Q1 2025 market overview: Ready, set, leap

2025 is moving fast right out of the gate. The new Trump administration is reshaping healthcare budgets, leadership, and oversight, setting the stage for changes to reimbursement and innovation. AI’s pace of change is intensifying with new initiatives, investments, and breakthroughs. Venture funding and market dynamics are shifting; startups are facing a more selective investment climate, while challenging markets make it especially difficult for publicly traded companies.

Amidst these shifting conditions, healthcare innovation continues forward at a blistering pace. The year kicked off with big fundraises, product launches, partnerships, M&A, and S-1 filings, raising the question: what’s driving players to make big moves in an otherwise uncertain environment?

To quote Formula 1 driver Ayrton Senna: “You can’t overtake 15 cars in sunny weather, but you can when it’s raining.” Uncertain times create opportunities for players both small and large to jump ahead, or “leapfrog,” over incremental change and shift to more leveraged strategies—but only if they’re willing to take creative risks with new business models and approaches. In this piece, we’ll discuss the leapfrogging strategies we’re seeing startups and large healthcare players deploy in Q1 2025, and how they’re changing digital health norms.

Baselining—what happened in the market in Q1 2025

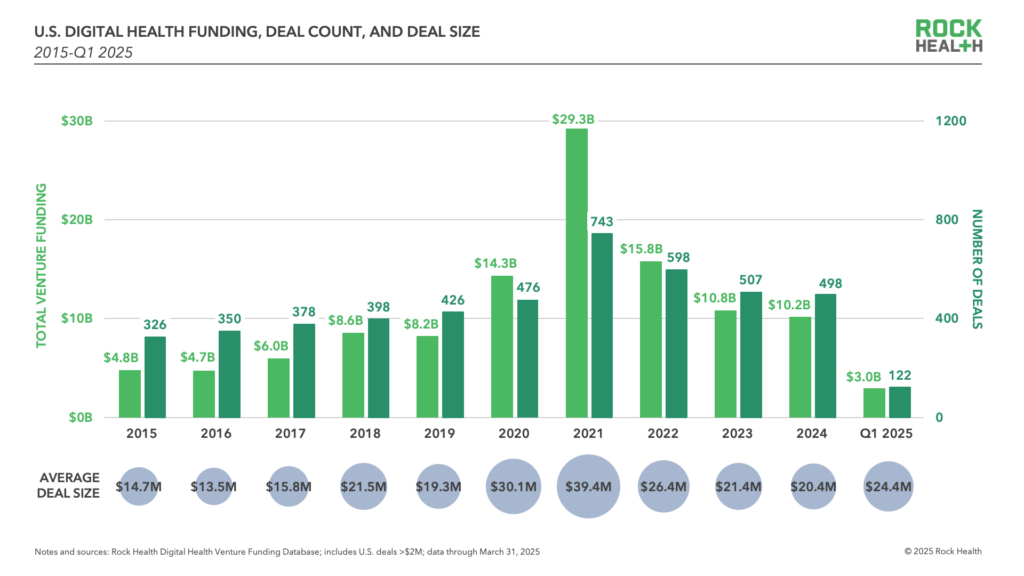

In Q1 2025, U.S. digital health funding saw $3.0B invested across 122 deals. Compared to last quarter, Q1 saw more total dollars invested across a relatively steady deal volume, pushing average deal size from $15.5M in Q4 2024 to $24.4M in Q1 2025. While Q1’s overall funding uptick aligns with seasonal patterns—Q1 funding totals beat Q4 of the prior year in the past four out of five years (2020-2024)—these trends also reflect a continuation of last quarter’s market dynamics and the return of late-stage funding in digital health.

