Digital health funding 2017 midyear review: A record breaking first half

What a difference three months can make! Just last quarter we described Q1 digital health funding as “business as usual.” Since then, it’s proven to be anything but.

There’s no two ways about it—Q2 2017 was a record-shattering quarter. Though uncertainty around national healthcare reform has dominated headlines, political volatility has not abated investor appetite for digital health. For entrepreneurs, clarity, rather than any particular policy agenda, provides the most confidence to foster innovation and growth. So we were surprised to see that amid one of the most uncertain periods in healthcare history, digital health investments saw their strongest quarter yet.

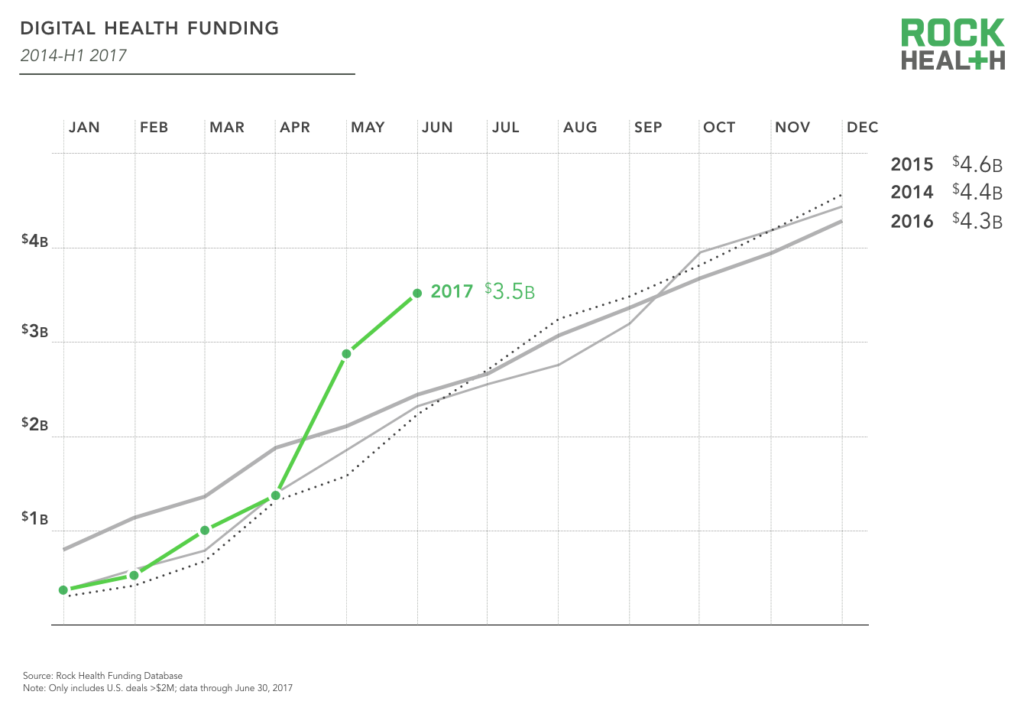

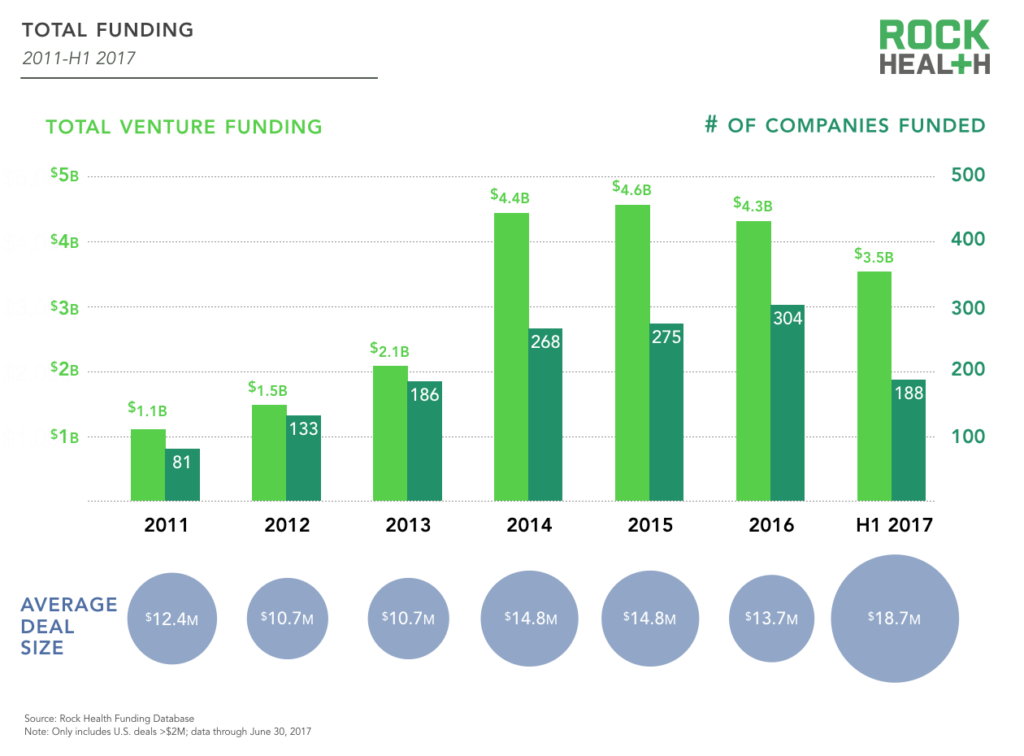

Halfway through 2017, there have been more digital health deals (188) and dollars invested ($3.5B) than ever before in a half-year. We’ve also seen a record seven deals over $100M, with Outcome Health and Peloton Interactive bringing in the two single largest digital health deals ever.

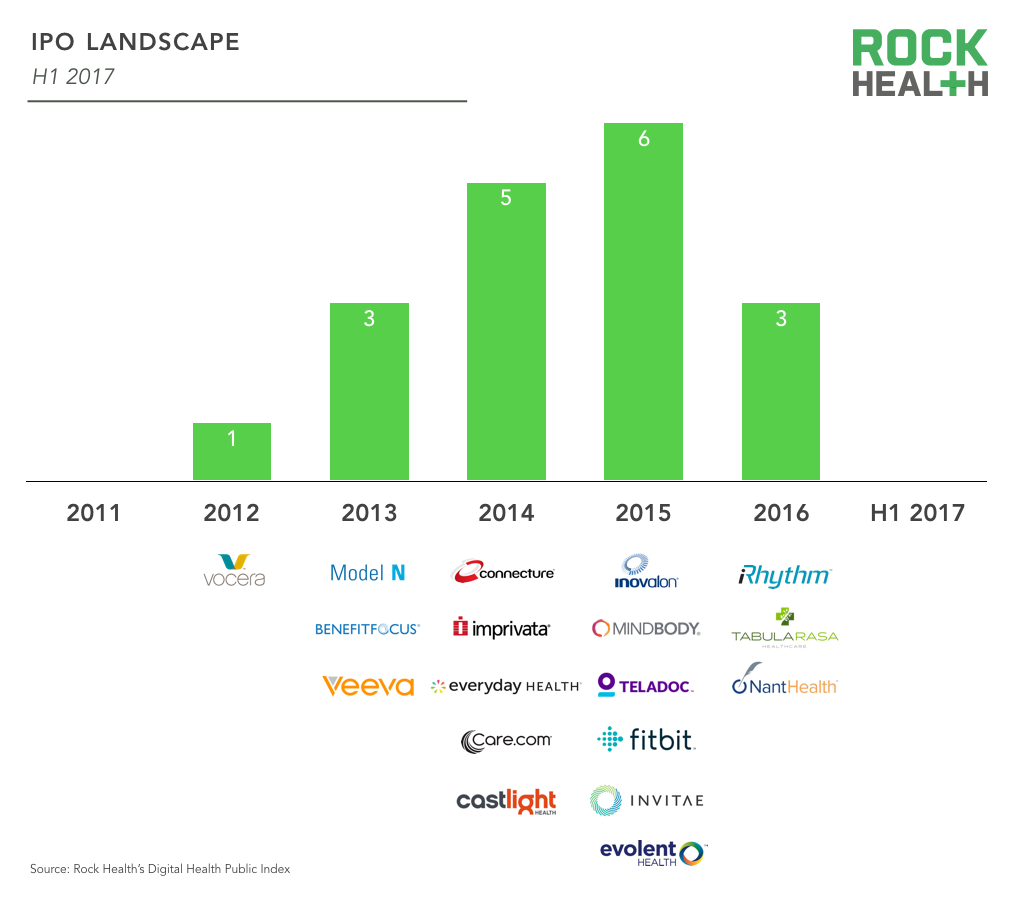

Perhaps even more exciting is what’s yet to come in 2017. Though no digital health companies have IPO’d yet this year, we’ll be keeping an eye on the robust pipeline of highly-capitalized companies that may be on the brink—particularly after the massive funding rounds filling companies’ coffers over the past few months.

