In digital health’s biggest year of funding, women CEOs emerge as Q3 2017 winners

A quick snapshot of 2017 thus far: Coming off the biggest half of digital health venture funding, we aren’t too surprised to announce 2017 as the largest funding year ever. We’ve already had more money poured into digital health companies this year than any year prior—and there are still three months left to go! Despite big bets on the space, digital health investors are keeping their fingers crossed for more exit activity. 2017 has lagged behind prior years with zero digital health IPOs and lower M&A activity. One can certainly argue digital health is still in its infancy, and the prime exits are yet to come. We will be keeping an eye on whether the slowdown in exit activity has an impact on future investor excitement in the space.

Two other pieces of news we’re thrilled to share:

- We’re heartened by another metric that has been advancing this past quarter: 16% of companies funded in Q3 are led by women CEOs. While there is still a ways to climb, 16% is a significant increase from the 11% (and lower) female representation that has more or less held steady for the past few years.

- We’re excited to announce our Digital Health Funding Database revamp! We are gathering more, better data on every digital health deal and company, so expect additional, insightful analysis to debut in our year-end report. If you’d like to participate in our beta launch of the updated database, please email research@rockhealth.com.

For a deeper dive, read on!

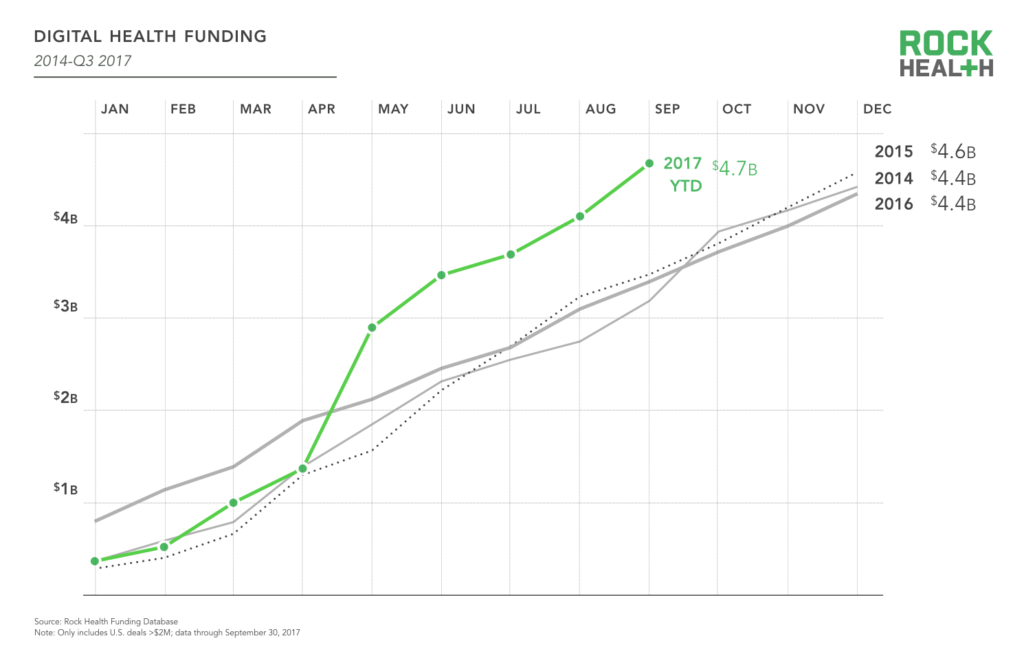

1. 2017 is already the largest year for digital health funding yet—but the funding spike of Q2 has steadied.

We’re coming off a record-shattering period for digital health funding: H1 2017 had the most funding, largest number of deals, and the most mega deals we’ve ever seen in a half-year. Investors have not been quite as prolific from July through September, with Q3 funding at $1.2B—bringing the year-to-date total to $4.7B. However, this is still enough to make 2017 a record-breaking year, pushing funding beyond the prior historic annual high of $4.6B in 2015.

