2020 Midyear digital health market update: Unprecedented funding in an unprecedented time

What a long, strange, and harrowing six months it’s been. At the end of 2019, many of the digital health focused venture funds we spoke with were focused on macroeconomic conditions and concerned about the effects of a potential economic downturn. We’re confident none of them expected the first half of 2020 to play out like this: a record high for the Dow in February 2020 was followed by the end of a 10-year bull market, unemployment rates unlike anything since the Great Depression, and the biggest rally in stock market history. Amidst this volatility (and contrary to our predictions), US digital health venture funding is on track to set annual records for overall funding, number of deals, and average deal size.1

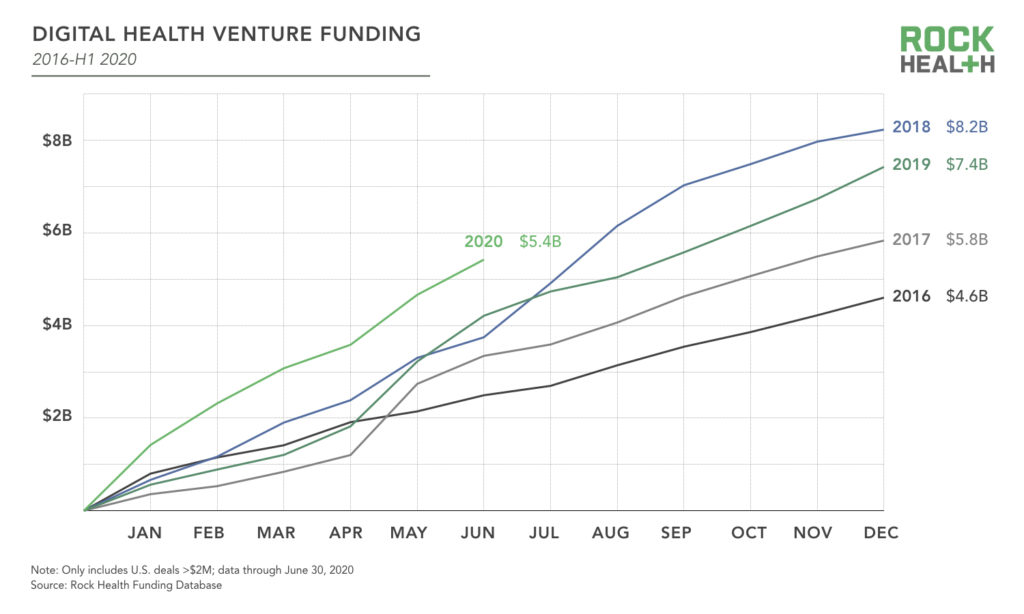

Digital health funding had a wild ride through the first half of 2020. After coming out of the gates quickly with a record $3B in funding in Q1, digital health investment—and overall venture funding—hit the brakes in April as COVID-19 spread rapidly around the globe. But investors came roaring back into digital health in May as several regulatory and reimbursement barriers to digital health adoption were brushed aside in a rush to keep healthcare systems operational in the midst of the pandemic. In fact, H1 2020 saw more funding than any previous first half of the year (from 2011-2019), ending at a record $5.4B—beating the prior record of $4.2B set in H1 2019.

The story is just getting started. On the one hand, the US officially entered a recession in February, and predicting the spread of COVID-19 and its impact on global supply chains, consumer sentiment, and public and private markets remains highly uncertain at best. Financial market uncertainty is hard to overstate, with even near-term economic forecasts having been thrown into a jumble. In just one example, the consensus estimate for U.S. monthly unemployment, a bellwether for investors and policy makers alike had the largest margin of error ever—over 30 times the second-largest estimate error (318,000 jobs, set in February 2003)2. Added to this uncertainty, a potential second wave of the virus could quickly reverse the Q2 public market rebound and growth in private digital health investment. While the pandemic appears to have stoked investors’ appetite for digital health companies in particular, their focus could shift in a longer term economic downturn.

On the other hand, there’s never been a greater need—or demand—for technology-enabled healthcare, a viewpoint the digital health investor community has so far this year resoundingly affirmed.

We’ve taken stock of an unprecedented six months, starting with a deep dive into the Rock Health Funding Database. This post explores the digital health investment landscape, highlighting who’s investing and where their dollars are going with an eye (as always) on exit activity. We also examine two underlying investment areas that are driving the trend in greater depth. On-demand healthcare services and disease monitoring received a significant amount of investment—an unsurprising trend given healthcare’s COVID-19-driven shift towards virtual care. Separately, we examine the significant upswing in behavioral health investment thus far in 2020—a trend we believe has staying power beyond the pandemic.