Get the whole story! To view our comprehensive analysis of this historic half, become a Rock Health partner. Want access to every tracked digital health deal from 2011 to June 30, 2017? Dive into the data and download our digital health funding database.

Dollars and deals

In H1 2017, we saw more, larger deals than ever before.

The pace of investment in Q2 comes as somewhat of an unsuspected twist—just last quarter, deals were tracking with, but not exceeding, prior years. Then second quarter hit, and funding skyrocketed to unprecedented levels, culminating in the most-funded half-year digital health has ever seen.

Source: Rock Health Funding Database

The growth spurt in funding dollars can be largely attributed to a few massive deals. However, the high number of companies funded signifies that the funding spike isn’t an anomaly based on a few deals, but rather, is an indication of investor excitement in the digital health sector. Although we saw some moderation in deal size last year, the average deal size this year is the largest on record at $18.7M. (Note: taking out the largest two deals, the average deal size reduces to $14.5M).

Source: Rock Health Funding Database

(As a reminder, Rock Health reports only US-based digital health deals of $2M or more. What’s not included? Healthcare services companies like One Medical and Oscar, biotech/diagnostic companies like Grail or Theranos, and software companies like Zenefits and Reputation.com that are not solely focused on healthcare. We don’t report international companies like German-startup Clue, even though many of their users and funders are US-based. We also don’t include grant or government funding, non-dilutive crowdfunding, or venture deals under $2M. Why? By comprehensively tracking companies within clearly defined parameters, our longitudinal data is more accurate and predictive.)

