Q1 2018: Funding keeps climbing as digital health startups double down on validation

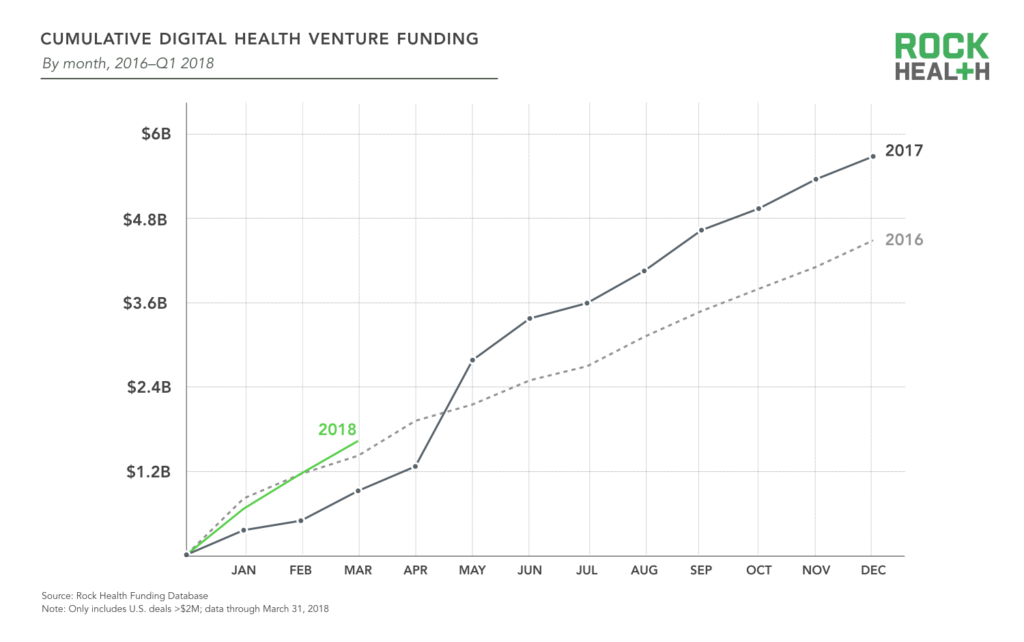

2017 was the biggest year for digital health funding, and investor appetite doesn’t appear to be diminishing in the slightest. In Q1 2018, $1.62B was invested across 77 digital health deals. This supplants Q1 2016 venture funding ($1.41B) as the largest Q1 yet.

Source: Rock Health Funding Database

As the digital health sector matures, investors have become more confident investing in large, late-stage rounds. Last year saw a record eight mega-deals ($100M+) completed, followed by three mega-deals already in 2018: HeartFlow, which creates 3D models of coronary arteries to help providers non-invasively detect coronary artery disease, raised a $240M Series E round; Helix, a consumer genetics marketplace spun out from Illumina, raised $200M; and Rock Health portfolio company Collective Health closed $110M to accelerate development of their health benefits solution for employers. The top 10 deals of Q1 2018 represent over 55% of total funding—but only 13% of deals—in the quarter. The average annual deal size has ticked up over the years, and this quarter was no exception: the average deal size is up to $21.0M relative to $16.4M last year.

