The genomics inflection point: Implications for healthcare

For full access to the report and all of our research, become a Rock Health partner—email partnerships@rockhealth.com.

The genomics industry has tremendous potential to move the needle in health. Thanks to a number of high-profile investments and initiatives—such as President Obama’s Precision Medicine Initiative (and the launch of its 1 million participant Cohort Program this past month)—consumers are becoming increasingly aware of genomics and its role in healthcare.

The value of the genetic code remains an untapped opportunity in healthcare, and a formidable challenge to the physicians, scientists, and technologists responsible for driving the industry forward. In this report, we explore an industry at a critical inflection point. Despite an unprecedented drop in sequencing costs and technological advancements, genomics has not yet achieved mass consumer appeal or seamless integration into clinical workflows. Delivering on the promise of genomics is dependent upon three main factors, most of which are within the purview of digital health: (1) ensuring broad access to diverse data sets used to deliver insights (2) removing barriers to clinical workflow incorporation, and (3) advancing technology, both in the lab and in the cloud.

To inform our research, we conducted a survey of one thousand consumers to understand potential pathways to greater adoption and current barriers. We provide novel data and insights regarding adoption, willingness to pay for specific use cases, and explore concerns around privacy and ownership.

The field of genomics has incredible promise for improving and personalizing health. But, just as the genome itself has remained relatively elusive for decades since its discovery, so too are the solutions for integrating genomics into healthcare at scale. We hope to shed some light on the challenges and exceptional opportunities of genomics for healthcare and technology.

Background

Is it right to say genetic data is more objective than other types of data? Will everything be reduced to binary outcomes? There are still lots of unknown unknowns. But, if we’ve searched everywhere else, this might be the final place to look to solve those puzzles.

Sajith Wickramasekara, Founder & CEO, Benchling

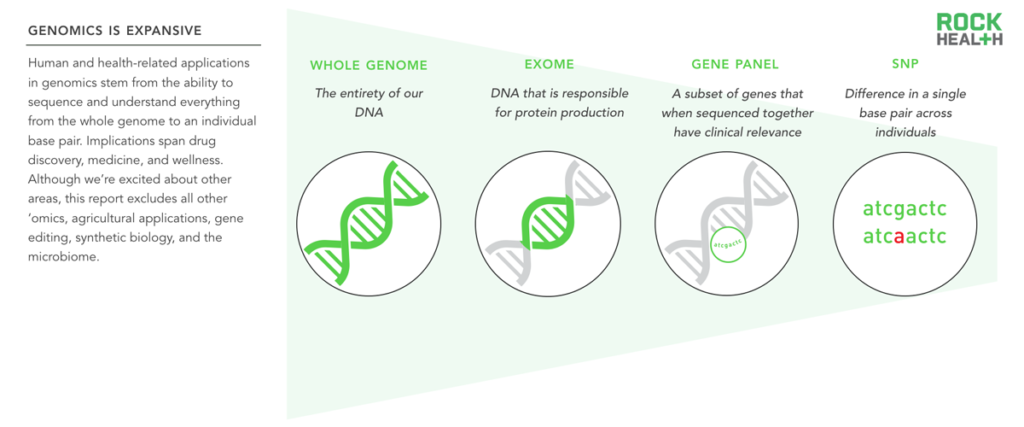

This report considers all human and health-related applications of genetic data, including SNPs, gene panels, exomes, and whole genomes.

The field of genomics—and its implications—are expansive. We focus this report on all human and health-related genomics applications, including the three billion base pairs of the whole human genome, SNPs (single nucleotide polymorphisms or single base pair changes), the exome (the 1-2% of the genome that leads to proteins1), and gene panels (groups of genes that when sequenced together have clinical relevance). Outside the scope of this report is the rest of ‘omics (for example, proteomics and metabolomics), anything related to agriculture, gene editing, synthetic biology, and the microbiome (another exciting area with implications for human health). We use the terms genomics and genetic tests in this report, and the distinction is important: genomics is the study of variations across large segments or the whole genome, while genetics refers to specific individual genes2.

The clinical opportunity for genomics is extensive, however consumer engagement is necessary for this potential to be realized.

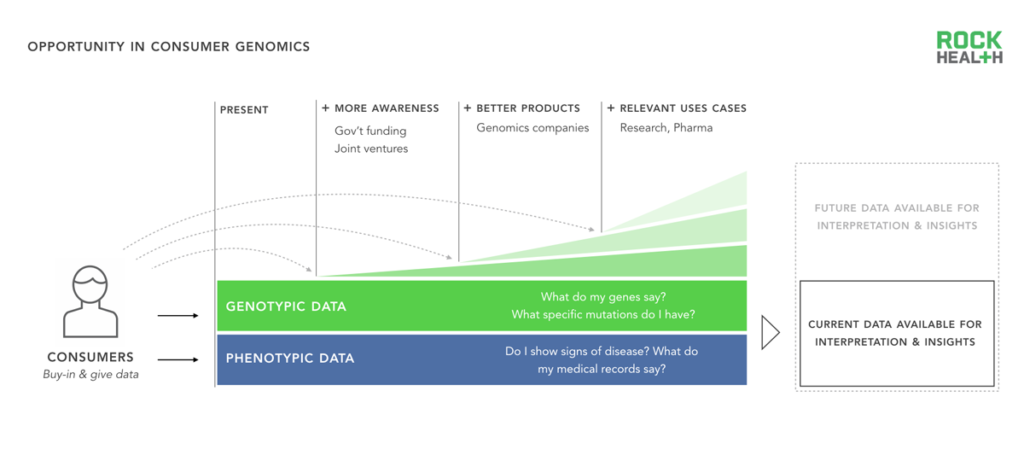

One of the primary aims of genomics is to generate personalized and actionable insights that lead to better health. Because much work is still needed to understand how genes influence and interact with a person’s health, scientists need greater amounts of diverse genetic and phenotypic data (e.g. personal information)3 and unfettered access to those linked data sources.

Genetic data in the ecosystem increases when consumers buy direct-to-consumer genomics products, opt in at the physician’s office to get a genetic test, or participate in clinical research trials. The genomics industry can and should encourage participation at these touch points. Currently, this is being achieved in three ways: (1) Awareness around the field of genomics, (2) Better consumer genomics products, and (3) More relevant consumer use cases. The US government is increasing awareness by funding well-publicized initiatives, such as the Precision Medicine Initiative, while companies, like 23andMe, are providing better consumer products that are easier to order and understand. Lastly, diagnostic companies and research institutions like The Broad Institute are uncovering novel associations and use cases that spur interest in consumer-facing products.