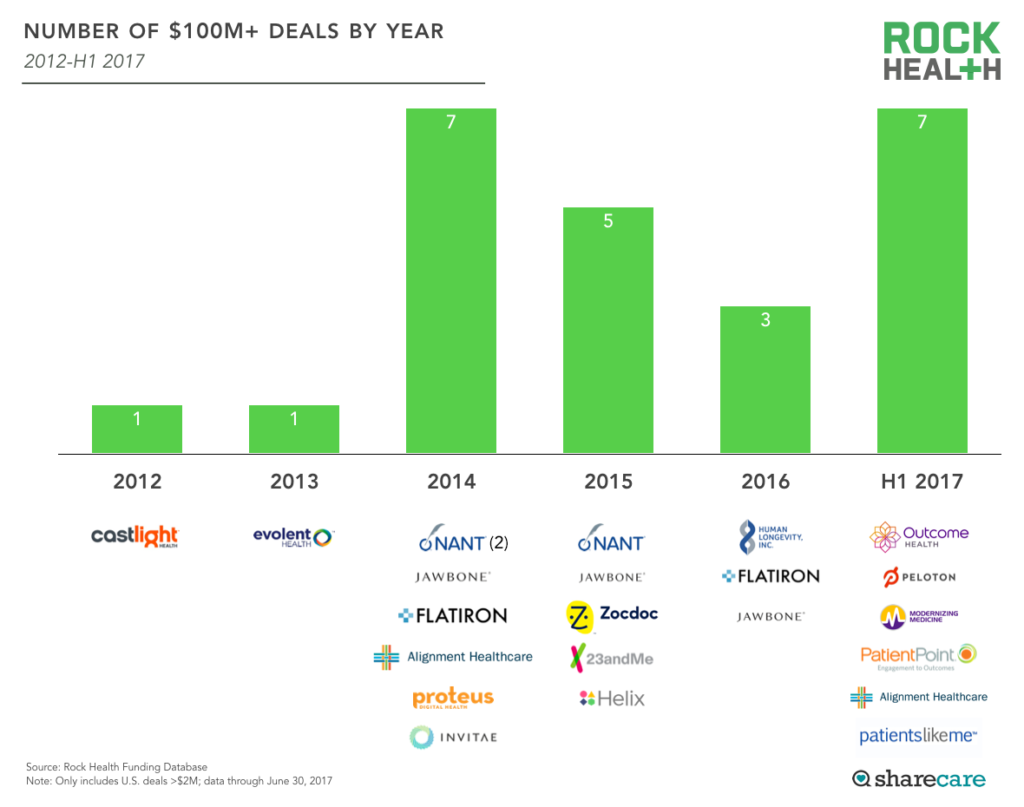

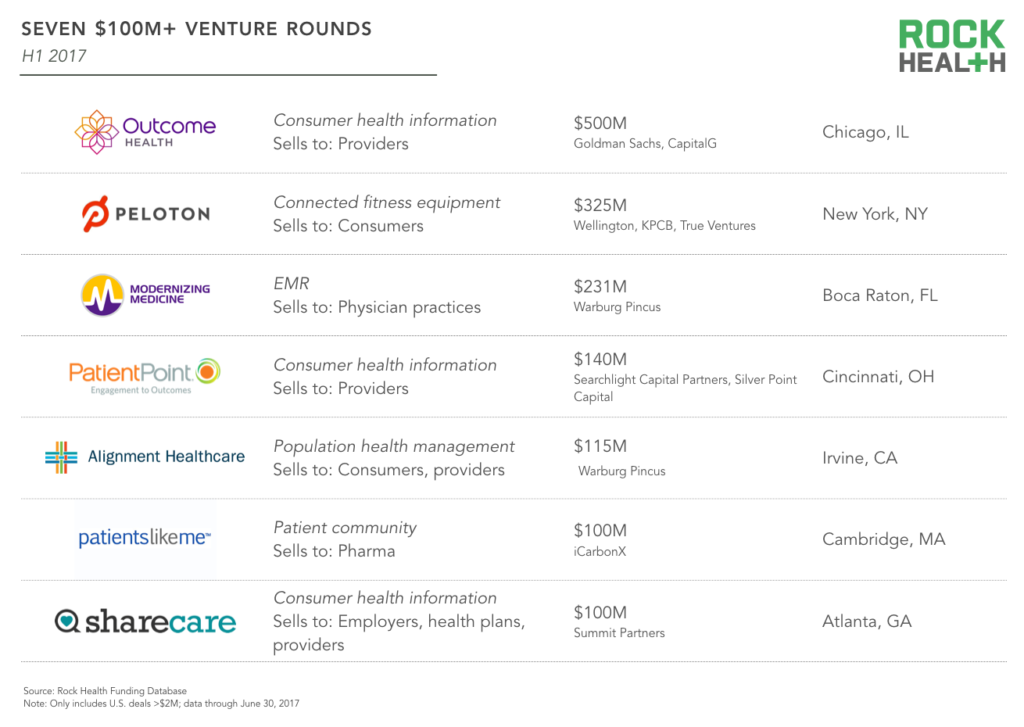

The $100M Club: The first half of 2017 set a record with seven $100M+ mega deals, including the two largest digital health deals on record.

Source: Rock Health Funding Database

Outcome Health closed its first round of funding: a record $500M (on a $5B pre-money valuation 🦄) from growth investors including Goldman Sachs Investment Partners, CapitalG, and Leerink Transformation Partners. Peloton Interactive, with the second-largest round ever, raised a $325M Series E led by Wellington Management, Fidelity Investments, Kleiner Perkins, and True Ventures. Before Q2 2017, the largest digital health deal on record was Jawbone’s $300M funding round from investment firm BlackRock in 2015.

Source: Rock Health Funding Database

As the digital health market matures and companies begin to show real revenue potential, we’re seeing more growth-stage and private equity investors lead large, pre-IPO rounds. While the majority of venture dollars continue to flow to Silicon Valley (more on that below), it’s notable that none of the seven $100M+ digital health deals in H1 2017 are based in the San Francisco Bay Area. Geographically, these seven mega deals are spread across the US.

Since we began tracking digital health funding in 2011, 18 companies have raised 24 unique $100M+ rounds (Alignment Healthcare, Flatiron Health, Jawbone, and NantHealth have all closed multiple $100M rounds). Nearly a quarter of these companies have gone on to raise money on the public markets (via IPO), including Castlight Health, Evolent Health, Invitae, and NantHealth. One, Jawbone, is shutting down.