Q1 2025 continued 2024’s David and Goliath story: small, early-stage startups dominated deal count, while the biggest moves (and raises) were helmed by large companies or startups prioritized by mega funders. Earlier-stage raises drove Q1 2025 dealmaking: Seed, Series A, and Series B rounds comprised 83% of labeled deals in Q1 2025, similar to 2024’s 86%. Yet, like 2024, Q1 2025 saw some extra-large early-stage rounds, including Achira’s $33M Seed, Open Evidence’s $75M Series A, and Hippocratic AI’s $141M Series B.

Q1 2025 also marked a return of larger late-stage funding rounds. While Q1 only clocked five raises that were Series D or later,1 three of them were megadeals, or deals over $100M—Innovaccer ($275M), Abridge ($250M), and Qventus ($105M). This cohort pulled the quarter’s median Series D+ round size to $105M—nearly double the $55M median Series D+ check size across 2024, and the first time we’ve seen Series D+ median deal size over $100M since 2021. We’ll be watching to see how Series D+ fundraising progresses throughout 2025—and how companies put this capital to work to scale sustainably.

Approaches to leapfrogging

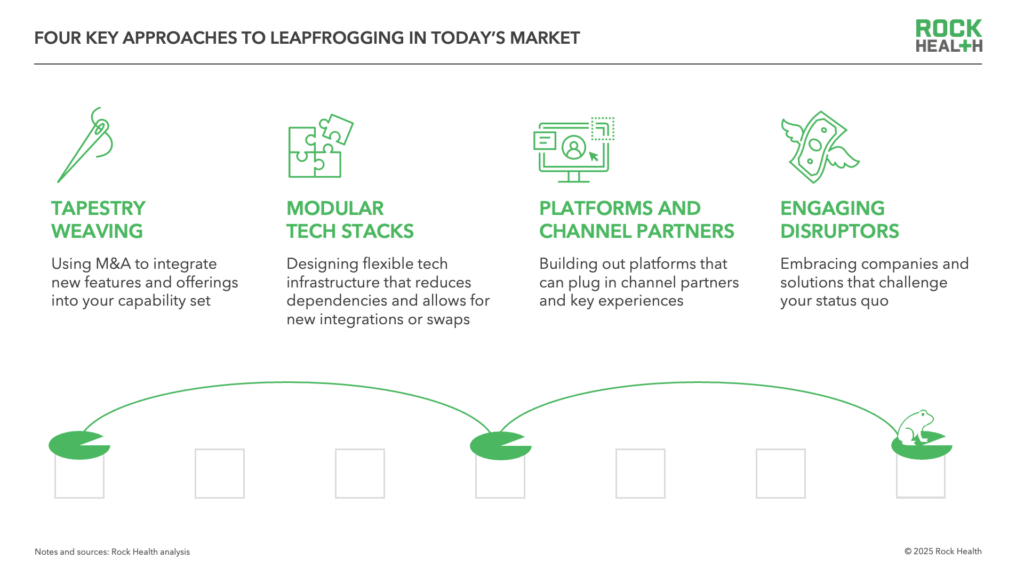

For digital health companies of all sizes, success in this climate requires “leapfrogging,” or leveraging market shifts as opportunities to jump ahead. Understanding leapfrogging strategies can inform one’s roadmap and offer clarity on competitive dynamics. In the next sections, we highlight four of the most common approaches we’re seeing in the market today.

Approach 1: Tapestry weaving

The first leapfrogging approach we’re seeing deployed is “tapestry weaving,” by which companies use strategic mergers and acquisitions to stitch together new features and capabilities into their healthcare offerings. We first reported on this rising trend in Q3 2024 and have since seen a surge in M&A activity involving two or more digital health companies. Of the 46 M&A deals we tracked in Q1 2025, 67% involved digital health startups acquiring other digital health startups—up from 53% across 2024.

Q1’s tapestry weaving deals showcase how digital health companies are using M&A to add new features. Hone Health used its Series A raise to expand into home health services by acquiring Ivee. H1 acquired Ribbon Health2 to offer new payer- and provider-facing products, moving beyond offerings for life science customers. Meanwhile, Hims & Hers leveraged its cash reserves to acquire Trybe Labs to provide more personalized treatment through the addition of at-home testing.

