2019 Midyear digital health market update: Exits are heating up

Stay up to date with the latest headlines in healthcare technology and new Rock Health content. Subscribe to the Rock Weekly.

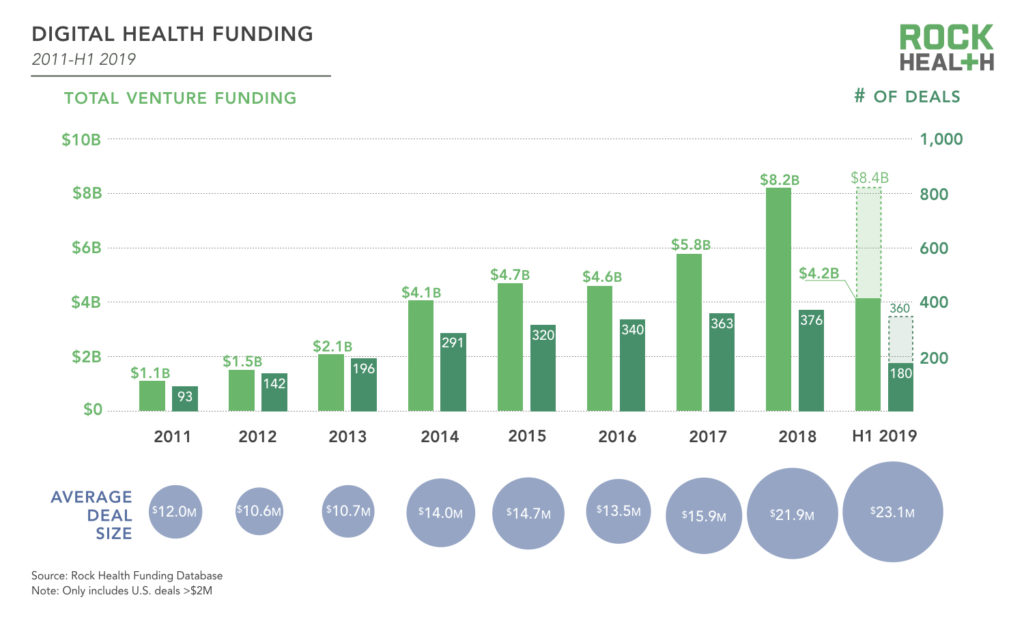

Investors continue to fund digital health at a steady clip. Digital health companies raised a total of $4.2B across 180 deals through the first half of 2019. If this pace holds steady, the sector is on track for an $8.4B year in 2019—and may even top 2018’s record-breaking annual funding total1. As in 2018, a handful of $100M+ mega deals are driving the overall trend.

Investment in the first half of 2019 is in line with the steady growth trend in annual funding since 2011. Despite some year-to-year variation, the funding environment remains fundamentally unchanged from recent years. About 30% of venture dollars in H1 2019 went to large ($100M+) mega deals. Experienced investors continue to return to the well—69% of investors in the first half of the year were repeat investors. As digital health continues to mature as a sector, we expect this theme to persist in the near-term, even as macro-economic conditions fluctuate.

All eyes are on the five companies reported to be planning public offerings in 2019. Livongo, Health Catalyst, Change Healthcare, Phreesia, and Peloton would be the first digital health IPOs since 2016. Through the IPO drought, M&A was the sole exit route offering liquidity for digital health investors. M&A continues to dominate the exit scene with 43 acquisitions in the first six months of 2019. Projecting this forward six months, 86 acquisitions in 2019 would be roughly 25% fewer than in recent years.

With exits on the brain, we decided to calculate how much digital health venture investment since 2011 is still waiting for liquidity via an exit. This post explores the avenues for startups to realize returns for investors. Clear paths to an exit are what will ultimately justify and sustain investment in the digital technologies transforming our healthcare industry.

But first, at the start of 2019 we questioned whether the current digital health funding environment is an investment bubble. It wasn’t. We give a quick update on that analysis below—spoiler alert: still not a bubble.

For access to all of the trends in the full report—including breakdowns of top-funded categories, investor breakdowns, and more—become a Rock Health partner. Email partnerships@rockhealth.com for more information. If you’re a startup who’d like access, get in touch by emailing research@rockhealth.com.

