Reinventing life science startups, Part I: Medical devices

Medical devices prevent, treat, mitigate, or cure disease by physical, mechanical, or thermal means (in contrast to drugs, which act on the body through pharmacological, metabolic or immunological means). They span they gamut from tongue depressors and bedpans to complex programmable pacemakers and laser surgical devices. They also diagnostic products, test kits, ultrasound products, x-ray machines and medical lasers. Incremental advances are driven by the existing medical device companies, while truly innovative devices often come from doctors and academia. One would think that designing a medical device would be a simple engineering problem, and startups would be emerging right and left. The truth is that today it’s tough to get a medical device startup funded.

Regulatory Issues

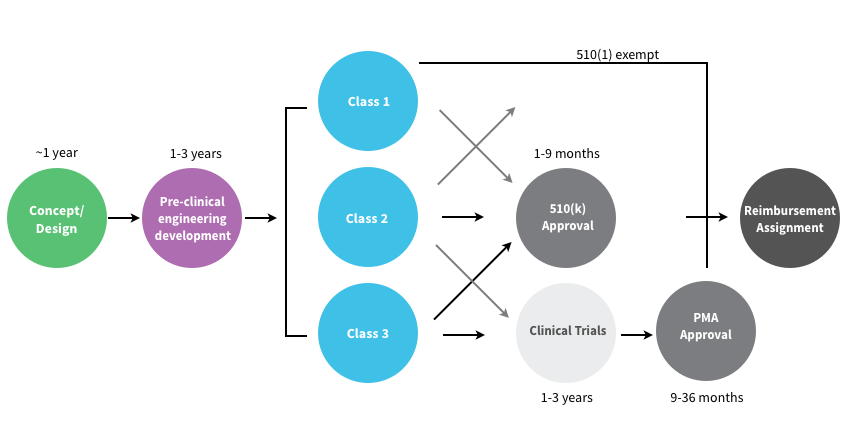

In the U.S. the FDA Center for Devices and Radiological Health (CDRH) regulates medical devices and puts them into three “classes” based on their risks. Class I devices are low risk and have the least regulatory controls. For example, dental floss, tongue depressors, arm slings, and hand-held surgical instruments are classified as Class I devices. Most Class I devices are exempt Premarket Notification 510(k) (see below.) Class II devices are higher risk devices and have more regulations to prove the device’s safety and effectiveness. For example, condoms, x-ray systems, gas analyzers, pumps, and surgical drapes are classified as Class II devices.

Manufacturers introducing Class II medical devices must submit what’s called a 510(k) to the FDA. The 510(k) identifies your medical device and compares it to an existing medical device (which the FDA calls a “predicate” device) to demonstrate that your device is substantially equivalent and at least as safe and effective. Class III devices are generally the highest risk devices and must be approved by the FDA before they are marketed. For example, implantable devices (devices made to replace/support or enhance part of your body) such as defibrillators, pacemakers, artificial hips, knees, and replacement heart valves are classified as Class III devices. Class III medical devices that are high risk or novel devices for which no “predicate device” exist require clinical trials of the medical device a PMA (Pre-Market Approval).

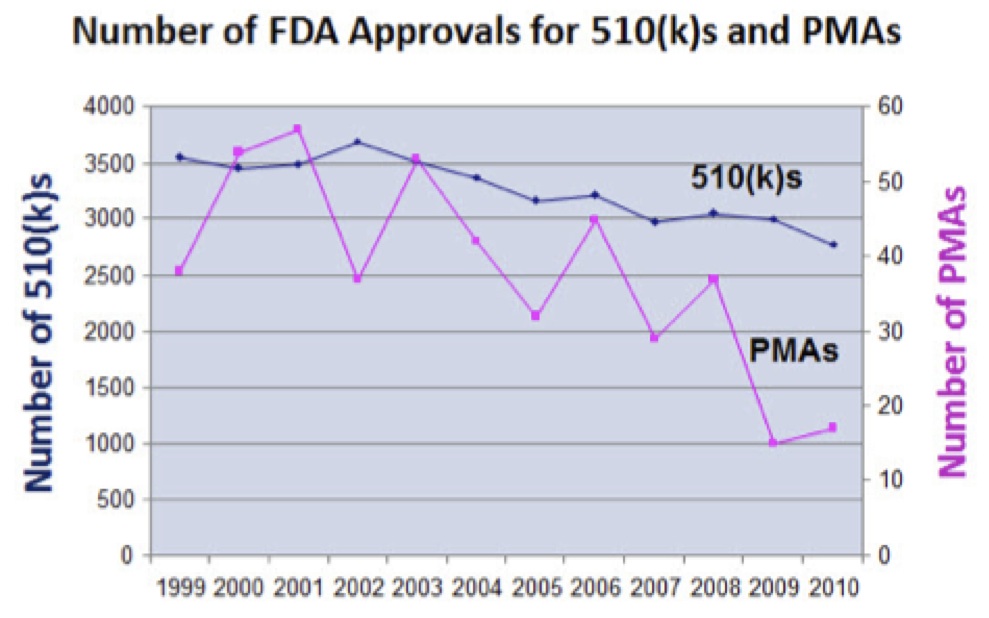

- The FDA is tougher about approving innovative new medical devices. The number of 510(k)s being required to supply additional information has doubled in the last decade.

- The number of PMA’s that have received a major deficiency letter has also doubled.

- An FDA delay or clinical challenge is increasingly fatal to Life Science startups, where investors now choose to walk away rather than escalate the effort required to reach approval.

Business Model Issues

Business Model Issues

- Cost pressures are unrelenting in every sector, with pressure on prices and margins continuing to increase.

- Devices are a five-sided market: patient, physician, provider, payer and regulator. Startups need to understand all sides of the market long before they ever consider selling a product.

- In the last decade, most device startups took their devices overseas for clinical trials and first getting EU versus FDA approval

- Recently, the financing of innovation in medical devices has collapsed even further with most Class III devices simply unfundable.

- Companies must pay a medical device excise tax of 2.3% on medical device revenues, regardless of profitability delays or cash-flow breakeven.

- The U.S. government is the leading payer for most of health care, and under ObamaCare the government’s role in reimbursing for medical technology will increase. Yet two-thirds of all requests for reimbursement are denied today, and what gets reimbursed, for how much, and in what timeframe, are big unknowns for new device companies.

Venture Capital Issues

- Early stage Venture Capital for medical device startups has dried up. The amount of capital being invested in new device companies is at an 11 year low.

- Because device IPOs are rare, and M&A is much tougher, liquidity for investors is hard to find.

- Exits have remained within about the same, while the cost and time to exit have doubled.

—-

Steve Blank is a serial entrepreneur and consulting associate professor at Stanford. He was named one of 2013’s 30 most influential people in Tech by Forbes, and in 2012, Harvard Business Review listed him as one of the “Masters of Innovation.” This post is the first of two excerpts we are featuring from “Medical Devices and Digital Health,” one installment in a twelve-part series documenting the Lean Launchpad for Life Sciences and Healthcare class at UCSF. The first class of this new program, teaching healthcare entrepreneurs how to move their technology from an academic lab or clinic into commercial settings, finished last December and was spearheaded by Blank.