2025 year-end digital health funding overview: A tale of two markets

In a turbulent year for healthcare and the broader market, digital health started to feel less like a tremor of innovation and more like bedrock infrastructure. Top players cemented themselves as core infrastructure, while investors bankrolled rapid AI-fueled growth. Annual funding for U.S. digital health startups reached $14.2B, a meaningful 35% increase over 2024’s $10.5B and the highest total we’ve seen since 2022. This wasn’t a return to the pandemic-era peak, but it was a growth year—thanks to AI exuberance, plus proof that startups are helping incumbents weather the storm and navigate coming change.

Under the headline of growth, a starker picture emerges: 2025 was a tale of haves and have-nots. On one side, AI-native upstarts attracted huge rounds at unprecedented speed, a handful of companies broke the IPO drought, and private equity made major moves, signaling real bets on an emerging “winner” class. On the other, 35% of venture rounds did not represent a step-up in round (i.e., “unlabeled”1 raises). Coupled with the elevated pace of M&A, which included a number of distressed exits, suggesting many companies are still grappling with valuation overhangs from prior cycles while operating in a more competitive market.

What’s driving this divide? Across 2025, we continued to see select players maintain outsized influence: mega funds,2 a well-capitalized unicorn class, and incumbents. These are the Goliaths we flagged last year, and their growing concentration of power is leading to a jockeying for influence at the top. New breakout companies are gaining significant market influence, sparking competition with incumbents wrestling to protect their role as healthcare’s backbone, plus the big foundation model companies looking for their next frontier. For all others—the “David” funds and startups still competing for their place—the pressure is on to find a plan to survive in an intensifying market. Success may increasingly rely on catching the attention of a Goliath (or a David on the rise) as a partner, acquirer, or investor.

Here’s where these dynamics stand at the end of 2025, the numbers behind them, and what we’re watching as we move into 2026.

2025 market overview

2025 saw $14.2B in venture funding for U.S. digital health startups, with Q4’s $4.2B across 129 deals marking the highest quarter total we’ve logged since Q2 2022. The headline numbers show a market that, like the broader VC market, has ticked up to a new normal around 36% above the pre-pandemic baseline (2019, adjusted for inflation).

But fewer companies are capturing this capital. Startups raised $3.7B more in 2025 than 2024, though deal count dropped by five percent (482 compared to 509 deals in 2024). Consequently, average deal size rose to $29.3M (up from $20.7M in 2024), and the median deal size budged from $10M to $12M. That average-to-median gap reflects the outsized influence of mega deals (raises over $100M) which accounted for 42% of all funding, the highest proportion since 2021 and nearly double last year’s share. Remove the top nine companies by 2025 dollars-raised and total funding falls below 2024.

The (funded) haves: Mega fund port cos, AI, and wellness

Across 2025, we identified two variables associated with funding “premiums,” i.e., the characteristics of the startups or deals correlated with larger check sizes. Both are relatively intuitive, but the data shows how much they matter: mega fund participation and an AI focus each drive meaningfully larger rounds. Plus, wellness-oriented companies got a boost—and it wasn’t just Oura raising the largest digital health funding round we’ve seen since we began tracking venture funding in 2011.

The “mega fund” moat

At the top of the market, 2025 saw 26 mega deals and 15 newly-minted unicorns (up from just six last year). The “Goliath” investors topped the term sheets, with Andreessen Horowitz (a16z), General Catalyst (GC), and Kleiner Perkins all participating in at least five mega deals each. The capital concentration we’ve seen since 2024 has only intensified.

With their large coffers, one might assume that mega funds have the largest imprint at the later stages, driving big dollars on the biggest deals. While true, the data also suggest that mega fund participation creates a durable premium on deal size across nearly all stages. We did a targeted analysis and found that when a16z and/or GC participated in a deal in 2025, the average deal size was larger than deals without their participation, and this delta grew as deal stages progressed. Take Series A, which saw an average deal size of $24.1M when a16z and/or GC was on the cap table, versus $18.9M without their participation, a difference of $5.3M. By Series D and beyond, the gap widens to near triple-digits at $93.6M.