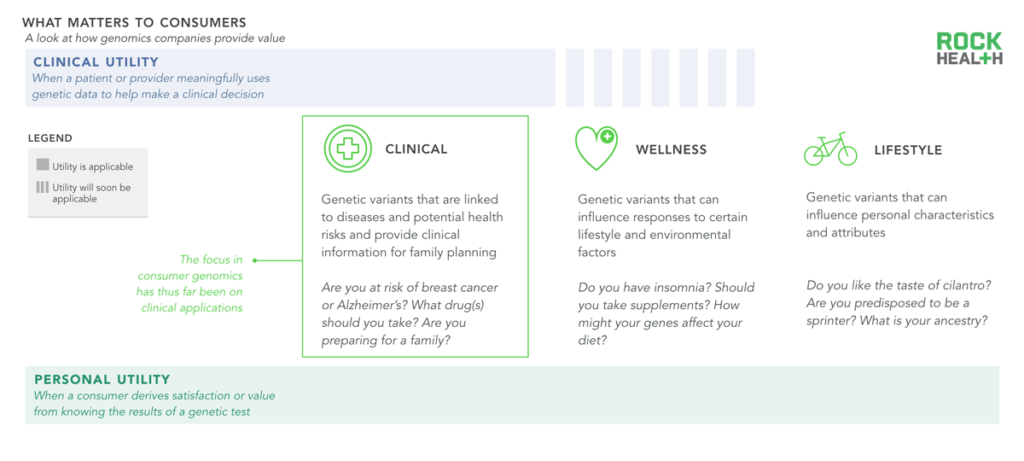

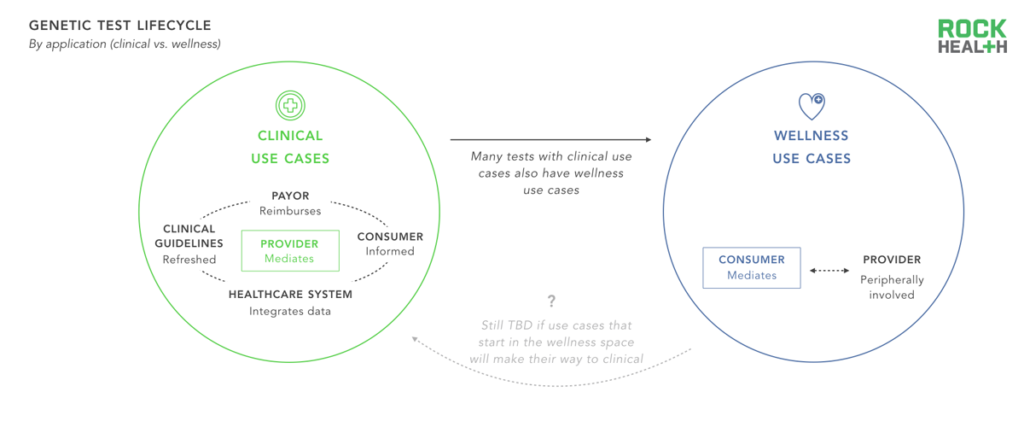

Consumer genomics use cases fall into three categories; applications vary in their ability to offer clinical and personal utility.

Consumers and patients derive two types of benefits (or utility) from a genetic test—clinical utility and personal utility. Clinical utility is relatively straightforward: Does this test change my potential course of treatment? Does knowing that I am at increased risk of a disease change how I make decisions with my doctor? Personal utility is more nuanced and depends in large part on how the consumer processes and makes use of the genetic information. For example: Does learning about my personal genealogy bring me happiness? Will sharing this data with family members or a physician be meaningful to me, even if there is little reward in terms of clinical actionability?

We grouped the most relevant consumer genomics use cases (i.e. products that provide utility) into three categories: clinical, wellness, and lifestyle. Clinical genetic tests help a patient determine whether he or she is at risk of a particular disease, facilitate the matching of specialized medications (often oncology drugs) based on a person’s disease genotype, and are used in fertility and family planning. Clinical tests comprise the majority of genetic tests available today. Wellness genetic tests answer questions related to chronic disease, diet, or exercise, but do not currently provide actionable clinical insights. Lifestyle genetic tests aim to quench a person’s curiosity about him or herself and may not be directly related to health.

Currently most genomics companies provide value to pharma, enabling drug discovery and personalized medications.

Note: Rock Health profiled 64 venture-backed genomics companies that received funding between Q1 2011- Q1 2016

Source: Company websites, Mattermark, Crunchbase, Rock Health digital health funding database

While we have thoroughly explored genomics applications that directly interface with consumers, nearly three-quarters of all genomics companies provide tools (both physical and in the cloud) to pharmaceutical companies and academic research institutions. Scientists and researchers utilize these tools primarily to expedite drug discovery and enable more personalized medicines—with oncology being the most notable application. Although not the focus of this report, life sciences applications promise great potential to impact health (e.g. better sequencing equipment indirectly facilitates more precise drugs).

Genomics companies not focused on pharma currently have fewer opportunities to sell their solutions; only a handful directly sell to consumers.

Note: To qualify for DTC in this report, the company had to transact directly with the patient and exchange both a product and a payment. There are a number of diagnostic companies that sell to patients through providers; these were counted in the “providers and hospitals” segment.

Source: Company websites

Although genomics companies still overwhelmingly serve the life sciences sector, this is subtly shifting as technology powers use cases outside of the research lab. For example, of the roughly forty venture-backed genomics firms selling to the care delivery ecosystem, many focus on enabling a more personalized ecosystem. Syapse, for instance, accomplishes this by providing clinical workflow integration tools, while others, such as InformedDNA, provide an end-to-end genetic testing solution that spans patient matching to counseling. Other companies provide diagnostic solutions, most often related to prenatal testing and oncology drug matching. The vast majority sell to physicians who intermediate between the test and the consumer. Of the few companies selling genetic tests directly to the consumer, most are focused on the ancestry and genealogy market, highlighting the many regulatory challenges in the direct-to-consumer market4.

Only a few genomics companies sell directly to payers or employers5, primarily on the premise that their products deliver healthcare cost savings via improved predictive power. For example, BaseHealth’s platform allows payers and employers to understand population-wide risk factors, using genetic data as one input to mitigate risk. These types of tools are still relatively nascent, likely because of the dearth of evidence needed for large systematic changes.

Business Models

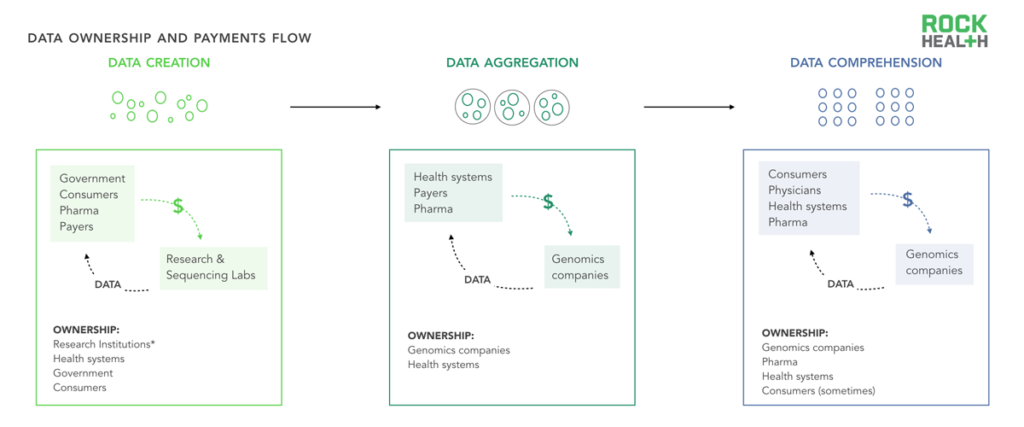

Data ownership and corresponding payments are complex; multiple stakeholders extract and produce value from data throughout the cycle.

