Digital health’s IPO window is back open

Interested in all the digital health research and datasets Rock Health has to offer? Learn more about becoming a Partner. Email us at partnerships@rockhealth.com to learn more.

Surprised to see the digital health IPO window opening up just three months after the steepest market crash in US history? We sure didn’t predict it, and neither did ten of the other eleven investors we surveyed for our Q1 market insights report. Three digital health companies—Amwell, Accolade, and GoHealth—stepped forward in June with plans to go public in 2020. These announcements came as the stock market found some respite from the gut-wrenching plunge triggered by the initial US COVID-19 outbreak in March. On July 2nd, Accolade went public at $22 per share, raising $220M in the first COVID-era digital health IPO. Two weeks later, GoHealth went public at $21 per share raising $914M. Though volatility persists, the recovery in stock prices provides a newly-open window for IPO-ready companies to raise capital from public investors.

The US’s recovery from the COVID-19 pandemic and its economic consequences is still fragile, to say the least. As of July 20, 39 states are experiencing a rise in cases compared to two weeks ago. Governors are hitting the breaks on plans for reopening their economies. The stock market, reawakened to volatility after years of slow and steady growth, has proven vulnerable to exuberance. Historic levels of unemployment do not signal an economy that is bouncing back. And lost tax revenue together with skyrocketing obligations for health and unemployment benefits will weigh dangerously on government budgets. All of these uncertainties risk dragging public markets back down from current levels. Not exactly a rosy picture for mature digital health companies to be planning their IPOs.

Despite abundant uncertainty, companies are forging ahead with plans to go public. To do so at a time like this is evidence of at least three significant tailwinds that counter the prevailing macroeconomic risks.

1. Flight to quality

As we predicted in Q1 and discussed in our mid-year market update, there are signals of a flight to quality in private markets. Amidst the economic uncertainty of the COVID-19 pandemic, digital health investors are funneling their dry powder into later (Series C+) and larger funding rounds. Established companies that also have COVID-resilient business models (or are being adopted at faster rates because of COVID) may be relatively safe bets for venture capitalists, and we expect a similar dynamic to play out in the market for IPOs.

Digital health IPOs may provide public investors with quality they seek—the performance of several recent digital health IPOs suggests a degree of COVID-resilience within the sector. Since the start of the year, Livongo is up nearly 200% and Peloton is up 90%; Teladoc, which went public in 2015, is up 130%. One Medical, a tech-enabled primary care provider (a bricks-and-mortar provider rather than a digital health company) is up more than 40% since going public on January 31st, 2020. Public markets are favoring software-enabled healthcare and wellness solutions during the COVID-19 crisis, and IPO-ready digital health companies have taken note.

2. Regulatory relaxation

Regulatory barriers to digital health innovation have fallen in the face of the pandemic as regulators rushed to extend healthcare capacity and improve patient access. As outlined in our midyear update, telemedicine’s reimbursement, privacy, and licensure regulations have become increasingly favorable, at least temporarily. The changes are a boon to companies such as Teladoc and AmWell. The FDA also loosened requirements for some remote monitoring and low-risk digital therapeutics, potentially increasing access to solutions from Livongo and others on Rock Health’s IPO Watch List (see below).

Major questions remain as to the duration of such regulatory changes beyond the COVID-19 pandemic, though hints from leading regulators suggest that at least some elements of the new environment will stick.

3. Shifting demand

Since March, demand for healthcare services has changed radically in both volume and channel. ICU admissions surged in outbreak hotspots, elective procedures were cancelled, and primary care went virtual. As the country finds and eventually settles into a new normal, demand for novel healthcare solutions such as contact tracing and workforce reentry will continue to expand. Companies that enable remote and at-scale healthcare delivery are quickly being adopted by enterprise care delivery systems and payers to meet shifting demand patterns—those that are positioned to enable care in healthcare’s new world order will ride the tailwinds into sustainable long-term growth.

The rebound in IPO activity comes on the heels of a big year for digital health public offerings

The two IPOs in July 2020 are restarting the engine for digital health public offerings, which was revving before the pandemic’s US outbreak. Nine companies went public in the last fourteen months, collectively raising $3.9B from public investors—40% as much as the $9.6B raised by digital health startups from private investors across the same time period.