Mega funds expect their portfolio companies to successfully use a larger amount of capital. The result is a bifurcating market. When mega funds do participate, they push up deal sizes and set benchmarks that ripple across the industry. For everyone else, this creates a widening gap: benchmark valuations are being influenced by a handful of outlier deals while the majority of startups compete for smaller checks from smaller funds, yet face the same sector-wide growth expectations.

The AI of it all

In addition to large funds driving larger deal size, AI is also pulling in a premium. Across 2025, 50% of deals were closed by “AI-enabled” companies,3 matching the broader VC market. AI-enabled digital health companies captured 54% of total funding (up from 37% last year) and commanded a roughly 19% premium on average deal size compared to companies not explicitly centering AI in their products and services.4 This was most pronounced at Series C, where startups commanded a 61% “AI premium.”

Is the premium warranted? On one hand, when looking cross-industry, AI companies’ revenue run rate is growing faster than ever. Healthcare specifically is embracing AI at an impressive pace: provider adoption is ballooning, sales cycles are shortening, and agentic AI is being adopted faster in healthcare than many other industries.

On the other hand, capabilities can quickly turn from differentiators to commodities. New AI players face encroachment from incumbents with existing client lock-in as well as foundation model players taking on healthcare opportunities. Further, many of the large LLM companies with deep pockets are willing to subsidize AI adoption to grab share (a clear parallel to Uber in its early days).

Then there’s the issue of timing. We saw funding velocity speed dramatically among a crop of AI-centric upstarts who compressed fundraising timelines from years into quarters. Abridge, Hippocratic AI, and OpenEvidence each closed back-to-back mega rounds within months in 2025—doubling, more than doubling or multiplying their valuations 6x across the year.

Racing through these rounds can make investors uneasy, as shorter gaps between raises leave less time to make durable progress. And AI companies are indeed burning more cash than their peers, yet investors continue to write big checks. That may reflect mounting pressure to “get in on” the AI race (at whatever cost) or confidence that AI itself can speed the path to product-market fit. Whether that bet pays off remains to be seen.

“We need to get back to thinking of investor money like carbs and customer money like protein. When customers pay you, they’re saying your service is worth more to them than their cash. Investor capital on the other hand, especially when it comes too fast, can make it hard for management teams to stay disciplined about how they spend. Raising money is exciting, but it can’t short-circuit the hard work of understanding why the world doesn’t yet have your innovation and how that innovation is actually going to change it.”

—Carl Byers, Partner, F-Prime

Wellness rises

Given the advent of AI-driven infrastructure bets, 2025 saw the most funding dollars flow to companies in the clinical and non-clinical workflow spaces, jointly capturing 39% of total funding. But beyond infrastructure, companies in the fitness and wellness space shot to the top of investors’ wishlists. Fitness and wellness startups raised $2.0B across 44 deals, vaulting from the eighth-most funded value proposition in 2024 to third in 2025. Oura’s $900M commanded nearly half that total, but even Oura aside, the category saw a 13% funding uptick, with companies like Function, Eight Sleep, and Nourish all taking in large raises.

And after years of D2C companies pivoting B2B or B2B2C amid rising customer acquisition costs, investors are dipping their toes in the water to back D2C again. 2025 saw a wave of activity around D2C lab testing, with Whoop, Oura, Function, Hims, and Superpower all launching D2C lab testing offerings. Several tailwinds are converging: wearables becoming more mainstream, younger consumers embracing preventive care and longevity, HSA/FSA growth expanding out-of-pocket purchasing power, and AI unlocking personalized interpretation. We’ll be watching whether growing competition pushes down prices on commoditized services like lab testing, plus if companies can build an ecosystem or drive benefits adoption to reinforce the growth of wellness as a whole.

