2017 Year end funding report: The end of the beginning of digital health

Executive summary

2017 was a record-smashing year for digital health, with venture funding approaching $6B and the most mega deals ($100M+) to date. While investor appetite certainly increased in 2017, exits waned with only 119 disclosed acquisitions of digital health companies and a surprising zero IPOs. However, there are more highly-capitalized, privately-held companies than ever, and investors are anxious for potential exit opportunities.

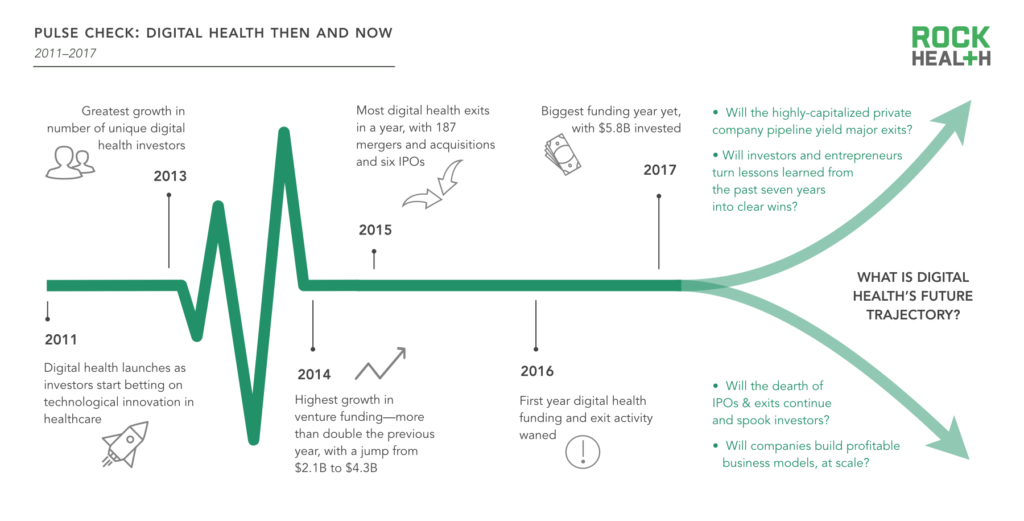

Looking back over 2017—and the seven years since we began tracking funding in 2011—it’s clear that the early game has concluded and digital health is entering the “middle innings” as an investment sector. We’re at the end of the beginning of digital health.

Over $23B flowed into digital health startups over the past seven years. But the early years—2011 and 2012—each represented just 5% and 7% of that total, and “steady state” investment levels took hold starting in 2014. The far larger cohort of companies fundraising between 2014-2016 is maturing, and 2017 arguably saw more mega deals simply because there exists a greater number of mature companies in search of large investments. However, the argument that the expected trajectory of these companies alone is driving 2017 investment levels is a bit simplistic. Investors do, after all, have a choice in where they deploy their capital.

In that vein, not only has the size (and number) of late-stage mega deals hit a peak, but so has the number of repeat digital health investors. Moreover, it’s worth noting that the record year in digital health funding occurred even in the face of substantial political turmoil, with healthcare policy playing a leading role in a hard-fought, high-stakes political battle at a national level. Conventional wisdom would expect this backdrop to surround a market crash or credit crunch—not a banner year. All of this points to a committed (or at the very least, dogged) investor base.

Despite notable achievements, investors and entrepreneurs face the challenge of a frozen IPO market, with zero digital health IPOs in 2017. Though cold comfort, they’re not exactly alone: you have to go back to the 1960s to find a time when there were fewer companies listed on American stock exchanges. Additionally, the number of and trend in IPOs per year are uninspiring. Finally, as public market investors stampede toward passively managed funds, there are fewer (and usually larger) “active funds” to act as buyers in future IPOs. The secular trends in American capital markets represent a headwind for public listings as a source of liquidity for private investors. So far, digital health has been subject to the same law of gravity. For now, at least, M&A is the new digital health IPO.