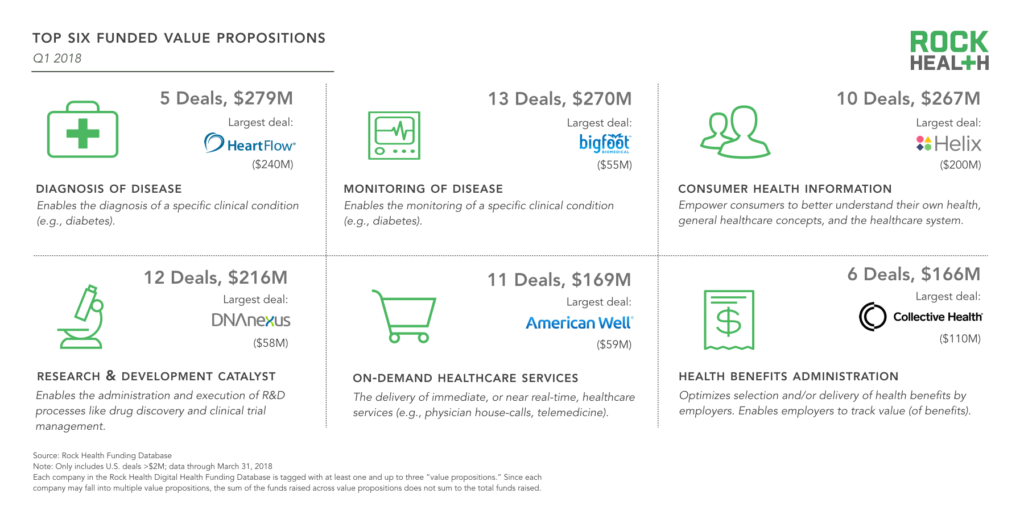

Top 6 value propositions

For the first time, (digital) Diagnosis of Disease was the most-funded value proposition among digital health companies, bolstered by the HeartFlow mega-deal. Monitoring of Disease, the second most-funded value proposition, also had the most deals (13). Here, there was significant clustering around monitoring in the diabetes space, with Bigfoot Biomedical, Sano, Intuity Medical, Siren, and Common Sensing all securing funding this past quarter.

Consumer Health Information—technology used to help patients navigate the healthcare system and their own health—continues to be a top-funded value proposition as well, with Helix leading the way.

We are in the early days of 2018 and a few large deals could dramatically swing these categories one way or another. Even so, we continue to see digital health startups both tackling the clinical aspects of care (Diagnosis of Disease, Monitoring of Disease) and reducing friction between patients and the healthcare system (Health Benefits Administration, On-Demand Healthcare Services).

Source: Rock Health Funding Database

Helix’s $200M mega-deal, along with 23andMe’s $250M round in Q3 2017, demonstrates a growing interest in the genomics space—in fact, digital health companies leveraging genomics and sequencing raised 17% of the total funding from this quarter. Last year, genomics companies accounted for 11% of total digital health funding. With new CMS reimbursement coverage, consumer testing amassing large volumes of data, and better technical infrastructure for precision medicine initiatives (from Oracle and Google), we seem to be hitting an inflection point for genomics.

Compared to last year’s volatile policy debates, investors and entrepreneurs are likely heartened by the progress made this year on the regulatory front. As part of the $400M FDA budget boost, Commissioner Scott Gottlieb has laid out plans for a new Center of Excellence on Digital Health—aiming to establish a new regulatory paradigm which expands its current pre-certification pilot into a program that streamlines review of digital health technologies for companies that earn a pre-certification based on their demonstrated ability to manage the quality and reliability of their software.

We have noticed an uptick in activity among the nine companies participating in the pre-cert program. Pear Therapeutics recently partnered with Novartis to develop and pursue FDA approval for digital prescription therapeutics for schizophrenia and multiple sclerosis. The collaboration represents pharma’s increasing recognition of digital therapeutics as a viable treatment modality and worthwhile business investment. Additionally, Fitbit is planning to seek FDA clearance for its sleep apnea and atrial fibrillation detection tools—a sign of the company venturing more seriously into chronic disease use cases. Apple Health Records launched out of beta allowing patients using certain providers, like Johns Hopkins and Cedars-Sinai, to store and share their medical records on the iPhone. And Samsung’s new smartphones will have a built-in optical sensor to measure blood pressure and stress levels as part of a health study with UCSF. As payers, providers, innovation buyers, and investors demand evidence before adoption (and reimbursement), we can expect more companies to demonstrate the efficacy of digital interventions via controlled studies—and to make moves such as seeking FDA approval to validate digital products as serious clinical tools.

