2018 year end funding report: Is digital health in a bubble?

Background

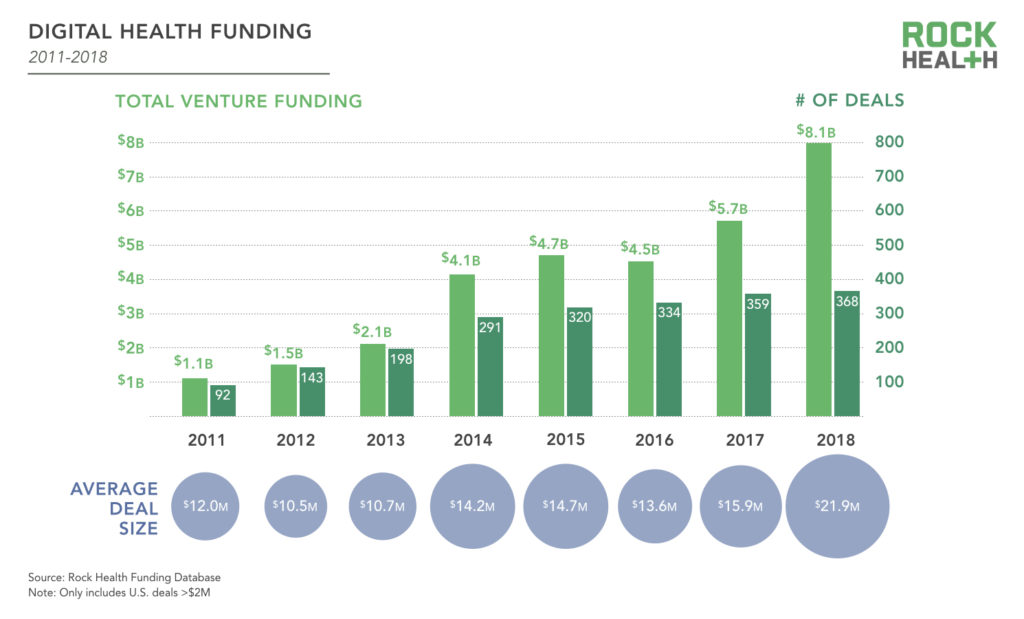

An unprecedented amount of capital is being put to work in digital health startups. Across 2018, investors poured nearly $8.1B into the sector, surpassing 2017’s record-setting total of $5.7B by a whopping 42%. With 368 digital health deals completed in 2018 (only slightly more than the 360 in 2017) the average deal size shot up to $21.9M. Half of all 2018 deals were seed and Series A rounds, suggesting investors continue to believe in new entrants as they double-down on maturing, later-stage companies.

As we said after Q3, 2018 was an entrepreneurs’ market. With capital readily available, young companies are raising larger rounds than ever before, more frequently than ever before.

Exit activity has been more measured. One hundred and ten digital health companies exited via acquisition in 2018, while the IPO drought stretched through a second year.

With the surge in funding, and absence of an equally robust exit market, there is more scrutiny on digital health than ever before, begging the question: will value creation track with recent investment trends? Given that over $30B in venture dollars have been invested in digital health since 2011, and assuming investors expect an approximate 4X return over 10 years, the market should grow to $120B in the next 4-6 years. That is a pretty large number, but with a $3.5T healthcare market, this magnitude of return is conceivable. However, with today’s high but as-yet-unrealized expectations, we aren’t surprised to see the b-word increasingly pop up in conversations.

So for part one of our two-part year-end funding recap, we dive headfirst into the question: is digital health in a bubble?

Please note: our op-ed published in CNBC reflects our funding data tallied through mid-December, as opposed to end-of-year. This accounts for the difference in the reported data between the two articles.

But first, what exactly is a bubble?

We’re defining an investment bubble as an economic cycle in which asset prices rise far beyond what is justified by fundamentals. When investors become wary of a bubble, they freeze new investments, causing a sharp contraction in prices that “bursts” the bubble. At that point, venture-backed startups that need access to fresh capital struggle to remain solvent—often regardless of their fundamentals—as valuations plummet.

A bursting bubble is not just a down cycle—it’s a rout.

