From Volume to Value: Accretive vs. Disruptive Innovation in Healthcare

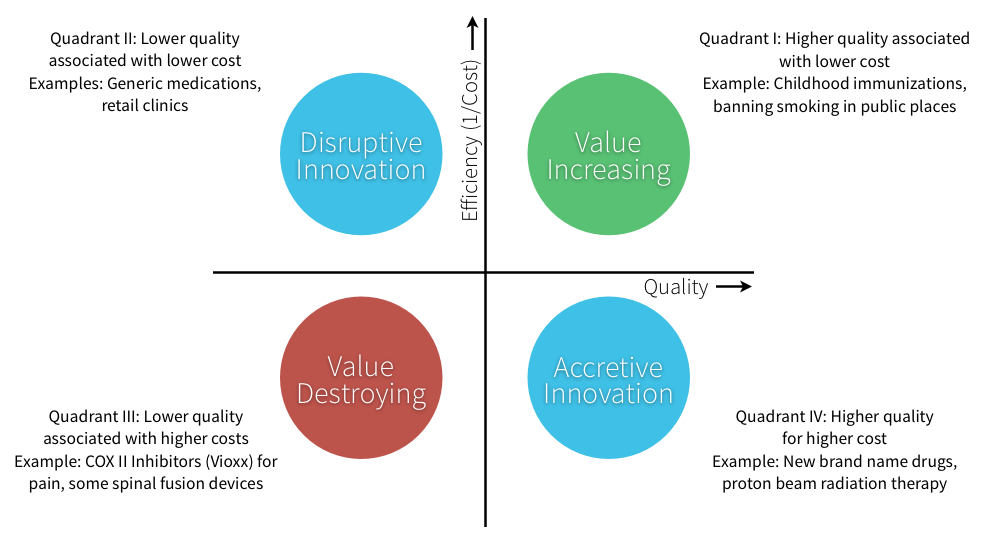

Health care has long resisted disruptive innovation – services that use technology to downshift work to those with less training and products that are “good enough” for many even if they aren’t the most advanced. Instead, healthcare has embraced accretive innovation, where we layer new products and services on top of what we’re already doing – refusing to jeopardize existing revenue streams.

Hospitals have purchased and promoted surgical robots which increase operating room time and raise costs – even while it appears that they don’t make care any better. Physicians have prescribed the newest brand name drugs – even when there are well-accepted and cheap generics available. We insist on an MRI machine with a 7 Tesla magnet, while Japan is able to deliver $99 MRIs with just a bit less resolution.

But all of this is coming to an end, which will create huge opportunities for entrepreneurs not burdened with sunk costs and huge legacy businesses they are afraid to disrupt. The confluence of unsustainably high prices in US health care, the Affordable Care Act, and changes in health care finance will immutably change health care purchasing, and make health care organizations avid for just the kind of innovation they would have thumbed their noses at a few short years ago.

Deductibles and coinsurance have been increasing rapidly within employer sponsored health plans for about a decade, and the Affordable Care Act has formalized benefit levels that include deductibles of up to $5,000 with out of pocket maximums of up to $12,700 for a family plan. Patients who have not been active consumers in the past will start “shopping” for better deals, at least for high-cost elective procedures where there is good data on quality. This includes many of the orthopedic, cardiac, and oncology services that represent outsized portions of hospital margins.

