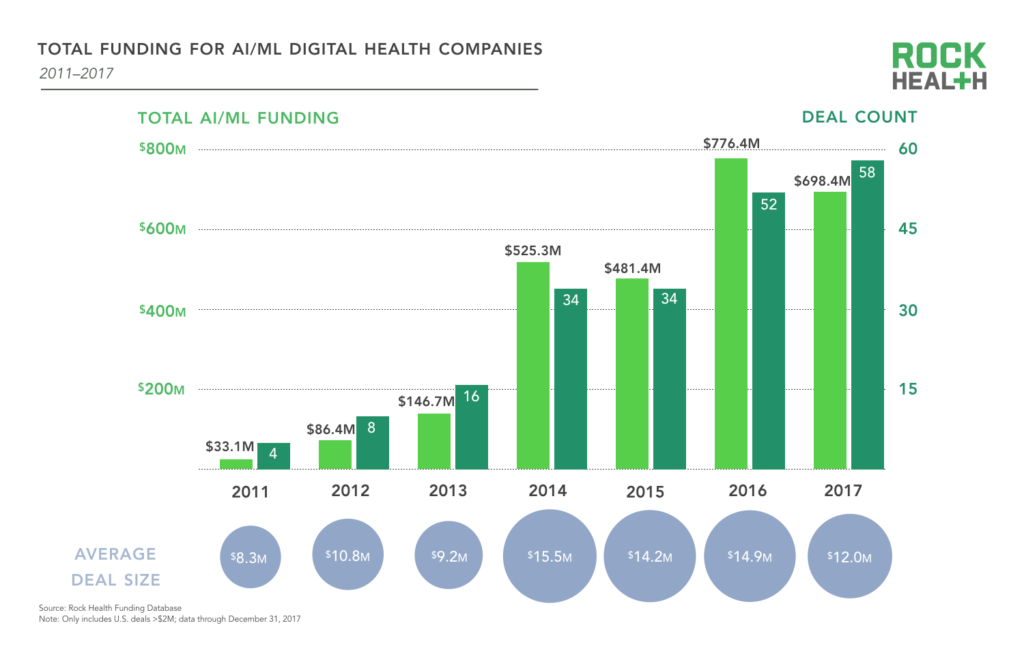

AI/ML dollars and deals

The funding of digital health companies leveraging AI/ML has largely mirrored the growth in digital health funding overall.

One hundred twenty-one digital health companies leveraging AI/ML (herein referred to as “AI/ML companies”) have raised a total of $2.7B with 206 deals from 2011 through 2017—just over 10% of all venture dollars invested in digital health during that period. Funding for AI/ML companies peaked in 2016 at $776.4M (largely due to Flatiron Health’s $175M mega-deal), representing nearly one-third of total funding to AI/ML companies since 2011.

Though total dollars fell slightly in 2017, the number of deals peaked—58 compared to 52 in 2016—a sign that companies are increasingly leveraging AI/ML algorithms to drive business value. The sizable drop in average deal size from $14.9M in 2016 to $12M in 2017 largely accounts for the dip in total funding.

