2018 Funding Part 2: Seven more takeaways from digital health’s $8.1B year

It was another banner year for digital health venture funding in 2018. In Part I last week, we dove headfirst into assessing the “froth” in digital health. Our conclusion: digital health is not in a bubble.

For more bubble debate, catch our latest podcast with Sitka co-founder & CEO Kelsey Mellard, Flare Capital co-founder & Partner Michael Greeley, and Rock Health Managing Director & CEO Bill Evans—recorded during the JP Morgan Healthcare Conference week in San Francisco.

In this post, we move from macro funding and exit trends to a deeper look at investment in 2018. Here are seven insights on the who, what, where, and how of U.S. digital health startup funding.

1. Mega deals sent funding skyrocketing

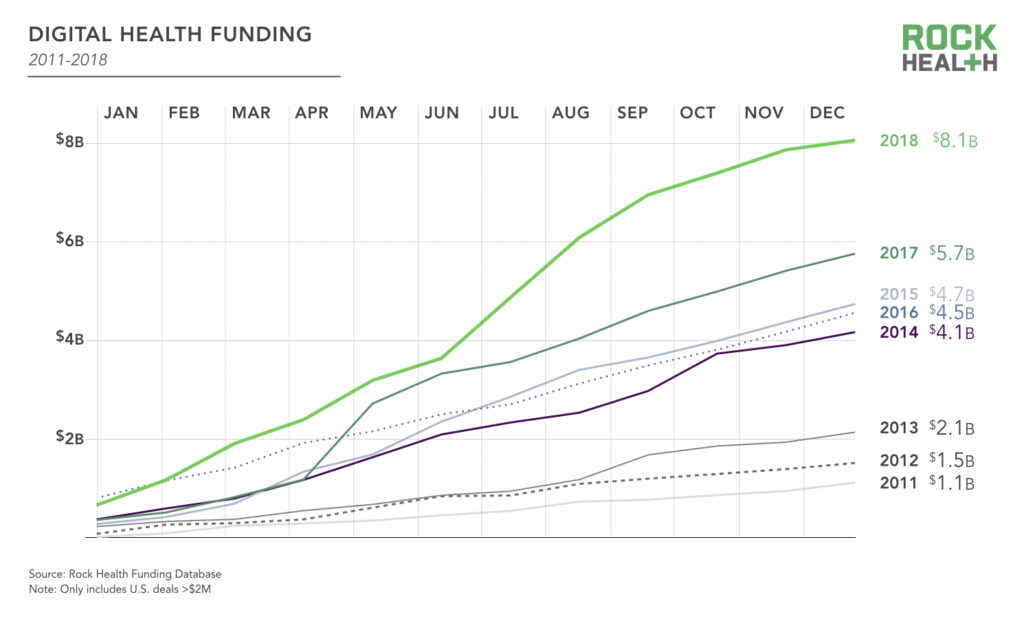

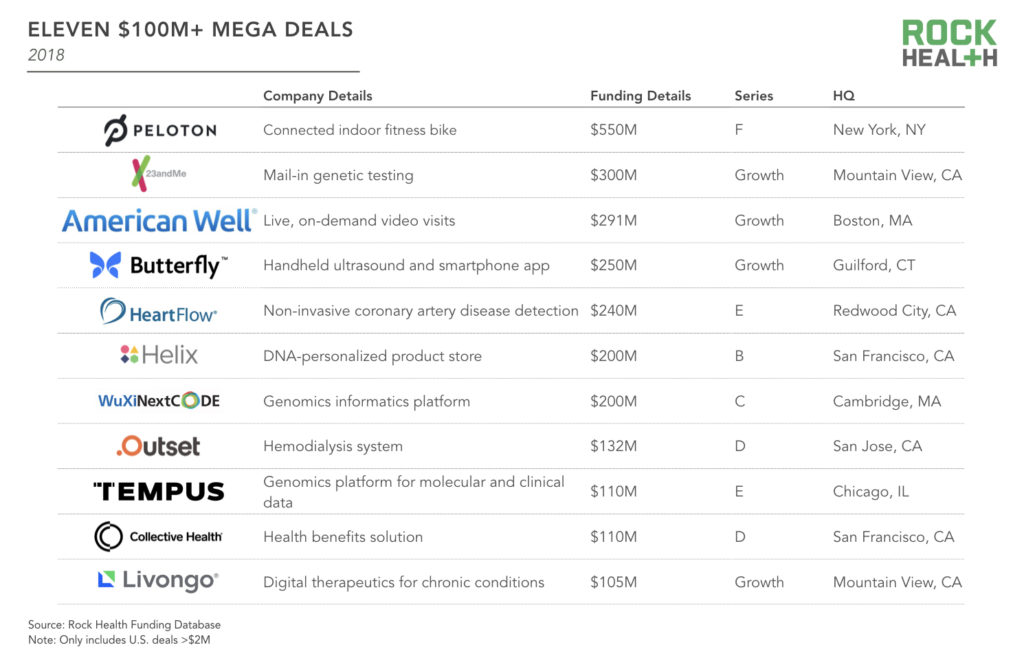

Digital health startups raised an unprecedented $8.1B in 2018 compared to $5.7B in 2017. This uptick isn’t simply explained by more deals—there were 368 deals in 2018 compared to 359 in 2017. Instead, it