We spoke with a wide range of colleagues and collaborators at leading healthcare companies as well as fellow investors at prominent healthcare-focused venture funds. We heard from them, in equal measures, a sense of surprise at how quickly things have changed, of anticipation on the future of the market, and of resolve that this crisis ought not go to waste.

Go deeper with leaders from Rock Health, Bessemer Venture Partners, Kaiser Permanente Ventures, and Fenwick & West on 7/30 in a live conversation about the outlook for digital health. RSVP here.

What? Overall digital health funding is on pace for a record high in 2020?

At the end of Q1, we anticipated a swift, pandemic-driven slowdown in digital health funding, and predicted a dearth of digital health IPOs for the remainder of 2020. Through April, this held true. But May and June surprised on the upside, with a significant uptick in investment. Our own experiences as an investor through H1 and those of the other investors we spoke with for this report suggest three possible reasons for the downswing—and the subsequent reversal.

- First, investors slowed the pace of investment in March and April perhaps as much because they needed to turn their time and attention to the needs of their existing portfolio as out of risk aversion. Triaging their existing portfolio, working with portfolio executives to update financial and strategic plans, and reallocating reserves based on a rapidly-changing environment took first priority. With only so many hours in a day, fewer deals were completed.

- Second, price uncertainty—particularly in later stage deals where public market volatility is a more proximate influence—temporarily chilled enthusiasm and, in some cases, undid deals that had otherwise been in flight. Late-stage deals are, by definition, larger in size, potentially driving the drop in overall funding in April and May.

- Finally, the record rally and reduced volatility in public markets (for now) warded off concern over financial-system instability (and a replay of the Great Financial Crisis). Paired with loosened digital health regulations and a COVID-19 driven surge in demand for digital health solutions, this may explain the reversal of the trend from “down” in late Q1 to “up” in May and June.

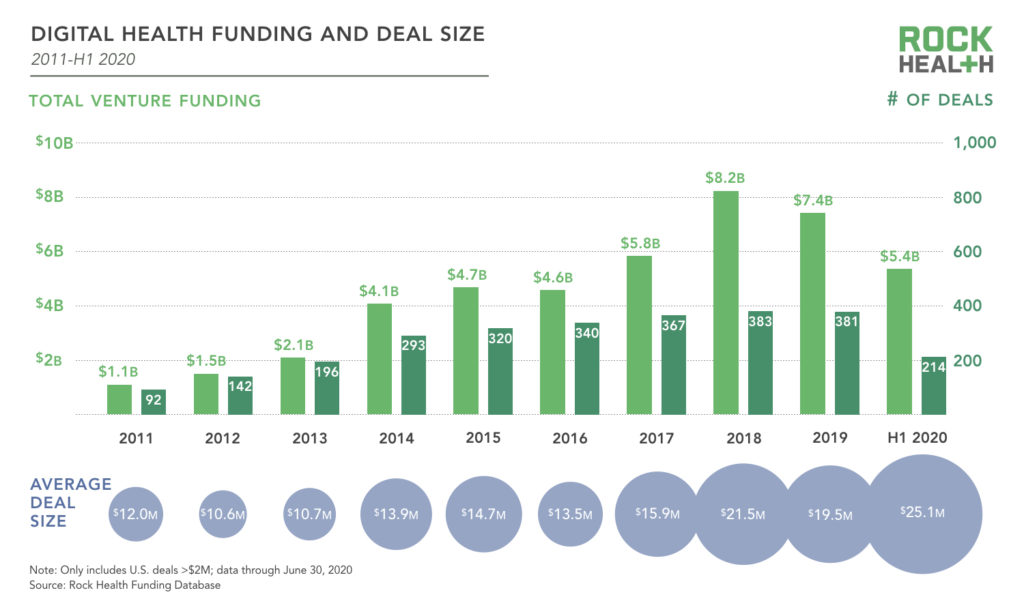

The reversal was significant. Overall digital health funding in Q2 was $2.4B, 33% higher than the $1.8B quarterly average for the prior three years. And average deal size in the first half of 2020 was $25.1M, well above the previous record of $21.5M set in 2018.

The breakdown of investors in 2020 is similar to prior periods, with traditional venture capital firms accounting for 67% of digital health transactions, two percentage points higher than in 2019. Corporate venture capital remained stable, accounting for 14% of total transactions.

Eleven $100M+ mega deals led the way for digital health in H1. Notably, five of these deals occurred in May and June, well into the COVID-19 outbreak and resulting economic downturn in the US.