These nine companies didn’t all fly out of the gate at IPO. Livongo, Health Catalyst, and Change Healthcare each saw their stock prices fall below their initial offering price during the first two months on public markets. Of course, the story changes in February 2020. The first COVID-19 death outside China was reported on February 2nd and by the end of the month Italy was struggling with a surge in cases. During that time, Schrodinger—a digital health company that uses AI to discover new drugs—entered public markets on February 6 and promptly rose 194% by February 21. Over the next several days, the share prices of the seven recent digital health IPOs, along with the rest of Rock Health’s Digital Health Public Index, the S&P 500, and the Dow Jones, came crashing down in March. But as the market rebounded in June, so too did the IPO window. Accolade went public on July 2nd, followed by GoHealth on July 15th.

Between March 23rd (the stock market’s low point) and the end of Q2, digital health’s recent IPOs companies recovered to varying degrees:

- Schrodinger: +114% across March 23-June 30 (+439% in H1 2020)

- Livongo: +255% across March 23-June 30 (+197% in H1 2020)

- Peloton: +148% across March 23-June 30 (+100% in H1 2020)

- Phreesia: +49% across March 23-June 30 (+6% in H1 2020)

- Progyny: +57% across March 23-June 30 (-6% in H1 2020)

- Health Catalyst: +23% across March 23-June 30 (-17% in H1 2020)

- Change Healthcare: +37% across March 23-June 30 (-32% in H1 2020)

Notably, though perhaps unsurprisingly, the near-term winners have been digital health companies providing remote care (Livongo), AI drug discovery (Schrodinger), and remote health and wellness (Peloton). Companies whose business models involve selling large contracts to employers and healthcare providers—both of which are facing increasingly tight (in some cases dire) budgets—have not rebounded as strongly from the market crash.

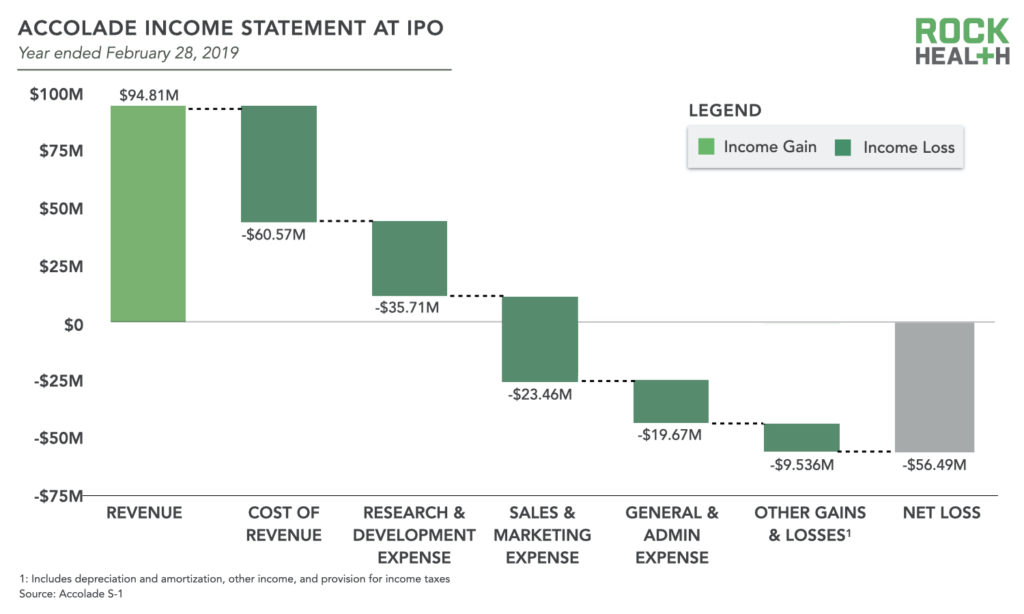

Earlier this year our team combed through the S-1 filings of the recent and upcoming digital health IPOs to build a picture of “IPO-ready” companies. We had planned to share the findings in our Q1 market update report, but when the pandemic broke out in the US our story pivoted. Now that the IPO window is opening up again, we’re publishing this resource with waterfall charts of digital health’s pre-IPO income statements—which offer a snapshot of company revenue, costs, and profit margins. Here we preview findings from Accolade, which went public on July 2nd, 2020. Download the full slide deck to access findings for recent and upcoming digital health IPOs: Accolade, GoHealth, Schrodinger, Livongo, Health Catalyst, Progyny, Phreesia, Peloton, and Change Healthcare.