was largely the result of eleven mega deals ($100M+), seven of which were rounds over $200M. Excluding those seven deals, total funding and average deal size for 2018 were $6B and $17M respectively, which largely align with 2017 levels.

These mega deals clustered in Q3 2018, with Peloton, 23andMe, American Well, Butterfly Network, and Outset Medical all raising $100M+ rounds. As a result, Q3 2018 was the most prolific quarter ever, with $3.3B invested.

These mega deals represented significant investment around scale and monetization strategies. American Well raised $291M to scale given friendlier regulations around reimbursement for remote care. GSK acquired a $300M stake in 23andMe, alongside an exclusive deal to use the genomic data to find novel drug markers. Meanwhile, Collective Health closed $110M to accelerate development and staffing of its health benefits solution for employers.

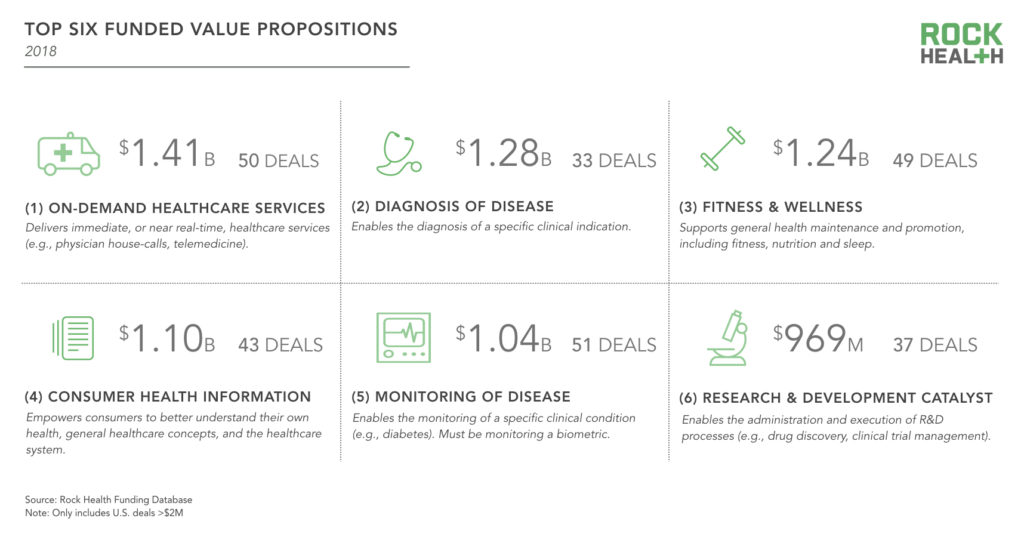

2. Investors were most eager to fund on-demand healthcare services and digital diagnostic tools—particularly those leveraging AI/ML