- ClassPass raised $285M in a Series E in January to expand their global presence and product offerings, connecting users to in-person fitness classes. ClassPass then quickly pivoted to offer a catalog of pre-recorded classes and enabled partners to host virtual classes

- Alto Pharmacy provides a full-service digital pharmacy and prescription delivery service and raised $250M in a Series D in January

- Amwell raised $194M in May to meet increasing demand for telehealth services as a result of COVID-19

- Element Science, which makes a wearable defibrillator that stems cardiac arrest, raised $146M in a Series C in March

- Insitro, an AI-driven drug discovery platform, raised $143M in a Series B in May

- DispatchHealth, which provides on-demand urgent care services, raised $136M in a Series C in June

- Outset Medical, a durable medical equipment company that delivers a connected dialysis system, raised $125M in a Series E in February

- Cedar, a developer of a software platform for health systems to manage patient payments, raised $102M in a Series C in June

- Mindstrong Health, which built a platform to deliver evidence-based therapy and psychiatry, raised a $100M Series C in May

- Tempus raised a $100M Series G in March to redefine how genomic data is used in a clinical setting

- Verana Health raised $100M in a Series D in February to become the “Google for physician-generated healthcare data”

Rock Health portfolio companies raised a total of $290M in the first half of 2020—Avive, Benchling, DrChrono, Evidation, Omada Health, Virta, Vivante Health, and Wellth all closed deals to support healthcare’s changing landscape.

Corporate venture capitalists closed more deals than expected in late H1 2020

Corporate venture capital funds (CVCs) didn’t watch from the sidelines as digital health investment rebounded in May and June. CVCs invested aggressively despite the uncertainty and deep financial stress facing many incumbent healthcare organizations in H1 2020. “Strategic investors” have held steady so far this year, completing 76 transactions in H1 2020 (on pace to equal CVC deal count in 2019 which had 143 transactions overall). CVC investment surged in May with a spike of 28 transactions, which was 150% above the trailing 12 month average—beating the previous record of 26 transactions set in November 2017. We speculate that rather than pressing pause on strategic initiatives and waiting for a sense of normalcy to return, CVCs may view this crisis as an opportunity to accelerate bets on digital health companies that they believe will help them navigate the post-COVID world.

In H1 2020, provider organizations (primarily health systems) accounted for 34% of all corporate venture digital health transactions, making them the largest single source of CVC participation. Simultaneously, providers have been hit particularly hard by the pandemic—inpatient services like elective procedures have been delayed and hospitals have had to re-allocate resources to prepare for and treat patients with COVID-19. Despite these challenges, provider venture capital funds have continued to invest frequently throughout the first half of 2020 and are still the most active strategic investment segment in digital health. We’ll be keeping a close eye on how this segment changes as potential second and third waves may impact the amount of dedicated funding available.

Corporate venture capital funds invested in startups with similar value propositions this year compared to recent years, namely companies that provide consumer health information, on-demand healthcare services, precision medicine, and research and development solutions. Though we heard from a number of CVC investors in the early weeks of the pandemic that they were likely to change course, from every angle, the data suggests that CVCs as a group maintained “current course and speed” through the hurricane of H1 2020.

Technology will be crucial for companies to differentiate and to compete effectively; for example, tools to track quality metrics, like reporting, under VBC payment models as well as tools to address and track the consumerism of healthcare, like the digital front door.

—Fei Ren, Vice President, The Riverside Company

Capital concentration and growth in late-stage funding accelerates (despite or because of COVID-19?)

