2016 YTD digital health funding: 10 things you should know

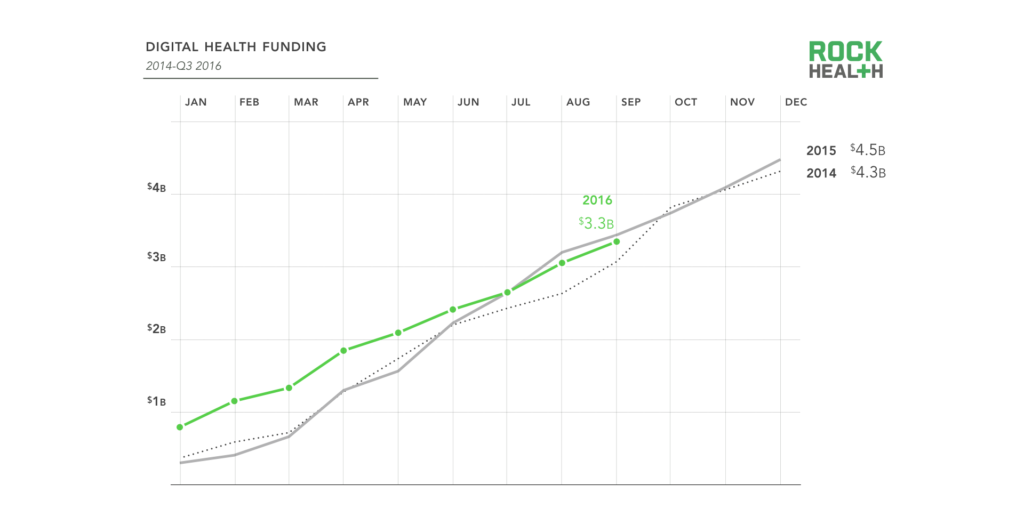

1. It’s unlikely this year will shatter any funding records. There have been 233 digital health venture deals (for 176 unique companies) closed so far this year, up from 219 deals in Q3 2015 and totaling $3.3B in venture funding. The actual dollar value is down slightly year over year, but we’re likely to end the year on par with the previous two years.

2. Growth stage digital health deals are at an all-time low, representing just 10.2% of all deals. On the other hand, investor appetite for early stage companies continues, with Seed and Series A deals accounting for the majority of deals (60.9%) in 2016.

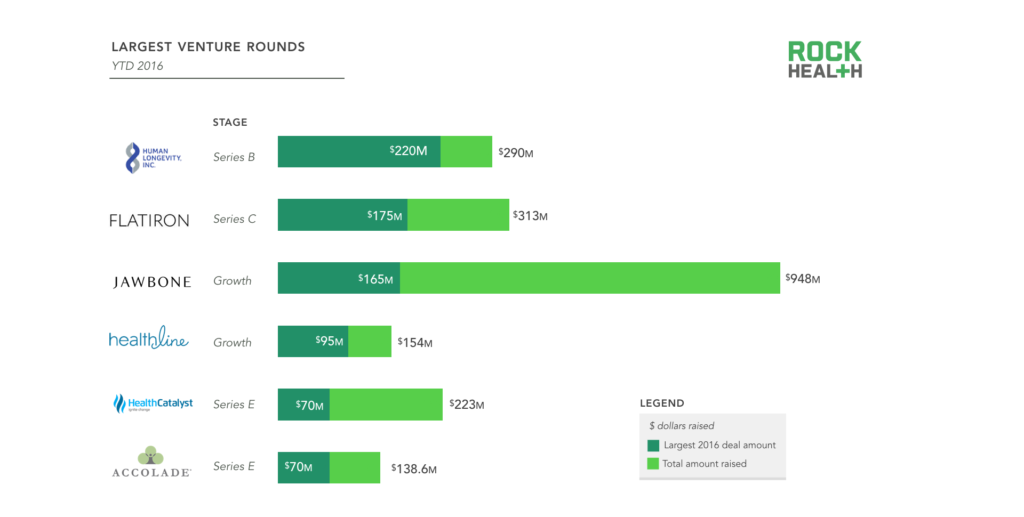

3. The top six deals make up nearly a third of all funding this year, with several massive rounds. Human Longevity raised the third largest single venture round we’ve seen (behind Jawbone’s $300M round in 2015 and NantHealth’s $250M round in 2014).