Note: *Research institutions and the government may be able to use data in broad ways under informed consent, but may not technically own data

Data comprises the backbone of many genomics business models. In genomics, just as in healthcare, data ownership (which we define as having control over when and how data is used) often exists in a gray zone. Although the Obama administration has issued guidance that patients should have access to their medical records (including genetic test results), the stakeholders that “own” genetic data are not necessarily the entities that interpret or digest that data or are involved in its creation.

As an illustrative example, let us assume that a health system wants to better understand (“comprehend”) the impact of oncology interventions within a given population. To do so, the system may pay a third party vendor to help compile various data sources (“aggregation”) and may rely on its physicians to ask patients to opt into genetic tests or research studies (“creation”). The role of these three stakeholders is critical for the data flow; yet, it is often ambiguous who owns the sample, the deidentified data, or the identifiable data. The health system? The aggregator? The consumer? This case, like many others, would depend on the specifics of the research study and patient consent forms, which may not be salient to the consumer. In addition, the DNA and data itself takes many forms and may be stored physically in gene banks, in the cloud on health system servers, or across multiple sites.

More work is needed to clarify ownership policies not only for consumer privacy and protection, but also for companies whose business model relies on the assumption that they can extract value from owning consumer data6. Companies who enter the genomics space with a data acquisition strategy need to be prepared for the complexity in how data and money are transferred (and need to get comfortable with nebulous regulations that may change).

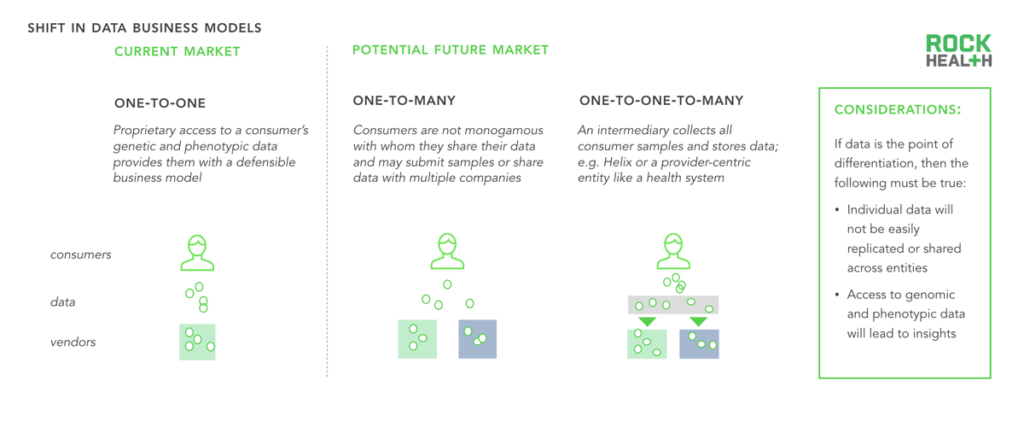

Consumers’ interactions with genomics companies are likely shifting from one-to-one to one-to-many.

The business models of many genomics companies rely on proprietary consumer data (both phenotypic and genetic). Two future data ownership business models could emerge. Today, most consumers are relatively monogamous with a single genomics company and submit a sample only once. However, as tests become cheaper and companies expand and differentiate the value they provide, consumers are likely to share their samples or their processed-DNA with multiple companies. Helix promises a third model, in which a consumer shares a sample once but has access to an infinite number of use cases.

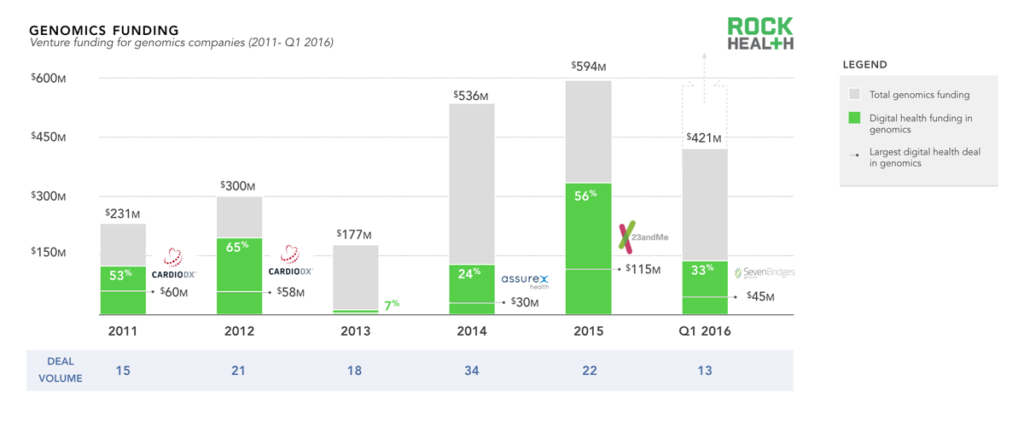

Digital health funding has made up a small, yet steady portion of overall genomics funding due in part to the complexity of the space.

Source: Genomics funding data from Mattermark; through Q1 2016; digital health data based on the Rock Health digital health funding database

Note: only includes U.S. deals >$2M. For the purposes of this report, we did not include basic life sciences tools, synthetic DNA, or gene editing companies

Testament to the potential of genomics is the influx of capital from both private and public funders. We looked specifically at venture funding over the past five years and found an upward trend, with total funding of genomics companies amounting to just over $2.2B7. The recent uptick in 2015 and Q1 2016 was driven by a handful of large deals (Helix and 23andMe both received over $100M in 2015; Grail and Guardant both received $100M in Q1 2016).

While genomics has always had strong life science roots, it has only recently become more integrated with technology and cloud solutions at scale. Funding for digital health genomics companies (genomics companies with an essential technology component8) comprised half of overall genomics funding in three of the five years. Technology continues to drive consumer, provider, and health system engagement by enabling easier-to-comprehend products, more relevant use cases, and better clinical workflow integration. While technological advances in life sciences enable more efficient research, digital health has the potential to facilitate the integration of genomics into healthcare.

Liquid biopsy technology (which promises non-invasive cancer detection) has recently gained attention due to a number of large clinical trials in place and substantial funding events (e.g. Guardant and Grail). Actual clinical adoption is relatively nascent but is expected to expand pending favorable results.

Lastly, although we do not delve deeply into the investors behind genomics, it is important to note that Illumina has been instrumental in propelling the industry forward. Beyond its role as an industry leader, it has spun out two potentially transformational companies (i.e. Grail and Helix), funded a number of early stage startups through its business accelerator program, and plans to do more via its recently announced $100M venture fund (Illumina Venture).