In 2018, 44 startups offering on-demand healthcare services as a primary value proposition closed 50 deals for a total of $1.41B. This included telemedicine companies like American Well and Doctor on Demand, and we’ve seen more innovation centered on building patient-centered experiences around prescriptions and drug delivery with companies like Nurx, Hims, and Alto Pharmacy receiving funding. This points to investor confidence in businesses that empower patients with control over when, where, and how they access healthcare.

Butterfly Network, HeartFlow, and WuXi NextCODE each raised $200M+, making digital diagnosis the second-most funded value proposition. This space has been accelerated by AI and machine learning (AI/ML) advancements—more than one third of funded digital diagnostic companies leverage AI/ML technology.

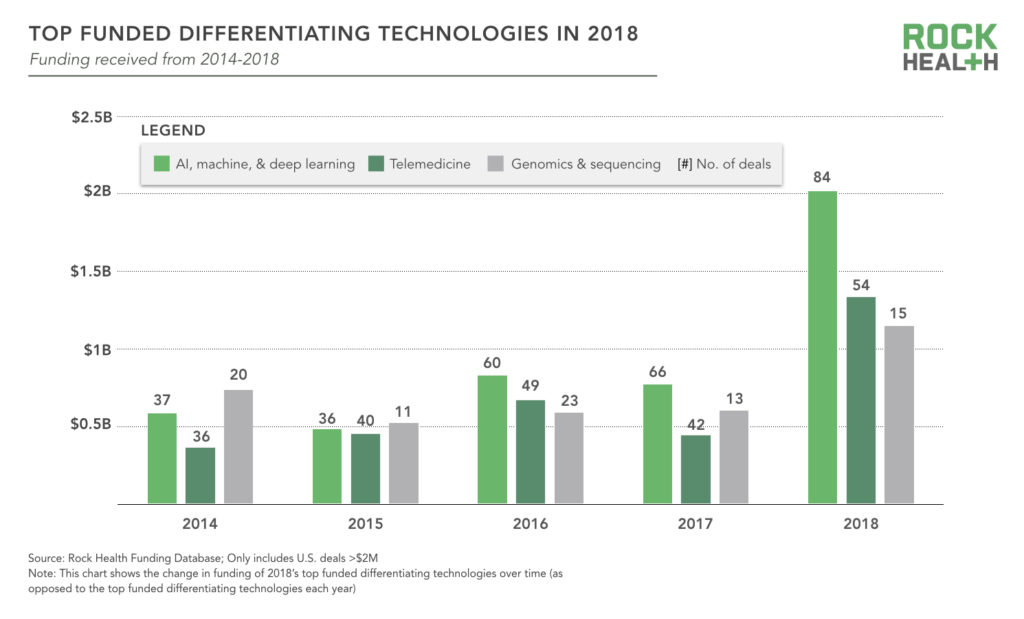

3. AI/ML is the top funded transformative technology in healthcare (by far)

Entrepreneurs are putting AI to work in healthcare across the board, with solutions ranging from medical imaging to triage chatbots. AI/ML-powered digital health companies raised over $2B in 2018—a massive 161% increase over 2017. This made AI/ML the most well-funded of the differentiating technologies we track, which include telemedicine, genomics & sequencing, IoT, and blockchain, among others.

Note: Rock Health’s tracked differentiating technologies do not include ubiquitous technologies such as apps, SaaS, and mobile functionalities. Other differentiating technologies tracked but not listed here include: genomics and sequencing, wearables/biosensors, non-medical device hardware, remote monitoring, IoT, blockchain, and robotics. Each company in the Digital Health Funding Database can be tagged with up to three “differentiating technologies.” Since each company may have multiple differentiating technologies, the sum of the funds raised across differentiating technologies does not sum to the total funds raised.