Those digital health companies already in the public markets have fared well, outperforming the S&P 500 31% to 19% in 2017.

We count ourselves among the committed investors who firmly believe there’s still plenty of room to make healthcare massively better for every human being. For us, 2018 represents the end of the beginning in digital health, the start of a new era with new challenges—not the beginning of the end.

Our growth in 2017

Much like digital health at large, Rock Health has grown. We continue to look for ways to better serve our community by sharpening our ongoing analysis of the digital health space. In 2017, we significantly expanded the information we track on every venture deal and company—including the company’s value proposition(s), clinical indication(s), business model(s), and differentiating technology(ies)—in the Rock Health Digital Health Funding Database. We are excited to announce the release of the updated database and debut new insights for entrepreneurs, investors, and innovators within major healthcare companies looking to better understand emerging trends in digital health. Stay tuned for an upcoming blogpost that highlights the key changes and valuable analyses we now support.

Dollars and deals

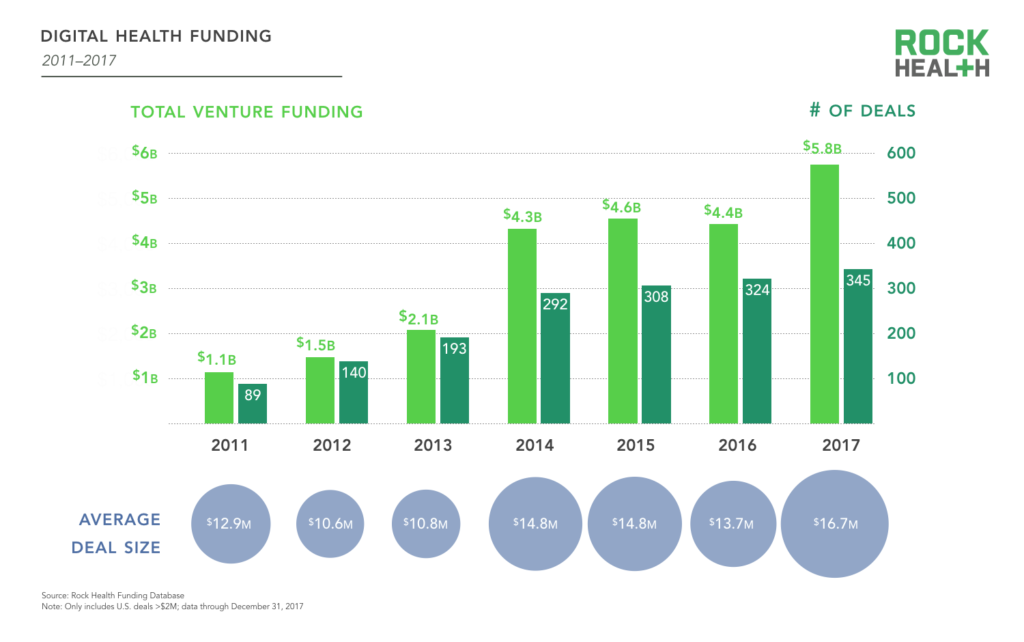

Annual funding of digital health companies surpassed $5B for the first time ever in 2017.

2017 saw the greatest amount of funding being poured into digital health to date, with a steady but not dramatic increase in completed deals. More deals alone didn’t drive the steep funding jump. Rather, we saw investors in the space get more comfortable, confident, and willing to make larger investments in digital health companies. In fact, Outcome Health and Peloton Interactive raised the largest digital health investments on record at $500M and $325M, respectively. Boosted by these mega deals, the average deal size hit an all-time high of $16.7M.