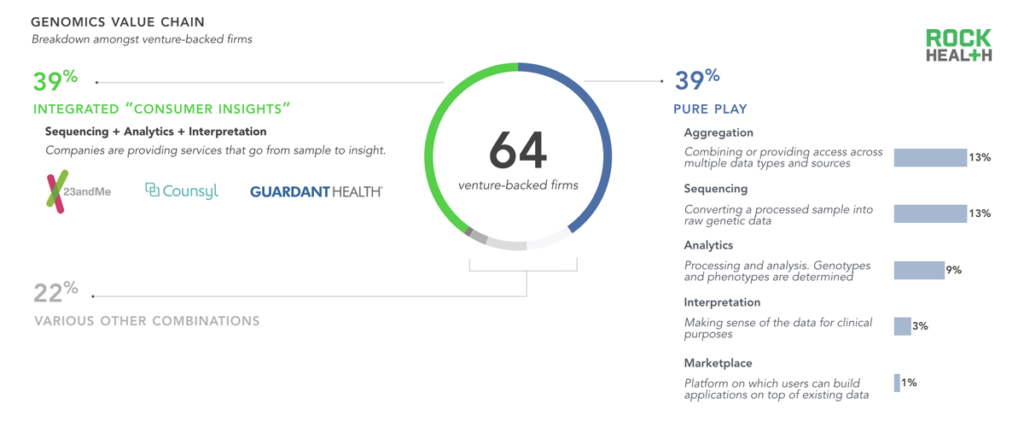

Many niche, fragmented point-solutions have emerged across the genomics value chain.

Note: We did not include sample preparation or processing companies, nor did we include pure life science platforms used for sequencing. Companies profiled received venture funding from Q1 2011- Q1 2016

Sources: Mattermark, Crunchbase, and Rock Health digital health funding database

In order to better understand how companies package their tools and services into products, we analyzed five elements of the genomics value chain: sequencing, analytics, interpretation, aggregation, and the marketplace. Nearly forty percent of venture-backed genomics companies offer a pure-play solution, focusing on only one element of the genomics value chain, while none provide solutions across the entire continuum. One reason for this is that researchers and labs have dozens of highly specific needs, and many vendors choose to meet a specific use case, often only for a handful of clients.

There is substantial demand for a completely outsourced diagnostic solution, and many companies (39% of venture-backed firms) provide a bundled sample-to-insight product for providers and health systems. The majority of firms tackling sequencing are providing ‘sequencing-as-a-service’, often relying on Illumina’s Next Generation Sequencing (NGS) technology for the process itself. No other combination of services exceeded 10% of the sample, suggesting that other offering models fail to capture value or are not currently feasible.

A new element of the value chain has emerged recently: the marketplace. A marketplace is a centralized repository of data that provides broad data access across multiple stakeholders. Marketplaces make it possible for consumers to provide a sample only once, and to continue to derive value from that sample over time as companies provide new use cases and as research emerges on correlative relationships. Helix, which is funded by Illumina and other investors, is the only venture-backed firm at the time of writing to promise a marketplace-like product.

All of these things (sequencing, data aggregation, sophisticated analytics, reaching patients) have been done before, but they haven’t been wrapped up into one before. It’s a matter of bringing things together, not reinventing the wheel.

Dr. Dietrich Stephan, Chairman, Department of Human Genetics, University of Pittsburgh

Novel partnership models have emerged because comprehensive end-to-end solutions have not been feasible.

Note: Partnerships were sourced from 2015-Q1 2016

Source: GenomeWeb and Rock Health digital health funding database

As most companies do not offer end-to-end solutions, genomics is often propelled forward by partnerships. To better understand these dynamics between and across companies, we built a database of roughly two hundred genomics company partnerships (launched between January 2015 and April 2016)9.

The largest category—capturing nearly half of all partnerships analyzed—consists of a product partnership (i.e. a genomics company partnering with another firm). For example, in March 2016, 23andMe announced that its software integrates with Apple’s ResearchKit app, allowing consumers to share their genetic information with researchers. With consumer consent, researchers can analyze participants’ behavioral/phenotypic data (captured via iPhone or Apple Watch through ResearchKit) and genetic data from 23andMe to identify novel genetic correlations10. (Read more on this trend in our The Emerging Influence of Digital Biomarkers on Healthcare report.)

Partnerships between various government organizations and private companies (10% of our database) have largely been spurred by President Obama’s Precision Medicine Initiative, announced in 2015. Initial efforts will focus on expansion of cancer research, followed by research on other common diseases such as diabetes and Alzheimer’s. The White House has agreed to fund the NIH $130M, the NCI $70M, the FDA $10M, and the ONC $5M to facilitate precision medicine in partnership with private companies. For instance, the FDA is working with DNAnexus on precision FDA, which will create a platform for centralizing genetic testing results and ensuring high quality standards.

Pharmaceutical companies have allied with genomics companies to discover new therapeutics or identify genotypic and phenotypic correlations. One of the largest of these partnerships (as measured by the expected length of partnership and number of genomes sequenced) is a ten-year deal announced in April 2016 between Human Longevity Inc. (HLI) and AstraZeneca, in which HLI will sequence 500,000 genomes from AstraZeneca’s clinical trial populations. AstraZeneca plans to use the data to identify new drug targets and add insights to HLI’s Knowledgebase, which HLI claims is the most comprehensive of its kind. AstraZeneca will also have access to the proprietary Knowledgebase to inform clinical trials, augment biomarker discovery, and facilitate drug development.

Lastly, we identified roughly 60 relationships in which health systems and vendors have joined forces (often simply as customer/vendor) to deliver precision medicine effectively. Syapse’s efforts with Intermountain Healthcare and IBM Watson’s work with Columbia University Medical Center highlight two examples in which health systems are leveraging actionable insights from genomic data to personalize oncology treatment plans.

It’s a gold rush into data, and there’s the question of how much value can we add? Let’s make it useful for the patient, first.

Dr. Jimmy Lin, Chief Scientific Officer, Oncology, Natera

Consumer Sentiments

Consumer adoption of genetic testing is key to extracting insights and value from genomics by increasing the amount of information available to researchers. Although interested parties have painted a partial picture of consumer preferences for genomic data, we wanted to provide novel data regarding adoption, willingness to pay for specific use cases, and general trust of companies in the space to help inform company products and offerings.

We surveyed over one thousand individuals who were representative of the US adult population11 in an effort to answer the following: (1) How does adoption of genetic testing differ by use case? (2) What are individuals’ attitudes toward data sharing, ownership, and privacy? (3) Do individuals think about genetic data differently from traditional health data? and (4) How much are individuals willing to pay for knowledge about themselves and their health?