Relative to past years, investors significantly increased funding for clinically-focused AI/ML-startups in 2018. Those offering digital diagnosis garnered the most funding in 2018, raising $592M across 12 deals. Many startups are supporting physicians through faster, more accurate, and convenient diagnosis (e.g., Butterfly Network’s handheld ultrasound device), and some are bringing diagnosis to consumers (e.g., Ezra’s diagnosis telemedicine platform for prostate cancer). This investment aligned with impressive advancements in image and speech recognition for diagnosis, including the first FDA-approved device (from IDx) for diagnosis without a doctor. Meanwhile, startups using AI/ML to improve clinical decision support and precision medicine raised $565M across 17 deals.

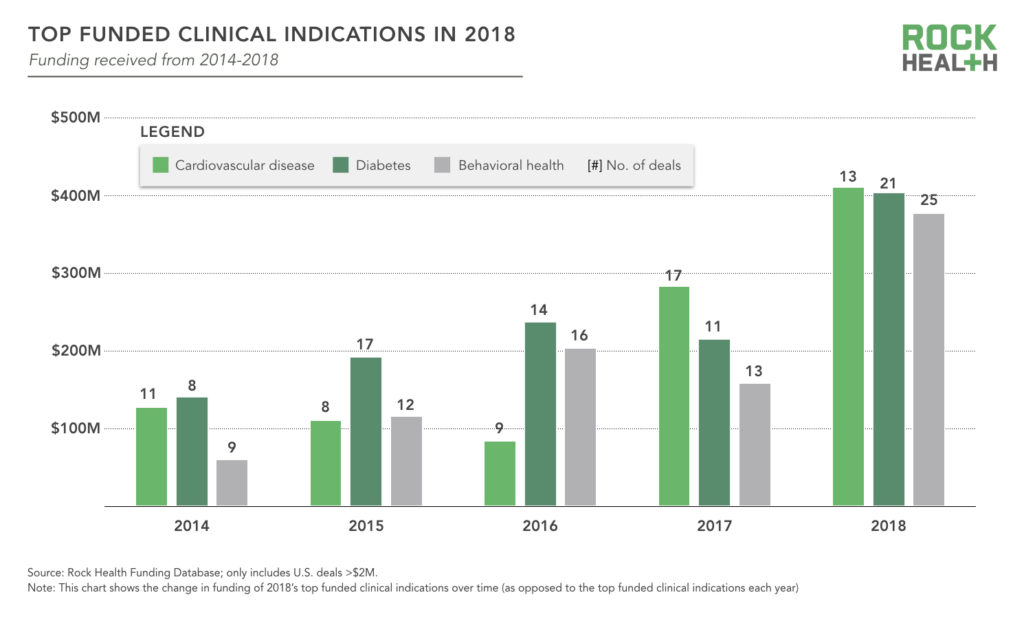

4. Digital tools to manage chronic conditions continue to attract the most funding, while many new behavioral health startups emerged

In 2018 investors continued to back startups addressing the leading causes of death in the U.S., as cardiovascular disease, oncology, and diabetes were three of the top four funded clinical indications in digital health.

Led by HeartFlow’s $240M Series E deal, 13 cardiovascular-focused startups raised $411M in 2018. Of course, in the cardiovascular space the spotlight wasn’t just on startups—to great fanfare, Apple announced its FDA-cleared ECG app for the Apple Watch.

Most notable in 2018 was the jump in funding for behavioral health startups. Investors funded 25 rounds with digital behavioral health companies, 14 of which were seed or Series A. To expand access to care, select companies have emerged that leverage AI to provide support (typically cognitive behavioral therapy) to users, but investors have largely invested in companies using technology to connect patients with behavioral health providers. And under the broad umbrella of prevention and treatment, solutions widely vary from offering meditation apps, to treating disease via digital experiences and software. Highlights among behavioral health-focused startups include:

- Pear Therapeutics raised a $46M Series B to pursue further evidence of clinical efficacy of its digital therapeutics (Pear is building a host of solutions for various therapeutic areas, some of which are behavioral health-related such as depression and PTSD). Pear also recently announced its commercial launch of reSET-O for Opioid Use Disorder after receiving FDA clearance in December.