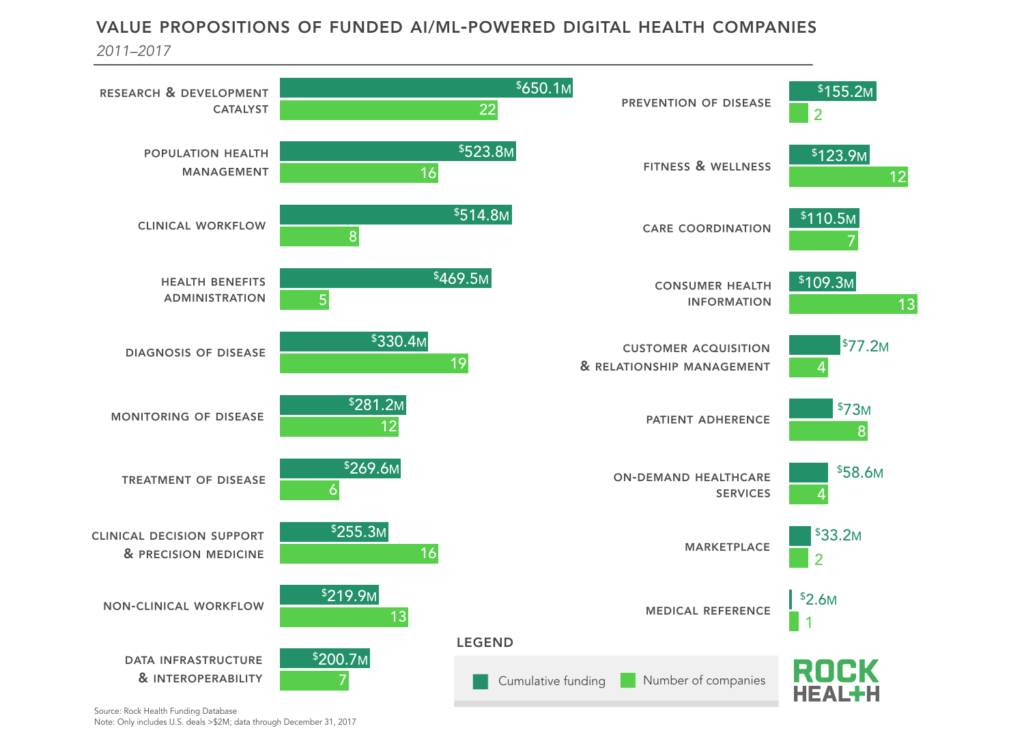

Top value propositions of AI/ML companies

Companies leveraging AI/ML are driving transformation across nearly all use cases of healthcare, with investors particularly drawn to drug discovery and population health management use cases.

Rock Health tracks and organizes companies across 19 value propositions outlined in the chart below. The chart shows the amount of venture funding flowing to companies that leverage AI/ML in service to each respective value proposition.2

Notably, each value proposition is being pursued by at least one AI/ML company, demonstrating a belief among entrepreneurs and investors that AI/ML has the potential to disrupt all aspects of healthcare business and delivery.

We think all areas of care provision will be rebuilt with compute and empathy. The rate of change will differ tremendously upon the ‘job to be done,’ but massive change is inevitable. As an investor the biggest risk is not whether deep compute (AI/ML/DL) will matter in healthcare—it’s timing. The far-future is profoundly different than most people think, but pontificating on the short-term is fraught.

Scott Barclay, Partner, Data Collective

Since 2011, AI/ML companies serving as Research & Development Catalysts have received the most funding—this includes companies in the drug discovery and clinical trial management space. Flatiron Health—notably acquired last month by Roche for $1.9B— accounts for nearly half of the dollars flowing to this value proposition, having raised $130M in 2014 and $175M in 2016. Other Research & Development Catalyst AI/ML companies include Evidation Health, whose platform creates novel digital biomarkers and analyzes real-world behavioral data to quantify health outcomes, and Utah-based Recursion Pharmaceuticals, which employs a combination of automation and bioinformatics to rapidly screen small molecules for drug discovery. And to kick off 2018, Atomwise just raised $45M to leverage deep learning algorithms to analyze and make predictions about molecule efficacy early in the drug discovery timeline.

With AI/ML enabling robust risk stratification and intervention matching, Population Health Management, bolstered by Welltok, comes in as the second highest-funded value proposition with $524M invested. The Clinical Workflow value proposition comes in third at $515M, with companies such as Qventus and LeanTaas leveraging predictive algorithms to optimize hospital supplies, labor, and throughput.

Investors are exercising caution when applying AI/ML to direct patient care delivery.

Although much of the media attention is placed on the potential of AI/ML-powered clinical tools to better diagnose and develop treatment plans, many venture dollars are flowing to companies that are streamlining operational and administrative inefficiency, and those that are optimizing resource allocation. Welltok uses ML algorithms to assess the risk of a population and recommend targeted interventions and incentives. Collective Health uses ML techniques to help members navigate the many different treatment options available, and connect them with the right care that fits their profile. Though critically important, most of these use cases are not directly reinventing clinical healthcare delivery—something we view as an intentional omission.

There are far fewer risks for using AI/ML to power a business function like determining a customer outreach strategy or connecting someone with a disease management app recommendation than there are for deciding how to treat someone with heart disease. And investors are wary of this risk (at least in the short-term), with only 30% of deals going to AI/ML companies that are embedded to support providers in direct patient care (e.g., Treatment of Disease, Clinical Decision Support & Precision Medicine).

In the short term, the biggest impact we’ll see is in clinical operations and better utilizing staff and resources— scheduling, billing, rev cycle management. There are also massive entrants leveraging AI/ML in the pop health space. These systems are changing how we manage health since they can flag things like which patients need treatments when, and who needs more at-home visits. The concept of the ‘AI doctor’ is overhyped. We’re not replacing physicians anytime soon. Instead we’ll be assisting and improving the efficiency of providers. Replacing a holistic diagnosis, treatment, and management care pathway with machines is far out—I’m not sure we’ll see that in the next ten years.