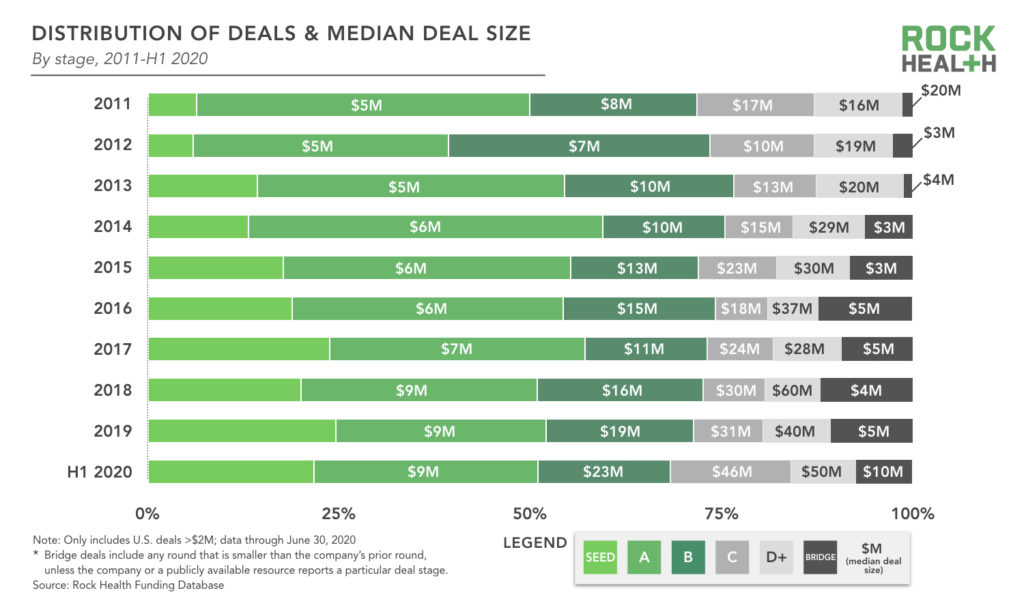

While industries across the board were bracing for the impact of COVID-19—overall VC funding came in at $34.2B in Q1 2020, similar to the quarterly average of $34B set in 2019—digital health funding hit a high of $3B during Q1 2020 in comparison to the $1.9B average in 2019. Average deal size in the first half of 2020 for digital health startups was 29% higher than in 2019 overall. This sign of a maturing market is something we’ve commented on prior to the pandemic. We observed an acceleration of this trend during H1 with larger funding rounds in established, late-stage digital health companies fueled by investors pursuing certainty in an uncertain environment—likely a sign of the proverbial flight to quality. The data supports this view with the median deal size for Series C and higher reaching record highs compared to 2019.

However, smaller firms looking to identify funding need not fret, as the top of the funnel remains active. Seed and Series A deals continue to represent over 50% of all deals (by count), a trend that goes back to 2013.

A continued downward trend in M&A clouds the path to liquidity for investors, but public digital health companies are thriving as the market rebounds

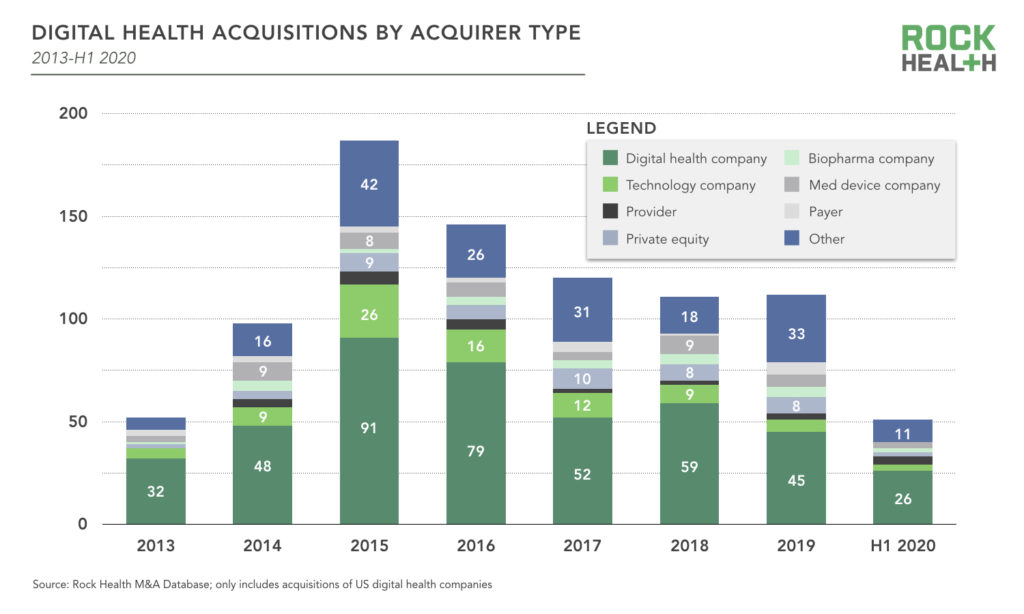

M&A remains the most common source of liquidity for digital health investors. Fifty-two US digital health companies were acquired in H1 2020, continuing the downward trend in digital health M&A since its peak in 2015. Across industries, funds have pressed pause on many potential deals as they assess market recovery timelines and work to conduct due diligence remotely. Despite this slowdown, investors have generally supported acquisitions that strengthen market position, with several deals announced this year. Notably, digital health companies were the acquirers in 52% of digital health acquisitions this year, twelve percentage points higher than in 2019.

Digital health companies are looking externally to acquire additional capabilities and talent to expand their scale. Several notable deals (and near-final deals) in H1 followed this trend:

- Teladoc acquired InTouch Health for $600M in stock and cash in January to expand its provider-facing capabilities for their telemedicine platform.