Tapestry weaving spikes when acquisition targets are cheaper and acquirers have cash on hand. That dynamic persists today: some digital health companies are still navigating the fundraising fallout from the peaks of 2020-2021, making them prime acquisition targets, while others have managed their balance sheets or raised enough capital to “buy” assets rather than build internally. We’re also seeing some companies, specifically those with mega investors, raise money with the intention of acquiring assets. In addition to Hone Health, both Flo and Datavant raised late-stage rounds with stated intention of making tapestry-weaving acquisitions.

“The current dominant M&A thesis is that for larger healthcare players with strong distribution, acquiring startups that can use those distribution channels over and over again is the right play. When executed correctly, combining new technologies with distribution results in immediate ROI.”

– Travis May, CEO, Shaper Capital

Approach 2: Modular tech stacks

In this hyper-cycle of AI innovation, healthcare organizations are learning that aligning too closely with any one technology player or solution is risky business. New AI models and working methods (e.g., on-prem versus cloud-based software) are changing the calculus of selecting technology components. In response, we’re seeing both startups and large companies bake flexibility into their tech infrastructure by creating modular tech stacks, where components can be easily swapped out as better or more cost-effective solutions emerge.

Companies that adopt modular tech stacks can more quickly pivot and incorporate new technologies. Take Chinese virtual care provider Ping An Health, which quickly integrated DeepSeek’s LLM into two of its existing medical AI models less than one month after DeepSeek’s official launch. Modular tech stacks enable companies to A/B test models and switch them out based on comparative improvements: see Apple adding Google Gemini to its Apple Intelligence platform, in addition to other internally- and externally-developed AI models. Players like Lumeris are prioritizing the system flexibility of modular tech stacks as a guiding strategy. In Lumeris’ case, their newly-launched Primary Care as a Service agentic AI platform—dubbed ‘Tom’—is leveraging best of breed capabilities amongst 60+ LLMs that can be interchanged for various use cases.

“Our entire team is aligned to taking a modular approach to our product’s tech stack. Even though a faster, cheaper build was possible, there is a shared understanding that building system flexibility is a worthwhile investment, given how quickly GenAI technology evolves.”

– Jean-Claude Saghbini, CTO & President of Technology Solutions, Lumeris

For large organizations, modular tech stacks offer a middle ground in the ‘platform versus point solution’ tug of war, enabling flexibility across technologies while building toward a resilient IT framework. For smaller players, the challenge will be earning—and keeping—that spot within larger organizations’ stacks, which will require both ease of integration and best-in-class performance.