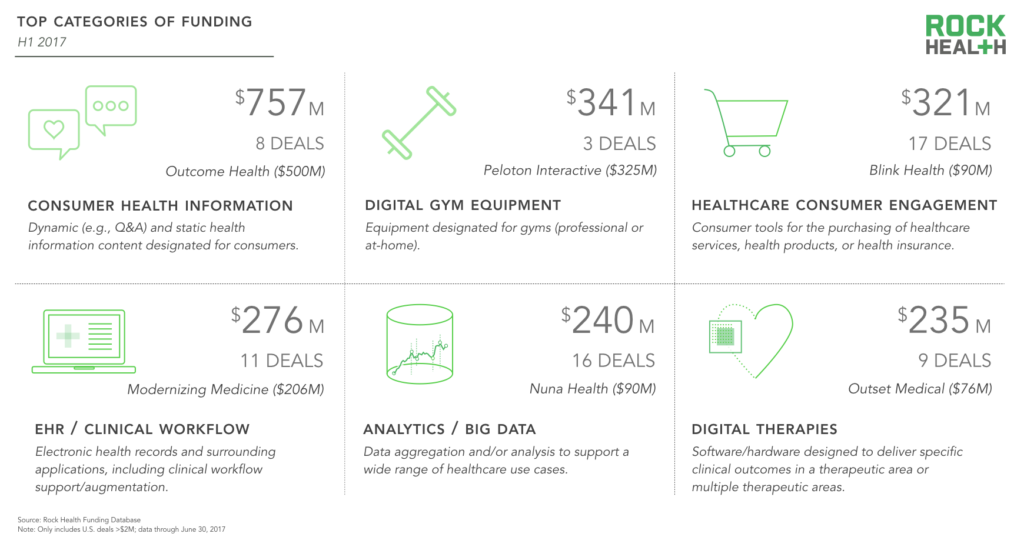

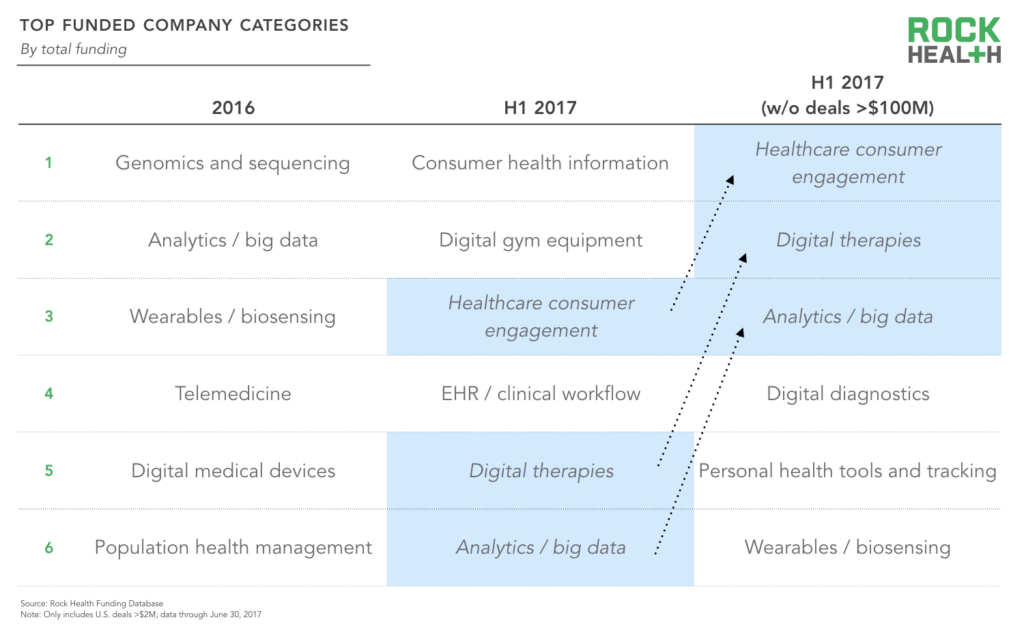

Top categories

The top categories of funded companies illustrate a strong interest in both consumer-facing and enterprise-focused companies.

Mega-sized deals this half-year heavily influenced the top funded categories, with the top six categories accounting for 63% of all digital health funding. Only one of these categories—analytics and big data—was on the top six category list from last year.

Source: Rock Health Funding Database

Due to the outsized impact of the largest deals, the top-funded categories do not provide the full story in terms of which types of companies investors are funding. That’s why we ran the data with and without the top deals over $100M.

Without the top deals, only half of the categories remain in the top six. For instance, Peloton closed a large deal of $325M, but we’ve only tracked seven other companies in the digital gym equipment category since 2011. The top categories with and without the two top deals illustrate a diversity of focus among investors—there is strong interest in both consumer-facing and enterprise-focused companies.

Source: Rock Health Funding Database

Of note, only one of 2016’s top funding categories (analytics / big data) appears in H1 2017’s top categories. Two of 2016’s top funding categories (analytics / big data and wearables / biosensing) appear in H1 2017’s top categories as calculated without the top deals over $100M.

