Well, is digital health in a bubble or not?

Everyone is asking the question: is digital health in a bubble? The topic is making headlines and is top of mind in our conversations with digital health leaders. As an industry, digital health has boomed in recent years. The pandemic fueled the industry’s growth, accelerating adoption and catalyzing changes to the regulatory environment. Now the macroeconomic outlook has started to dim amidst surging inflation, rising interest rates, persistent supply chain challenges, and geopolitical tensions. Digital health investors and innovators are starting to wonder if the music will stop playing, and if so, what does it mean for them?

In order to address this, we explore three questions:

- Question 1: Is digital health in an investment bubble? – assessment of whether key characteristics of investment bubbles are present in digital health today

- Question 2: How can you assess your bubble risk? – a framework to help digital health innovators assess the bubble risk of their individual sector and/or company within digital health

- Question 3: What should you do about it? – tactical recommendations for innovators, tailored to their unique bubble risk assessment

Question 1: Is digital health in an investment bubble?

What is an investment bubble?

An investment bubble occurs when asset prices (in this case, company valuations) rise far beyond what is justified by fundamentals. This can happen due to excessive hype around an asset or asset class, or runaway herd behavior among investors (Gamestop, anyone?). When investors become wary of a bubble, they freeze new investments, causing a sharp contraction in prices that “bursts” the bubble.

From an entrepreneur’s perspective, the run up to a bubble means (relatively) easy access to capital and the audience of eager investors competing to fund your vision. On the other side of the market’s peak, a bubble’s burst can be harsh. Venture-backed startups that depend on fresh cash injections may struggle to stay solvent as investors shy away from new investments, regardless of their fundamentals.

Assessing digital health’s bubbliness

Given the tremendous rise in venture funding over the past two years, the “B” word comes up with increasing regularity in our conversations with entrepreneurs and investors. We’ve been tracking the bubbliness of digital health since 2018. In refreshing this analysis, we examined six key attributes of past investment bubbles:

- Hype supersedes business fundamentals

- High cash burn rates

- Rapid increase in valuations

- Surge of cash from new investors

- Unclear exit pathways

- Fraud or misuse of funds

Not to keep you in suspense, our takeaway is that digital health is not in an investment bubble, but the market has more froth (i.e., valuation risk) than in the past. Unpacking this along the six key attributes:

Hype supersedes business fundamentals: No

- Various sustainable business models have been demonstrated in recent years, including value-based, SaaS, payer reimbursement, and D2C models (even B2C2B models)

- The pandemic has accelerated adoption and created a more supportive regulatory environment for approval and reimbursement

High cash burn rates: Somewhat

- Some signs that companies are raising (and potentially spending) funds quickly—64 companies raised twice in 2021, 36% more than 2020, and 113% more than 20181

Rapid increase in valuations: Yes (likely, based on deal size trends)

- We based this assessment on the fact that deal sizes are going up—average digital health round size was $39.5M in 2021, up 82% from 2018—and assuming no major change in average investor ownership share2—it appears likely that valuations have increased. This is happening across all parts of the venture life cycle—average Series D+ deal size across 2021-Q1 2022 was $144M, up 98% from the $72.7M average across 2019-2020. Early-stage rounds have also increased significantly, although not to the same extent—Series A rounds were $18.5M on average across 2021-Q1 2022, 61% higher than the $11.5M average across 2019-2020. A variety of factors can influence changes in round size across different stages as the industry continues to mature, but the data is clear on one point: average round sizes are significantly up across all stages.

- The above data is not an indication that valuations are decoupled from fundamentals, though it does illustrate that, on average, investors of late likely valued digital health companies higher than in the recent past. Anecdotally, Rock Health Capital reviewed over 1,200 pitch decks from early-stage companies last year, and observed that valuations were up from prior years.

Surge of cash from new investors: Somewhat

- Growth and crossover funds that are new to digital health have been particularly active in digital health (e.g., Tiger Global made 25 digital health investments in 2021)

- On the other hand, 55% of digital health investors in 2021 were repeat investors—similar to the average 58% repeat investors across the prior three years 2018-2020

Unclear exit pathways: Somewhat

- After a boom in public exits in 2021 (eight IPOs, 15 SPACs), there have not yet been any IPOs or SPACs yet in 2022 (although five are planned). The slowdown comes amidst cooling public market conditions in the face of macroeconomic headwinds (e.g., rising interest rates, geopolitical conflict)

- 58 digital health merger or acquisition deals through Q1 2022 puts the industry on pace for ~200 deals this year—off pace by about a quarter from 2021; still up from the average of 130 per year across 2019-2020

