A new research tool for a new phase of digital health: the analyses we now support

Healthcare is complex. And anyone who’s tried to organize, analyze, or sort the landscape of companies in digital health has probably encountered and struggled with this complexity. We at Rock Health certainly have—as have others who come to us for insight. Across the board, we get interesting questions from everyone in healthcare:

- Entrepreneurs looking to develop a competitive landscape

- Major corporations and non-profit health systems seeking to develop a landscape for business development or M&A

- Investors looking to sharpen a thesis or perform diligence on a prospective investment

- Academics looking for data input for their research

To satisfy our own curiosity and to enhance the value we provide, we spent much of the past year updating our methodology for tracking venture-funded digital health deals in the Digital Health Funding Database. We are grateful to our beta users who provided thoughtful feedback on how we could refine the data to best meet their business needs. We are excited to debut this new offering and share a glimpse of the types of analyses it now supports. We’re eager to hear your questions, feedback, and data requests at research@rockhealth.com.

For full access to our research, database, and experts, become a Rock Health partner—get in touch.

2017 was a record year for digital health by many accounts: total funding far surpassed previous years, there were more investors participating in digital health deals, and we saw more mega deals of $100M+ than ever before. With the industry maturing and entering its “middle innings,” our new Digital Health Funding Database enables us to surface and share new emerging trends in the sector.

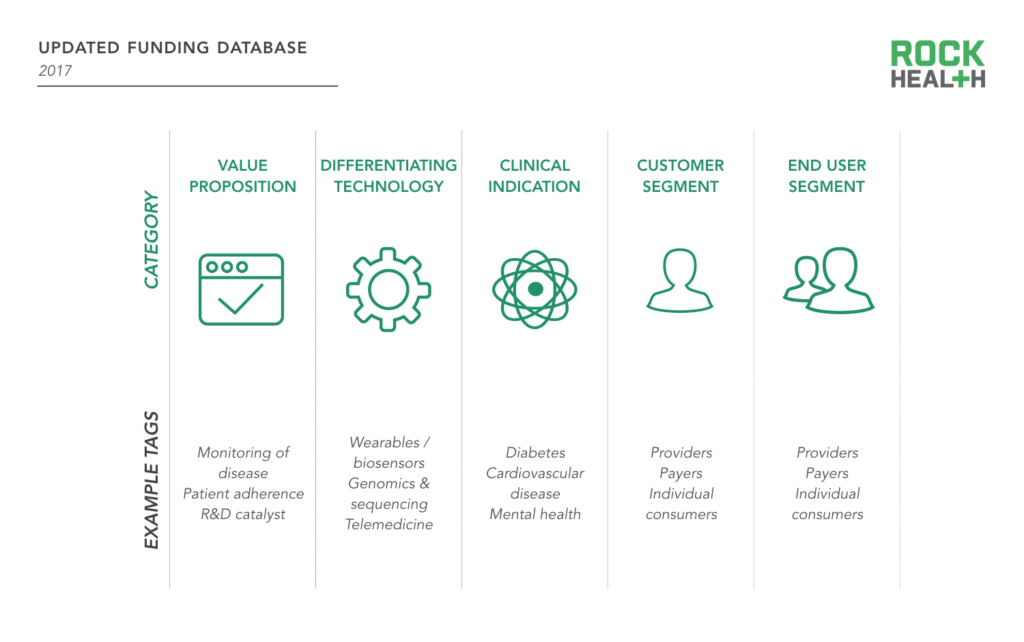

To support this, the database now contains even more information on every digital health deal and company. Instead of assigning each company to a single category, we now capture each company’s:

- Value proposition(s)—value of the product/service that accrues to the customer, irrespective of the mechanism used to deliver the value

- Differentiating technology(ies)—technologies leveraged by the company

- Clinical indication(s)—the primary therapeutic area the company seeks to address (if relevant)

- Target customer segment(s)—purchaser of the product/service

- Target end user segment(s)—stakeholder that uses the product/service

Source: Rock Health Funding Database

The new labels support targeted market scans and emerging trend analysis. Here are just a few of the types of questions the database can now quickly answer:

- Which diabetes companies sell to self-insured employers? (We could also run this analysis for any other tracked clinical indication!)