Source: Rock Health Funding Database

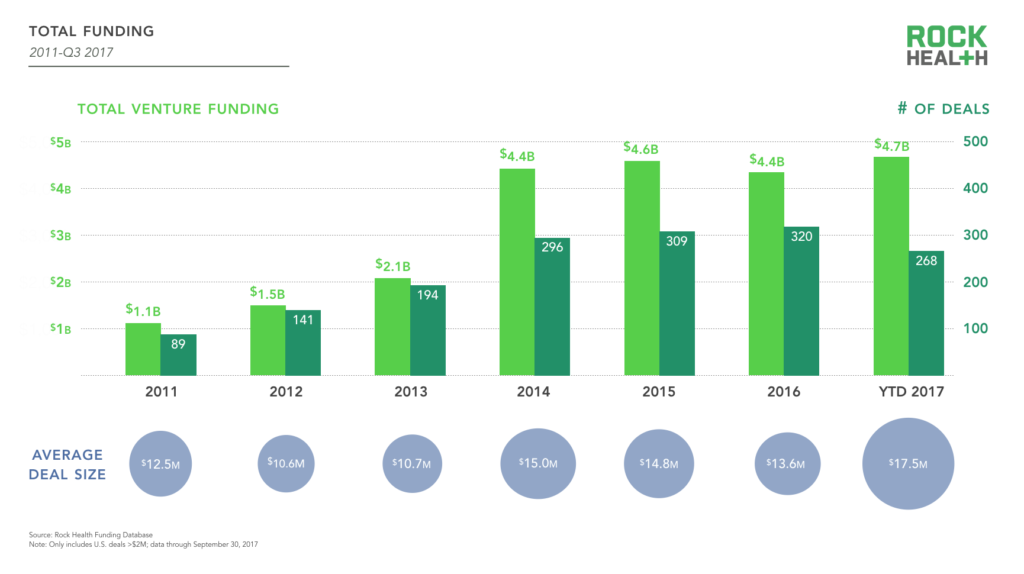

2. We’re also on track for 2017 to have the most deals ever recorded.

Thus far in 2017, there have been 268 digital health funding deals1 across 261 companies. Comparatively, 240 digital health venture deals had closed by the end of Q3 in 2016.

Source: Rock Health Funding Database

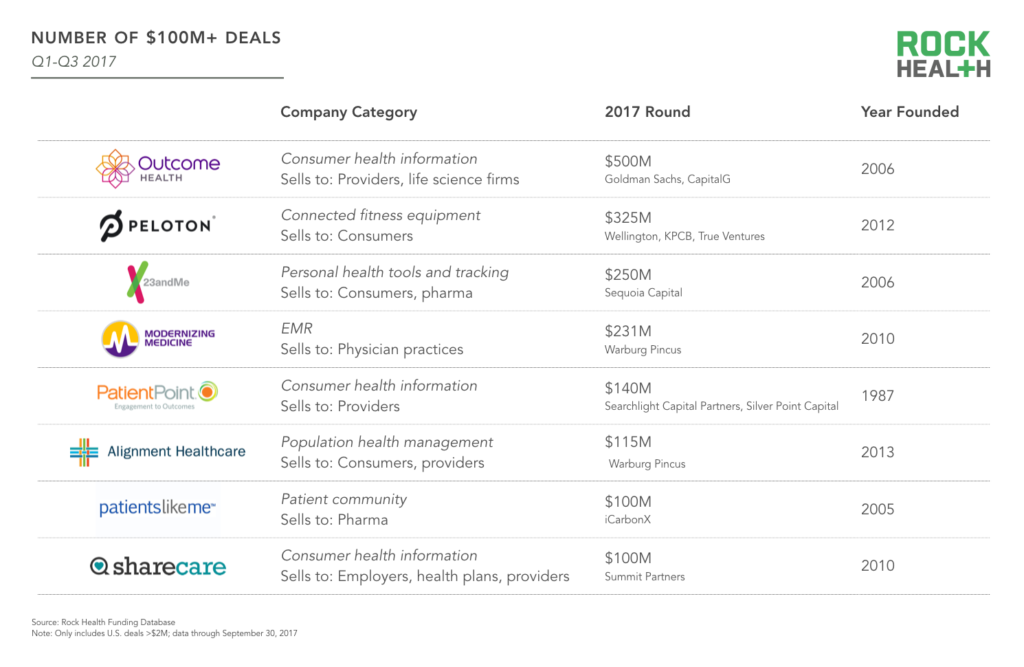

3. Mega-sized deals dominated the first half of the year—but since H1, only 23andMe has raised over $100M.

Seven digital health companies raised more than $100M in the first half of the year. In the months since, only 23andMe has reached mega deal status, announcing a $250M round in September led by Sequoia Capital. The second-largest deal of Q3 came in at $70M for Tempus’ Series C led by New Enterprise Associations and Revolution Growth. As a result, the average deal size for the year is $17.5M—but the average deal size for the quarter dropped to $14.6M.