Source: Rock Health Funding Database

The 2017 funding total comes with one significant caveat. Despite its midyear momentum, Outcome Health now faces serious allegations which have led to a Department of Justice subpoena, an investor lawsuit, and a buyout/severance package for over one third of its employees. But even without Outcome Health’s blockbuster deal, 2017 digital health funding is still the largest yet (by a landslide), demonstrating an undeniable growth in investor appetite. It’s hard to predict the repercussions of the Outcome Health allegations on the industry, but they may result in increased investor scrutiny. This is a welcome development, and the pace of funding in 2018 may temper in the absence of another $500M deal (a rarity).

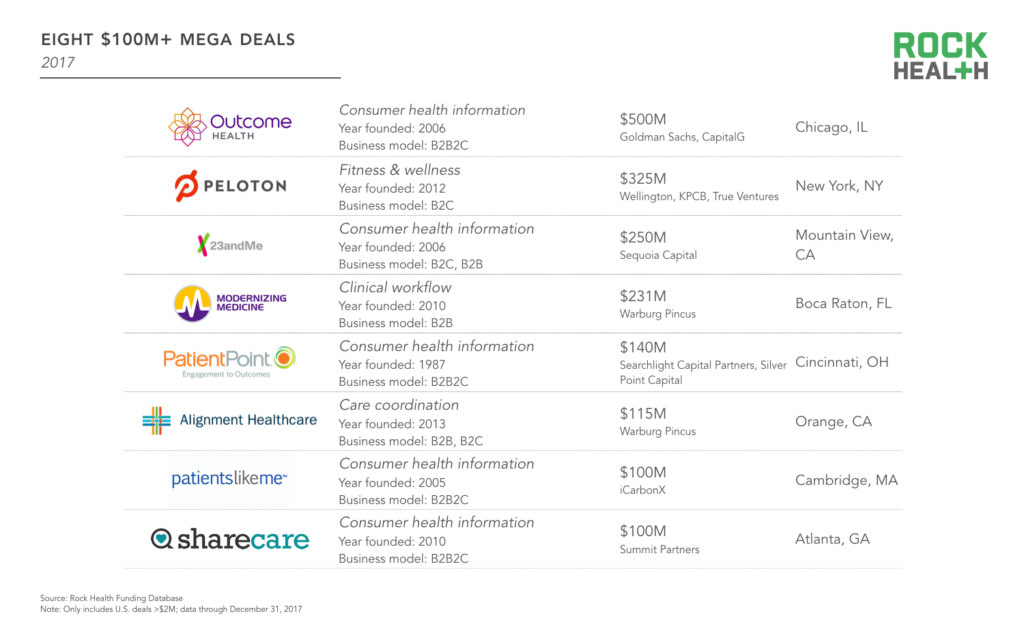

After a record-breaking seven $100M+ mega deals in H1 2017, only 23andMe raised a $100M+ deal in H2.

Collectively, the eight mega deals in 2017 represent 31% of total digital health funding for the year. These mega deals were raised by digital health companies across the US—only two are headquartered in California. Several of the companies were more mature, established players, with an average company age of 11 years.

Despite a record seven mega deals in the first half of 2017, there was only one mega deal in the latter half—$250M to 23andMe (the company’s second such mega deal, contributing to the $423M total raised since 2011). Its genetic testing kits were among Amazon’s top five sellers on Black Friday 2017, with many consumers jumping at its reduced price. Coinciding with the gift-giving season, recommendations from the FTC urged consumers to consider the privacy implications of at-home DNA test kits.