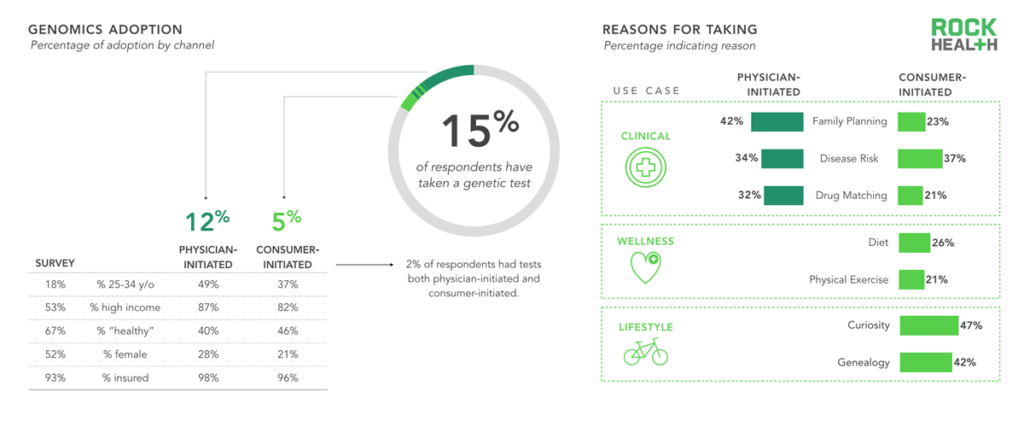

Most consumers had not previously taken a genetic test. Those who had, did so mainly for clinical reasons.

n = 1,060

Note: “Physician-initiated” refers to a test prescribed by a physician; “Consumer-initiated” refers to an at-home kit purchased by the individual

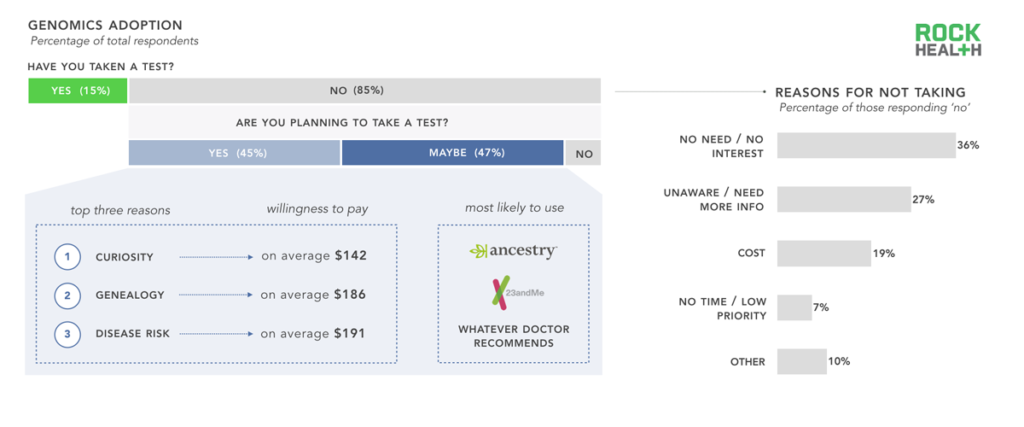

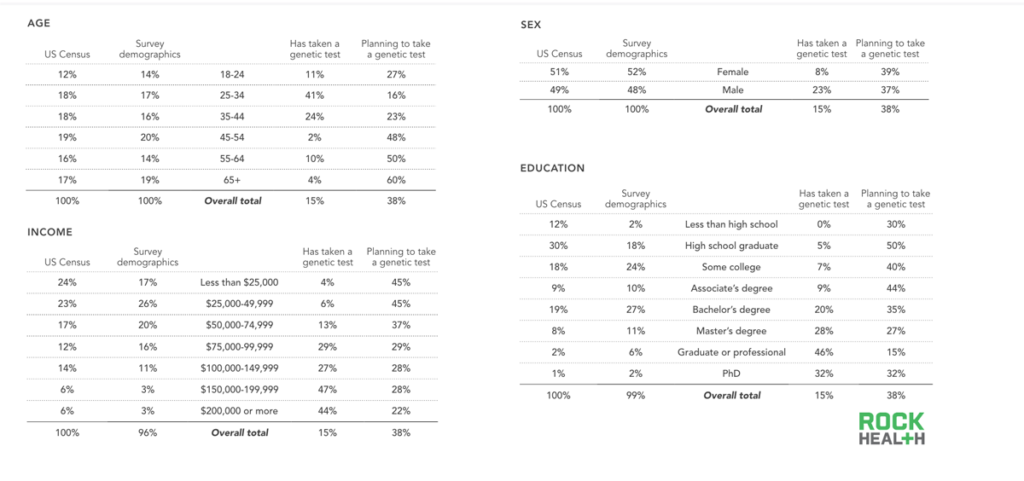

We found that only 5% of our sample purchased a genetic test on their own and that 12% were prescribed a test by their physician. As one might expect, those who purchased on their own did so for wellness and lifestyle reasons related to diet, exercise, curiosity, and genealogy; a large portion sought knowledge about family planning, disease risk, or how a specific drug might react with their genotype.

At least half of consumers were open to taking a genetic test in the future; most sought to satisfy personal curiosity but half wanted to know more about potential disease risk.

n = 1,060

Note: “No” segment represents a combination of both “No” and “I don’t know” responses

The majority of our sample, and US adults overall, have yet to take a genetic test. We were curious as to why. Additionally, we sought to understand what reasons consumers had for planning to take a genetic test in the future. The most common responses to our open-ended question asking why a respondent had not taken a genetic test was that he or she did not see a need to take one, followed by an unawareness about available tests, and a need for more information before ordering a test. Cost was cited as a reason for only one out of every five respondents.

Although many of our respondents who had previously taken a genetic test had done so for reasons related to wellness, the top three reasons for those who planned to take a test in the future were related to curiosity and genealogy (both lifestyle use cases) and/or disease risk (clinical use case). Although numerous newly funded companies are launching tests for wellness use cases, the majority of our respondents did not mention wellness applications as a reason to take a test in the future. While Ancestry.com and 23andMe were the most commonly cited companies consumers plan to use, a large portion of respondents defer to their physicians for choosing a service, regardless of whether the use case was clinical, wellness or lifestyle related.