- Akili Interactive Labs raised a $68M Series C to build out its digital therapeutic offerings, including treatments in development across neurology and psychiatry such as Major Depressive Disorder

- Lyra Health raised a $45M Series B to develop its telemedicine platform and support therapists with practice management tools

5. Digital health investors increasingly bring experience and healthcare expertise along with their venture dollars

Traditional venture capital firms consistently account for about two thirds of all investor transactions in digital health. Well-known names like Khosla Ventures, New Enterprise Associates, and Founders Fund—joined by BoxGroup, an angel group in NYC—were among the most active investors in digital health in 2018, each making about 10 investments.

Corporate investors have been a consistent presence, accounting for at least 15% of transactions each year since 2014. Corporate healthcare investors can lend valuable demand-side insight to startups, not to mention offering the potential for commercial contracts and a potential exit. But aligning with large enterprise players can make it more challenging to navigate competitive dynamics with customers or other future investors.

The digital health corporate investor mix is roughly equal parts providers, biopharma, payers, and traditional tech—each group accounts for about a fifth of all corporate VC transactions. Biopharma has steadily increased its venture funding activity, accounting for 19% of all corporate VC transactions in 2018. Provider participation, on the other hand, has dipped—17% of corporate VC transactions in 2018 were by providers compared to 33% just two years ago. The top ten all-time most active provider investors, a group that includes Kaiser Permanente, Mayo Clinic, and Providence Health & Services, among others, made on average less than one investment in 2018, down from 2.6 investments in 2015.

As for big tech moves into healthcare, Google Ventures was particularly active in 2018. The firm made seven digital health investments ranging from participation in a $7M Series A round for OWKIN, a company providing AI algorithms to cancer centers and pharmaceutical companies for drug discovery and clinical trial optimization, to participation in the $110M Series D round for Collective Health.