Investors

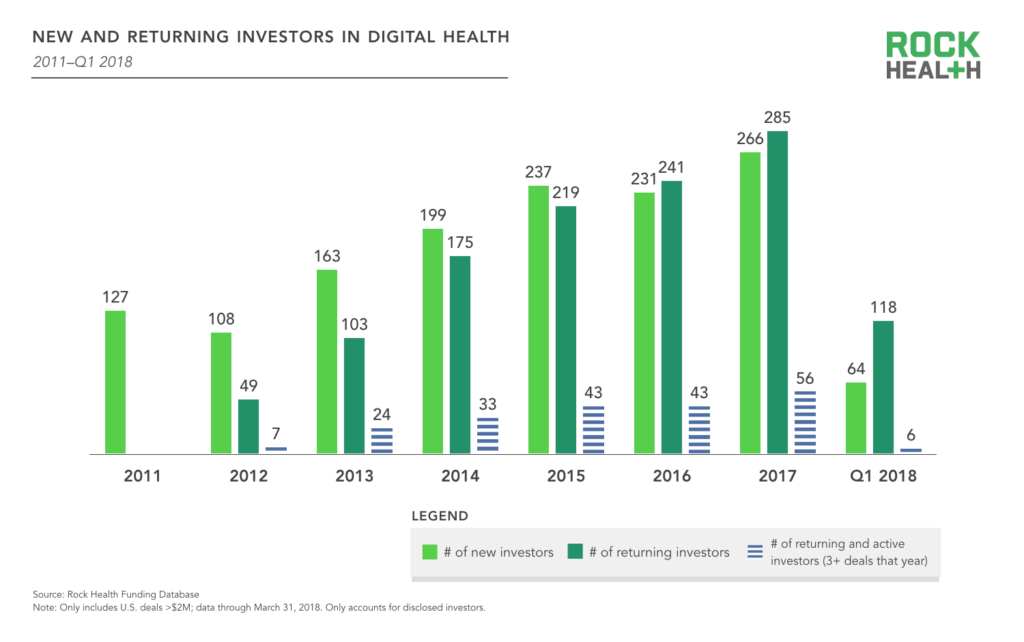

Thus far in 2018, 182 (disclosed) investors have contributed to 77 deals. Beginning in 2016, more than half of the year’s digital health investors were repeat investors who had participated in at least two digital health deals since 2011. This trend continued in 2017, and the spread between returning and new investors continues to grow, signaling investors returning for either follow-on or new investments in the space.

Among all digital health investors, 803 (58%) can be considered dabblers, with only one deal in the space. On the other end of the spectrum, 145 (10%) have made six or more deals.

Source: Rock Health Funding Database

In addition to tracking the investors on every deal, we’re now tracking investor type in our Digital Health Funding Database. We categorize investors as traditional venture capital, corporate investors, private equity, growth, accelerator/incubator, and other (angel groups, family offices, etc.). Unsurprisingly, traditional VCs are the most prominent investors in the digital health space, accounting for 64% of all investor transactions in deals with at least one disclosed investor. Corporations making investments are the next most active type of investor, accounting for 17% of investor transactions. Private equity firms account for 5% of investor transactions.

Source: Rock Health Funding Database

Notes: Number of investor transactions refers to the sum of all investments made by each investor. Please note that a single deal may have multiple disclosed investors, which would amount to multiple investor transactions.

Providers (hospitals, health systems, and physician practices) are the most prolific type of corporate investor, accounting for 24% of all corporate investor transactions in deals with a disclosed corporate investor. Biopharma companies accounted for 13% of corporate investor transactions, followed by payers at 12%. Many of the corporate investors are categorized as “other” since they do not fall into a traditional healthcare company category. These companies include firms such as GE, Amazon, Best Buy, Apple, Baidu, and other non-traditional players who have demonstrated sustained interest in digital health startups—often to advance their own healthcare strategy.

Source: Rock Health Funding Database

Note: Number of investor transactions refers to the sum of all investments made by each investor. Please note that a single deal may have multiple disclosed investors, which would amount to multiple investor transactions.

Corporate investors are acting as one would expect—as strategic investors. Between 2011 and 2017, providers were most likely to invest in digital health companies with the value propositions of Non-Clinical Workflow and Clinical Workflow, payers were most likely to invest in Population Health Management startups, and biopharma in Research and Development Catalysts (e.g., drug discovery, clinical trial management).

Providers’ prolific investments may be due in part to a numbers game. There are just more startups selling to providers than any other customer—60% of digital health startups funded in 2017 were selling to providers, compared to 20% selling to payers and 15% selling to biopharma. In other words, the business value provided by startups most aligns with hospitals and health systems, and so is likely to be of most interest to provider investors.