Fraud or misuse of funds: No

- Few signs of dotcom era-style extravagance or fraud (there are a few rumblings of misconduct by recently public companies; those lawsuits are not yet concluded)

We do not believe digital health is in a bubble—proven business models, a stable pool of experienced investors, and a robust (if moderating) exit market paint the picture of a sustainable investment sector. That said, froth has clearly increased across the past three years with valuations increasing and companies raising rounds more quickly. Yet, digital health is not a monolith—the bubble risks will vary across different segments within digital health. Therefore, we posit that some sectors within digital health are, in aggregate, seeing valuations that may outstrip their business fundamentals, while other sectors are attracting valuations in-line with their long term opportunities. Next, we present a guide for startup and enterprise innovators to assess the bubble risk within their own segment of digital health.

Question 2: How can you assess your bubble risk?

The danger of a frothy investment market (and the deflation that may follow) is that it becomes difficult for companies to raise capital at valuations in-line with their business fundamentals. Digital health is composed of many different segments, and the bubble risk and implications for digital health innovators will vary across segments. Here, we aim to give innovators a framework to understand the bubble risks in their particular segment.

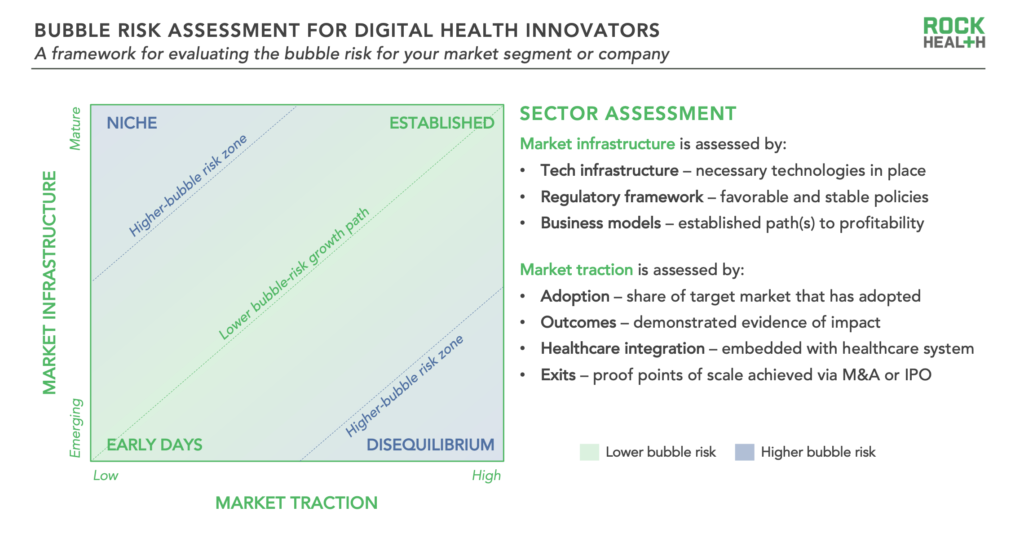

A framework for innovators to assess bubble risk

There are two key dimensions that innovation leaders should use to evaluate their bubble risk: market infrastructure and market traction. These dimensions are evaluated using several inputs:

Market infrastructure:

- Tech infrastructure: required technologies exist, are low cost/high quality, and/or are commonly available to end users

- Regulatory framework: policy environment is stable and conducive to sector growth

- Business models: established pathway(s) to profitability

Market traction:

- Adoption: significant share of target market that has adopted the innovation

- Outcomes: demonstrated impact on clinical, financial, and/or engagement measures

- Healthcare integration: degree of embeddedness within the traditional healthcare system

- Exits: proof points of scale achieved via M&A or IPO

The central idea of this framework is market segments and/or companies that advance their market traction in proportion to market infrastructure face relatively lower risk if they get caught in a bubbly environment—a situation where valuations exceed business fundamentals. This is because balance between market traction and market infrastructure makes it easier for companies to “grow into” any high valuations they may achieve during times of froth. Companies along the “lower bubble-risk growth path” axis can put their investors’ capital to work creating value along the growth path they are already on, rather than plugging gaps in their market infrastructure or overcoming challenges in market traction.

The four corners of this framework represent different zones of market dynamics; sectors and companies can fall anywhere along the axes. Each of these zones carries unique bubble risk and implications. Broadly, companies in lower-risk zones are more likely to weather the storm should a bubble deflate. To help innovators use this tool effectively, we illustrate a few examples below.