Putting digital health within the broader VC context

To assess the future trajectory of VC funding for digital health, we started with two factors: (1) the health of the economy as a whole, and (2) the dynamics driving investment in healthcare innovation.

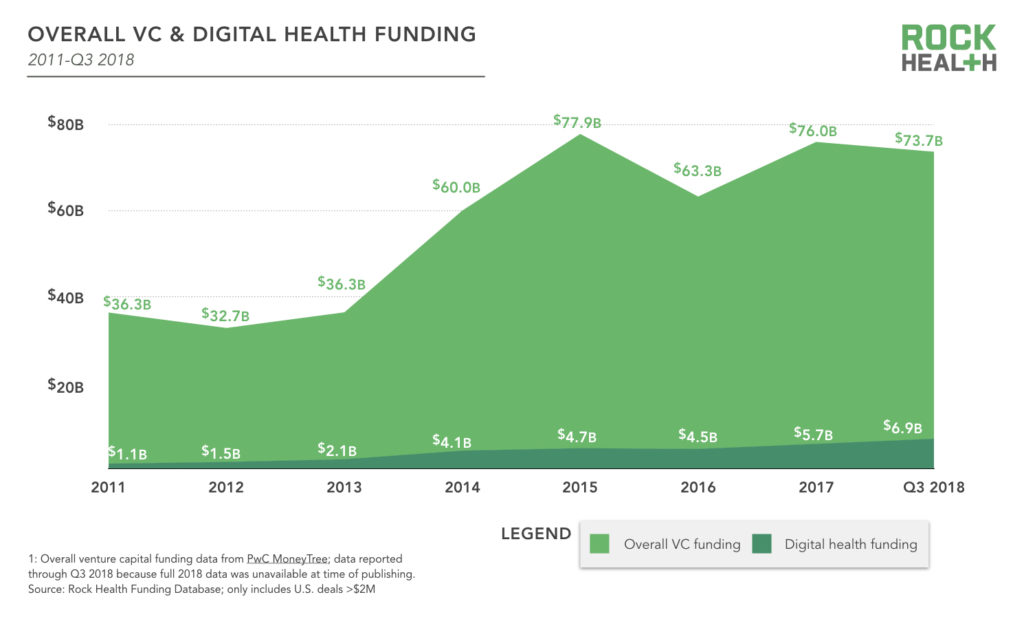

As for the first factor, investment bubbles in specific sectors are inextricably linked to the general economy and venture investment overall. Digital health is no exception. Investment in digital health has mirrored the growth in venture investment overall: both digital health and overall VC investment hit decade-high deal values in 2018 just as the public market bull run reached its 10-year anniversary.

An increase in public market volatility, a recent stock market correction, and shifting macroeconomic forces set a different, more restrained backdrop going into 2019.

Given the signs in the public market, we wouldn’t be surprised to see venture funding for digital health flatten somewhat over the next few years. We estimate digital health to be nearly 10% of overall venture funding today—something that we expect to remain fairly stable (and will watch more closely than the top-line number for total investment).

The rest of this post dives into the second factor—the fundamentals of the market for digital health products and services. We offer our data-driven perspective on the “bubbliness” of digital health, as well as how the sector might fare in a more capital constrained environment should the broader economy move in that direction. Most importantly, we consider what digital health entrepreneurs and investors should do to continue delivering value to healthcare in the months ahead.

Just how bubbly is digital health?

To provide some structure around this question, we validated a simple framework with fellow investors to assess the current “bubbliness” of digital health. The framework includes six attributes observed in previous bubbles1:

- Hype supersedes business fundamentals

- High cash burn rates

- Unclear exit pathways

- Surge of cash from new investors

- High valuations decoupled from fundamentals

- Fraud or misuse of funds

Our TL;DR take

Digital health is not an investment bubble. There is significant value being created by digital health startups, and investors and entrepreneurs are pursuing new and sustainable paths to revenue and scale. On the whole, we see highly-capitalized companies that are consistently meeting validation and reimbursement milestones.

However, these same signals—large, late-stage rounds at high valuations and shorter periods between rounds—are those of an investment cycle nearing its peak. While the future is not yet written, it seems unlikely that capital will continue to flow at the current rate. Though not a bubble burst, we anticipate the growth trajectory of venture investment in digital health to slow along with general venture investment conditions in 2019.