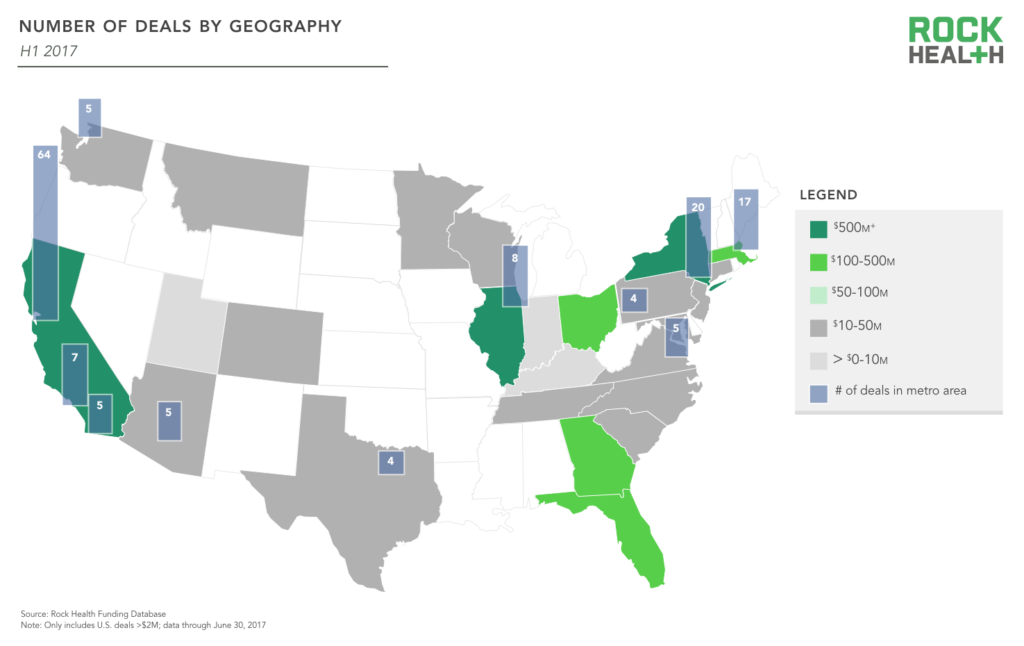

Geographies

Digital health investments reached companies in 25 states, with California accounting for a third of total dollars invested.

For the first time, New York and Illinois joined California in the top tier of funding, with companies headquartered in each raising over $500M+, respectively. Meanwhile, Florida and Georgia joined Massachusetts in the second tier of funding ($100-500M).

As expected, the San Francisco Bay Area continues to solidify its status as the mecca of digital health, receiving nearly as many deals (64) as the next ten metros combined (80). However, deal size outside of the usual hubs has increased: Cincinnati, Bethesda, Miami, Milwaukee, Nashville, and St. Cloud all house startups that received $20M+ rounds.