Our survey suggests that consumers are willing to pay for knowledge about themselves, especially for information that is otherwise opaque.

n= 1,060

Note: Consumers were asked in an open-ended format about willingness to pay for various genetic tests

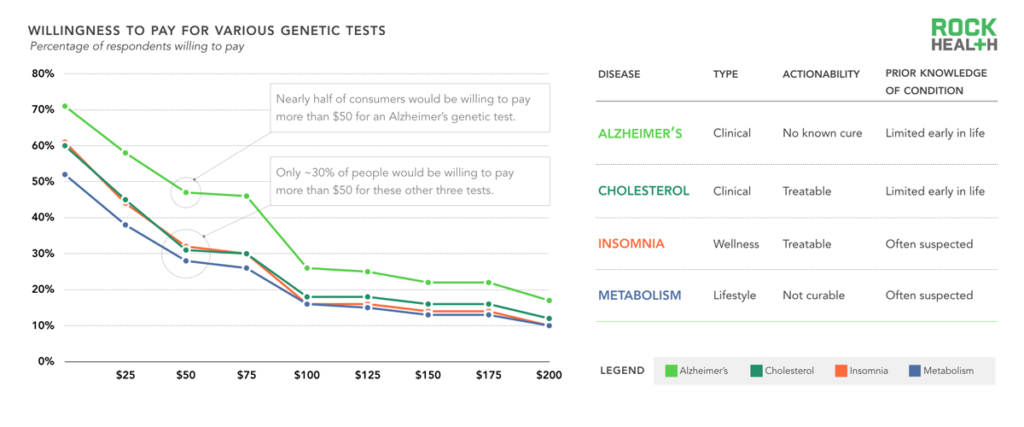

Because of the attention direct-to-consumer tests have received and the gap for incorporating genetic tests in clinical settings, we wanted to gauge consumer receptivity to various condition-based tests depending on the following attributes: (1) The use case (clinical, wellness, or lifestyle) (2) Level of actionability (i.e. does this genetic test lead to a specific clinical intervention?) (3) Prior knowledge about the stated condition (i.e. before the genetic test, how much did a consumer already know?). We asked consumers how much they would be willing to pay for a test that would predict whether they would or would not develop four different conditions (chosen for diversity across our selected attributes): Alzheimer’s disease, high cholesterol, insomnia, or a slow metabolism12.

We found that consumers were much more willing to pay for a genetic test that would tell them whether they would develop Alzheimer’s than they were for tests about high cholesterol, insomnia, or slow metabolism. For example, 47% of consumers were willing to pay $50 for the Alzheimer’s test, whereas only 28% were willing to pay for the metabolism genetic test at that price point. Beyond knowing their family history, people have little insight into their likelihood of developing Alzheimer’s, and a genetic test provides new clues about the future. The fact that there are no known cures and few early treatments for the disease did not seem to deter people’s willingness to pay. People were least willing to pay for a test that provides insight on slow metabolism, likely because the genetic test would not reveal anything previously unknown.

As a final note, we found no difference in willingness to pay whether we asked the question in the affirmative (a test that confirms you will get a disease) or the negative (a test that confirms you will not get a disease).

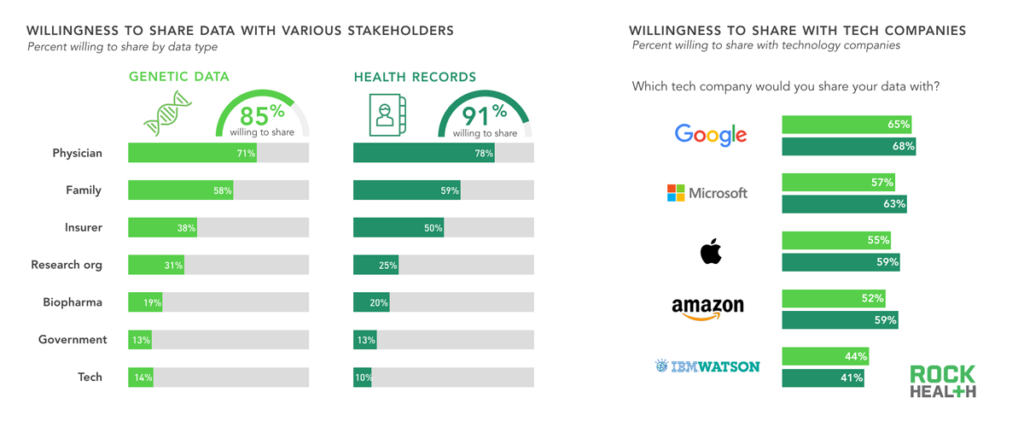

Consumers are much more willing to share genetic data with their physicians and families than other entities; some concerns remain about sharing data with insurers.

n= 1,060

Consumers have a high willingness to share their health records and genetic data, especially with physicians and family members, suggesting that trust plays an enormous role. Consumers were almost as likely to share health data with insurance companies as with family members, but trust for insurers dropped significantly when sharing genetic data. This may stem from concerns about genetic data being used against consumers when obtaining insurance. Although the 2008 Genetic Information Nondiscrimination Act (GINA) specifically forbids health insurers and employers from using genetic data to deny coverage or increase premiums, the act does not cover long-term care insurance or life insurance. Consumer confusion is not helped by state laws that provide varying degrees of protection.

Only 11% of consumers in our survey were willing to share their health data with technology companies, which ranked below pharmaceutical companies and government. Of the technology companies we included in our survey, consumers had the most trust in Google, despite other companies like IBM and Apple having a stronger presence in the genomics field.

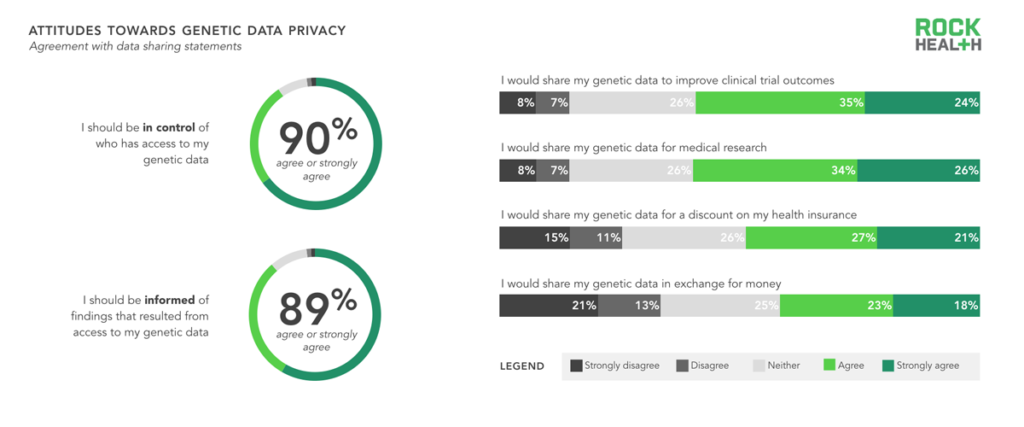

Consumers wanted to be stewards of their genetic data; contributing to the greater good was a stronger motivator than receiving money to share data.

n= 1,060

Nearly 90% of consumers believed they should be in control of who has access to their genetic data, and nearly 89% want to be informed when findings result from accessing their data. However, consumers were still hesitant to share their genetic data—even when offered benefits like lower insurance premiums, improved clinical trial outcomes, and cash. In fact, there was a negative association with receiving money for sharing genetic data. However, as consumers become increasingly responsible for managing their own health (for further reading on this trend, see our Digital Health Consumer Adoption report) and genetic data, it may become more acceptable for them to also receive compensation in return. For now, the best approach for genomics companies continues to be providing consumers with valuable and actionable use cases in return for sample and data submission.

Challenges

A successful $100M revenue genomics company will be one that creates a solution that consumers understand and allows the consumer to be in control of all of their tracked and collected health data. But, how does that exist when data isn’t centralized or interoperable? Interoperability and APIs are the key.