- Lululemon acquired Mirror for $500M in June to continue its expansion beyond retail and further into digital fitness services.

- Optum is in advanced talks to buy AbleTo for $470M to expand its virtual behavioral health capabilities.

- Omada Health acquired Physera for $30M in May, adding virtual musculoskeletal services to its care offerings.

- Health Catalyst acquired Able Health for $27M in February to enhance their quality and regulatory measure capabilities.

- Virgin Pulse acquired Blue Mesa to expand its employer offering to include remote diabetes care and prevention in its existing platform offering.

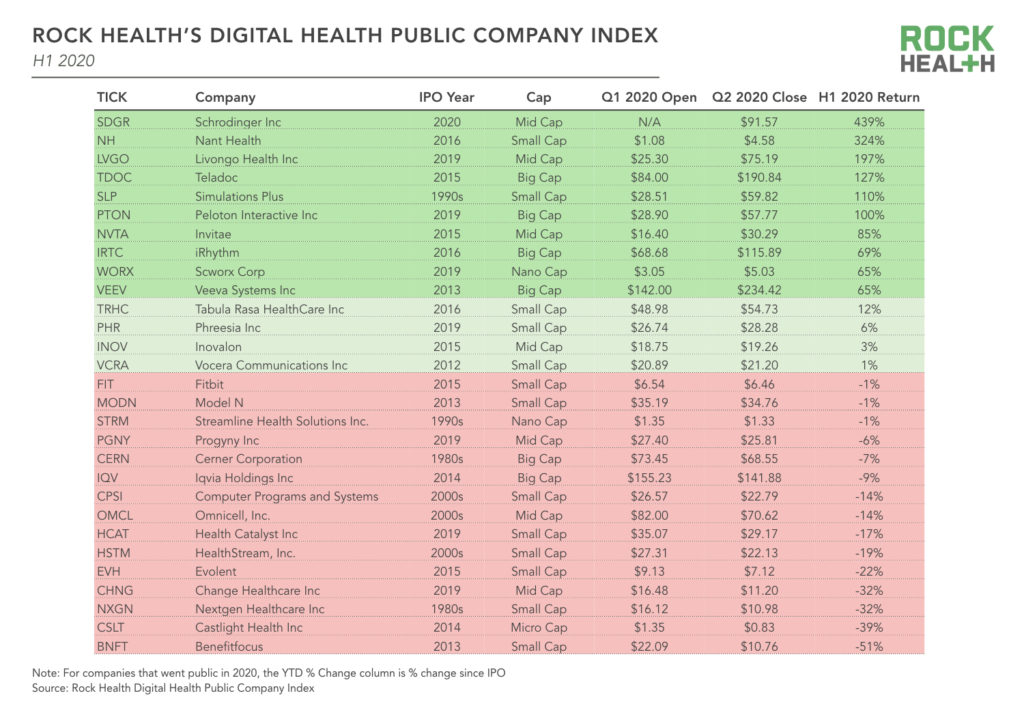

Surging public markets improve the outlook for current and future public digital health companies

At the end of Q1, the IPO outlook was grim. Outside of digital health, Airbnb—the expected darling of the 2020 IPO class—delayed its plans for an IPO and raised another $1B in private funding as its valuation fell. Suffice it to say expectations for digital health companies on our IPO watchlist were being monitored carefully to see who would be able to pivot and support COVID-19 relief efforts. However, the surging stock market and telehealth adoption have paved the way for Amwell—fresh off an additional $194M round—to go public this fall. Teladoc, one of Amwell’s key competitors, reported 41% year-over-year revenue growth and a 92% increase in new users on its Q1 earnings call, which bolstered its already rising stock price. Also looking to go public is GoHealth, which offers a Medicare-focused health insurance marketplace, with hopes of raising $100M in its IPO later this year. Accolade, which offers a health benefits platform for employers, raised $220M in its July 2nd IPO, debuting at $22 per share and a $1.2B valuation.

The Digital Health Public Company Index gained 30%3 in the first half of 2020—soaring above the S&P 500’s 4% loss on the year, despite a historic second quarter. After a three-year IPO drought starting in 2016, eight digital health companies have entered the public market in the last 12 months (Accolade, Livongo, Health Catalyst, Phreesia, Change Healthcare, Peloton, Progyny, and Schrödinger). This class (aside from Accolade which went public at the start of Q3), has performed particularly well as the markets bounced back in Q2 2020. The combined market cap for the six 2019 IPOs as of June 30, 2020, is $27B, which is 50% higher than it was at the end of 2019. Schrödinger, which went public in February 2020, is up 439% from its price at IPO.