Bubble watch: A pulse check on the digital health investment sector points to mostly healthy growth

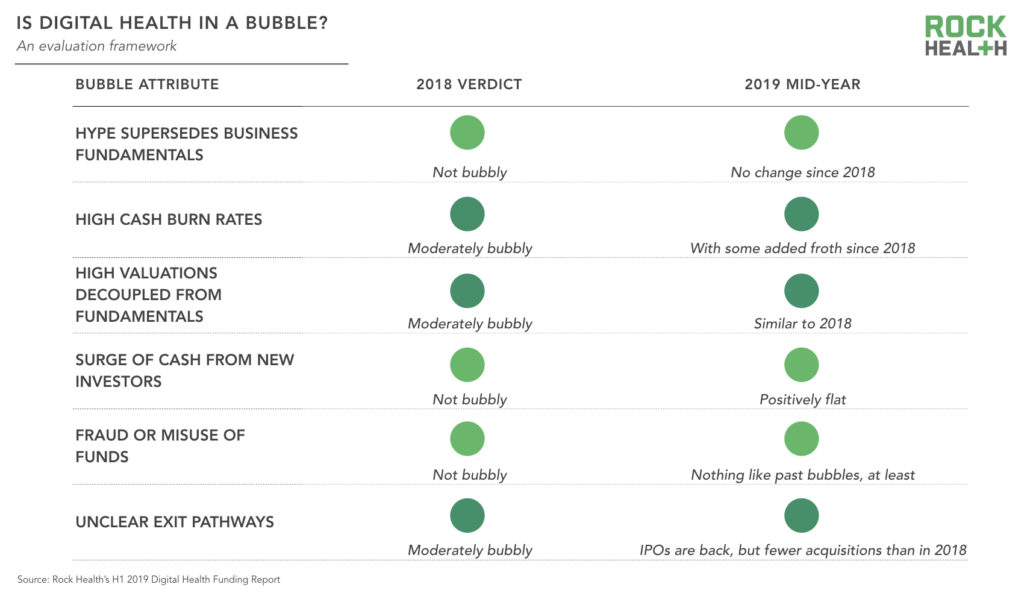

We kicked off 2019 by diving headfirst into a debate that had begun stirring among investors late last year: is digital health in a bubble? With record-levels of funding in 2018 and no jump in exit activity, it was a timely and important topic. Our verdict? Digital health was not an investment bubble.

The bubble analysis was built on a framework of six attributes common across other investment bubbles2:

- Hype supersedes business fundamentals

- High cash burn rates

- High valuations decoupled from fundamentals

- Surge of cash from new investors

- Fraud or misuse of funds

- Unclear exit pathways

An investment bubble is an economic cycle in which asset prices rise far beyond what is justified by fundamentals. When investors become wary of a bubble, they freeze new investments, causing a sharp contraction in prices that “bursts” the bubble. At that point, venture-backed startups that need access to fresh capital struggle to remain solvent—often regardless of their fundamentals—as valuations plummet.

A bursting bubble is not just a down cycle—it’s a rout.

Business models

Verdict: Not bubbly (no change since 2018)

Sustainable digital health businesses will create value, demonstrate their value, and overcome the complexities inherent in healthcare such as regulation and long sales cycles. There’s ample evidence of this in 2019. Investors (who have clearly learned from missteps in the early days of digital health) continue to fund startups with B2B business models—87% of funded digital health companies in H1 2019 sell to enterprise—the employers, payers, providers and others that hold pursestrings in US healthcare.

Notably, the long enterprise sales cycles in healthcare aren’t killing early stage innovation: a higher percentage of pure B2B digital health startups that raised a seed round across 2011-2015 have since raised a subsequent round of funding compared to pure D2C seed-funded companies in the same time period.

Savvy entrepreneurs are also pursuing value-based business models. Virta Health, a Rock Health portfolio company, recently published two-year results from its ongoing clinical trial in which 18.8% of participants who completed two years of the trial achieved either complete or partial diabetes remission—a proportion higher than typically observed with usual care or intensive lifestyle interventions. Virta’s validated clinical outcomes enable it to tie 100% of fees to patient outcomes.