Source: Rock Health Funding Database

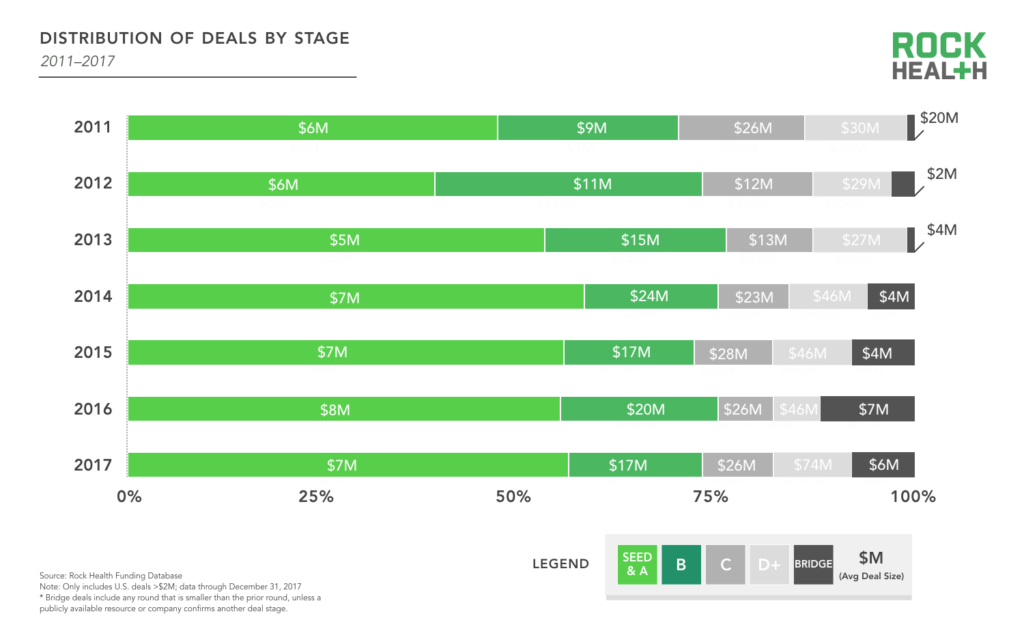

Driven by mega deals, the average deal size of Series D+ deals increased by 60% in 2017.

The overall distribution of 2017 funding across company stages mirrors that of previous years—Seed and Series A deals continue to account for the majority of deals. However, the average size of Series D+ deals skyrocketed, increasing by 60% to $74M per deal. If we run the analysis excluding the Outcome Health deal, the size of the average Series D+ deal still grew sizably to $60M, suggesting investor comfort in participating in big rounds for companies with proven track records.

Source: Rock Health Funding Database

Top value propositions

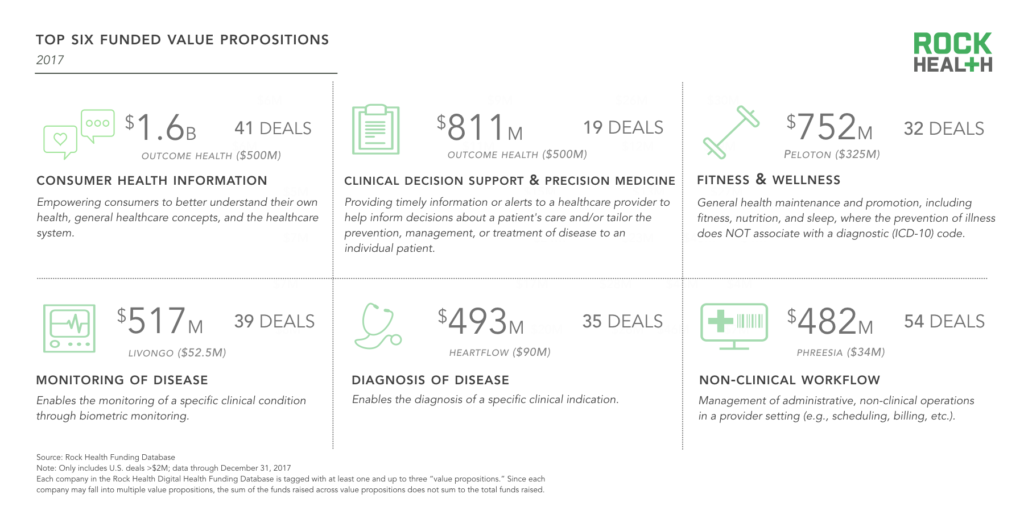

As part of our update to the Digital Health Funding Database, instead of assigning each company to a single category, we now track each company’s value proposition(s), differentiating technology(ies), relevant clinical indication(s), paying customer segment(s), and end user segment(s). As such, the following section is the first time we’ve reported on the most-funded “value propositions” (the complete analysis of funding by clinical indication, customer segment, etc. is available in the full report).