Shahram Seyedin-Noor, Founding CEO/Chairman of Rgenix

As explored previously, consumers derive value from three categories of genetic tests: clinical, wellness, and lifestyle. Despite great interest in genomics, many consumers fail to see a clear value proposition for why they should take a genetic test. The question is: in what ways can the industry increase the number of useful tests available or increase their value to consumers? But the industry faces a “chicken or the egg” problem: to get more useful insights, it needs more data, and to get more data, it needs more consumers to buy in.

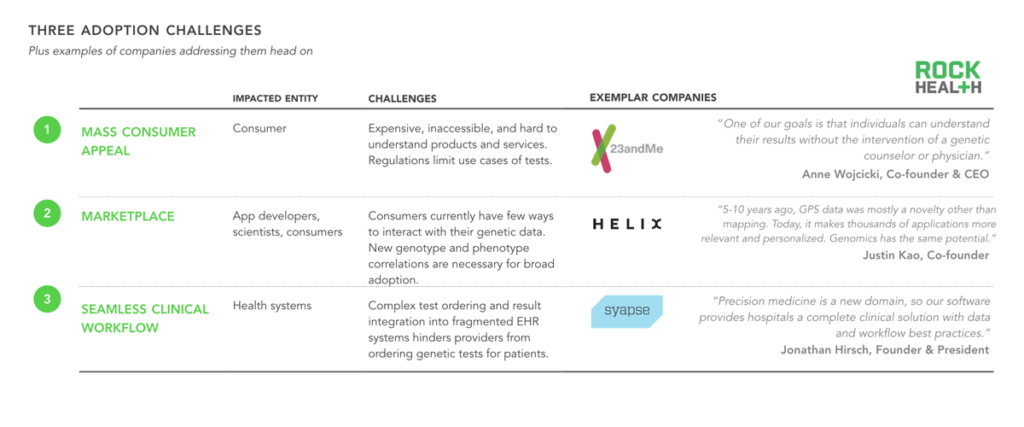

In order to obtain broad consumer utilization, genomics companies need to consider three primary adoption challenges.

After speaking with more than thirty firms, we identified three potential ways to incentivize consumer buy-in. First, companies (such as 23andMe) break down the primary barrier to mass consumer appeal by creating affordable, easily accessible, and enjoyable products that encourage even the most hesitant consumers to buy, due to limited downside. Similarly, companies offering products that generate value long after the genome is initially sequenced (i.e. by providing not-yet-discovered insights at some future point) have an even greater chance of incentivizing consumers to get a genetic test—an endeavor that Helix has set out to achieve. A third approach is one in which physicians and health systems drive data collection. We spoke to several innovative health systems (including Intermountain Healthcare) and found that many providers are recommending that broader patient populations (i.e. beyond specific patient populations, such as oncology) take genetic tests, in advance of traditional payer reimbursement. Intermountain is working closely with Syapse, which makes a product that simplifies the integration of genetic tests into clinical workflow.

Despite technological advances in genomics, human talent is in high demand and required for continued progress in the field.

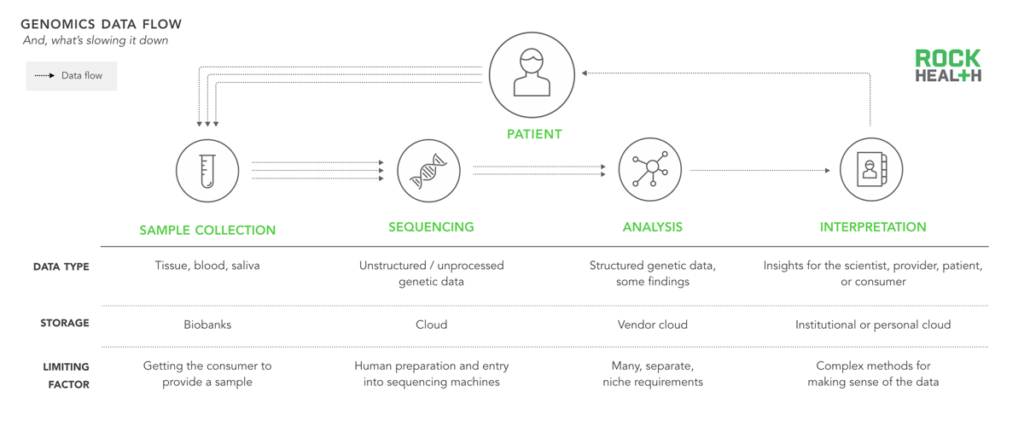

In addition to simply generating more data, the industry needs to improve at every point along the genomics cycle by better digesting, comprehending, and reporting on the value of that data. Historically, progression through the genomics cycle was limited by the high cost of sequencing. But advances in life science technology have pushed sequencing costs down and advances in computing power and storage (e.g. Amazon Web Services) have made processing and storage attainable for most labs.

Based on our interviews, many scientists and engineers agree that the ability to “interpret” or find associations in genetic and phenotypic data has become the rate-limiting step. Although surely some of this can be solved by algorithms, the process requires highly specialized bioinformaticians to undertake a nuanced method for testing each hypothesis they investigate. As Andrew Guo from Omicia stated, “We’re talking about a field in which analysis would take a person hundreds of hours to see which variants are most damaging and relevant.”

Now, assuming that the first two requirements—more (and better) data and interpretation of that data—are satisfied, what remains?

Due to a reduced regulatory burden, companies are more likely to go after wellness use cases first.

Note: GINA is the Genetic Information Nondiscrimination Act of 2008 intended to forbid the use of genetic information in health insurance and employment decisions

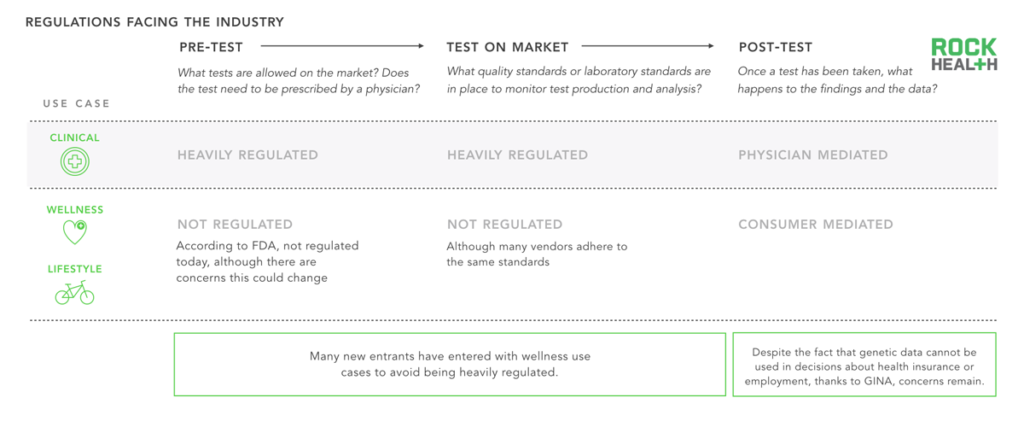

Two of the last remaining hurdles for genomics adoption stem from unclear regulation and limited reimbursement options. Regulations apply to a genetic test before it makes it onto the market (“Pre-test”), while it is on the market (“Test on market”), and after the data and insights have been generated (“Post-test”).