The public market for digital health companies will continue to be robust with more money moving to later rounds encouraging more companies to consolidate or go public.

—Keith Figlioli, General Partner, LRVHealth

On-demand healthcare services and remote monitoring drives the industry to virtual care

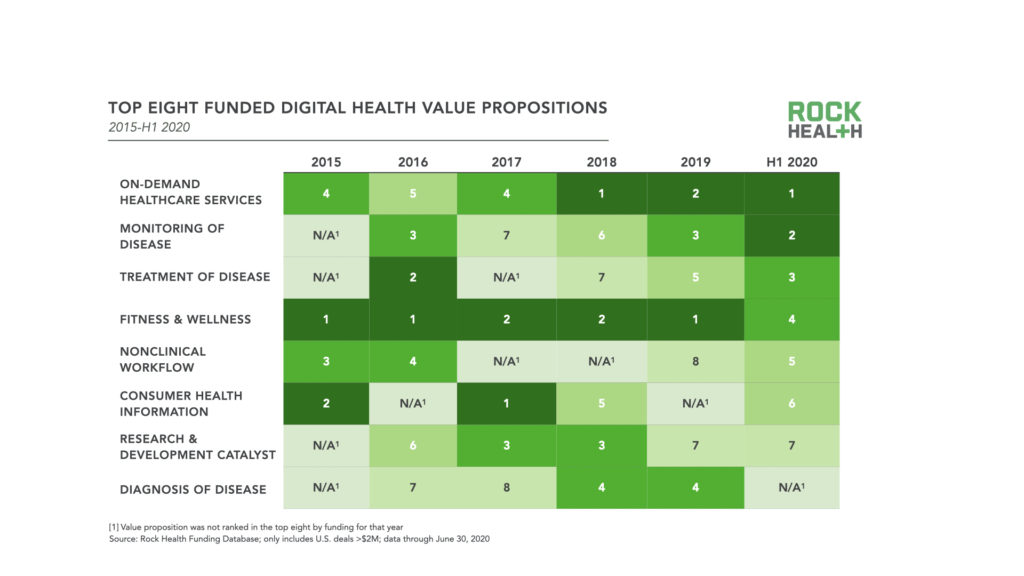

COVID-19 has accelerated virtual care by requiring that enterprise organizations use technology to treat and monitor their patients remotely. With spiking demand for virtual care options, venture investors are seizing the moment. The monitoring of disease and on-demand healthcare services value propositions4 have been well-funded for several years, and investors are evidently doubling down on their conviction. Digital health companies providing on-demand healthcare services (e.g., Alto Pharmacy, Amwell) raised $1.1B in the first half of the year, while monitoring of disease firms raised $831M, putting each category on pace to exceed 2019’s totals by 100%.

In H1 2020, telemedicine companies—which we define as companies leveraging synchronous or asynchronous virtual care technology—raised $926M. As many patients and providers use telemedicine for the first time, surveys show patients are increasingly comfortable with telemedicine for COVID-assessment. A second and even third wave of the pandemic potentially looms on the horizon. With telehealth powerhouse Amwell reportedly seeing a 158% increase in usage, the dual benefits of convenience for consumers and capacity rationalization for providers suggest virtual care solutions are here to stay.

Meanwhile, barriers to virtual care and remote monitoring—including reimbursement, licensure, and provider adoption—have been reduced. In 2020, several long standing policies have changed to help healthcare organizations deliver care virtually:

- CMS expanded reimbursement for telemedicine services by waiving the video requirement for many services; allowing billing for outpatient services furnished remotely; and expanding the types of providers eligible for remote-care reimbursement. Long term policy implications remain unclear, but it is unlikely HHS will go back to pre-COVID norms.

- HHS announced it will waive HIPAA penalties for telehealth cases conducted in good faith and has reduced the penalty cap for some violations.

- Many governors and state health agencies reduced state licensure barriers, allowing clinicians to more easily provide care across state lines.

Collectively, these changes make it easier for digital health companies to scale and meet the surging demand for virtual care solutions. While some of these changes may not be permanent, it’s tough to close the barn door after the cat is out of the bag—consumers and providers have experienced the value and convenience of virtual care. We believe these new virtual care habits will create new care paradigms beyond the pandemic.

COVID-19 has presented a new pattern of healthcare behavior that is here to stay. Previously, the biggest impediment has been the status quo—and now certain processes that have been previously underutilized, like telehealth, are being meaningfully catalyzed, compressing five years of work into weeks.