Companies delivering consumer health information as a primary value proposition dominated the year’s funding.

Source: Rock Health Funding Database

Note: Each company in the Rock Health Digital Health Funding Database is tagged with at least one and up to three “value propositions.” Since each company may fall into multiple value propositions, the sum of the funds raised across value propositions does not sum to the total funds raised.

In 2017, consumer health information was the most funded value proposition, bolstered by five of the eight mega deals. While Outcome Health carried the category with the largest deal, consumer health information would have topped the charts regardless. Other deals within this value proposition include: PatientPoint, which employs tablet- and screen-based media to enhance patient-provider discussions; 23andMe, which provides individuals with their genetic health risk; and ShareCare, which uses surveys to assess wellness and answers questions based on symptoms. While employing different modes of communication, these products deliver information to consumers to manage their own health while navigating a complex health system. Large tech companies also view this space as ripe for innovation. Amazon is exploring the use of Alexa’s voice-enabled technology to deliver health information for common issues, and Apple is working to make the omniscient iPhone a central location for patient health records.

Companies advancing the next leading value proposition, clinical decision support & precision medicine, raised half the amount of funding ($811M) that was raised by consumer health information companies ($1.6B). Over the last two years, as investors have pursued solutions delivering tangible clinical impact, investment in monitoring, treating, and diagnosing diseases has increased within each category (ranging 60-115%).

Investors

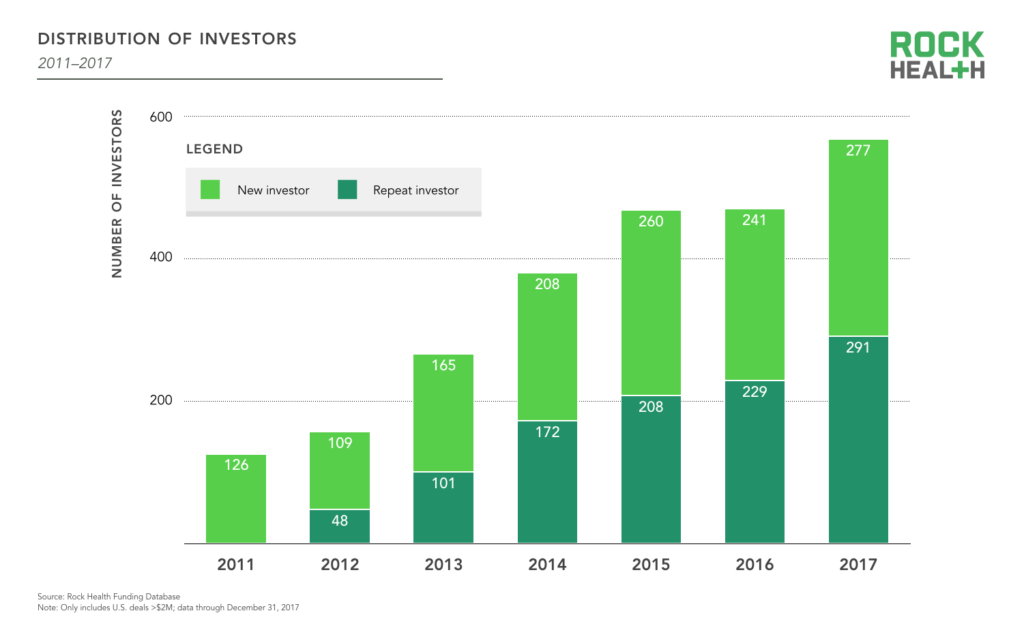

There are more repeat digital health investors than ever before.