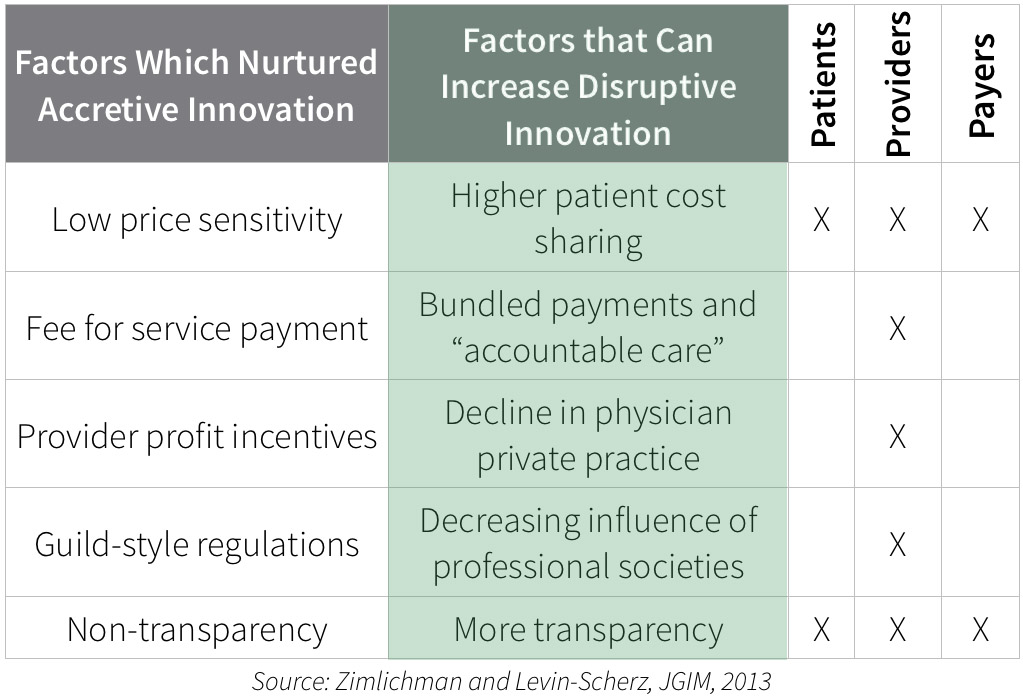

Fee for service payment has encouraged accretive innovation with more utilization and higher costs per unit, but fee for service is under attack. Many providers are moving into accountable care organizations, and accepting bundled payments or payment for value. These providers will push down the prices of implantable medical devices and supplies. They will decrease high cost imaging and surgical referrals. We’ll start seeing fewer hospitals with cranes erecting new buildings, and more hospitals making investments to lower their resource costs.

Physicians are also moving in droves into employment arrangements, where higher utilization will not necessarily lead to higher take-home pay. This lessens the subconscious urge to do more or bill more, and will make health care more fertile for disruptive innovation.

Regulations that were initially meant to protect patients, but increasingly mandate the use of expensive medical professionals when others could do the task, are falling by the wayside. Nurse practitioners are gaining full scope of practice in more states, and pharmacists are helping to manage diabetes. The “guild” rules that mandated staffing have been a major obstacle to disruptive innovation, and they are being dismantled.

It’s still not easy to tease out accurate price information from the delivery system – but there is increasing pressure to do so- from government, from health insurance plans, from employers, and from patients themselves. Innovations that lower resource cost will be even more important as we achieve greater price transparency.

Some of the disruptive innovations that are likely as we move into the post-Affordable Care Act world include:

Information plays

- Inform purchasers of the true “total cost of ownership” of different approaches or different providers.

- Segment populations, and restrict the most expensive drugs, devices or services to those who will really benefit.

Patient empowerment and self service

- “Downshift” preventive care and risk reduction to the patient herself, limiting the role of the (expensive) health care system

- Inform patients and their families of the most appropriate care for chronic diseases, and offer them effective navigation funded out of cost savings.

- Offer diagnostics directly to patients. Once upon a time physicians opposed home pregnancy tests. Patients can now do their own home HIV tests, and purchase a lab machine to check on their Coumadin dose on Amazon. The FDAs recent enforcement action against 23andme could paradoxically help open up the genomics market.

- Remote sensors will decrease the need for monitoring in the medical milieu, and require intermediary software and systems to filter the terabytes of data that would overwhelm current providers.

Lower cost sites of care

- Hospitals have been acquiring ambulatory facilities (and bumping up billing). This will lead to more opportunities to move testing and treatment to the home. This transition is already hitting sleep apnea testing.

As health care finance moves from volume to value, the opportunities for upstarts to change health care grows larger and larger.

Fee for service and high levels of insurance coverage encourage accretive innovation, while disruptive innovation will increase with bundled payments and increased consumer price sensitivity.

—————————-

Jeff Levin-Scherz , MD is a physician executive and Assistant Professor at the Harvard School of Public Health. He blogs at www.managinghealthcarecosts.blogspot.com