- Which companies are leveraging machine learning and selling to pharma to optimize drug discovery? How much money have they raised?

- What is the competitive landscape for telemedicine? Are we seeing more telemedicine plays specific to particular clinical conditions as opposed to multipurpose telemedicine? How has funding of this category changed since 2011?

- What are the predominant business models of digital health companies?

Of course, we continue to track all of the usual details, such as information on each company (founding year, founder name, gender, and education) and each deal (deal size, investors, and series).

We’re pleased to see our beta users already finding significant value from the updates.

This database does exactly what I was asking for. I am primarily focused on consumer-facing businesses. The database helps me filter to identify targets to reach out to, informs market mapping exercises, and gets me up-to-speed quickly on competitors in adjacent spaces.

—Sara Eshelman, Principal, Emerging Tech at Omidyar Network

I loved going through the new database! Overall, I was impressed with the ability to make more cuts to identify companies. I use the database for a variety of activities, but usually when a colleague asks a specific question on a company that does ‘X,’ I find that filtering by ‘end user’ and ‘value proposition’ allows me to find that answer.

—Analyst, Healthcare Company

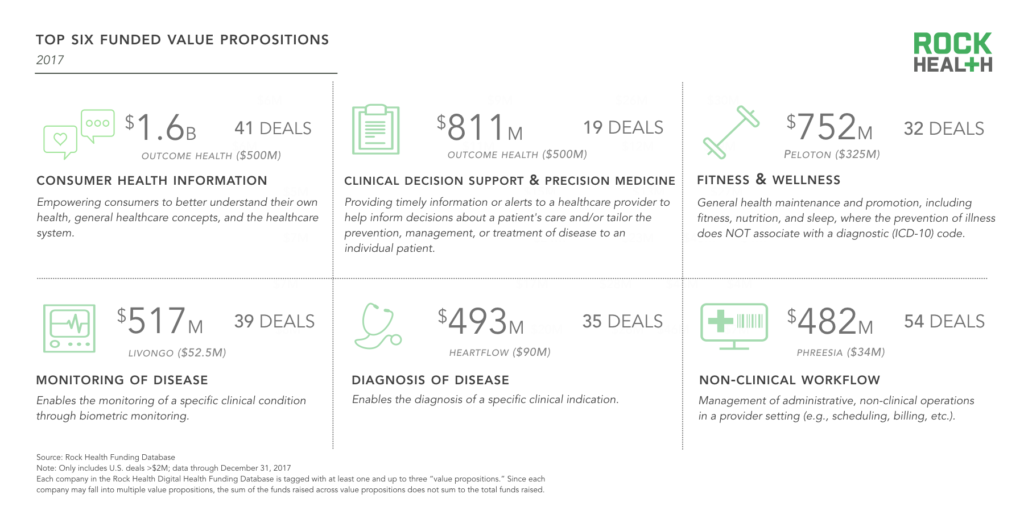

Top value propositions

Source: Rock Health Funding Database

Note: Each company in the Rock Health Funding Database is tagged with at least one and up to three “value propositions.” Since each company may fall into multiple value propositions, the sum of the funds raised across value propositions does not sum to the total funds raised.

In 2017, companies delivering consumer health information topped the charts—with most of the funding coming from five mega deals of $100M+. This is a remarkable increase compared to 2016, when consumer health information did not make the top six value propositions.

Notably, despite delivering health information to consumers, the consumer is not always the paying customer. Thirty-eight percent of these companies are employing a B2B2C model. We explore this industry trend further in our enterprise report.