Early days

In this zone, market infrastructure is still being established and companies have achieved limited market adoption, however, these two dimensions are in relative proportion to one another. This seems to indicate that as long as the infrastructure continues to develop, enabling additional traction, there is a long runway of potential opportunity ahead.

Example early days sector analysis: Virtual reality (VR) therapeutics

The VR therapeutics sector (solutions that use VR technology to help patients manage or treat health conditions) is in the early days—its market infrastructure and market traction both have potential for significant growth. On the infrastructure front, the sector is primarily limited by the limited use of VR headsets (this may change if metaverse technology becomes widespread). Until the contours of VR technology access become more clear, we expect companies to continue testing new go to market and access models. This process of business model iteration is a natural part of a sector’s progression toward mature market infrastructure.

Market traction, relative to the potential opportunity of VR therapeutics, is also low. These solutions are not yet broadly embedded into the traditional healthcare system as a standard of care. Yet the opportunity is apparent, as companies have demonstrated positive clinical outcomes in pain management, anxiety, and fear of heights, to name a few. The sector also has not yet had any significant financial exits. Given the early stage of VR therapeutics’ market infrastructure and market traction, the sector has a promising potential growth path ahead.

Disequilibrium

In this zone, companies have achieved a relatively high level of market traction, but that traction outstrips the maturity of critical market infrastructure. Key technology, regulatory, or business model challenges need to be overcome to unlock significant further growth.

Example disequilibrium sector analysis: Consumer genetic testing

The consumer genetic testing sector (consumer-ordered tests that provide individuals with genetic information about ancestry and/or health risks based on their DNA) has been hampered by market infrastructure that has not kept pace with early market traction. While the price of genetic testing has come down, and companies have solved the logistics of at-home sample collection, there remain outstanding challenges to develop clear predictive markers of disease using these tests. Consumers’ concerns about data privacy may also dampen growth—just 13% of consumers in Rock Health’s latest Digital Health Consumer Adoption Survey were willing to share genetic data with a healthcare technology company. Future growth of this sector may hinge on the development of business models that generate more recurring revenue than the original one-off high cost testing model. The sector’s second generation business models—leveraging de-identified genetic data for drug discovery and using genetic tests to inform treatment decisions—are still being proven out.

Consumer genetic testing burst onto the scene over a decade ago, and quickly achieved significant market traction. To date, leading players have analyzed the genomes of millions of consumers. Market leaders have also exited via multiple pathways, including SPACs and acquisition by private equity (financial returns from such exits appear to be mixed). Unlocking significant future market traction in this sector, as with other disequilibrium sectors, will likely require shoring up of key components of market infrastructure (i.e., science and technology, regulatory, business models).

Niche

Companies have achieved limited market traction relative to their total addressable markets to date, despite mature market infrastructure. There are potential opportunities to tap into larger markets by pulling levers around adoption, outcomes, and/or integration with the traditional healthcare system

Example niche sector analysis: Personal health records

The personal health record sector (standalone solutions for patients to manage their health data, excluding EHR-based patient portals) appears to have market infrastructure in place to enable sector growth. Recent interoperability regulations that mandate consumer access to medical data via standard APIs make it easier for personal health record companies to aggregate and share data across multiple sources (although it also risks commoditizing these aspects of the value proposition). Additionally, two business models are showing promise. Apple’s Health app demonstrates how device manufacturers can embed health records as an integrated smartphone feature. Several startups are also working to prove out the life science channel whereby they support data collection for RWE and clinical trials.

On the other hand, the sector as a whole has not yet achieved broad market traction beyond early adopters. Personal health records have historically struggled with low consumer adoption—Microsoft and Google both shut down early products. On the exit front, there has been just one notable acquisition. Ciitizen, a startup that enables patients to share health data with researchers, was acquired by Invitae in 2021. Niche sectors such as personal health records have the potential for significant growth due to their mature market infrastructure, once they solve for a path to greater market traction.

Established

Companies have achieved a high degree of market traction amidst a mature market infrastructure. Continued growth in the sector hinges on strengthening competitive advantages and/or expanding into adjacent use cases while maintaining balance between market traction and infrastructure.

Example established sector analysis: Telemedicine

The telemedicine sector (solutions that enable real-time and asynchronous communication between patients and providers) achieved a mature market infrastructure over the past two years as the pandemic made virtual care a necessity. The technology infrastructure for telemedicine has existed for decades, and most consumers have access to broadband and the necessary devices (this does not mean the technology infrastructure adequately serves all consumers—distribution challenges continue to create inequities in virtual healthcare access). The regulatory environment shifted through emergency COVID-19 measures, and there is intention on the part of policymakers, startups, and patients alike to create lasting change on this front.