Burn rates

Verdict: Moderately bubbly (with some added froth since 2018)

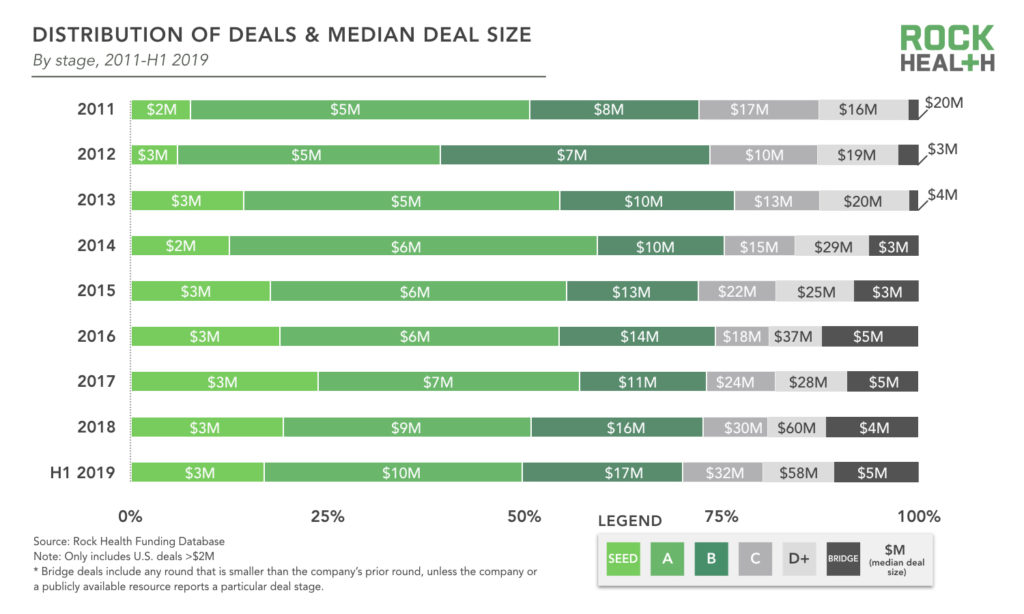

Digital health startups, like startups across other non-healthcare industries, are raising historically large rounds. The median size of a Series A digital health deal in 2019 thus far is $10M—up 11% from the $9M median in 2018 and 2X the median Series A in 2011. Series B deals have experienced similar growth—the median $17M in 2019 is 2.1x the median Series B in 2011.

Companies generally aren’t using these large rounds to extend their runways—the average time between funding rounds hovers around 20 months for companies that raised a Seed, Series A, or B in 2014-20163. We recommend that entrepreneurs should manage cash prudently in the months ahead. Companies with high cash burn rates will feel more pinch when venture funding levels off or dips into a more capital constrained environment.

Valuations

Verdict: Moderately bubbly (similar to 2018)

Investors minted three new digital health unicorns in the first half of 2019. Zipline raised $190M, reportedly at a $1.2B valuation, to expand its drone delivery operations. The company currently delivers blood and medicines to clinics in Rwanda and Ghana. Gympass raised $300M at a valuation of more than $1B in a round led by SoftBank’s Vision Fund. The Brazilian startup moved its headquarters to New York City in 2018 and offers monthly gym passes to employees at more than 2,000 companies. Hims, the direct to consumer prescription and delivery service, raised $100M4 at a $1B valuation to fuel its rapid expansion—the company hit unicorn-status little more than a year after its founding in 2017.

Surge of cash from new investors

Verdict: Not bubbly (No bubbles. Positively flat.)