The next stage of digital health will be shaped by how entrepreneurs and investors reset for a tighter market in 2019. Doing so will safeguard against future market corrections—and allow the digital health community to continue making healthcare massively better for every human being.

We also heard opposing views from other smart, experienced investors, and welcome a healthy debate as this cycle unfolds.

We take a deeper look at these points and others in our full analysis below.

How digital health stacks up

1. Is hype superseding business fundamentals?

Bubbles grow when investor exuberance outstrips economic realities. During the dotcom boom, investors poured money into companies in the new internet economy. The trouble was, few had viable business models to justify the hype (cue Pets.com sock puppet Super Bowl advertisement). Because this painful lesson has stuck with investors and entrepreneurs, it’s the first place we looked for signs of a digital health bubble.

It’s no secret—healthcare is complicated. Digital health startups must figure out how to navigate long sales cycles, slow-moving reimbursement paradigms, regulatory complexity, and scale, and some bold early movers entered the space without fully appreciating these challenges. But investors and entrepreneurs are actively learning and moving toward sustainable business models. Today, we see bold and savvy startups doing things like risking payment on their ability to produce meaningful clinical outcomes and pursuing strong validation pathways for reimbursement. This shift towards producing and demonstrating value aligns startup innovation with macro-trends like the move to reimbursement models that reward quality and efficiency. Additionally, most startups have supplemented or supplanted a direct-to-consumer approach with an enterprise one, with 61% of companies that started B2C switching to B2B or B2B2C (and some shuttered after making big bets on B2C).

In our view, today’s digital health investments are driven far more by the fundamental, realistic potential for technology to transform the healthcare market than by irrational hype. And we’re in good company.

The U.S. healthcare market is over $3T, which is nearly 15X the U.S. advertising industry. Given the enormity of the market opportunities, it feels more than large enough to absorb the amount of capital being invested today. It has taken a decade to reach the $8B investment pace we will see this year. I just don’t conclude we are in a bubble. When we saw bubbles created in other sectors, it was often around uncertain business models and when too much capital flooded in too quickly. We have crystal clear business models here addressing enormous market opportunities.

Michael Greeley, Co-founder and Partner, Flare Capital

Verdict: not bubbly

2. Are burn rates unreasonably high?

During the dotcom bubble, companies burned through loads of investor capital but struggled to remain solvent when funding dried up.