—Amy Belt Raimundo, Managing Director, Kaiser Permanente Ventures

Outlook for 2020: Surging consumer demand and investor interest in digital behavioral health

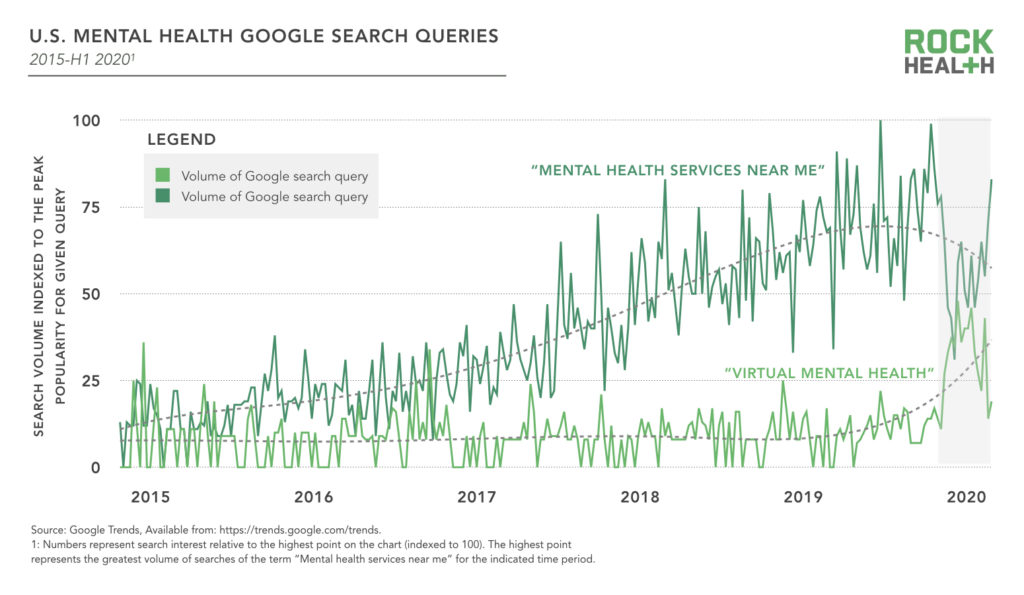

The COVID-19 pandemic has ushered in unprecedented levels of anxiety and isolation. Social, political, and economic instability, combined with a prolonged period of physical distancing, have exacerbated a mental health crisis that was already taking shape. Nearly 100,000 Americans have reported anxiety or depression as a result of the pandemic, according to a recent survey by Mental Health America. In April 2020, one study found that 13.6% of US adults reported symptoms of serious psychological distress, relative to 3.9% in 2018. Google searches for “mental health services near me” have risen steadily for the past five years, but those searches tapered off quickly once stay-at-home orders were put in place across the country. Searches for “virtual mental health,” on the other hand, quickly spiked at the end of Q1 as people searched for alternative options for in-person behavioral health services.

Behavioral health companies have received an influx of capital in recent years5. This has somewhat positioned the sector to respond to this shift in consumer demand, allowing those who have developed scalable solutions to offer novel, tech-enabled behavioral health services.

