Pulse check: An analysis of the FDA’s list of AI- and ML-enabled devices

Artificial intelligence and machine learning have come a long way—once buzzwords in digital health, they’re now minted in healthcare’s dictionary. We at Rock Health took a stab at demystifying AI and ML back in 2018 (prehistoric by digital health standards, we know). Since then, both the roles and regulation of AI and ML in healthcare have continued to evolve.

Earlier this month, the FDA shared a database1 of artificial intelligence (AI) and machine learning (ML) enabled medical devices cleared or approved to be marketed in the US. With new publicly available data, we were eager to take a closer look to better understand AI & ML regulatory activity to date. Who has been submitting AI & ML-enabled products to FDA so far, and for what? With the FDA still determining its stance on how best to regulate this technology, it’s useful to get a sense for what has come through its doors so far.

What’s in the database?

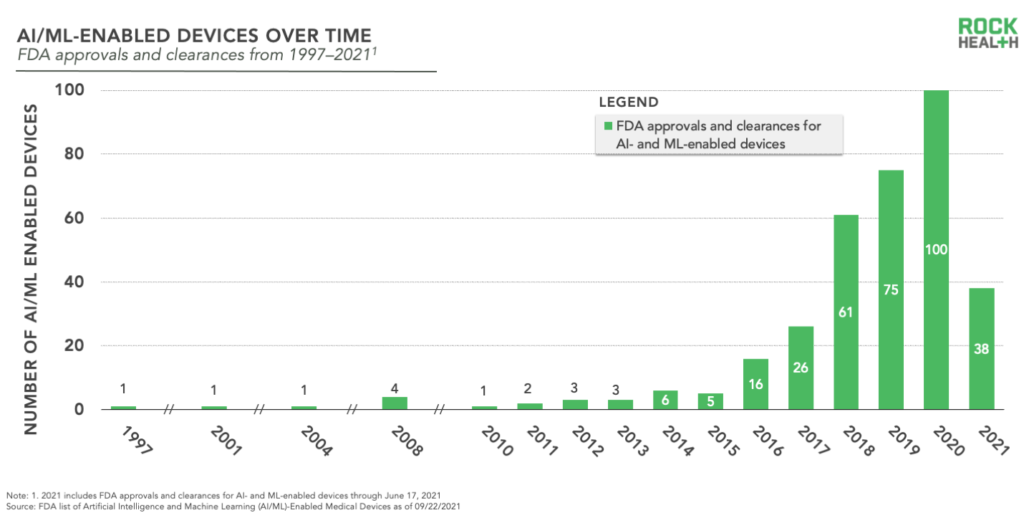

The FDA’s new list captures regulatory decisions from 1997 through June 2021, including 343 distinct entries.

Following the first clearance, the list shows more than 10 years with only a smattering of decisions. The FDA began to consistently approve submissions for AI/ML-enabled devices in 2010—that’s three years after the iPhone was released and just one year before CMS solidified incentive programs for EHR use (both sources of data generation). After a period of steady increase (2010-2017), 2018 shows a sharp influx with 61 entries before 2020’s peak of 100. With 38 decisions through June, 2021 is not exactly on pace to reach last year’s levels. However, we won’t discount the potential for a come-from-behind ending in 2021 (especially given this year’s funding boom across digital health).

What are AI and ML-enabled devices for?