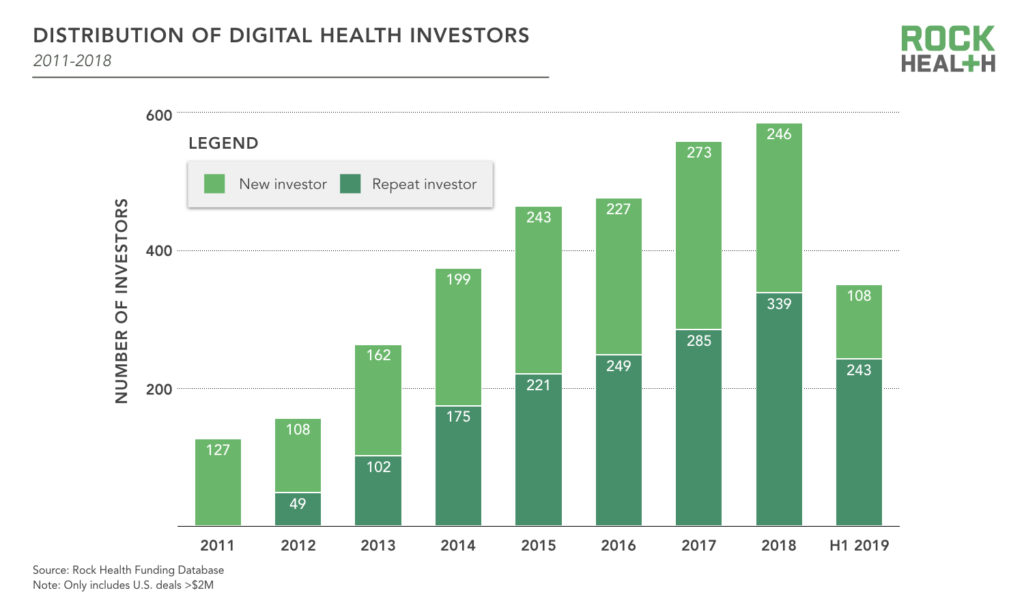

Repeat investors in the digital health sector are a mark of a maturing investment sector. Their smart dollars come with valuable experience for entrepreneurs. There have been more repeat investors than new investors in digital health every year since 2016, and the spread has never been as wide as it is now. Sixty-nine percent of the 351 disclosed investors made a previous investment in a digital health company.

Fraud and misuse of funds

Verdict: Not bubbly (Nothing like past bubbles, at least)

Through 2018, just one digital health company was flagged for fraud and misuse of funds—Outcome Health broke the trust of its customers and investors by manipulating data about the effectiveness of its pharma advertising business. We don’t consider the most notable failed healthcare startup, Theranos, a digital health company.

2019 adds another to this list: uBiome is under investigation by the FBI for alleged improper billing practices. The company put its co-founders on leave and is laying off employees. uBiome suspended two of its lab tests, SmartGut and SmartJane, and named general counsel John Rakow as interim CEO—but Rakow left the company on June 30. Curtis Solsvig, a director at consulting firm Goldin Associates, was appointed interim CEO and the company is cooperating with the investigation.

Journalists have flagged some additional digital health companies for reportedly cutting corners in attempts to scale quickly. Nurx, an online prescription and delivery service, reportedly maintained an unusual in-office inventory of medication and blurred the line between medical and business decision making. In another case, Shannon Spanhake, the former CEO of Cleo, a company that virtually connects employees with “guides” to coach them through pregnancy and subsequent return to work, is alleged to have included fabrications on her resume. Although neither of these are examples of company fraud, they are part of a concerning narrative of venture-backed companies prioritizing growth above all else. When patient health is the outcome, integrity is particularly important, and we hope to see this integrity maintained by entrepreneurs, investors, and all participants in the digital health innovation ecosystem.

Exit pathways

Verdict: Moderately bubble (IPOs are back, but fewer acquisitions than 2018)

Though no one would describe the exit market as “overheated,” digital health does not have a full-on liquidity problem. There are five digital health companies reportedly planning to go public in 2019. These exits build upon a steady stream of M&A—another 43 digital health companies were acquired in the first six months of 2019. We delve deeper into exit analysis in subsequent sections of this post.

I don’t foresee a long cold winter for digital health. The systemic problems are so massive and under addressed— there’s so much wood to chop in this market.

Robert Garber, Partner, 7wire Ventures

Venture funding activity in digital health through the first half of 2019 largely supports our analysis from six months ago: digital health is not in a bubble.