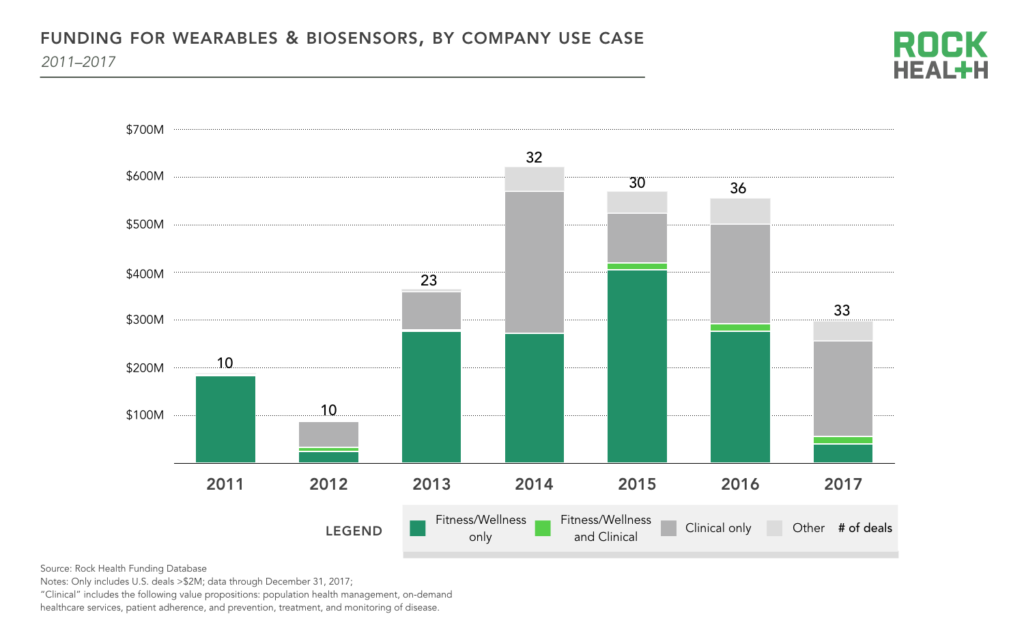

Top differentiating technologies

It’s not just hype—investors are betting on smart algorithms to transform healthcare. In 2017, AI, machine learning, & deep learning was the most funded differentiating technology, with companies leveraging AI/ML collectively raising $698M. With its deal count steadily rising each year, AI, machine learning, & deep learning has been among the top five funded differentiating technologies since 2014. For more on trends in AI in healthcare, watch out for our upcoming report!

While the fifth most funded differentiating technology in 2017, wearables & biosensors was the most-funded technology in 2011—accounting for 17% of total digital health funding that year. At the time, these products were primarily focused on fitness & wellness. Since, the use case for wearables has largely shifted from fitness to specific clinical indications, with wearables & biosensors accounting for just 5% of total venture funding in 2017.

Source: Rock Health Funding Database

Note: “Clinical” use cases include the following value propositions: population health management, on-demand healthcare services, patient adherence, and prevention, treatment, and monitoring of disease.

When reflecting on the rise and fall of Nike’s early wearables, Sr. Director of Nike’s Smart Systems Engineering Jordan Rice noted that while many fitness wearables were sold, they inundated consumers with data without contextualizing the information or delivering an intended impact. Adidas, Nike, and Under Armour have all announced cutbacks in fitness hardware; and Jawbone, once valued at nearly $3B, closed up shop in 2017. The CEO and several employees moved to Jawbone Health Hub, rumored to have pivoted to clinical and health-related devices. Additionally, Fitbit had a tough year on the public markets with shares closing at $5.71 per share—a drop of 71% since going public in 2015 at $20 per share. In response, Fitbit is looking beyond fitness—they are involved in hundreds of research studies (including some focused on diabetes and heart disease) and are joining eight other companies in FDA’s Software Precertification Pilot Program.

Jonathan Palley, CEO of Spire, also reflected on the maturation of the wearables space, noting,

About four to five years ago, there was a lot of hype about the transformative potential for wearables. Unfortunately, people were naive in thinking that the first generation of devices—basic step counters and optical heart rate monitors—were magically going to make them healthier. That era is over. Now we have a much more educated consumer base that is interested and looking for proven products that solve specific problems for them.