Rock Health partners can see the full breakdown of investor profiles in our Digital Health Funding Database. If you’re interested, please email us at partnerships@rockhealth.com.

M&A

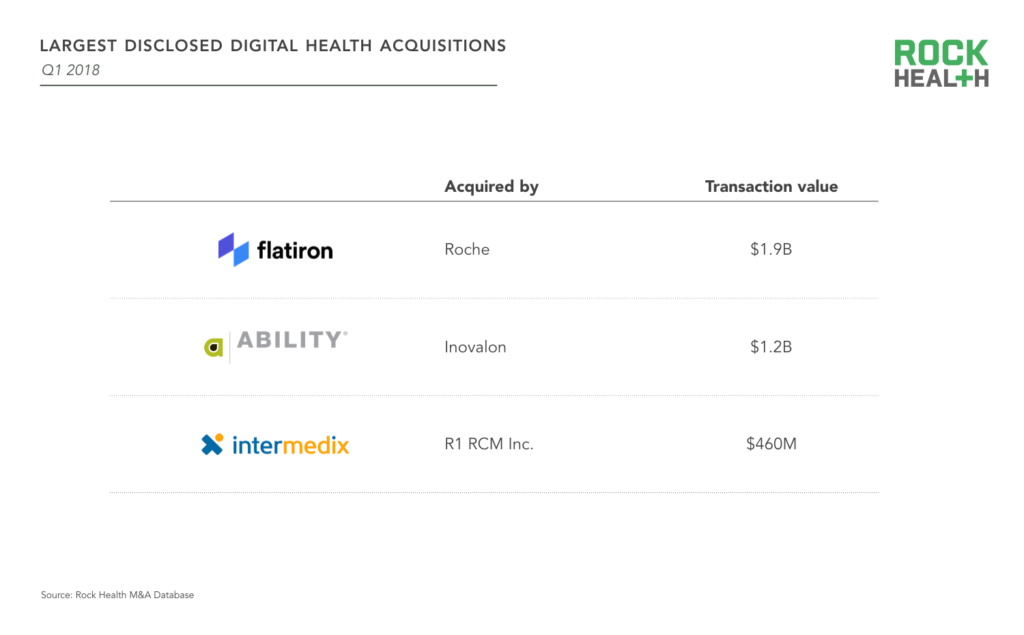

With a handful of peaks and valleys, Q1 of 2018 was a roller coaster for digital health M&A. 37 digital health companies were acquired this quarter, which puts the sector on-track to beat last year’s 119 acquisitions and 2016’s 146 acquisitions.

Source: Rock Health M&A Database

The year began with Allscripts’ $100M acquisition of Practice Fusion—just a sliver of its peak $1.5B unicorn valuation. Allscripts previously offered $250M for the free, cloud-based EHR company, but withdrew the offer after another company in the digital EHR space was fined $155M following a DOJ investigation. This spurred a DOJ investigation into Practice Fusion’s own EHR compliance, which resulted in acceptance of the lower offer with Allscripts taking on full responsibility for the results of the investigation.

Notably, a few weeks later, Roche acquired Flatiron Health for a whopping $1.9B—nearly 1.6X its last valuation of $1.2B. Flatiron was acquired five and a half years after its founding in 2012. The company has aggregated the largest source of longitudinal real-world oncology datasets in the US from the 265 community oncology practices that use their EHR platform, along with six major academic medical centers. Its abstraction process for generating high-quality data directly from the EHR combines the human expertise of clinical oncology experts with targeted implementation of machine learning and natural language processing to increase abstraction efficiency (as an aside, companies leveraging AI/ML algorithms raised $319.3M and accounted for nearly 20% of total funding in Q1 2018). Flatiron’s highly-curated oncology dataset is the key driver of the acquisition and allows Roche to leverage insights on drug efficacy, expedite clinical trials and market launch, and reduce overall R&D costs.

To learn more about how enterprise organizations are leveraging the AI and machine learning startup ecosystem, request an invite to our upcoming Enterprise Insights Forum.