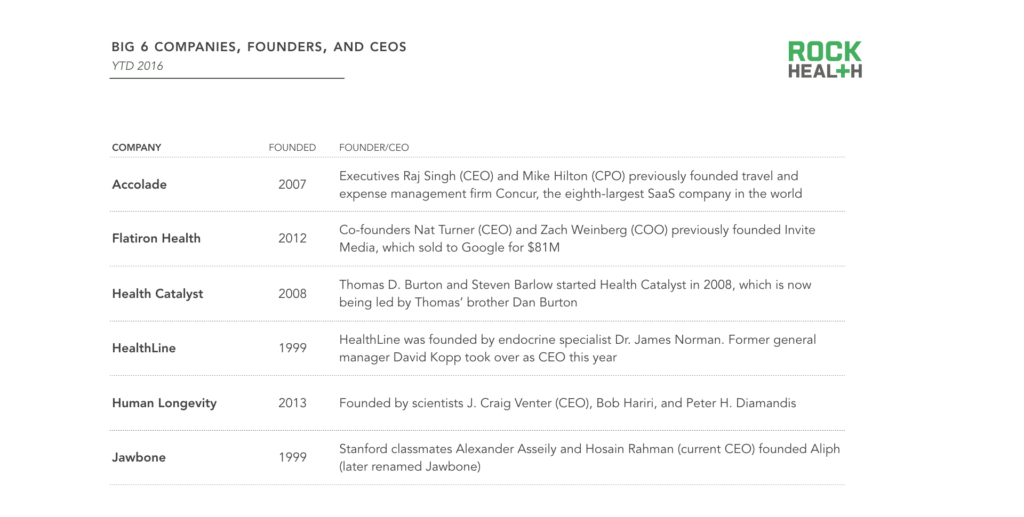

4. Companies making up the six largest deals YTD were founded an average of 10 years ago, with the youngest being Human Longevity (founded in 2013) and the oldest being Jawbone and HealthLine (both founded in 1999). Some other fun facts about the ‘Big Six’:

- The average age of founders at the time of company launch was 37; and 46 when they raised their latest round.

- The most common undergraduate majors among these founders and CEOs are economics, engineering, and biology. But for aspiring CEOs who prefer the path less traveled, those aren’t your only options. HealthLine CEO David Kopp received a literature degree from Harvard, Peter Diamandis received a graduate degree in Aerospace Engineering from MIT, and Health Catalyst co-founder Steven Barlow received a BS in Health Promotion and Education from the University of Utah.

- While nearly a third of all digital health CEOs have an MBA, the only ‘Big Six’ CEO with an MBA is Dan Burton of Health Catalyst, who received his degree from Harvard Business School.