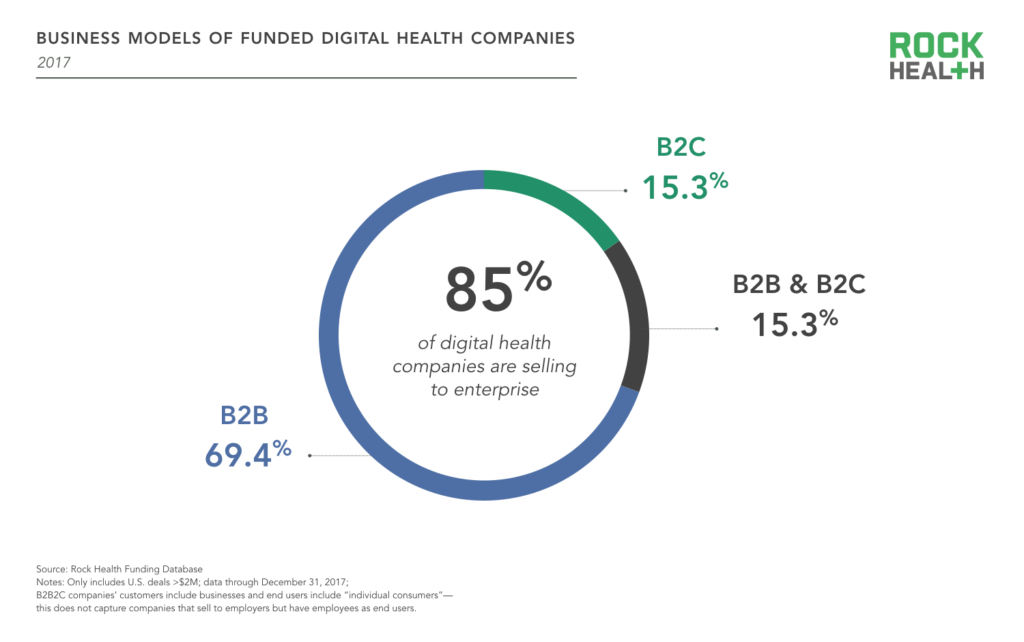

Dominant business models in digital health

We’ve said it before: digital health is a B2B world. 85% of companies funded in 2017 are selling to enterprise. By comparison, 31% of companies sell directly to consumers (and 15% of companies only sell to consumers). Fifteen percent of companies have a diversified customer base, selling directly to businesses and consumers alike, and 39% of companies employ a B2B2C model, selling to businesses to eventually reach consumer end users.

Source: Rock Health Funding Database

Companies finally stopped imagining that consumers would be the ones to pay in US healthcare. True B2C models have declined for this reason, and I think this realization within the sector has made it stronger.