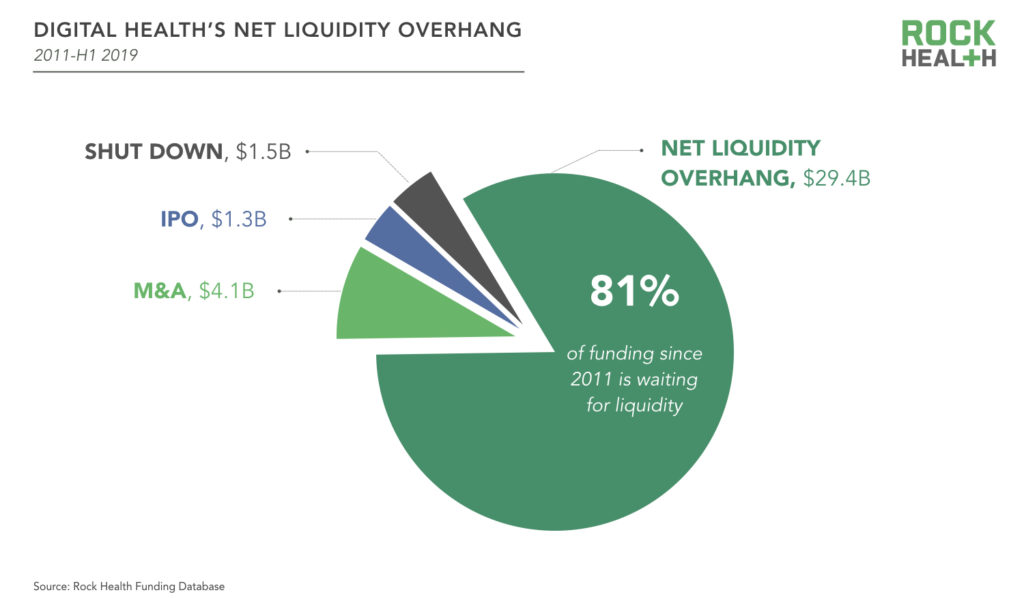

Digital health’s “net liquidity overhang” (to coin a phrase)

Since 2011, we’ve extensively tracked the bets investors have made on digital health startups. As the sector has matured, many of those bets have already played out—for better or for worse. To understand how much money is still “on the table” after accounting for the bets (investments) that have already reached their conclusion, we’ve calculated a number that we refer to as the “net liquidity overhang” (NLO). NLO is the amount of invested capital still awaiting a liquidity event, investments on which investors have yet to realize returns. Here’s the math:

NLO = (Total dollars invested) – (Investments made in companies that have already exited)

As of July 1, 2019, $36.3B has been invested in 1,274 digital health startups between 2011 and the end of Q2 2019. 170 companies were acquired in the same timeframe, providing liquidity to investors who, in aggregate, invested $4.1B in those 170 companies. Another ten startups have gone public since 2011, taking an additional $1.3B of invested capital “off the table.” Finally, $1.5B was invested in startups that shut down5 (more than half of which went to a single company: Jawbone6). Altogether, that adds up to $6.2B in invested capital that is no longer awaiting an exit. Doing the math:

NLO = ($36.3B) – ($4.1B + $1.3B + $1.5B) = $29.4B

Looking just around the corner, if all five rumored IPOs take place in 2019 and if investment in H2 2019 mirrors the first half, the NLO at year-end will be $31.9B.

So… who cares?

As digital health continues to mature, investors should be concerned both with the overall health of the market’s fundamentals today (for which we built our “bubble watch” framework) as well as the prospects for healthy exits tomorrow. NLO is a measure of the aggregate “pressure” on the exit market and the risks this pressure represents for entrepreneurs and investors. With NLO, we can begin to ask questions about the timing and multiple of returns the sector as a whole “needs” to achieve to be considered a success, the possible equilibrium-level NLO, and other factors—which we dive into further in our comprehensive reports (become a Rock Health partner for access).