Source: Rock Health Funding Database

4. 23andMe’s strategy shift is illustrative of a broader migration within digital health to B2B.

After coming out of the starting gates as a consumer-facing genetics test company, 23andMe is now positioning itself for drug discovery. They’ve opened a drug lab, have a large deal to share data with Genentech, and are already publishing clinical analyses. This shift from a B2C business model to B2B is increasingly common in digital health. Based on our recent report on enterprise sales, only 14% of surveyed digital health startups are currently B2C, though many more began there. Sixty-one percent of companies that started with a B2C business model shifted to either a B2B or B2B2C business model.

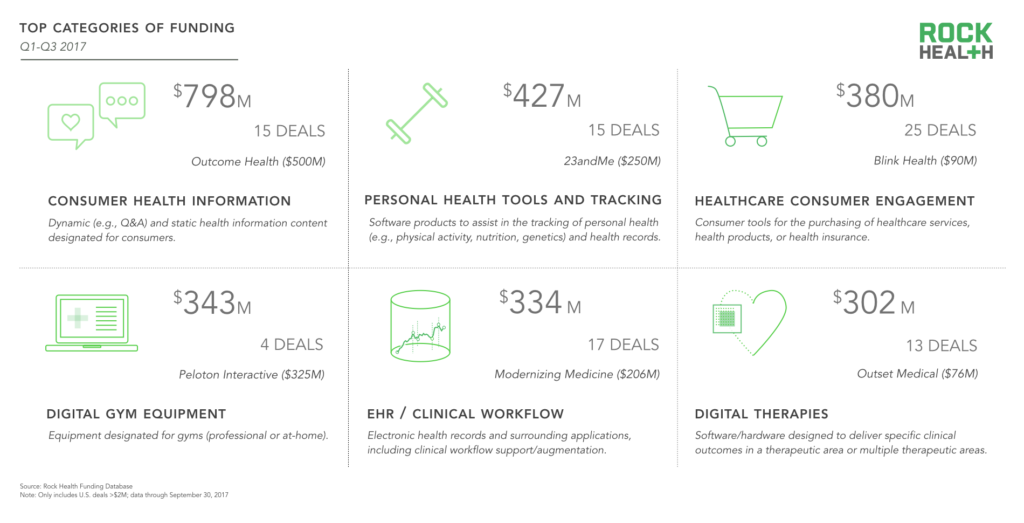

5. Since H1, companies in the “Personal Health Tools and Tracking” space have received significant funding, pushing it into the top six funded categories year-to-date.

The other top categories such as consumer health information and healthcare consumer engagement are bolstered by mega deals from the first half of the year, with these top six categories accounting for 74.3% of total funding in 2017 thus far.