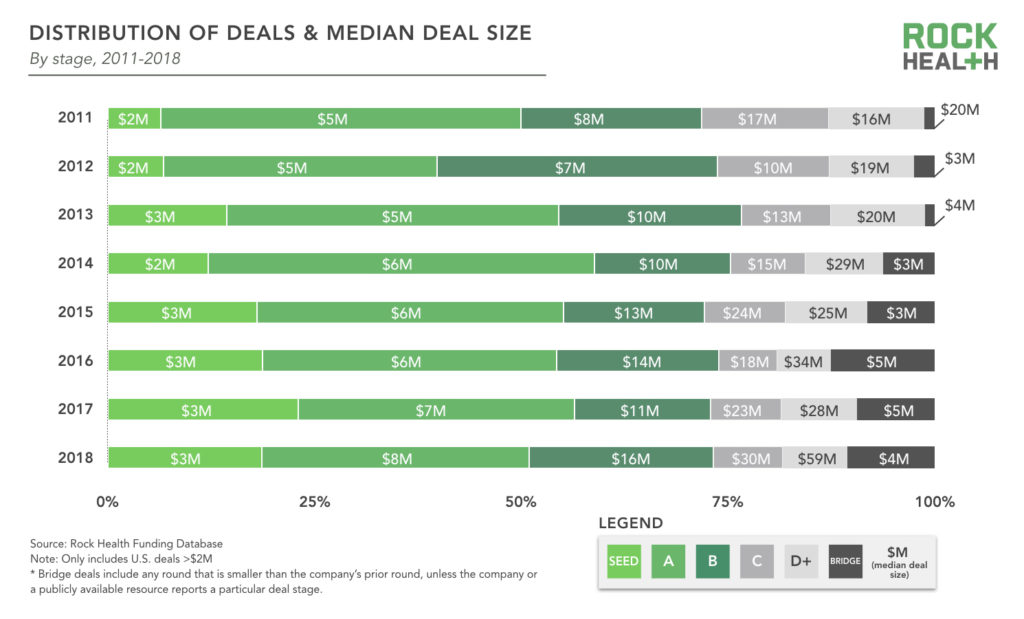

This is perhaps the “bubbliest” attribute of digital health—many well-funded startups are raising larger rounds, and doing so more quickly. Since 2011, the median deal size has increased across all stages and this trend has been particularly pronounced among later-stage deals (B+).2

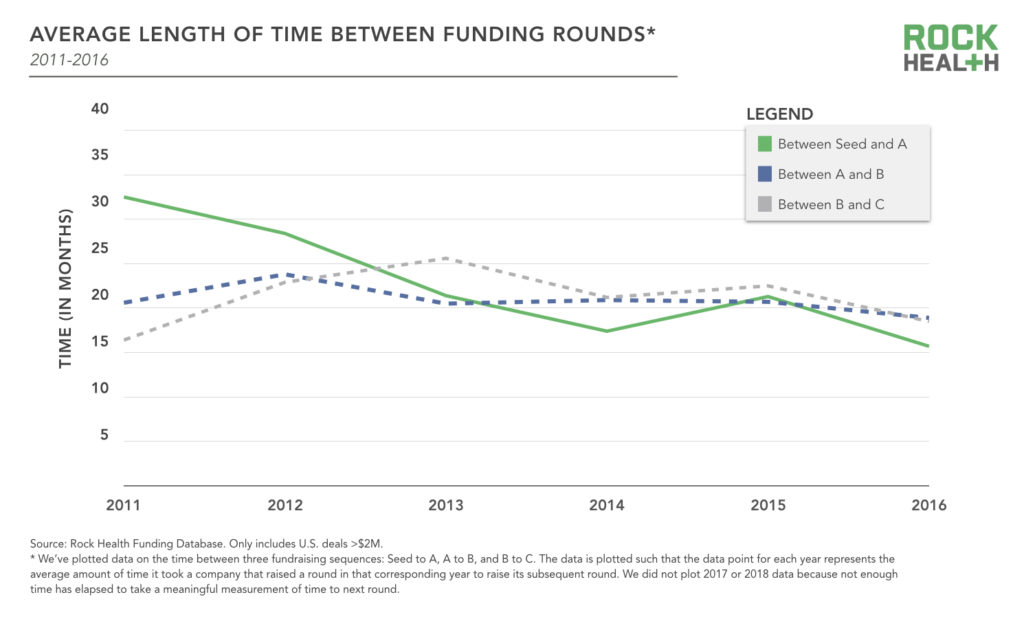

Meanwhile, since 2011, time between raising seed and Series A rounds has been cut roughly in half, from over 30 to 15 months. This increased pace of fundraising is due in part to the availability of capital, but also likely reflects a maturing space. A lag of over 30 months between seed and Series A does not fit the realistic growth needs of most startups. While its difficult to say whether 15 months is too short an interval for this market, the move in this direction aligns better with the timing of the growth milestones successful digital health startups should achieve before raising their next round. We’d like to see this number stabilize—and perhaps moderate—in future periods.

Several investors we spoke with highlighted the hybrid nature of digital health: less-capital intensive than traditional healthcare investments such as biopharma and medical devices, but with more complicated, slower sales cycles than traditional tech. Startups have to spend time and capital to figure out (and sometimes develop) the market for their technology, and they often run into healthcare incumbents as gatekeepers who control the pace and scale of innovation adoption. Overcoming friction between the demand side of the market and startup innovation is absolutely essential, so startups can use cash to scale as opposed to just stay afloat during long sales and pilots.

With sales cycles being as long as they are, you have to burn a fair amount of capital to figure out where you’re headed. It’s a fundamental, uncomfortable reality. The CEOs that figure out how to do that as efficiently as possible will be able to retain a lot more ownership in their companies and give themselves more flexibility at exit.