Gloria Lau, Co-founder, Alpha Medical

However, Diagnosis of Disease is a notable (and unsurprising) exception with 19 companies leveraging AI/ML for diagnosis. Investors seem bullish on this space given the potential created by recent advances in image processing to detect disease better and faster than humans.

Although discussion of the advances in AI/ML image processing generally are followed by questions of whether or when radiologists will be replaced, replacement remains a minority view and experts more commonly believe that AI/ML will instead augment the provider. Expect companies that help physicians do their current tasks better—rather than allow new capabilities—to take hold more quickly.

AI/ML CEO Demographics

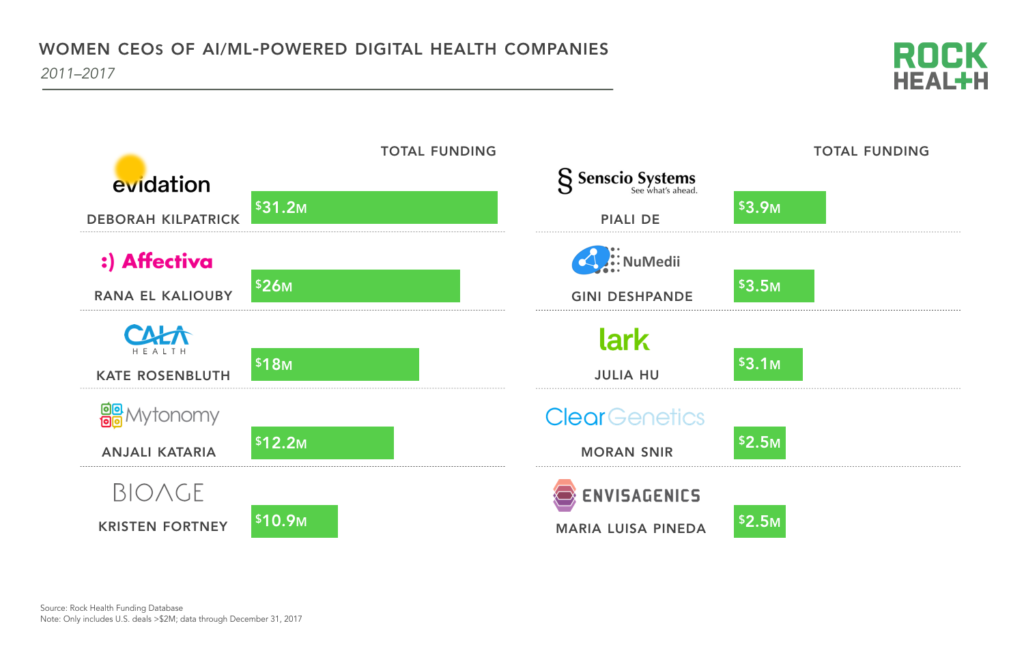

In addition to highlighting where venture funding is accelerating AI/ML, our whitepaper also dives into the leaders and companies driving change. For instance, when looking across the leadership of AI/ML-powered digital health companies compared to all digital health companies, a few findings emerge: while the gender imbalance still exists, AI/ML female CEOs are among the most highly-educated digital health CEOs.

Women are CEOs at only 8% of AI/ML digital health companies, and thus account for a small portion of overall funding (as a point of comparison, 12% of all funded digital health companies in 2017 were led by women). Both men and women CEOs of AI/ML companies are nearly two times more likely than all digital health CEOs to hold PhDs—22% of AI/ML CEOs have PhDs compared to 12% of those in all of digital health. Interestingly, while women are less likely to be the CEO of an AI/ML company, they are more likely to have received a higher educational degree, with a whopping 60% holding PhDs.

To learn more about the companies transforming healthcare via AI/ML, check out the full report.

We’re also excited to be launching an event, the Enterprise Insights Forum, to further the discussion on demystifying AI/ML in healthcare. Learn more and request your invite!

1This analysis does not include healthcare companies that fall outside Rock Health’s definition of digital health, including medical diagnostic companies, such as Freenome and Grail, and service companies that use AI/ML, like Clover Health and Oscar. Though we did not include them in this analysis, these companies raised significant venture rounds and leverage AI/ML algorithms in their work. This analysis also does not include any companies whose headquarters are outside of the US.

2A value proposition consists of the business reason or driver that motivates a decision to purchase a digital health company’s products or services. Companies can be assigned multiple value propositions when appropriate, so a single company’s funding may be represented across multiple value propositions.