Source: Rock Health Funding Database

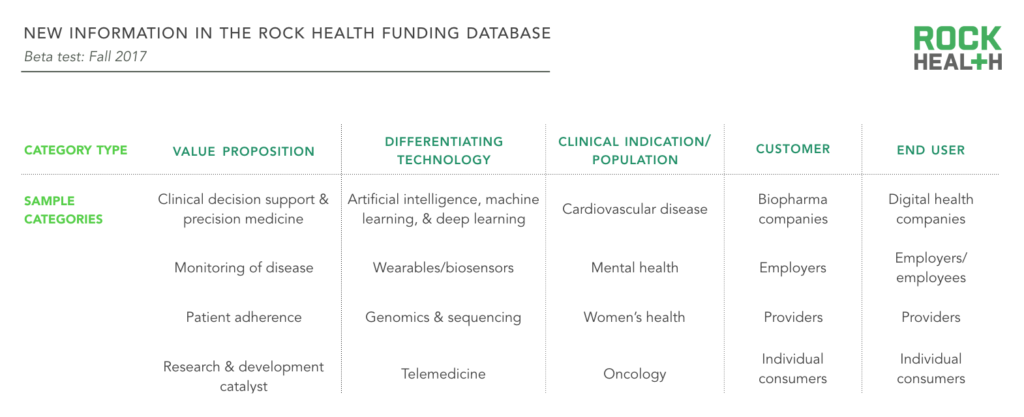

Get ready for a revamped “category analysis” next quarter! Rather than tracking a sole category for each company, we’re taking a new approach that captures the nuanced characteristics of every funded company. We’ll track each company’s value proposition(s), differentiating technology(ies), clinical indication(s), customer(s), and end user(s). This information will be captured in our Digital Health Funding Database and analyzed in our quarterly reports. If you would like to be considered for participation in our beta launch of this database, please email research@rockhealth.com.

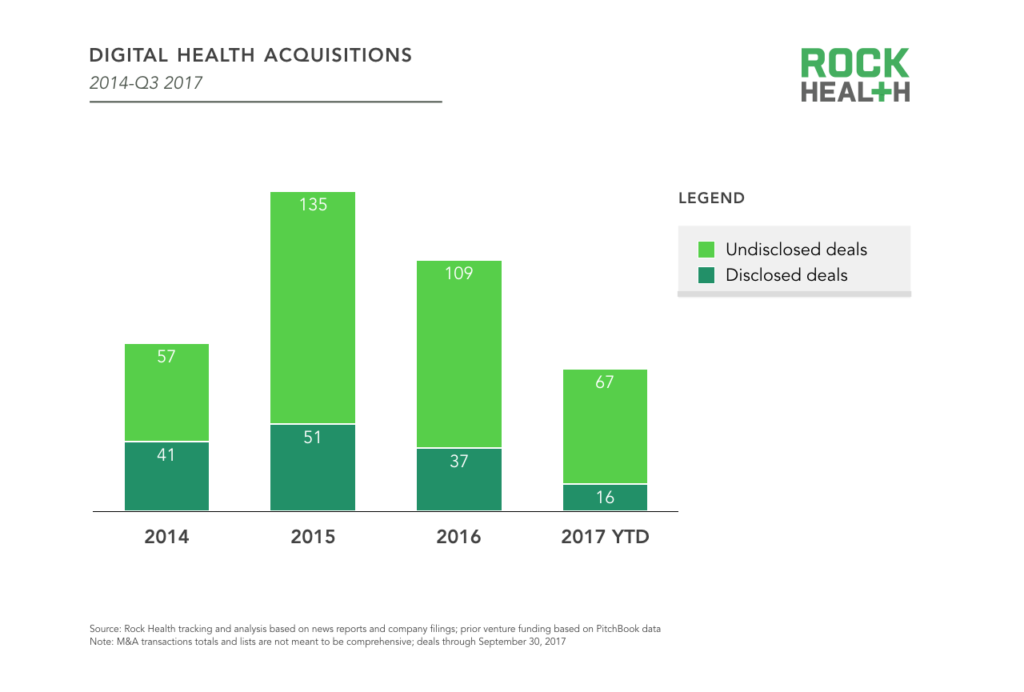

6. A yearlong trend continues: there has been a slowdown in M&A activity, with 83 deals so far in 2017.

We’ve observed this slowing trend in M&A across the past couple of years—last year at the Q3 mark, 112 digital health deals had closed, which was lower than the 146 by the close of Q3 2015. Of the 83 deals reported thus far, only 16 had a disclosed transaction amount—so there’s no clear signal from these deals on how companies and investors are faring.

7. Compared to previous years, there is greater alignment between where venture dollars are going and where they’re getting returned.

EHR and clinical workflow is both a top funded and most acquired category this year. In fact, since 2015, EHR and clinical workflow companies have been the most acquired type of companies, with nine acquisitions of this type thus far in 2017 and 66 total since 2015. Additionally, healthcare consumer engagement companies are among both the most funded and acquired. However, a few enterprise-focused categories are represented as most acquired but not most funded—payer administration (6 M&A deals), physician practice management (5), enterprise wellness (5), and hospital administration (5).