The (unfunded) have-nots: Stuck in the murky middle

While the “premium” spikes of mega rounds and AI grabbed headlines, a harder story unfolded for some in the middle of the market. As we noted last quarter, many companies remain in precarious positions, even as capital flows elsewhere. A clear indication is the elevated number of unlabeled rounds (35% of deals in 2025)—down from the 44% peak in 2023, but still far above the single-digit levels of the pre-2021 market.

Another indication is the more than 600 companies that last raised in 2021 or 2022 that may still be in limbo—based on publicly available data, these companies are still operating but have not raised venture funding since their last round, nor have they exited. While some may have found a way toward sustainable profit (or quietly obtained funding), others represent a pandemic-era cohort that raised at peak valuations and have been weighed down by them since. And, the high-activity M&A market may foretell a possible path for these assets.

The Spectrum of Exits: Popping champagne or feeling the pain

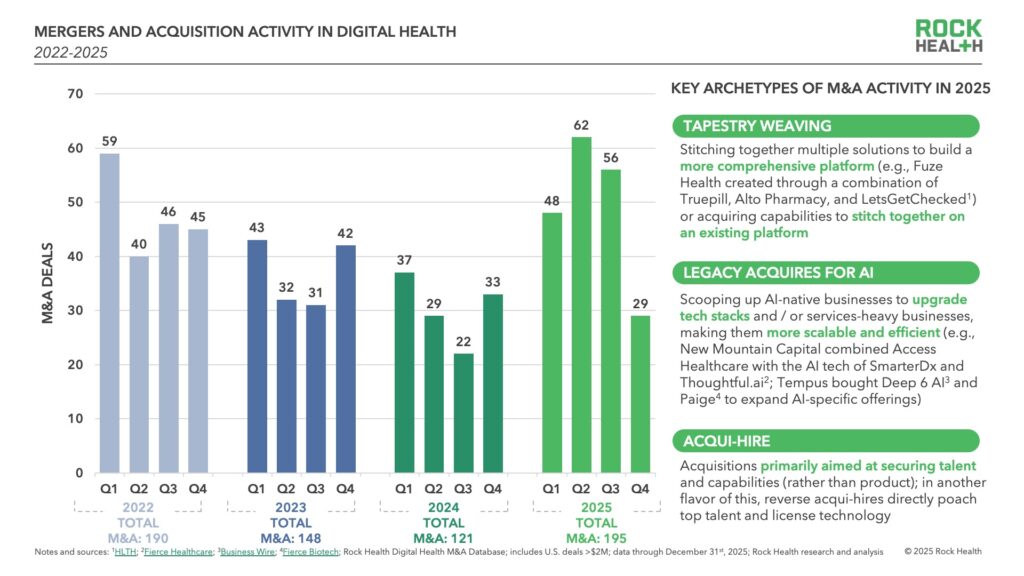

M&A: Reconfigurations and reckonings

M&A activity surged to 195 deals in 2025, up 61% from 2024—a notable acceleration after last year hit a five-year low. Digital health companies remained the most frequent acquirers, capturing 66% of deals (up from 53% in 2024 and the highest proportion since we started tracking in 2013). PE firms were the second most common acquirer of digital health companies with 10% of all deals—Pitchbook reported this as a nearly 600% increase in PE healthtech spend compared to 2024.

So why the surge? The upswing reflects the broader economy, as well as the confluence of a few trends in digital health.

Some M&A activity was driven by the aforementioned mega deals—growth-stage companies with fresh capital went on shopping sprees to pick up new capabilities, talent, and customers. Companies continue to follow the “tapestry weaving” playbook—acquiring startups for new features and capabilities to integrate with existing offerings. Consider Talkspace acquiring Wisdo Health to expand into peer support, or Fabric Health continuing to stitch together stalled businesses into a more comprehensive platform. M&A has also become a central strategy among AI infrastructure players. To compete with incumbent capabilities and meet buyer needs, many large startups (e.g., Commure, Abridge, Innovaccer) are relying on inorganic growth to bulk up teams and roll out new use cases.