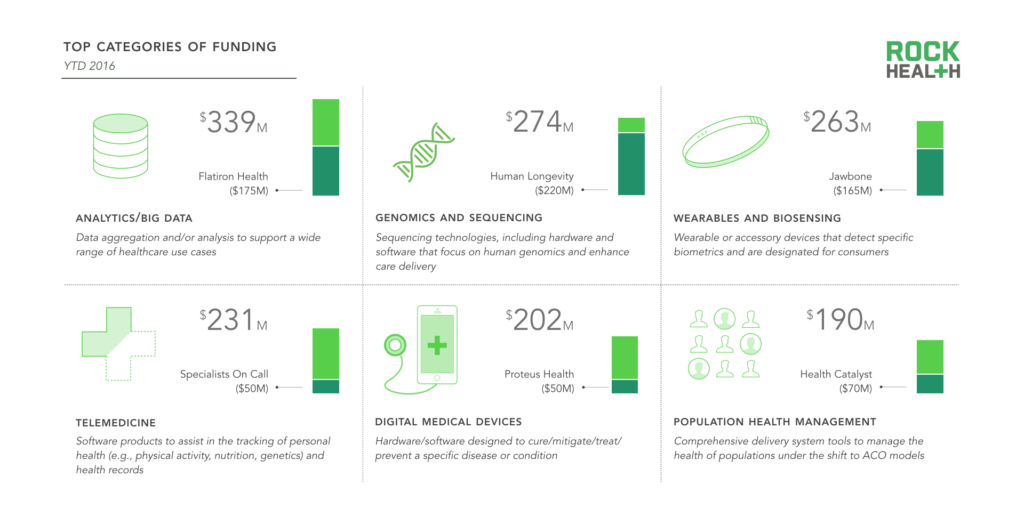

5. The top six categories represent almost half of all venture money raised this year (44%). Buoyed heavily by Human Longevity’s massive $220M round, the genomics and sequencing category shot up dramatically, appearing in our top categories for the first time. We dug in on the opportunity in our latest report.

6. Forty-seven cents per VC dollar invested in digital health goes to a company headquartered in California, for a total of $1.5B invested in the state so far this year. New York saw 28 deals this year, followed closely by Massachusetts with 24 deals. Emerging hubs Texas and Illinois continue to grow, with 14 and 12 deals, respectively (compared to just eight deals each in 2015).

7. Twenty-one MD CEOs raised funding this year. The medical school with the most representation is Stanford, with three MD CEOs, followed by the University of Pittsburgh School of Medicine, with two. Five of these CEOs went to medical school outside of the US, from China to Israel.

8. Reproductive health companies gained traction in 2016, providing tools to support women’s reproductive health from fertility through pregnancy. These companies are more likely to have a woman CEO, with five out of seven CEOs being a woman—compared to just 8% of digital health CEOs overall.

9. Several new investors became active during the third quarter, with 25 firms making three or more investments, compared to only 12 funds crossing that threshold in the first half of the year. The University of Pittsburgh Medical Center (UPMC) began investing this year and has already become the most active venture investor of the year with six investments (including Health Catalyst and Lantern). Not far behind is long-time tech and healthcare VC Khosla Ventures, with five deals (including Neurotrack and Color Genomics).

10. Compared to the 176 companies that received venture funding so far this year, far fewer had to shut their doors. The most memorable shutdowns of 2016 include four companies and two notable products.

- January, 2016 Wellero

Two years after it launched, Portland-based Cambia Health Solutions shuttered its mobile payment startup Wellero. MobiHealthNews reported that, “with only about 1,100 users on the app despite it being deployed at 700 health plans, it appears the service just failed to get traction.” - January, 2016 HealthSpot

Despite securing $43.8M in funding, being within a hot category like telemedicine, and having backers like Rite Aid, Cleveland Clinic, and Xerox, the telemedicine kiosk company filed for bankruptcy at the start of 2016, five years after launch. - April, 2016 BioBeats Pulse app

Upon raising $2.3M, BioBeats pulled its Pulse app from app stores. The product matched music to a user’s heart rate data using the smartphone’s camera. - May, 2016 Google MyTracks app

Google killed its activity-tracking app MyTracks, which recorded users’ path, distance, and speed on walks, runs, or bike rides to focus on “more wide-reaching, mapping projects,” though the company still offers activity-tracking features via Google Fit and the Android-only Google Now. - May, 2016 Enigma

Cambia pulled the plug on another in-house startup, Enigma (formerly known as Muse), which aimed to help customers minimize unexplained medical symptoms through a “cognitive-behavioral” approach. - August, 2016 Drugstore.com

Five years after it scooped up Drugstore.com and subsidiaries for $429M, Walgreens dropped the e-commerce startup to streamline operations.

Join us on Tuesday, October 4th at 11am PT for a Twitter chat (#RHQ3) with some of our portfolio companies and get their take on doing work in this year’s funding environment.

Uncover the biggest companies and trends in digital health, including details of every deal since 2011. Rock Health partners receive access to quarterly updates of our Digital Health Funding Database, our consumer survey data and reports, and more. Learn more at partnerships@rockhealth.com