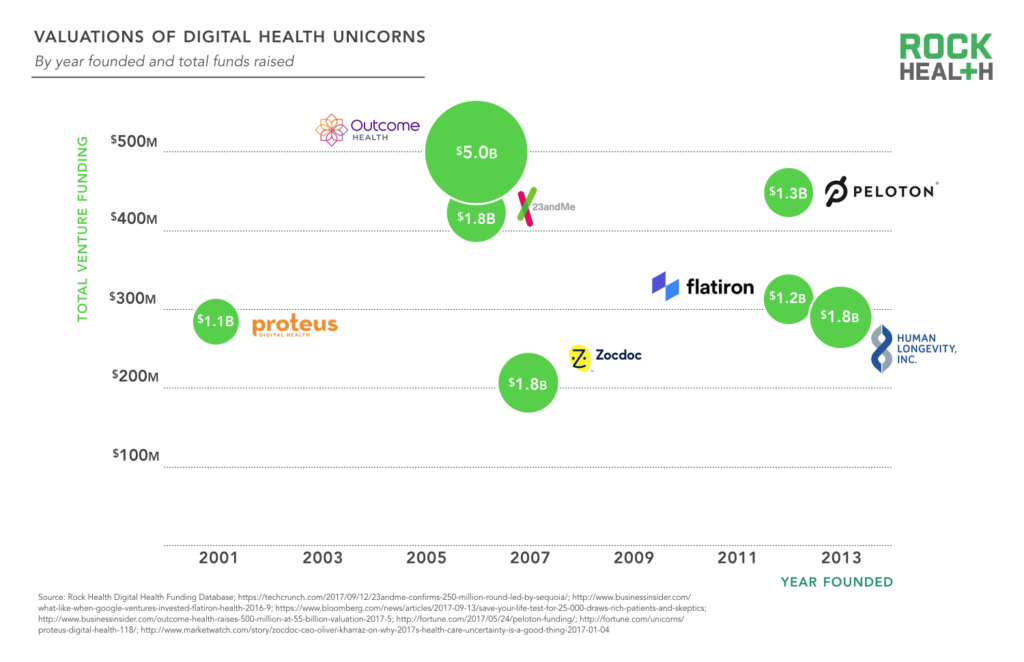

8. There may be no digital health IPOs in 2017.

There has been at least one digital health IPO every year since 2012 (peaking at six IPOs in 2015). But we haven’t seen one so far in 2017. While mega rounds this year have created many highly-capitalized companies—with a handful of unicorns—it’s unclear if these will lead to any movement in the public markets. 23andMe, a unicorn even before their latest funding round and now reportedly valued at $1.75B, decided to raise a big round rather than go public. Until the public markets catch up, shareholders will be relying on acquisitions for any liquidity.

9. Overall, slow movement on the exit markets means investors are oscillating between feeling frustration and preaching patience.

Investors (particularly those newer to the digital health space) may be anxious about the waning exit activity, but others are viewing this as an expected side effect of investing in healthcare with its long sales cycles, high levels of regulation and complexity, and relative immaturity in technology adoption. As Steve Kraus of Bessemer Venture Partners (one of Rock Health’s LPs) posited on our midyear funding podcast, “I think we’re in the early innings of a nine-inning ballgame and at the beginning of the digitization of healthcare.” Our data backs up the notion that taking the longview in healthcare (as both an entrepreneur and an investor) is a good idea. For instance, the eight companies that closed mega deals this year are on average 11 years old—the oldest being Patient Point, founded in 1987, and the youngest being Alignment Healthcare, founded in 2013. Additionally, of the 18 digital health companies that have gone public, the average time from founding to IPO was ten years.

10. We’re seeing slightly more geographic diversity in digital health funding.

California still dominates when it comes to digital health funding, with over a third of funding (38%) coming to companies headquartered in California. Comparatively, Californian companies were bringing in 48% of funding dollars in 2014. Other high-funding hubs this year include New York and Illinois, which represent 15% and 14% of overall digital health funding activity, respectively.

11. You may not have guessed it from this quarter’s industry headlines, but the needle moved in favor of gender diversity in digital health.