Liz Rockett, Director, Kaiser Permanente Ventures

The pace at which startups raise capital should ultimately reflect these realities, and savvy entrepreneurs will find ways to reduce the need for fresh capital while reaching growth milestones.

Verdict: moderately bubbly

3. Are exit pathways clear?

Anywhere from 60% to 90% of startups fail. But as long as enough companies successfully exit, the VC equation holds and investor capital is returned with a profit. When exit pathways fail to materialize, the music stops playing and investors will pull back on funding.

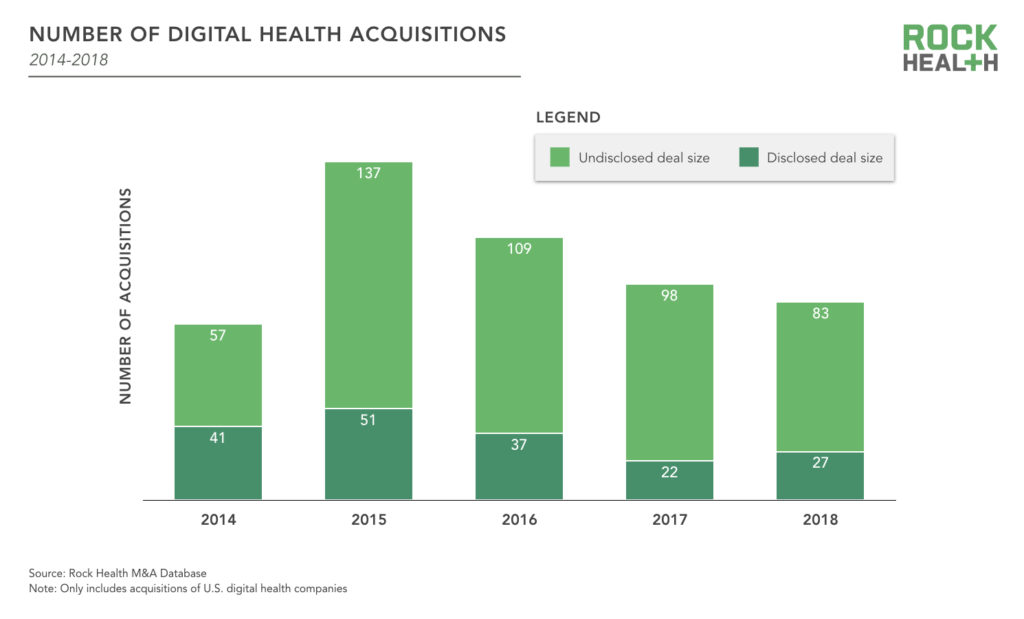

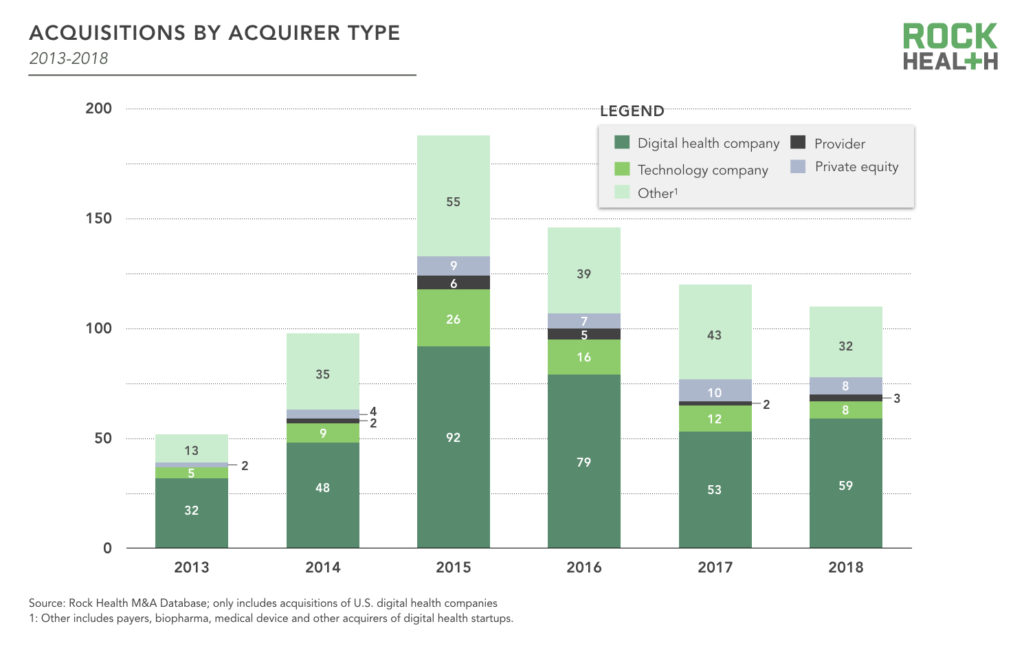

In digital health, the exit market has been sluggish. There hasn’t been a digital health IPO since iRhythm’s 2016 public offering, despite tech IPO activity picking up in 2018. M&A remains the dominant exit strategy, but has been slightly declining for the past three years, with 110 acquisitions in 2018.

Digital health companies continue to be the most prolific group of acquirers of other digital health companies. We believe this signals a trend toward consolidation in the next few years. To date, consolidation has taken a few forms. There have been a few acqui-hires and fire sales this year, but there’s an emerging pattern of digital health companies acquiring to expand their portfolio of offerings. Livongo acquired Retrofit and its DPP solution to grow their digital therapeutic offerings. And in September, Welltok acquired WellPass (itself a merger between Sense Health and Voxiva), continuing Welltok’s acquisition spree of digital health companies (including Mindbloom and Predilytics). Additionally, ResMed closed out the year acquiring Propeller Health for $225M with the hopes of becoming “the global leader in digital health for COPD.” This was just after ResMed announced a $750M deal to acquire MatrixCare, an EHR company. We also saw private equity firms combining point solutions into bigger players, just as Marlin Equity Partners acquired Virgin Pulse and RedBrick Health, bringing together two employee health and wellness solutions.

Some investors expressed concern that overall healthcare consolidation will limit the number of potential buyers for digital health companies. But, dramatic shake-ups among the biggest players, including the entry of tech giants and vertical integrations such as that of CVS and Aetna, will necessarily drive more demand for digital innovation—not less—as these combined entities sprint to demonstrate synergies to shareholders and customers alike.

This third bubble attribute was tough to grade because while the exit market has been sluggish, there’s opportunity for (and rational predictions of) consolidation on the horizon.