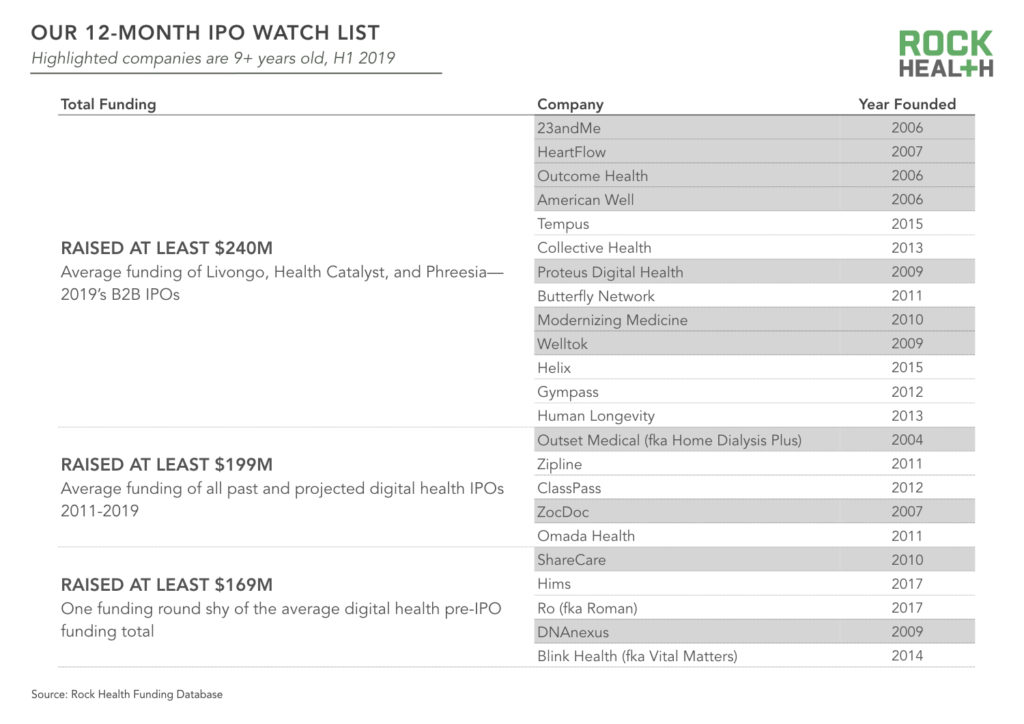

There are five digital health IPOs on tap for 2019—twenty-two more companies are on our watch list

2019 marks the end of the three-year digital health IPO drought. Five companies—Livongo, Health Catalyst, Change Healthcare, Phreesia, and Peloton—have announced plans to enter the public market this year. The question everyone is asking is: What will this year’s batch of IPOs signal about the future?

Four of these companies—Livongo, Health Catalyst, Phreesia, and Peloton—raised an average of $425M from private investors (Change Healthcare is excluded here because it grew out of a series of acquisitions and a spinoff from McKesson). A total of $1.7B was invested in these four companies. That’s 5% of all money invested in digital health since 2011 and 6% of the NLO, making this year’s IPO class one worth watching.

According to Pitchbook, the most recent private market valuations of these four companies pegs their combined valuation at $6.4B. To get a sense of scale, assume for a moment that public investors pay exactly $6.4B—with no additional premium at IPO. This represents a multiple of 3.8 on the $1.7B invested, and is 22% of digital health’s current NLO. (Put another way: Though the IPO window is fickle, at this pace the digital health sector would break even on the $29.4B of today’s NLO in four and a half years). Of course, these IPOs represent returns for the 40 disclosed investors in these four companies, or just 2% of the 1,693 total disclosed investors in digital health since 2011.

What 2019’s digital health IPOs look like—and hint at for the near future

Looking at the 10 past and five projected digital health IPO companies between 2011 and 2019, these companies raised an average of $199M and went public at an average age of 9.4 years. This contrasts with the frothy dotcom days where companies like Pets.com raced to IPO just after its first birthday (and to its grave at about the same pace).

Using these 15 companies as a baseline, 19 more digital health startups have raised at least as much as this group’s average of $199M. The list grows to 23 when we add just a 15% buffer to the $199M cutoff—these companies could be just one funding round shy of the average digital health pre-IPO funding total.

Six7 of these companies are at least ten years old and have raised at least $240M, appearing, at least on the surface, to be at comparable maturity points as digital health’s 2019 B2B IPOs8. This group includes American Well, a telehealth platform; 23andMe, a consumer genetics and research company; HeartFlow, a medical technology company using AI to create a personalized 3D model of the heart; Proteus, a developer of digital medicines that communicate when they have been ingested; and Welltok, an enterprise-level consumer healthcare SaaS platform.