Between VC resignations over sexual harassment and the now-infamous Google memo, we were heartened to see a different storyline about women in tech emerge in the digital health world. In Q3, 16% of the 83 deals were raised by companies led by women CEOs. Comparatively, in H1 that number was at 11%. On average, the deal size for companies with a woman CEO in Q3 was $31.4M compared to $11.4M for men CEOs. This is due in large part because a woman, Anne Wojcicki, is the CEO of 23andMe. Excluding 23andMe’s mega deal, the average deal size for companies with a woman CEO in Q3 was $12.2M.

12. Of the 462 unique investors this year, 45% (207) are investing in digital health for the very first time.

Though this is a significant number of “tourist” investors, it’s the smallest percentage of new investors since we started tracking this metric in 2011. In 2015 and 2016, 55% and 52% of investors were new to the space, respectively. The most prolific investors so far this year include: Kleiner Perkins Caufield & Byers, GE Ventures, F-Prime Capital, and Mayo Clinic with six deals each, and StartX, SoftTech VC, and Flare Capital Partners with five deals each.

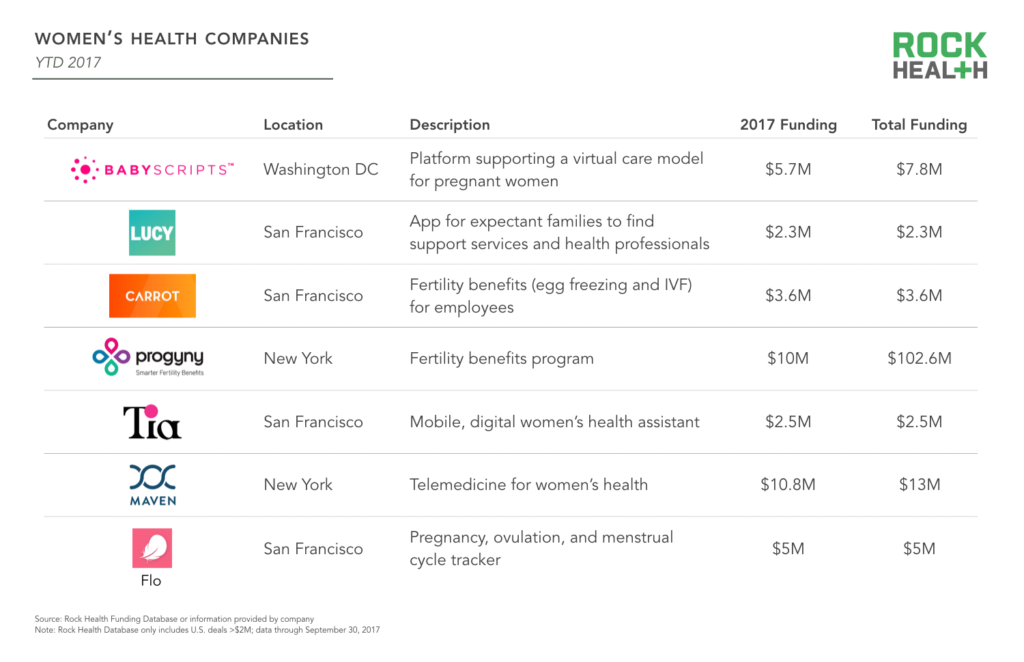

13. Like last year, we’ve seen women’s and reproductive health companies continue to gain traction.

Some—like Babyscripts and LUCY—are supporting pregnancy and expectant families, while others—like Carrot Fertility and Progyny—are focused on fertility benefits. Of the seven companies listed below, four are led by women CEOs and the majority raised their first round this year (congrats!).

Source: Rock Health Funding Database or information provided by company

14. 11 of the 26 companies in our Digital Health Public Company Index are profitable on a shareholder basis, with a positive EPS.

The digital health stocks with the greatest returns YTD are Teladoc (up 101%), Care.com (up 90%), and Tabula Rasa HealthCare Inc (up 79%). The stocks with the biggest losses YTD are Connecture (down 61%) and Nant Health (down 58%).

To get the scoop on every deal, download our Digital Health Funding Database. Or become a Rock Health partner and get access to all reports and data.

Footnotes

1This deal count (and other statistics throughout this post) does not include Availity’s growth investment from Francisco Partners because it was for an undisclosed amount.