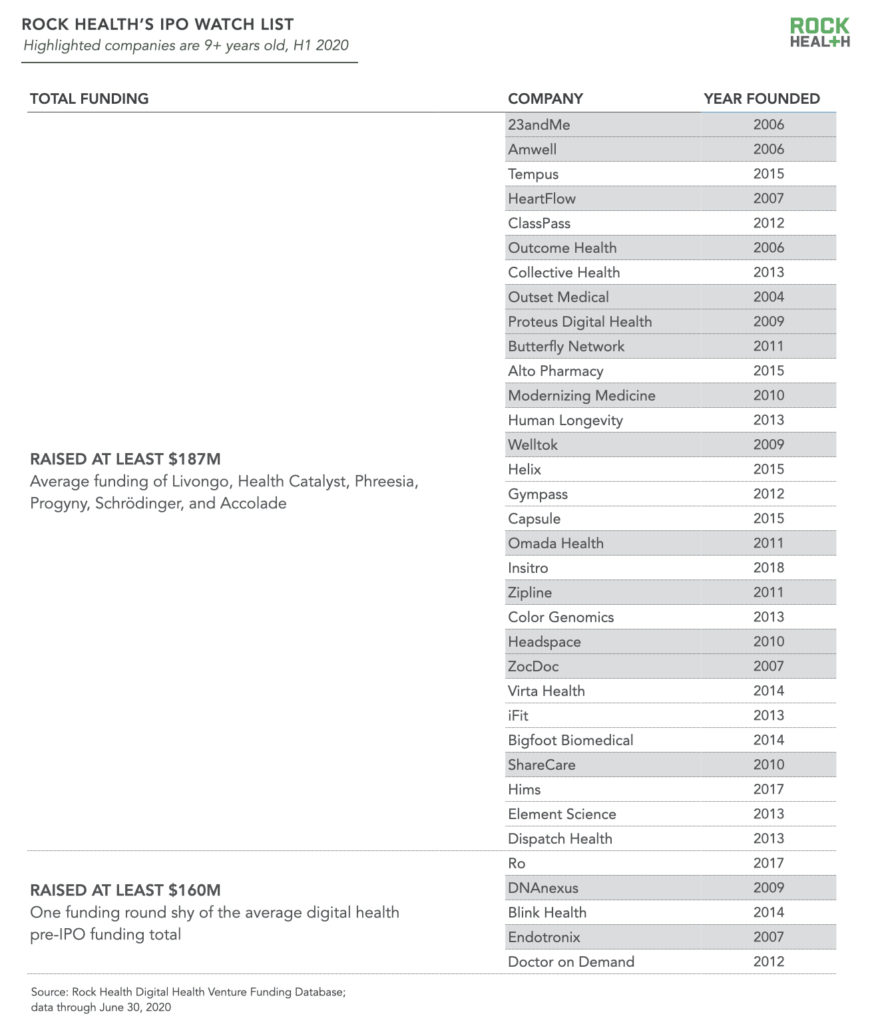

Rock Health’s IPO watch list is growing

There is a large and growing cohort of highly capitalized, mature digital health companies. To build our IPO Watch List, we reviewed pre-IPO capital raised by six recent digital health IPOs. These six companies1 had raised an average of $187M pre-IPO funding. We then compared private companies to this barometer to determine which might be ready to IPO, exclusively based on funds raised. Thirty private digital health startups have raised at least $187M. The list grows to 35 when we add a 15% buffer to the $187M cutoff—up from 23 companies on the IPO watch list when we first published it one year ago.

The future is more uncertain now than at any point in recent memory. There is no guarantee that the current window for digital health IPOs will remain open. But if it does, there are plenty of mature digital health companies that could be nearing such an exit. The COVID-19 pandemic has brought the need for virtual and connected healthcare into stark relief—expect digital health companies to continue tapping public markets for capital to scale their solutions as long as the window is open.

We’re diving into the funding and exit market for digital health at the ninth annual Rock Health Summit on September 22nd-23rd. Register now to lock in early bird pricing for the two-day, virtual event.

Footnote

1We excluded Change Healthcare, because it was previously acquired by McKesson, and Peloton, because its nearly $1B in venture funding is an outlier.