Verdict: moderately bubbly

4. Has there been a surge of cash from new investors?

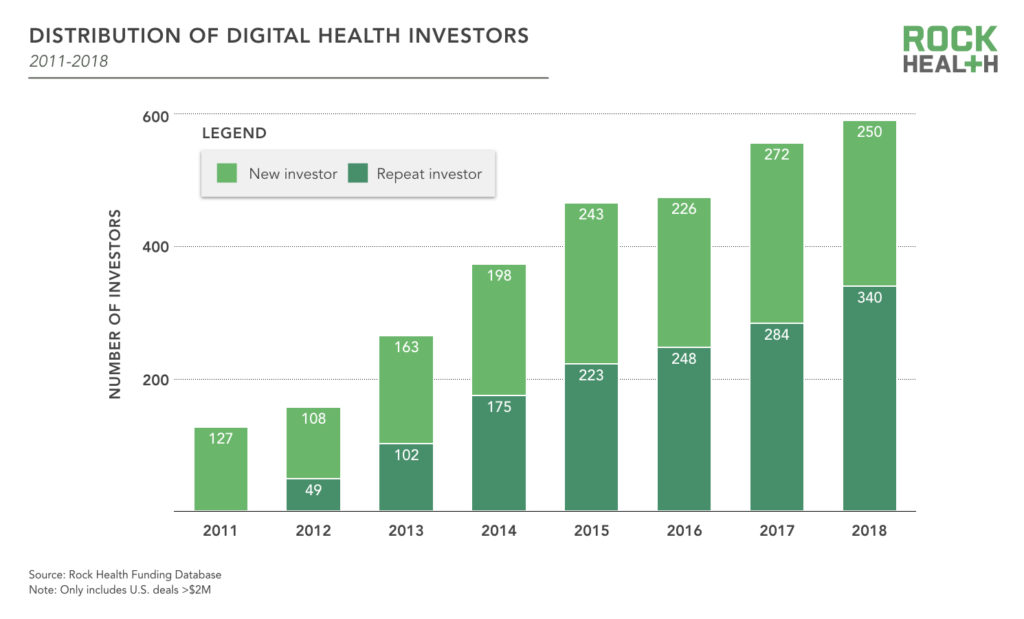

Rising prices in a bubble can attract new investors making speculative bets, following hype and capital as money continues to pile on. This may motivate the 200+ new investors who have entered the digital health sector every year since 2015. Depending on their healthcare experience, the additional capital from these “newbie” investors can potentially inflate valuations. And they may be the first to pull back at the signs of a downturn.

With the influx of capital from tech and other investors less experienced in healthcare, there has been much more of a focus on product features instead of what really matters, which is patient outcomes. Products and services that are only about features and sizzle will inevitably struggle to gain traction. This will be a tough and perhaps costly lesson to learn for many non-healthcare investors in the next two to three years.

Sami Inkinen, CEO and Co-founder, Virta Health

Flow of new capital can be a double-edged sword, but balance is everything. The data we reviewed painted a balanced picture: Even with a decent number of new investors each year, repeat investors have consistently and increasingly outnumbered new investors in digital health since 2015, and the spread is growing.

Commitment from those who know the space well is perhaps the strongest signal of a balanced investor community, particularly as they encourage companies to pace growth and develop a long-term fundraising plan that doesn’t hinge on an annual influx of cash.

Verdict: not bubbly

5. Are valuations high and decoupled from fundamentals?

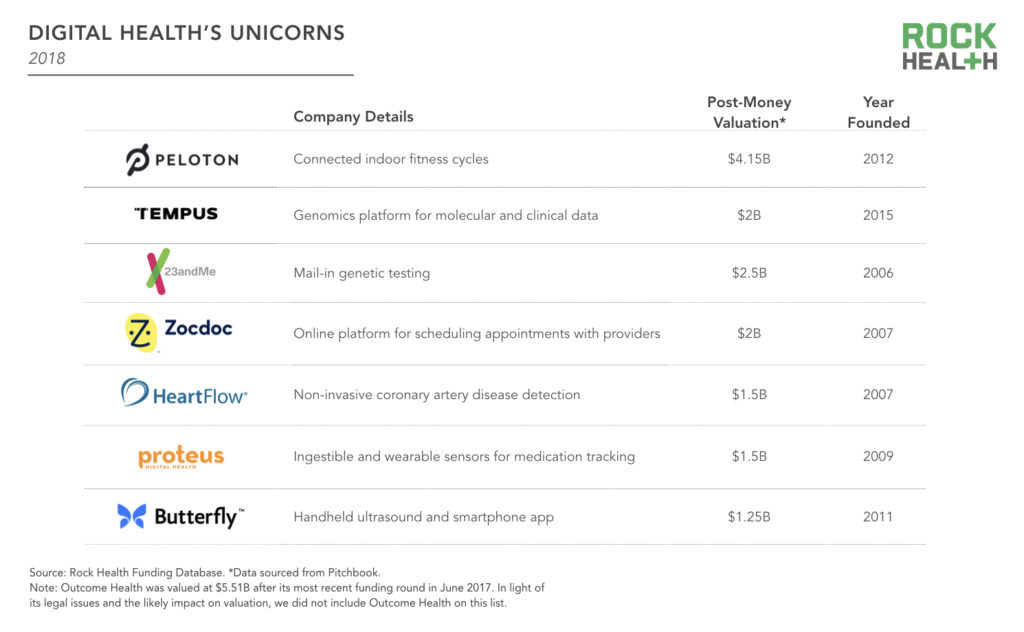

With bigger, more frequent rounds, some valuations are soaring, leading to seven digital health unicorns (private companies valued at $1B+). Six of these companies raised a round in 2018 with an average deal size of $231M. Tempus, a platform with clinical and molecular data for cancer research, raised two rounds this year–capping off a 12 month period in which it raised $260M.