M&A-powered growth holds the promise of creating companies that deliver greater reliability, scale, and an integrated experience to customers. But M&A wasn’t a win for everyone this year—for some, it was a survival strategy. Thirty Madison’s valuation reportedly fell from $1B to $500M as it sold to GLP-1 provider RemedyMeds, Upfront Health sold for $8M less than it raised, and SteadyMD sold for $25M after raising nearly $40M. Consolidation of this kind may not yield desired outcomes for acquirees and their investors, but acquirers are certainly benefiting from lower prices on assets that help them leapfrog on growth and infrastructure. Of course, the devil is in the details in terms of to whom and how capital is returned—and while there have been some reckonings, the appetite to piece together winning companies is high.

New Mountain Capital (NMC) in particular has put a couple different playbooks to work across 2025. Earlier this year, they rolled up legacy healthcare services with AI-native capabilities via Smarter Technologies and Machinify deals—betting that legacy reach and relationships could be optimized by AI margins and efficiency. Now, they’re weaving the largest “M&A tapestry” in digital health thus far: Matt Holt, NMC’s former managing director and president of private equity, is reportedly leaving to combine five NMC portfolio companies into a $30B holding company called Thoreau. It’s an ambitious bet, and with competition to own the AI infrastructure backbone of healthcare reaching a fever pitch, we expect M&A will continue to be a core strategy in the fight.

“Data rights and IP ownership are among the first issues we examine in AI-driven transactions. Buyers want confidence that companies actually have the rights to the data and models they plan to build future products on.”

—Heather Deixler, Partner, Latham & Watkins LLP

2025’s graduating class: IPOs make a comeback

After just two public exits in the prior three years, five digital health companies broke through in 2025—Hinge Health, Omada Health, Heartflow, Carlsmed, and Profusa. Two of the five were trading above their IPO prices (Hinge and Heartflow) as of market close in 2025. And after an IPO drought and a string of take–privates, the public markets rewarded validated digital health businesses moving into high-growth use cases and leveraging AI for turbocharged personalization and efficiency.

Celebrations are well-deserved, but reflect a market that’s recalibrated from the pandemic peak. Hinge debuted at $3B—less than half its $6.2B private valuation in 2021. Heartflow raised $0.5B less than it would have in a failed 2021 SPAC attempt. Regardless, the exits do matter for the sector. They return capital to LPs, unfreeze the investment cycle, create validated comps for future fundraises and exits, and most importantly, offer validation of the core theses of digital health—that technology applied to healthcare can create desired outcomes and durable businesses.

Looking ahead, there’s clearly pent-up demand for additional public exits, but uncertainty clouds the path forward: the federal government shutdown built an SEC backlog, and companies primed for an exit will need to tread choppy waters (e.g., bracing for coverage losses from the One Big Beautiful Bill Act). We’ll be watching to see if those potentially waiting in the wings like Aledade, Included Health, Maven Clinic, Virta, or Zelis can thread the needle in 2026.