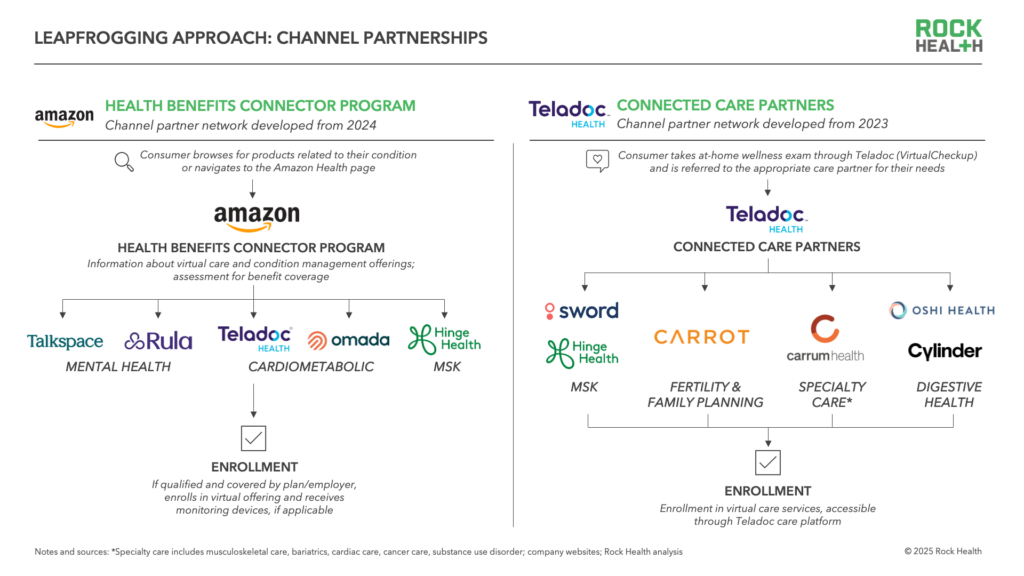

Approach 3: Channel partnerships

New healthcare channels are emerging with robust partner networks that connect consumers to the right partners at the right time. While channel partnerships aren’t new, these coordinated, multi-partner arrangements are redefining how companies present to consumers and extend their influence into new spheres. A frontrunner in this approach, Eli Lilly continues to build out its platform for channel partnerships, LillyDirect, adding new partners in Q1 2025. Other channel partnership initiatives also rounded out their networks, from Amazon’s Health Benefits Connector to Teladoc’s Connected Care Program. Meanwhile, digital health players Wheel and Huma launched a joint venture to offer direct-to-consumer channel access as a service—targeting large companies interested in this approach.

Channel partnerships play to the strengths of both Davids and Goliaths. Smaller digital health companies can continue to focus on high-quality consumer experiences while large players coordinate distribution and reach. However, thoughtfulness is key: while channel partnerships can be a fast track to reaching consumers, they still require care and coordination. Integrated consumer experiences require extra considerations to ensure reliable quality and patient safety throughout the experience.

“Channel partnerships, if done right, can be very successful. Sales cycles are long for healthcare, and for startups, channel partnerships allow you to ‘skip the line’ and acquire customers more quickly in the early stages. But the wrong channel partner is just as bad as the good channel partner is beneficial, so you need to select partners who are top in their class.”

– Michelle Davey, CEO, Wheel

Approach 4: Engaging disruptors

The final leapfrogging strategy is arguably the most counterintuitive, and involves directly engaging with competitors. Especially in times of rapid change, larger companies that embrace startup competitors will be better positioned to navigate—and even influence—market evolution.

The past few months saw big examples of healthcare incumbents engaging the startups trying to disrupt their businesses. To challenge direct-to-consumer virtual care platforms offering cheaper alternatives for GLP-1s, Eli Lilly partnered with virtual care platform Ro to offer consumers access to lower-cost vials of Zepbound.

There are also subtler examples, like Labcorp’s recent participation in Teal Health’s $10M raise, investing in an at-home, self-collecting cervical cancer screening device that redefines the traditional, in-office pap test. Labcorp is proactively aligning with its disrupter, which not only complements its existing diagnostic portfolio, but also reflects shifting consumer preferences. Instead of viewing innovators as outright competitors, these engagements position larger enterprises as partners, investors, or future acquirers of potential rivals.

Be ready to take the leap

Q1 2025 kicked off with rapid shifts in policy, market dynamics, and technology—pushing companies to rethink their footing. As we head into Q2, that volatility hasn’t eased. Embracing uncertainty is a necessary modus operandi for the near term. It’s a mindset we need to generate strategies that turn barriers into opportunities when the moment is right.

Tap into insights and strategic guidance for enterprise companies with Rock Health Advisory.

Get in touch with the venture team at Rock Health Capital.

Join us in advancing ecosystem change at RockHealth.org.

And last but not least, stay plugged into the Rock Health community and all things digital health with the Rock Weekly.

Footnotes

- Series D+ rounds include those designated series D, E, F, G, or H as well as growth rounds; debt and bridge rounds are not included in this cohort.

- Ribbon Health is a Rock Health portfolio company.