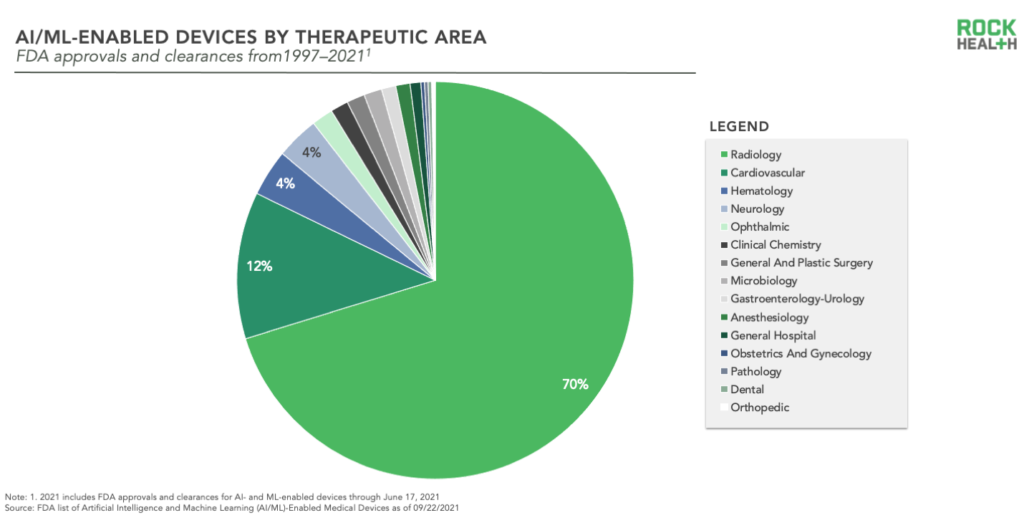

Rather than equally addressing the many clinical indications which could theoretically benefit from FDA-cleared AI/ML tools, the decisions to date are highly concentrated in just a couple areas—namely radiology and cardiovascular. The most common therapeutic area for AI/ML-enabled devices is radiology (by far), with 70% of decisions. Cardiovascular is the second most frequently represented therapeutic area, with 12% of decisions. More surprising, hematology and neurology are next—each with 4% of total decisions. It makes sense that radiology has acted as an ideal sandbox for the development and application of assistive AI and ML algorithms—the number of images producible via scans has increased exponentially, and this available data is horsepower for learning. This is the sandbox that has birthed a number of successful digital health startups including Zebra Medical Vision and Viz.AI, both with multiple entries on the FDA’s new list. With further progress on data availability and interoperability, we expect to see additional sandboxes emerge. We hope developers will take advantage of these opportunities and explore white space for AI/ML across other therapeutic areas.

Who are AI and ML-enabled devices coming from?

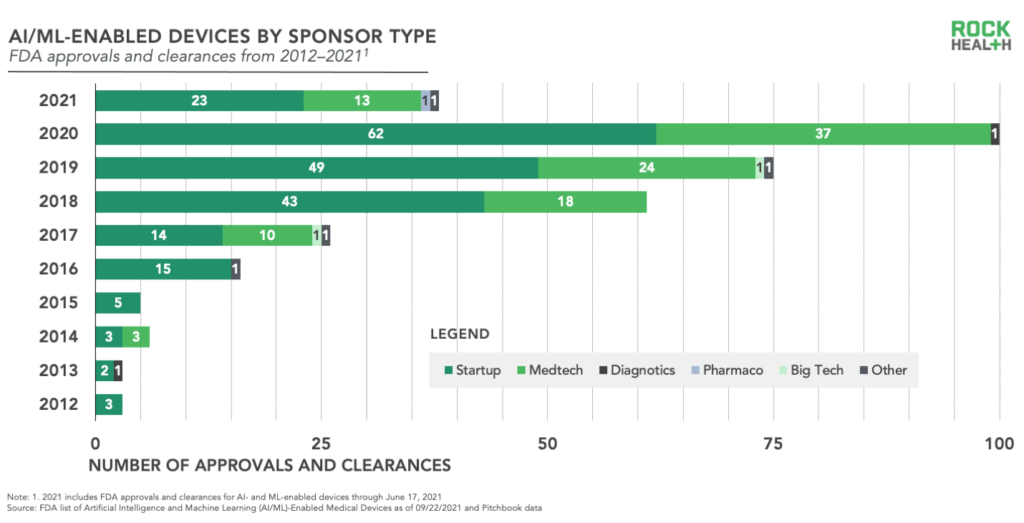

The obvious stakeholders—digital health startups and medtech enterprises—have been and continue to be the primary sponsors of AI/ML-enabled devices submitted to the FDA. All but missing are the other healthcare incumbents—diagnostics, pharma, payers, and providers—and one of healthcare’s new entrants—big tech.

Are these players driving forward business models in digital health which avoid regulatory pathways while the medical/digital device manufacturers establish precedence with FDA?

Among submission sponsors, nearly one-third (~27%) are repeat success stories with two or more entries making the list. Leading the pack are well known medical device organizations, GE Healthcare2 and Siemens3 with 22 and 18 entries, respectively. With big players receiving multiple positive decisions, there’s something to be said for enterprise and their diligent processes and robust resources. However, startups are holding their own in terms of multiple successful submissions led by Aidoc and Zebra Medical Vision with eight and seven entries, respectively.

Where are AI and ML-enabled devices coming from?