Healthcare’s big new entrants are buying digital health capabilities

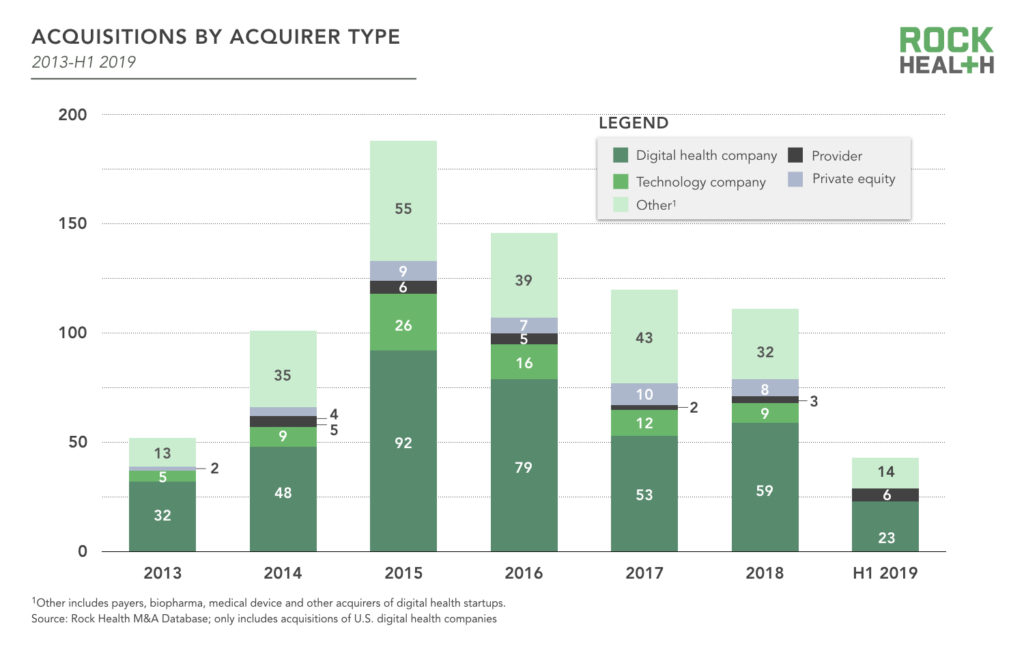

There were 43 acquisitions of digital health companies through the first six months of 2019. At this rate, the sector will fall shy of recent historical M&A activity of about 100-120 acquisitions per year. As usual, the most frequent acquirers of digital health companies are other digital health companies, accounting for 23 (or just over half) of the transactions.

We expect other categories of acquirers to become more active in the coming years. As more non-healthcare organizations enter the healthcare industry, their strategies include buying external innovation in addition to building it internally. Technology companies and other non-healthcare companies are consistently the second and third most active acquirers, respectively, in our Digital Health M&A Database.

Healthcare’s a huge market, but unless you have domain knowledge you shouldn’t play in healthcare because you could potentially ‘lose your shirt’. Perhaps [big tech companies] learned this painful lesson from their past attempts to penetrate this space. So, if they’re going to play in healthcare, they need to bring in technologies that are adjacent to their existing core competencies – areas in which they already have a strong position. They are likely to acquire technologies and companies with expertise and domain knowledge that allow them to take that next step to healthcare without just diving in blindly headfirst. I believe you will see more of this strategy play out in the future.

David Kim, Managing Director, DigiTx Partners

The $3.5T healthcare market is a promising source of future growth for a number of large non-healthcare companies. The biggest of these, like Amazon, Google, and Best Buy, may in some cases be “premium” acquirers—willing to pay somewhat higher premiums to secure later-stage companies that fill a strategic need and meet financial objectives. For example, in order to acquire PillPack, Amazon outbid Walmart with a $753M offer9. These buyers are not price-shopping for discounts.