—Deborah Kilpatrick, CEO, Evidation Health

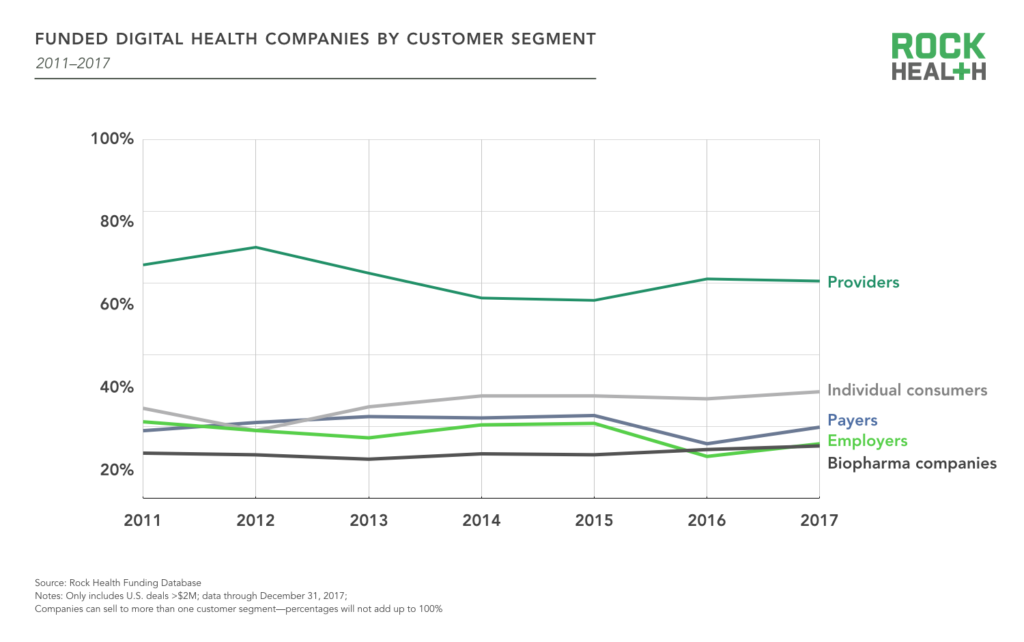

When it comes to enterprise sales, digital health companies are most likely to be selling into hospitals, health systems, and physician offices. Since 2011, more than half of the digital health companies we’ve tracked sell to providers (but not necessarily exclusively to providers). This is significantly higher than the next enterprise customer segment—20% of digital health companies funded in 2017 sell to payers. On one hand, this isn’t too much of a surprise. The passage of the ACA prompted providers to undergo significant payment and care delivery reform, a challenging and ongoing transition that is being supported by many digital health companies. Additionally, we’ve come to know a number of founders and investors who entered the digital health space due to a personal brush with healthcare. Driven by a desire to improve the patient experience, many have focused on the provider-patient interface. However, there are many other (paying!) healthcare players equally in need of transformation via technology.

Source: Rock Health Funding Database

Note: Each company in the Rock Health Digital Health Funding Database is tagged with at least one and up to five “target customer segments.” Since each company may have multiple target customer segments, the percentage of companies selling to different target customer segments does not sum to 100%.

Interviews with investors and entrepreneurs suggested that some of these other customers—like payers and biopharma—can offer advantages over providers, such as immediate access to a large volume of end-users and a more focused sales process.

Pharma is an attractive customer, so I look more for digital health companies selling to pharma. I’ve found providers have been really difficult customers to sell to. The provider market is large and there are lots of discrete problems to solve, but it’s a long commercial path. With providers, the risks are very high if a solution directly impacts patient care, so the technology has to be really mature. It can be easier to sell to pharma because the technology is often supporting infrastructure—not direct patient care.

—Dave Schulte, Managing Director, McKesson Ventures

Payers will be an increasing customer base for digital health companies. They offer something provider organizations generally can’t—an efficient path to scale. What we’ve seen with payers is that if you provide them with a compelling clinical and economic value proposition, they can deploy it to their patient base in a much more rapid and scalable fashion. And they can pay for it.

—Vijay Lathi, Managing Director, New Leaf Venture Partners

I think a large theme of 2018 will be the development of innovative partnership models for distribution. We’re right at the tipping point where classical life sciences will collaborate with digital health more deeply. This has been talked about extensively, but in-practice has not been demonstrated extensively. The maturity of select digital health companies will combine with cultural and strategy changes in large life sciences companies to create new, innovative offerings.

—Sean Duffy, Co-founder and CEO, Omada Health

We’ll be keeping an eye on these predictions and look forward to reporting on how the digital health customer base evolves in the years to come.

In conclusion

We are extremely excited to share our new and improved Digital Health Funding Database! As you review our new insights and explore the database, please share your feedback and comments at research@rockhealth.com. We hope you’re as jazzed about the new product as we are!

For ongoing access to our updated Digital Health Funding Database (with robust information on every venture-backed digital health company and deal), connect with us at research@rockhealth.com.