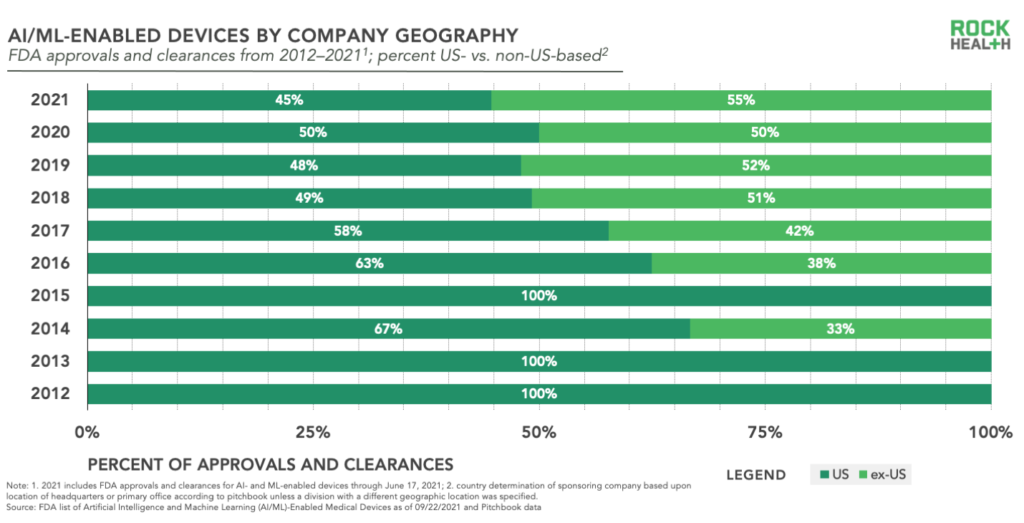

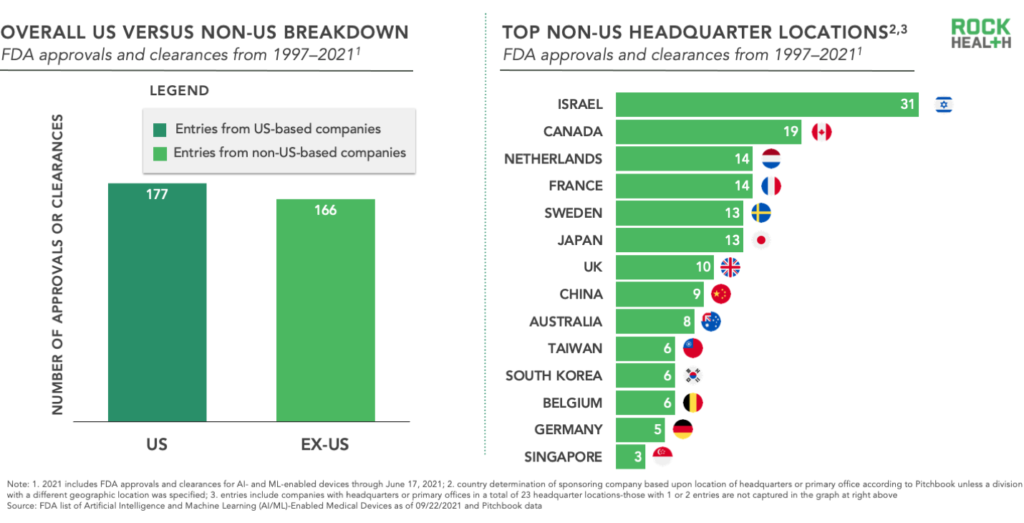

Given the FDA is a US regulatory body, you’d reasonably expect that the majority of companies submitting AI- and ML-enabled device applications are US-based—and overall that would be true. However, in recent years an increasingly large percentage of entries come from companies headquartered outside of the US, reaching 50% of total entries in 2020 and on track to exceed that for 2021.

From a global perspective, Israel—aka startup nation—leads non-US countries in number of entries, which is in line with the country’s established pattern of exporting local innovation to the US market. Canada, the Netherlands, and France follow right behind Israel though in recent years, while companies headquartered in Japan and China have crept in as well. Clearly, digital health is a global market as technology transcends geographic borders.

What does this mean for the industry?

The uptick in FDA approved or cleared AI- and ML-enabled devices is reflective of broader trends in digital health—the overall maturation of the sector and its growing scale, increasing data availability and advancement of science and technology, the crystallization of distinct business models, and the need to differentiate in an increasingly competitive environment.

To date, pursuit of regulatory oversight for digital health has been for the pioneers —however with increasing guidance from the FDA (enter stage right: CDRH Center of Excellence), we anticipate that it will become more mainstream. For clinical care digital health solutions evidence is—or should be—king (psst: hold onto the edge of your seats for upcoming Rock Health research on this topic) and FDA approval/clearance serves as the grand marquee. We’re still in early innings for regulated AI and ML as evidenced by the concentration of solutions in certain therapeutic areas (@Radiology) and a relative dearth in others. We expect to see solutions proliferate across the white space of other clinical areas. And if you’re in those underrepresented sponsor categories (big tech, pharma, diagnostics, etc), we suggest you start to play catch up.

Rock Health Consulting advises enterprise companies on digital health strategy and innovation. For more information, reach out to advisory@rockhealth.com.

References

- FDA (2021) Artificial Intelligence and Machine Learning (AI/ML)-Enabled Medical Devices

- Submissions attributed to GE Healthcare include “GE Hangwei Medical Systems, Co., Ltd.”, “GE Healthcare”, “ GE Healthcare Japan Corporation”, “GE Medical Systems SCS”, “GE Medical Systems Ultrasound and Primary Care Diagnostics, LLC”, and “GE Medical Systems, LLC”

- Submissions attributed to Siemens include “Siemens Medical Solutions, Inc”, “Siemens Medical Solutions, USA, Inc.”, and “Siemens Healthcare GmbH”