Additionally, Ability Network, a SaaS-based company simplifying administrative tasks in healthcare, was acquired by healthcare data analytics company Inovalon for $1.2B in cash and restricted stock. Fitbit acquired Twine Health (for an undisclosed amount), a company whose chronic disease management platform has produced clinically significant improvements in diabetes and hypertension.

The real-world impact of digital health

Of course, the dollars and cents of digital health do not equate to the sector’s ultimate success: transforming the healthcare system and lives of patients for the better. Last month, we announced the Impact Project—an initiative focused on surfacing the real-world impact of digital health. And validation is critical to that success.

With the theme of impact in mind, here are some of the latest validation milestones of digital health companies, which brings them closer to creating—and scaling—meaningful real-world outcomes:

Virta

Virta, which raised $37M in March of 2017, is conducting an ongoing clinical trial evaluating outcomes of patients with type 2 diabetes who receive the Virta Treatment (262 patients) compared to patients who receive usual care from their physicians (87 patients). Virta’s year-one results were recently published in the peer-reviewed healthcare journal Diabetes Therapy, and included the following outcomes for patients in the Virta intervention group:

- 60% reversed their type 2 diabetes

- 94% reduced or eliminated insulin

- 1.3% average HBA1c reduction at one year

- 30-pound average weight loss at one year

Ambient Clinical Analytics

Ambient Clinical Analytics and Response Evaluation (AWARE)—Ambient’s clinical decision

support tool—was associated with improved patient outcomes and reduced ICU and hospital length of stay. Within four ICUs at Mayo Clinic, overall in-hospital and ICU mortality associated with AWARE intervention decreased by 7%. AWARE also was associated with a 50% decrease in length of ICU stay and a 30% reduction in total hospital stay charges (by $43,745 after adjusting for patient acuity and demographics). Last year, Ambient closed a $5.4M Series A led by Waterline Ventures and Bluestem Capital.

Evidation Health/Lantern

Evidation, in collaboration with a researcher from Stanford Medicine and Lantern, developed an analysis framework to quantify the cost-effectiveness of Lantern’s internet-based, mobile cognitive behavioral therapy (CBT) for individuals with generalized anxiety disorder (GAD). Using this framework, they found that mobile CBT (used in a small pilot program deployed by Lantern) could result in a cost reduction of $2.23B and $4.54B when compared to traditional CBT and no CBT, respectively. In the analysis, mobile CBT also improved health outcomes relative to traditional or no CBT, as measured by quality adjusted life-years. Evidation raised $10M last spring from Sanofi-Genzyme BioVentures to help its partners maximize the impact of their products. Lantern has raised $21M in aggregate funding from UPMC, Mayfield Fund, SoftTech, and angels.

AliveCor

AliveCor’s FDA-cleared personal electrocardiogram (EKG) technology was validated in two separate studies:

- A study published in the Journal of the American College of Cardiology found that KardiaBand, a wearable EKG, can accurately differentiate atrial fibrillation from sinus rhythm when used with the Apple Watch and supported by physician review.

- A second study, conducted in a collaboration with the Mayo Clinic, found that the KardiaBand could detect hyperkalemia when paired with deep learning techniques.

IBM Watson

A study conducted at the Mayo Clinic found that IBM’s Watson for Clinical Trial Matching system resulted in an 80% increase in enrollment to Mayo’s clinical trials for breast cancer. Additionally, the time required for clinical trial eligibility screening decreased when compared to standard methods.

Upcoming studies:

- Omada Health announced the launch of the largest clinical trial of a digital diabetes prevention tool in collaboration with the University of Nebraska Medical Center and Wake Forest University.

- Evidation Health recently launched the DiSCover Project, a study seeking to develop better digital biomarkers to measure chronic pain severity, flare ups, and quality of life. They plan to recruit 10,000 participants in this entirely virtual study.

- In partnership with Merck and the National Sleep Foundation, researchers from Indiana University’s Regenstrief Institute have launched a new study to investigate whether sleep data from Fitbit wearables should become a vital sign considered in the primary care setting.

Is your company participating in a digital health validation study you’d like us to know about? Email us at research@rockhealth.com.

Want unlimited access to our Digital Health Funding Database? Become a Rock Health partner by emailing partnerships@rockhealth.com.