The PillPack acquisition signaled Amazon’s healthcare ambitions beyond Haven, its much-speculated-about healthcare joint venture with JP Morgan and Berkshire Hathaway. In a similar vein, JP Morgan made its own move into digital health in the first half of 2019 with the acquisition of InstaMed, a healthcare payments technology company. The acquisition, priced at more than $500M, adds healthcare payment technology to the financial institution’s growing wholesale payments business.

And last year, consumer electronics retailer Best Buy shelled out $800M to purchase Great Call, a provider of connected health and personal emergency response services to the aging population. Best Buy supplemented its senior-focused offerings with its Q2 2019 acquisition of Critical Signal Technologies, which offers a remote senior monitoring service.

Google and Apple are also stepping into the healthcare fray, though they’ve been less public about their acquisitions. It was recently revealed that Nest, the Alphabet subsidiary that recently rejoined Google, quietly acquired Senosis, a developer of smartphone-based health monitoring solutions. The move suggests digital health will be a component of Google’s smart home strategy.

Last year Apple scooped up Tueo Health, which uses apps and sensors to help parents manage asthma symptoms in children. The acquisition fits with Apple’s strategy of deploying spare cash to buy small startups for their talent and intellectual property. The iPhone maker’s healthcare ambitions, like other large, non-healthcare entrants, are not trivial. In 2016, Apple acquired Gliimpse, a small company building personal medical records, and has since launched a personal health record service available through over 100 provider organizations.

This (non-comprehensive) list of digital health acquisitions by big, non-healthcare companies is one that we expect to grow.

Of course, not all privately held digital health companies are for sale, even to acquirers with deep pockets like Apple. For April Fools Day, Epic poked fun at Jim Cramer’s suggestion that Apple should acquire the Wisconsin-based electronic health record provider.

Closing thoughts

The maturing digital health venture investment environment remains robust and relatively free of froth with signs of a near-term harvest in the IPO market. There is $29.4B of active venture capital—digital health’s net liquidity overhang (NLO)—anticipating a liquidity event (an exit) at some point in the future. The recently-rekindled IPO market for digital health will return capital invested in some of the most mature startups. Though M&A within digital health remains more common, acquisition by large healthcare and non-healthcare companies will be a significant source of liquidity and returns for digital health investors.

Partner with us!

A special thank you to our generous corporate partners for their continued support. For full access to the market update and database, among a host of other benefits, become a Rock Health partner. Email for more information about how your organization can work alongside Rock Health to build the future of healthcare innovation.

Thank you to our contributors

This report would not have been possible without the help of a number of individuals who have graciously shared their expertise:

-

- Robert Garber, Partner, 7wire Ventures

- David Kim, Managing Director, DigiTx Partners

Footnotes

1Our 2018 year end post reported a funding total of $8.1B. As of June 30, 2019, we’ve updated that total to $8.2B after including previously unreported deals.

2Speculative bubbles come in many different shapes and sizes. Historical bubbles have touched everything from mortgage backed securities and digital currencies to tulip bulbs and dot-com companies. In this case, we are evaluating the potential for a bubble where the object of speculation is privately held startup companies. We’d like to again thank our friends at Bessemer Venture Partners, Flare Capital, Kaiser Permanente Ventures, HealthTech Capital, Venture Valkyrie, Evidation Health, and Virta Health who helped us refine this framework.

3We did not analyze 2017 or 2018 data because not enough time has elapsed to take a meaningful measurement of time to next round.

4We did not originally include Hims’ funding round in our Q1 2019 Funding Update because we were unable to verify the funding. We’ve decided to include the $100M round now because it has a non-trivial impact on the story of H1 2019 digital health funding and the company has not refuted the significant press coverage.

5Admittedly, tracking deadpool companies is challenging because such exits are not always made public.

6Jawbone has since emerged from the ashes as a digital health phoenix, raising $65M.

7Outcome Health is excluded from this list because of its significant legal issues in 2017, despite having raised more than $308M and being more than ten years old.

8Most digital health startups sell to enterprise. The 2019 B2B IPOs include Livongo, Health Catalyst, and Phreesia—these three companies have raised, on average, $240M. As a D2C company, Peloton’s nearly $1B of funding skews the profile of an IPO-ready digital health company.

9The deal was originally reported as just under $1B. SEC filings show that the actual transaction amount was $753M.