In yet another sign that digital health has entered the “middle innings,” for the first time ever, more than half of the year’s digital health investors are repeat investors who have participated in at least two digital health deals since 2011. These deals were a mix of new and follow-on investments (in which investors “double down” on earlier investments).

Source: Rock Health Funding Database

Overall, there were also more unique investors in 2017 than in previous years, and it was the first year in which more than 500 unique investors funded digital health companies. It remains to be seen whether the 49% of investors who are new will continue investing in this space. Investor excitement can quickly deflate if they do not see monetization, meaningful outcomes, and notable exits. Vijay Lathi, a managing director at New Leaf Venture Partners, expects continued energy and investment in digital health, saying, “The overall objective of higher quality care with greater efficiency and lower costs is an irrefutable value proposition in healthcare today.”

Exits

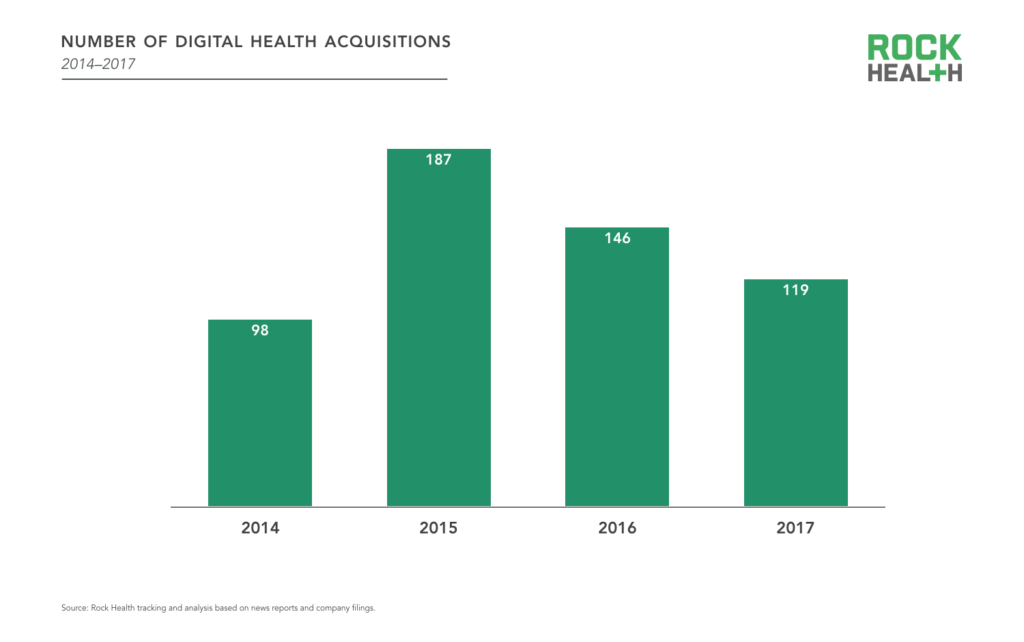

Despite a record year in funding, M&A transaction volume in 2017 dropped significantly to 119 deals.

The number of disclosed mergers and acquisitions declined for the second year in a row. 2017 closed with 18% fewer digital health M&A deals than 2016 and 36% fewer than 2015, when M&A activity peaked. Leah Sparks, Co-founder and CEO of Wildflower Health, remarked, “The big companies are going to wake up and realize they have to buy innovation—they can’t create it internally. However, the long sales cycle may just mean that few companies are yet at a scale from which a large enterprise can capture value by acquiring.”

Since 2015, companies focused on enhancing EHR functionality and/or improving the clinical workflow have been the most likely to be acquired. It has been four years since the EMR mandate went into effect, requiring hospitals to demonstrate meaningful use of an electronic medical record in order to maintain Medicare and Medicaid reimbursement rates. With penalties for noncompliance rising, we are seeing continued interest in companies serving this space.