Human Longevity was the former unicorn that lost its horn in 2018. Its recent down round valued the company around $310M—a dramatic drop from its 2017 $1.5B valuation.

The majority of investment professionals (64%) believe health care IT investments are overvalued. One entrepreneur noted, “The valuations seem outsized compared to the scaling risk and associated challenges, especially given how big the services component is in a lot of business models.”

Bessemer Venture Partners’ Steve Kraus cautions, “I’m not a big fan of the obsession with unicorn valuations. The focus should be on building a ‘unicorn product’ in healthcare and then the rest will take care of itself.” He sees startups hiking up valuations via large investments rather than taking a measured approach of raising less cash and selling at a lower, but good, multiple.

Others focused on the massive size of the healthcare market. If the future of US healthcare is digital, then the digital health sector may be fully valued and priced for success.

Valuations haven’t raced to wild extremes. Some later stage companies have high valuations—you might say on the margin those companies are fully priced for success.

Michael Greeley, Co-founder and Partner, Flare Capital

Fortunately, overvaluation isn’t an inevitability—startups can avoid this by taking smart, not big, money.

Verdict: moderately bubbly

6. Are startups partaking in fraud or misuse of funds?

Before it pops, a bubble tempts market participants with massive returns and can lead to greed and excess. During the cryptocurrency bubble of 2017-2018, as many as 80% of the initial coin offerings were scams. Pervasive stories like this are a signal that lavish extravagance—and at times unlawful greed—are tipping a market towards a bubble.

These stories are not common in digital health, but there are a couple notable exceptions. In 2017 Outcome Health broke the trust of its customers and investors by manipulating data about the effectiveness of its pharma advertising business. The company had achieved unicorn status with a $500M growth equity round only months earlier. The end of 2018 saw Theranos’ complete collapse, the most notable of failed healthcare startups.

Could Outcome Health and Theranos be indicative of a wider trend? We don’t think so. There hasn’t been further evidence of fraudulent behavior infecting the digital health industry. We hope Outcome Health and Theranos continue to be outliers and digital health companies maintain the course of innovation with integrity.

Verdict: Not bubbly

Closing thoughts

Now a significant part of the venture capital asset class, digital health funding will be increasingly tied to macroeconomic cycles. If and when capital becomes harder to come by, digital health companies will have to prove that they can deliver on their fundamentals (and should start planning for this now).

High valuations and burn rates are signals that the funding cycle is nearing its peak. But we don’t think there’s a bubble to burst given the smart investors and entrepreneurs invested in finding paths to validation and revenue, the viable exit paths and consolidation on the horizon, and the large overall opportunity for innovation in healthcare. But everyone should prepare for a moderation in funding—when it comes, the real value-creators in digital health will stand tall.

What’s your take on the state of digital health? Join the conversation on Twitter at #starttheconvoJPM or email us at research@rockhealth.com. Keep an eye out for Part 2 of our 2018 funding recap next Monday, January 14th. We’ll cover the companies investors are most excited about, the hottest technologies, and how the investor landscape is shaping up.

Partner with us!

A special thank you to our generous corporate partners for their continued support. For full access to the funding report and database, become a Rock Health partner. Email for more information about how your organization can work alongside Rock Health.

Thank you to our contributors

This report would not have been possible without the help of a number of individuals who have graciously shared their expertise:

- Anne DeGheest, Founder, HealthTech Capital and Medstars

- Deborah Kilpatrick, CEO, Evidation Health

- Lisa Suennen, Managing Partner, Venture Valkyrie

- Liz Rockett, Director, Kaiser Permanente Ventures

- Michael Greeley, Co-founder and Partner, Flare Capital

- Sami Inkinen, Co-founder and CEO, Virta Health

- Steve Kraus, Partner, Bessemer Venture Partners

Footnotes

1Speculative bubbles come in many different shapes and sizes. Historical bubbles have touched everything from mortgage backed securities and digital currencies to tulip bulbs and dot-com companies. In this case, we are evaluating the potential for a bubble where the object of speculation is privately held startup companies.

2Note that this trend largely holds for all venture-backed companies (i.e, digital health as well as other sectors like tech, social media, etc.) broadly during this same period.

3Rock Health does not consider Theranos to be a digital health company.