Source: Rock Health Funding Database

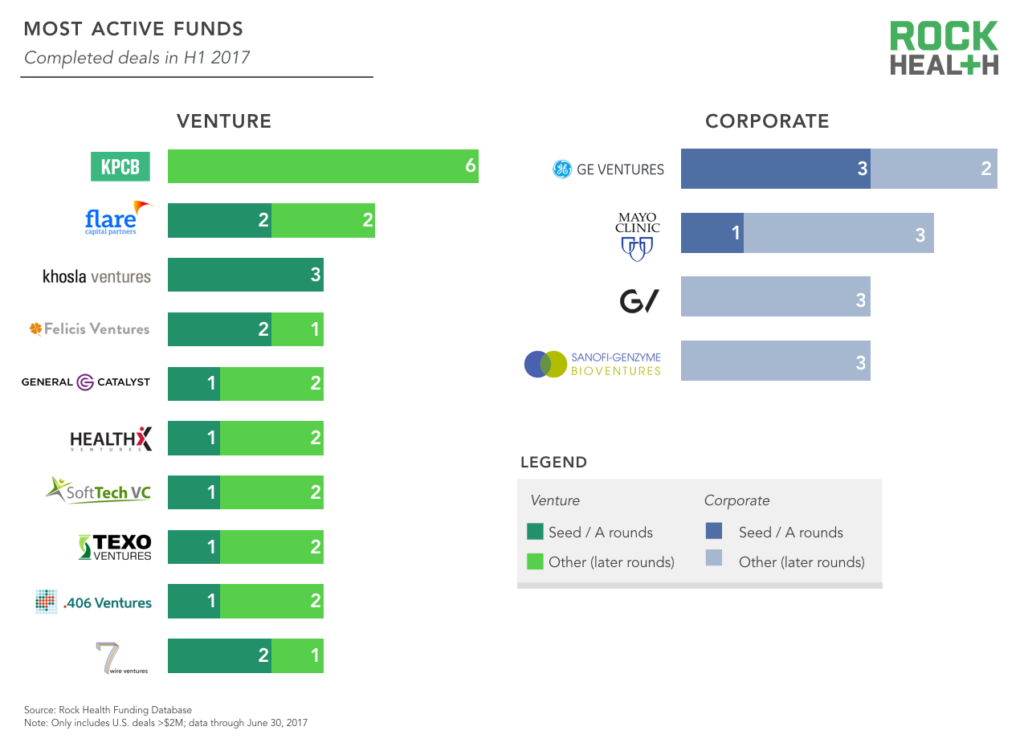

Investors

As in past years, digital health continues to receive support from a long-tail of funds.

Three hundred thirty-one distinct investors completed deals in H1, and 138 of those investors (42%) are new to digital health (despite some predictions that “tourist” investors would retreat from digital health). The number of repeat VCs indicates a continued maturation of not only the companies in the space, but also the firms investing in them—moving beyond dabbling and into double-down mode. Institutional venture firms have been the most active, with 12 firms making three or more investments in H1 2017.

The most active investors are largely on pace with prior years. For instance, khosla ventures and .406 ventures, with three deals each, are in line with their respective annual deal totals of six last year. One notable exception, Andreessen Horowitz, has not closed any deals so far this year despite closing six last year and 21 total over the past six years.

On the provider-as-investor side, UPMC has made just one investment after closing six deals last year. Meanwhile, Mayo Clinic has already made four investments—in the past, they’ve only made up to two deals in a year.

Source: Rock Health Funding Database

Exits

The pace of M&A has slowed, with 58 deals closed by the 2017 midpoint.

We’ve tracked 58 digital health mergers and acquisitions in H1, which is behind the 146 deals closed last year (with 87 by the half).

Notable transactions thus far include <McKesson’s major purchase of Ohio-based CoverMyMeds for $1.1B, Teladoc’s purchase of Boston’s Best Doctors for $440M, and Castlight Health’s purchase of Jiff for $135M. Also, Apple made an undisclosed acquisition of Beddit, a direct-to-consumer play for sleep monitoring.

Source: Rock Health Funding Database

As we’ve seen in recent years, digital health companies continue to be the most acquisitive, scooping up 24 of the companies we tracked. Nearly all types of acquirers—digital health, medical device, payer, technology, and providers—have made fewer acquisitions this half-year than what we would expect based on their total acquisitions from last year.

The top five exit categories include: payer administration, healthcare consumer engagement, analytics and big data, enterprise wellness, and life sciences tools. Of these, two correspond to the top six funding categories (healthcare consumer engagement and analytics and big data). Additionally, the majority of the top exit categories—payer administration and enterprise wellness, among others—signify enterprise plays as opposed to chasing the direct-to-consumer market. Enterprise wellness is picking up steam with five M&A deals completed this year, whereas there were only six across 2015 and 2016 altogether.

Still, half of the top categories for funded companies are centered around the consumer: consumer health information, digital gym equipment, and healthcare consumer engagement. So while exits largely reflect the dominance of traditional enterprise stakeholders in healthcare, investors are still excited about potential in the consumer market. (And consumers are, too—check out the findings from our second annual, 4K-person consumer survey).

Zero digital health IPOs thus far this year; but we predict that won’t be the case much longer.

There have been 70 IPOs across industries so far in 2017, including 11 in software and 14 in biotech. There have been zero in digital health. (Blue Apron went public at the end of June; while we don’t include them in our definition of digital health, one could argue that they’re promoting wellness through nutrition). While the dearth of digital health IPOs in H1 2017 is noteworthy, we believe that the pipeline of highly-capitalized digital health companies means more IPOs are on the horizon.