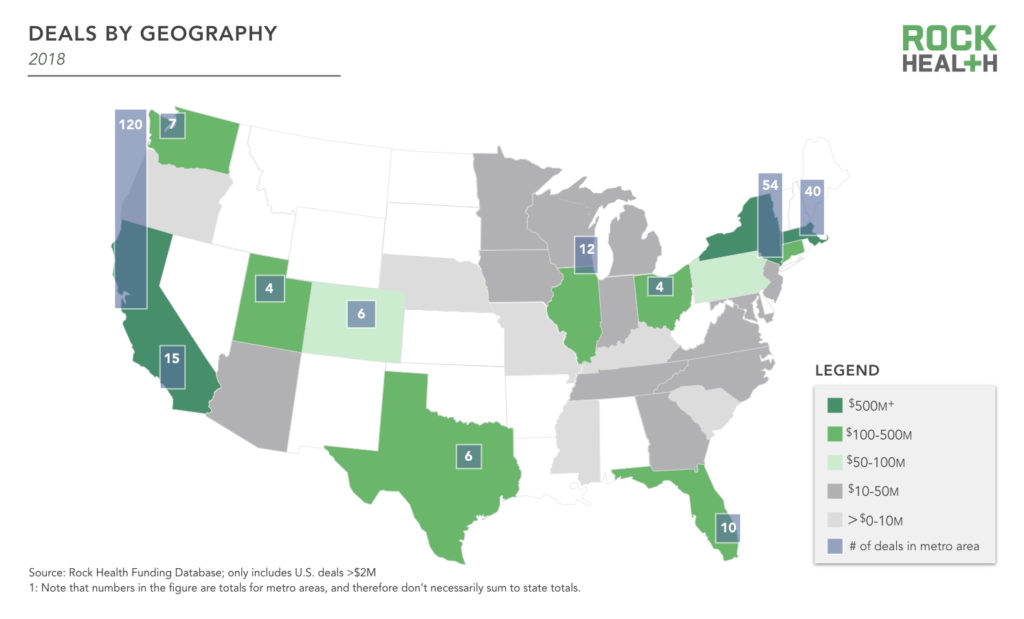

6. Digital health funding follows startups sprouting up outside leading tech hubs

Holding on to its spot as the primary digital health hub, California had 147 startups raise more than $3.5B across 140 deals1. But investors are increasingly painting the map green as funding increases for digital health companies outside the California and New York strongholds. Eight other states—MA, IL, CT, FL, WA, OH, TX, and UT—are home to startups that collectively raised more than $100M of venture funding in 2018.

To connect with digital health ecosystems across the country, Rock Health is going on the road this spring with our Enterprise Insights Series. Held in cities across the U.S., these curated events feature the latest market insights from Rock Health research, facilitated networking opportunities, and strategies for enterprise and digital health startups to overcome barriers to innovation.

The Series is coming to Boston, New York City, and Washington, DC in Spring 2019. Interested in attending—or want to see your city on the list? Let us know and sign up for updates.

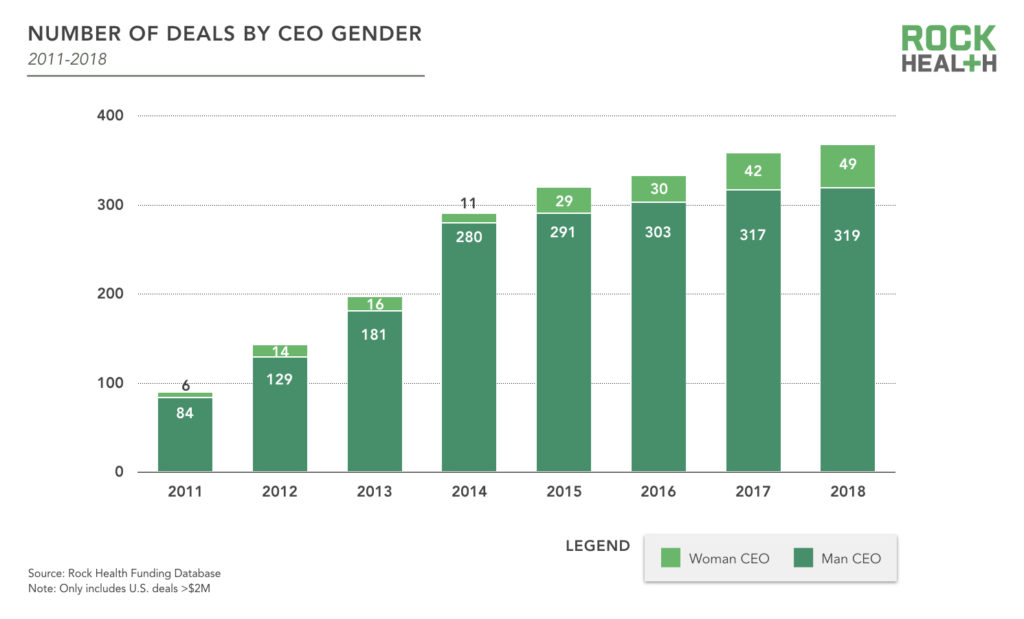

7. Women CEOs closed more rounds in 2018 than ever before, but still represent a small sliver of the pie

In 2018, investors funded one woman-led digital health startup for every six man-led startups. Though still far from where we’d like the industry to be, this is the largest number (49) and percentage (13%) of women-run, funded companies since Rock Health began tracking the digital health sector in 2011.

Partner with us!

A special thank you to our generous corporate partners for their continued support. For full access to the funding report and database, become a Rock Health partner. Get in touch to learn more about how your organization can work alongside Rock Health.

Footnotes

1 Note that numbers in the figure are totals for metro areas, and therefore don’t necessarily sum to state totals.