Telemedicine has also achieved a high degree of market traction. The sector experienced a rapid acceleration in adoption due to COVID-19, and while it has decreased since then, it is still significantly higher than pre-pandemic levels. While the “optimal” share of telemedicine visits as a portion of all patient encounters is still being worked out, it is clear that the use of virtual care solutions has been normalized for many patients and providers. In addition to adoption and healthcare integration, there have been a number of high-profile exits of leading telemedicine companies via IPO, merger, and acquisition. Telemedicine companies, like those in other established sectors, have an opportunity to build on past successes by fortifying their current market position and/or leveraging their mature market infrastructure to expand their target markets.

Question 3: What should you do about it?

Given the frothiness of the digital health investment sector, and the framework outlined above to assess individual sector or company bubble risks, what’s an innovator to do? This section outlines tactical operational and financial steps that startup and enterprise leaders can take to prepare their companies for the potential of tighter capital markets in the future.

Some recommendations are relevant to all innovators regardless of your company’s bubble risk. Forward-looking leaders should work to lengthen their cash runway and raise capital at valuations grounded in realistic evaluations of business fundamentals. The balancing act is to raise enough money in good times to weather a future storm, while avoiding unrealistically high valuations that could necessitate a down round if market conditions change.

The following recommendations are tailored to a company’s zone within the bubble risk assessment framework above:

Early days

Operationally, companies should work to put in place mission-critical market infrastructure pieces (e.g., internal technology infrastructure that will ease your path to scale, solving for sustainable business models). Identify potential partners that you could work with to acquire these components (e.g., middle children companies, digital health infrastructure companies).

Financially, it’s important to watch your funding and burn rate carefully. Make sure you have the runway needed to both invest in infrastructure and prove your market traction by the next stage of fundraising.

Disequilibrium

Operationally, companies should focus on addressing the shortfalls in technology infrastructure or regulatory strategy to enable continued growth. Identify companies with complementary assets that you could partner with in order to fortify your market infrastructure (e.g., regulatory expertise or a foothold in adjacent markets). Also consider alternative business models (e.g., new enterprise customer segments) that build upon the assets and capabilities you’ve developed to date.

Financially, be cautious of pursuing high valuations ahead of commensurate amounts of progress in market infrastructure, since growth is most contingent on fixing the mismatch between market traction and market infrastructure. Scenario plan for exit opportunities by identifying companies with complementary solutions in areas of lower bubble risk.

Niche

Operationally, consider expanding the types of customers you target in order to secure more stable (i.e., bubble-proof) revenue. Be open to the idea that a new customer type may present an even larger market opportunity for your company. Also consider alternative business models (e.g., value-based care models) that provide a compelling new value proposition to your current customer type.

Financially, double down on your existing investors. If you and your investors both believe in your technology and your vision, then work together to secure the cash runway you need. Consider finding a strategic investor with complementary assets that could assist a pivot into a more bubble-proof position (i.e., by advancing market traction).

Established

Operationally, companies should consider expanding into novel use cases for your technology. If your sector as a whole is established, you risk commoditization by simply continuing to do what you’ve been doing. Strategically invest in technology infrastructure that will continue to drive greater profitability (e.g., better reimbursement mechanisms, better cloud/AI infrastructure).

Financially, keep an eye out for complementary M&A or partnership opportunities in areas of digital health that are at higher bubble risk, which may be seeking partnerships or exit opportunities if tightened capital markets make their current trajectory less viable.

Boiling down the bubble question

To recap, digital health is not in an investment bubble, but it is frothy. Bubble-risk varies across sectors within digital health, and innovators can evaluate their own bubble risk by assessing their sector or company’s market infrastructure and market traction. Given this assessment, innovators should take concrete actions to prepare for tighter capital markets in the future.

We believe firmly in the fundamentals of digital health. There is still room for massive growth into the future until digital health becomes part of our healthcare system’s DNA.

Want to stay on top of all things digital health? Don’t forget to subscribe to the Rock Weekly.

Rock Health Consulting works with enterprise companies on digital health strategy and innovation. For more information, reach out to advisory@rockhealth.com.

Footnotes

1Unless otherwise stated, analyses were completed using data from the Rock Health Digital Health Venture Funding Database through the end of Q1 2022 (March 31, 2022)

2We make several educated assumptions to determine that valuations are likely going up based on trends in average deal size. The average digital health deal size was $39.5M in 2021, up 82% from 2018. If we assume that investors held constant their average ownership share in each deal compared with average ownership in prior periods, then it necessarily follows that average valuation has increased by the same proportion as average deal size.