Source: Rock Health tracking and analysis based on news reports and company filings.

Surprisingly, not a single digital health company raised money on the public markets in 2017.

While 2014 and 2015 saw an uptick in digital health IPOs, they completely halted in 2017, without a single digital health company entering the public market since iRhythm’s October 2016 IPO.

It’s noteworthy that there were no IPOs in light of the fact that 2017 also saw the greatest number of mega deals to date. With both more and larger pre-IPO rounds, investors face the pressure for exit activity in the upcoming 12 to 24 months. Among those digital health companies that have IPO’d in prior years, each company, on average, waited ten years and raised $136M before entering the public markets. A handful of private companies (e.g., 23andMe, PatientPoint, and ZocDoc) meet both of these benchmarks and have raised mega deals since 2011.

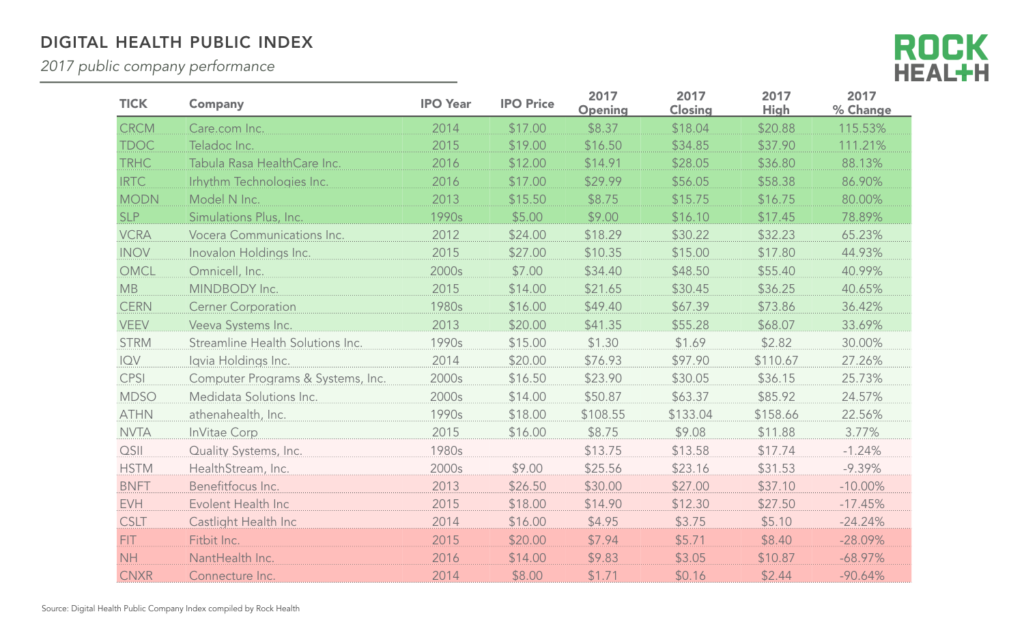

Despite no new entrants, the Digital Health Public Company Index fared well in 2017.

In 2017, the Digital Health Public Company Index outperformed the broader S&P 500 public market index.

2017 was a big year for the stock market overall, with the S&P 500 up 19%. Despite uncertainty in the political environment, the economy thrived. And despite the uncertainty of healthcare reform, the Digital Health Public Company Index did even better, beating the S&P 500 in its performance and growing by 31%. The biggest market winners of 2017 were Care.com, and Teladoc. Teladoc in particular saw an increase in value after its inaugural investor and analyst day in November 2017. Both of these companies more than doubled in share price over the year. Overall, 18 of the 26 public digital health companies’ stock prices went up in 2017. Of note, the number of digital health companies included in the index shrunk from 27 to 26 in 2017 due to KKR’s buyout of WebMD. While an overwhelmingly positive year for the Digital Health Public Company Index, some digital health companies saw their stock price plummet—in particular, Connecture and NantHealth lost more than half of their value in 2017.