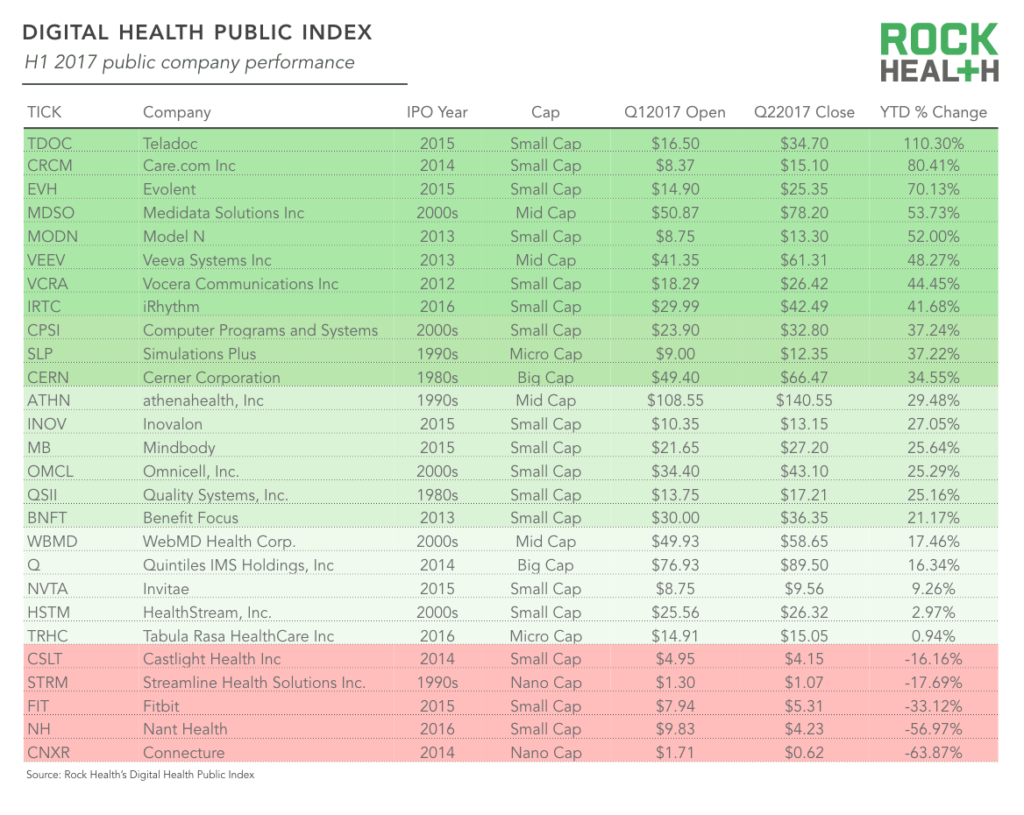

Overall, the Digital Health Public Company Index is up 30% YTD, compared to the S&P 500 Index which is up 8%.

The vast majority of stocks on our digital health public index closed the quarter with positive YTD returns. The biggest market winners of H1 2017 include Teladoc (up 110% YTD), Care.com (up 80%), and Evolent Health (up 70%). Fitbit, which is calling 2017 a “transition year” as they explore more medical use-cases, hit a 52-week low this quarter. Only five companies are trading below their 2017 opening stock price.

Looking forward

Healthcare policy and the future of digital health.

We expect the momentum of the first half of the year to carry throughout 2017. We are on course for a record-breaking year in terms of total funding, number of deals, and average deal size. And with a robust company pipeline, we expect to see new digital health IPOs in the near future.

We also expect digital health to get more attention and definitive guidelines on the regulatory front. Just last month, the FDA’s recently-appointed commissioner Scott Gottlieb announced the impending unveiling of its new “Digital Health Innovation Plan.” The plan seeks to provide further clarity on digital health regulation so entrepreneurs don’t have to seek out the FDA’s position on a case-by-case basis. The announcement was met with initial optimism, and the implications for entrepreneurs will unfold in the coming months.

Along with our industry peers, we will be closely tracking the vigorous healthcare debate (though we do not anticipate policy ambiguity to temper investments in H2 2017). Since venture capitalists raise their funds up front and invest that capital over several years, deal volume doesn’t necessarily trend parallel to policy. However, we do expect to see some shift in the types of startups funded as new policy closes doors for some startups and opens new doors for others.

While the healthcare debate in Washington is centered on changes to coverage reform (particularly Medicaid), government payment and delivery system reforms are still moving ahead. Neither the Senate nor House GOP bills threaten the CMS Innovation Center or MACRA, CMS’ new value-based payment program for clinicians. So as the shift to value-based care continues (seemingly with bipartisan support), the need for innovation that significantly transforms care delivery is as pressing as ever. There will be continued urgency to offer better care at lower costs for patient populations. Additionally, the trend of “patients as consumers” already well underway is expected to grow under the current administration. Both the House and Senate GOP health plans would lead to significantly greater patient cost exposure. This would create more opportunity for companies to innovate around offering more affordable healthcare solutions—and ensuring patients understand and can easily access those options.

Regardless of the outcome of the healthcare policy kerfuffle, we look forward to seeing how startups will continue to meet the urgent needs of patients and transform healthcare for the better.