Regulations determining which tests are sold and how information can be used are constantly evolving. Clinical use cases are regulated by the FDA (as we have seen with 23andMe’s public challenges)13; at the time of writing, if a genetic test makes a claim related to diagnosis or treatment of a disease, it must be moderated by a physician and cannot be directly ordered by a consumer. To date, the only act to specifically dictate post-test information usage has been GINA, which states that genetic information cannot be used for discrimination in health insurance and employment.

Beyond the fact that regulation is constantly evolving, it is also important to note that a number of parties are involved, further complicating the process. While the Centers for Medicare and Medicaid Services (CMS) requires Clinical Laboratory Improvement Amendments (CLIA) certification for each diagnostic laboratory, the FDA is responsible for regulating test kits, and the Federal Trade Commission (FTC) oversees potentially false advertising or marketing. Currently, the FDA regulates laboratory developed test kits for whether the test is accurate and reliable (analytical validity), whether it provides medically meaningful results (clinical validity), and whether it provides health information that will be clinically helpful to the consumer (clinical utility)14. Some states have additional regulations that companies must abide by to sell or develop products in their state (e.g. New York).

Due to heavy and constantly evolving regulations for clinical genetic tests, and relatively limited regulations for wellness and lifestyle tests, many early-stage consumer-focused companies choose to enter the market with non-clinical genetic products.

Only clinical-grade genomic solutions operate within the formal closed information and feedback loop of the healthcare system.

When a genetic test operates within a closed healthcare loop (e.g. when a doctor orders a test, the payer reimburses the lab, and the data is inputted into the EHR) the results from the test inform clinical decisions which can be linked to health outcomes. As a result, it is possible to accumulate evidence on the efficacy and cost-effectiveness of tests, which can be used in future care decisions and reimbursement guidelines. Many companies are entering the market with tests focused on wellness and lifestyle to avoid FDA scrutiny; yet, these tests do not integrate with the broader healthcare system. As a result, they miss out on the opportunity for a potential feedback loop and rely on consumers for payment, traditionally a challenging channel.

It remains to be seen whether genetics tests that offer wellness and lifestyle use cases will undergo scrutiny to be offered as clinical tests (i.e. the test itself will still report on the same gene(s), but its application will broaden), whether regulation of wellness tests will become more strict, or whether wellness and lifestyle tests will continue to operate separately from tests with clinical applications. Because healthcare systems stand to benefit from understanding which genetic tests drive clinical value, they are especially well positioned to drive demand for clinical tests.

Closing

Companies that can overcome regulatory, reimbursement, and data hurdles will ultimately provide tremendous value to patients and see big gains. Consumers want and will have access to their genetic data. It remains to be seen whether physicians and experts will continue to serve as intermediaries in making sense of the genome, or whether we will reach a point in which consumers can be stewards of their own data. For now, it is clear that health systems are well positioned to move the needle in genomics, as they collect data and increasingly rely on evidence to drive clinical decisions. As science continues to make sense of the three billion base pairs that comprise the human genome, we’re excited to see its impact on the healthcare sector and on people’s health and well-being.

Informatics tools will become more standardized and the FDA will help push that along. Testing will become a commodity. And interpretation of genetic variants will also become a commodity as free public data sources proliferate.

Lincoln Nadauld, Director of Cancer Genomics, Intermountain Healthcare

Methodology

Source: Rock Health consumer genomics survey data (n = 1,060)

Note: Totals of survey demographics may not add up to 100% due to rounding and due to respondents who preferred not to say

Survey demographics:

- Qualifying population: Individuals with personal Internet access, either at home, work or via their mobile phones were eligible to take the survey. Additional screening was based on demographic requirements.

- Demographic breakdown: With a sample size of n=1,060, respondents were a nationally representative population based on US Census percentages for sex, age, and region. Soft quotas were met for household income and ethnicity.

- Survey timing: The full launch of the survey began on April 28th, 2016 and ended on May 17th, 2016.

Data quality:

- Respondent quality: We employed Toluna to deploy our survey. To ensure data quality, Toluna authenticates all respondents and further validates against third-party data sources including the U.S. Postal Service and telephone directories. Additionally, flash/cookie-based and digital fingerprinting technologies were used to ensure there are no duplicate respondents. Industry standards for screening bad completes were used such as red herring questions and monitoring time for speeders.

- All free responses were reviewed and coded by Rock Health—respondents with invalid answers were not included in overall adoption metrics.

Survey design and analysis:

- Survey design: Rock Health conceived and wrote all questions and materials used in this survey.

- Survey analysis: Findings from the data were based on internal analyses conducted in R.

Acknowledgments

This report would not have been possible without the help of a number of industry partners and startup entrepreneurs who have graciously shared their expertise.

Special thanks to Alex de Winter, Andrew Guo, Brad Kittredge, Daniel Kim, Dhiren Belur, Dietrich Stephan, Erica Jayne Walsh, Gary Kurtzman, Jack Young, Jennifer Turcotte, Jimmy Lin, John Conley, Jonathan Hirsch, Justin Kao, Kaylene Ready, Lyon Wong, Malinka Walaliyadde, Megan Hanley, Nickolas Mark, Othman Laraki, Saji Wickramasekara, Shahram Seyedin Noor, Shivani Nazareth, Shruti Tibrewala, Thomas Metcalfe, and Tod Stoltz for their time and insights.

1 Genome.gov

2 National Coalition for Health Professional Education in Genetics

3 Phenotypic data includes observable or measurable characteristics about a person. E.g. a person’s weight or disease status as recorded in a medical record

4 At the time of writing, Color Genomics offers a clinical test directly to consumers (although the test is technically ordered by an in-house or external physician).

5 There are hundreds of tests on the market that all have varying levels of reimbursement based on many variables (family history, age, insurance contracts, etc.). We did not consider reimbursement to constitute a customer relationship for the purpose of this report.

6 For example, Human Longevity Inc. (HLI) seeks to create the largest genomic database and sell information to biotech/pharma companies and academic centers.

7 We excluded funded related to pure life science tools, synthetic DNA, and gene editing. We utilized the Rock Health Digital Health Funding Database and MatterMark data for our funding data and deals numbers.

8 We specifically considered genomics companies that leveraged software as a critical component of their business model or offered an web/mobile interface or product as “digital health”

9 The typical length of these partnerships span years. However, only partnerships that were announced in the last year were included.

10 This partnership is supported by Stanford University, the Icahn School of Medicine at Mount Sinai, and an app developer named LifeMap Solutions.

11 More details on our survey can be found in the methodology section

12 Each respondent was randomized to answer either the affirmative (a test that confirms you will get a disease) or the negative (a test that confirms you will not get a disease) for each condition. We found no difference in willingness to pay across the two.

13 FDA granted approval to market carrier status testing direct-to-consumer and classified these tests as Class II devices.

14 Genome.gov