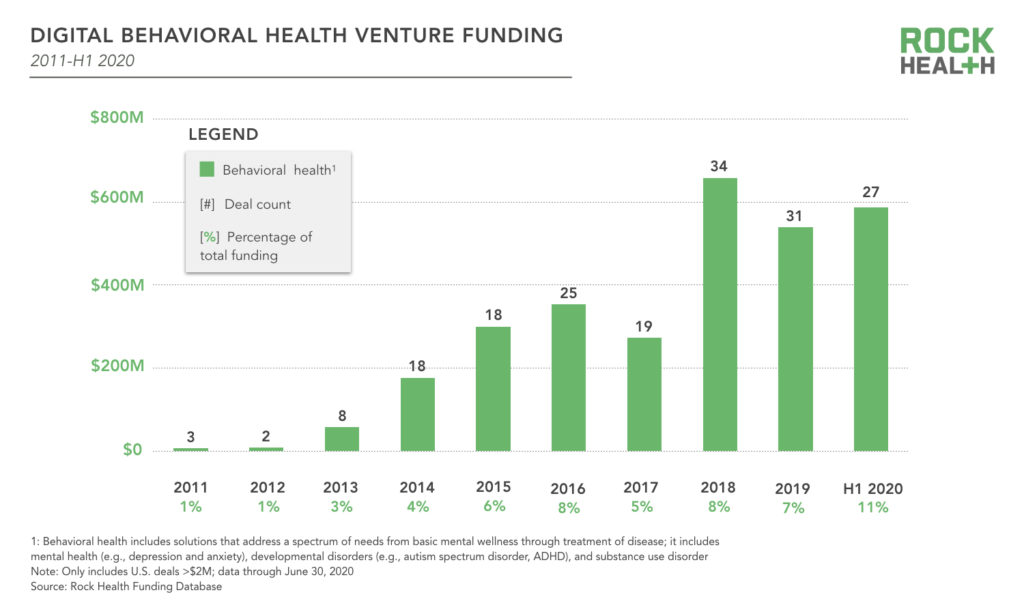

In H1 2020, digital behavioral health companies received $588M, roughly the annual funding for this segment in any previous year (total behavioral health funding in prior three years was 2019: $539M, 2018: $658M, 2017: $273M). Funding has gone to companies with a range of product features, from fully automated chatbots to video chat platforms with additional tools that augment patient-clinician interactions. The majority of funding in this segment in H1 of 2020 has gone to digital behavioral health companies that provide one of two services:

- Solutions that enable providers to provide remote treatment for acute and chronic conditions

- Digital therapeutics that are themselves a clinical treatment (like Lyra Health) or a non-clinical service (like Headspace)

The largest rounds were raised by these three companies, encompassing 54% of the entire behavioral health funding segment:

- Headspace raised $140M ($100M in equity and $40M in debt, across two rounds of financing) to continue building its mindfulness and meditation application

- Mindstrong, which makes an app that pairs patients with a network of providers to deliver personalized mental health care and utilizes a digital biomarker tracker of mood and cognition via patterns of smartphone interactions raised $100M in a Series C

- Lyra Health, a platform designed to deliver customized behavioral and mental health care virtually and/or in-person through their own network of providers, alongside self-care lessons and exercises, closed a $75M Series C

This increased funding has accelerated a quickly maturing segment. While this may, in the short run, complicate the marketplace for enterprise and individual customers navigating what is still a relatively new market, behavioral health companies with proven business models, clinical results, and culturally competent care will stand out in a growing landscape.

The low-to-mid acuity behavioral health market has become very saturated, but there is still a major opportunity for companies that address high acuity mental and behavioral health issues to help the portion of the population that is driving the majority of the cost.

—Alyssa Jaffee, Vice President, 7wire Ventures

Has anyone seen the future around here?

The first half of 2020 was tough to predict on enough fronts to make us pause before we put together a thesis for the next six months. But we’re thesis-driven by design, so here goes:

- Macroeconomic conditions will play a role in the second half of 2020—but not as big a role in digital health as in the rest of the economy because…

- Macroeconomic turbulence will, we expect, continue to drive enterprise buyer, consumer, and investor interest in digitizing healthcare in a way that offsets the negative effects of a recession as they did in H1. The “flight to quality” among investors observed in H1 will likewise continue.

- Digital health companies will not all fare the same. Startups who sell to providers and employers may face stiffer headwinds than those in other categories.

- If, however, financial system instability of the sort seen in the last economic downturn rears its head, fundamentals (of the sector or individual startups) will take a back seat for a bumpy ride.

The H1 data and upside surprise leaves us with guarded optimism for the remainder of 2020. Just the same, we’re looking forward to looking back when this year is done!

Interested in access to our full H1 market insights report and funding database with every deal from this half? Become a Rock Health partner or consulting client! Email us at partnerships@rockhealth.com to learn more.

Join us for an in-depth discussion about the funding environment for both digital health companies and investors on 7/30—register here.

Footnotes

1Digital health funding was $3.0B in Q1 and $2.4B in Q2. There were 109 deals in Q1 and 105 deals in Q2. Using a straight-line projection for the remainder of the year, 2020 will end at $10.2B in total funding over 432 deals resulting in an average deal size of $23.6M.

2When we spoke with one particular executive at a major investment bank to help contextualize general public market uncertainty and the impact of this particular forecasting miss at the time it occurred, he put it simply: “To say that our ‘forecasts were off’ would be like saying the dinosaurs ‘had a bad day’ when the asteroid hit.” It’s worth noting, however, that since the May report sources of measurement error and misreporting have been identified as a partial cause of the unpredictability in the BLS numbers. Uncertainty abounds.

3The Digital Health Public Company Index’s H1 return excludes Schrödinger Inc (SDGR), which went public in February 2020. SDGR is up 439% from its price at IPO.

4Each company in the Rock Health Digital Health Funding Database is tagged with at least one and up to three “value propositions.” Since each company may fall into multiple value propositions, the sum of the funds raised across value propositions does not sum to the total funds raised.

5Rock Health tags companies with the following three clinical indications in the Digital Health Venture Funding Database, which roll up into the behavioral health category: mental health, substance use disorder, developmental disorders.