A look ahead at shifting policy tides

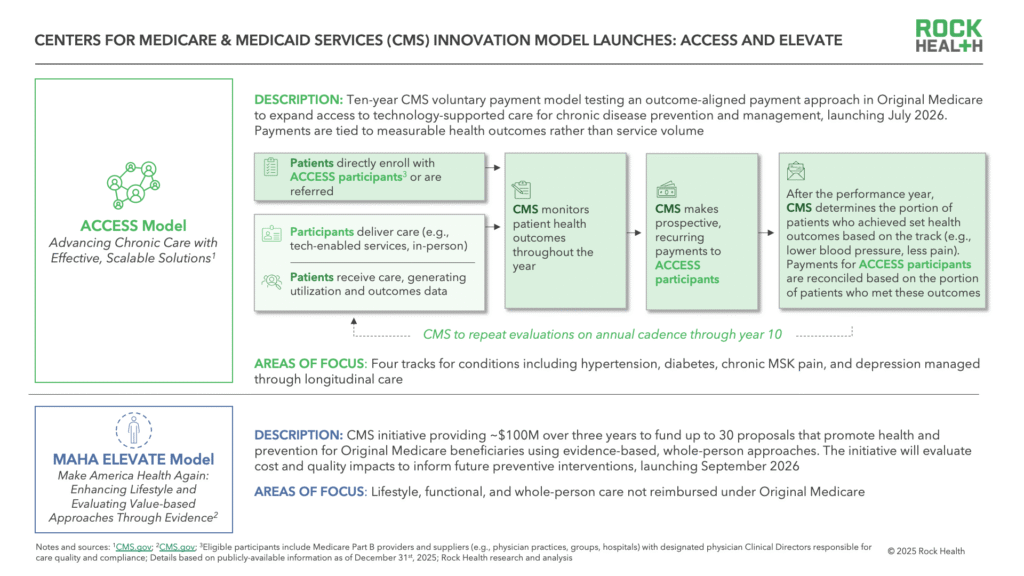

We expect the 2026 healthcare innovation landscape to be shaped by policy as the Trump administration moves from intention to action. 2026 will see the launch of CMMI’s ACCESS Model in July. It’s the first meaningful Medicare value-based pathway for digital health—a 10-year program offering consistent payments for treating chronic conditions like diabetes, hypertension, and depression. Critically, it addresses common barriers for digital health to work with Medicare: it pays for outcomes (offering flexibility on which technology is used), offers direct patient enrollment, and gives the option to waive patient copays. The opportunity is not guaranteed (payment levels aren’t set yet and few digital health companies are enrolled as Part B providers), but for mature startups that can navigate it, or new entrants building for it, ACCESS could be a real unlock. The ELEVATE Model could similarly open doors for functional medicine and longevity players by creating evidence pathways for services that aren’t currently reimbursed. And TrumpRx, reported launching in January 2026, could benefit companies enabling pharma’s DTP plays but also, within the arena of GLP-1s, heighten competition for those betting on compounding.

On the regulation front, ONC recently nixed Biden-era AI transparency requirements and sought ideas to promote AI use in clinical care, while the FDA explored the idea of directly contracting with VC firms so portfolio companies can compete for federal contracts, with the intention of disrupting procurement processes that favor established players.

The administration is clearly eager to remove barriers (especially around AI) and open doors for startups to tap federal dollars. But deregulation doesn’t necessarily mean equal access. Some mega funds, for example, are positioning aggressively—standing up Washington-focused teams and institutes to build relationships with agencies. Smaller funds may find themselves on the outside looking in, and we could see policy access become another axis of advantage for the mega funds’ port cos: not just more capital, but earlier information and priority access.

Acceleration and accountability

Competition is heating up. Technology adoption is accelerating (in healthcare!). And regulators are signaling a desire to let innovation speed ahead. The pressure on entrepreneurs to pull ahead is intensifying, and the jockeying for capital and market share will only grow more fierce. In moments like this, hype (and funding) can outpace impact. As we head into 2026, our hope is that durable advantage comes not from inflated promises or bloated cap tables—but from ethical growth, safety, and patient outcomes. If that holds, market leaders will be crowned, but patients will ultimately emerge as the real winners.

Tap into insights and strategic guidance for enterprise companies with Rock Health Advisory.

Get in touch with the venture team at Rock Health Capital.

Join us in advancing ecosystem change at RockHealth.org.

And last but not least, stay plugged into the Rock Health community and all things digital health with the Rock Weekly.

Footnotes

- “Unlabeled round” is a term we first used in our H1 2023 analysis to refer to capital raises without associated round labels (e.g., Series A, Series B).

- Venture capital firms with at least $500M to deploy are often referred to as “mega funds.”

- Rock Health defines AI-enabled digital health startups as startups using artificial intelligence, machine learning, and/or deep learning as a core part of their product or offering.

- All startups are likely using AI in some capacity (e.g., internal, operational). Rock Health defines non AI-enabled startups as those in which AI is not (publicly) a core part of products or offerings.