Digital health funding 2016 midyear review

After years of record-breaking venture funding in the digital health sector, we wondered if 2016 would continue on this torrid pace. The numbers are in: we ended the first half of 2016 with slightly over $2B in total venture funding–on track with the levels of both 2014 and 2015. While this number didn’t eclipse either of the previous years’ numbers, it’s important to keep context: in a year when everyone expected funding to decline, digital health has been as steady as ever and accounted for a healthy 8% of total venture funding. The first half of 2016 came out on top in one aspect however, as a record-breaking 151 companies raised more than $2M.

With so many companies raising money, the next question for investors has always focused on the exit opportunities. Comparatively, 2016 has been much slower in the public markets than previous years; NantHealth had the lone IPO, creating almost $1.5B in market capitalization. Though digital health is still waiting for the public market to heat up, M&A continues to be a viable exit route. Disclosed dollars from acquisitions are almost twice 2015 levels ($10.4B vs $6B) and there have already been 87 recorded deals in 2016.

We’re excited to see how the rest of the year plays out, and expect more M&A activity, a few IPOs, and many more deals from (more) new investors. Stay tuned to find out if this year will become the new normal or if we’re still waiting for the proverbial shoe to drop.

Dollars and deals

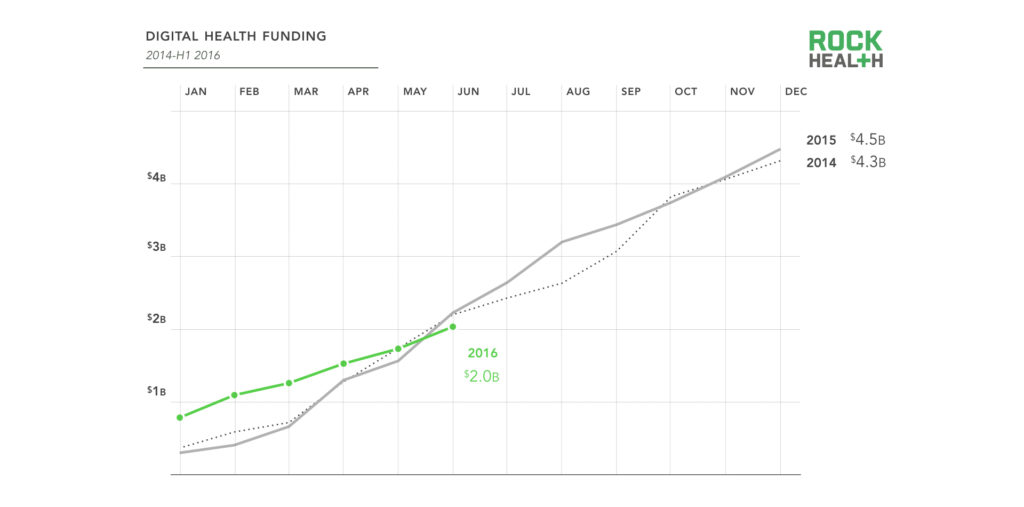

The pace of digital health funding in the first half of 2016 echoed the record-breaking years of 2014 and 2015, with funding just eclipsing $2B.

Source: Rock Health Funding Database

Note: Only includes U.S. deals >$2M; data through June 30, 2016

Following two record years of digital health funding, 2016 has started with a more moderate pace. Overall, funding is about $191M below 2015’s first half record.

The first quarter had a number of large rounds (average deal size was $15.4M), but the second quarter leveled off slightly, resulting in a $13.3M average deal size for 2016. Growth on a trailing twelve month (TTM) basis has flattened out (-0.67%) after experiencing constant upward movement for the last eleven quarters.

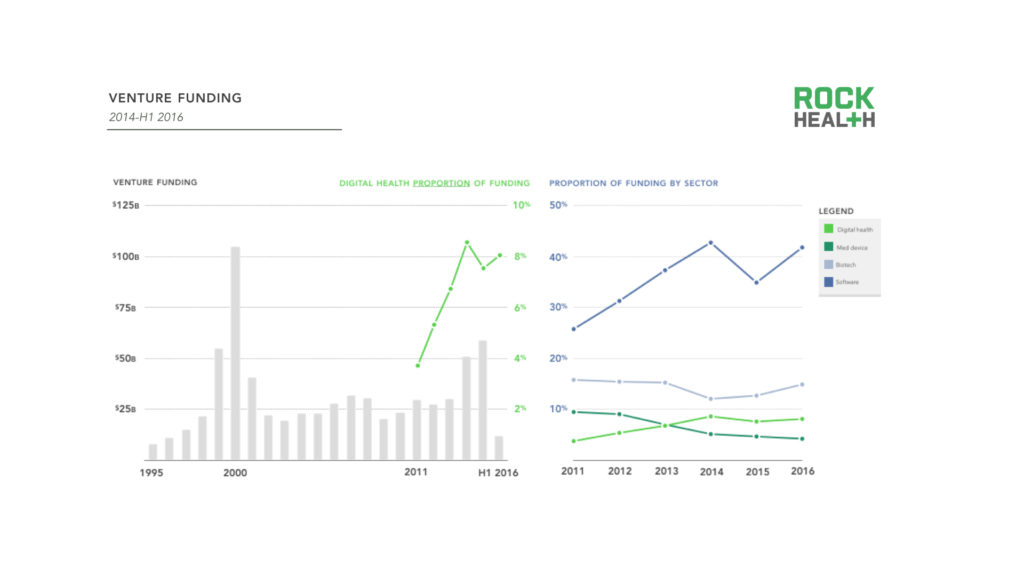

Digital health investment remains within a healthy range proportionate to the rest of the funding landscape and is at its highest level since 2014.

Source: PwC MoneyTree (latest available is through Q1 only); digital health data based on Rock Health data

Note: Digital health only includes U.S. deals >$2M

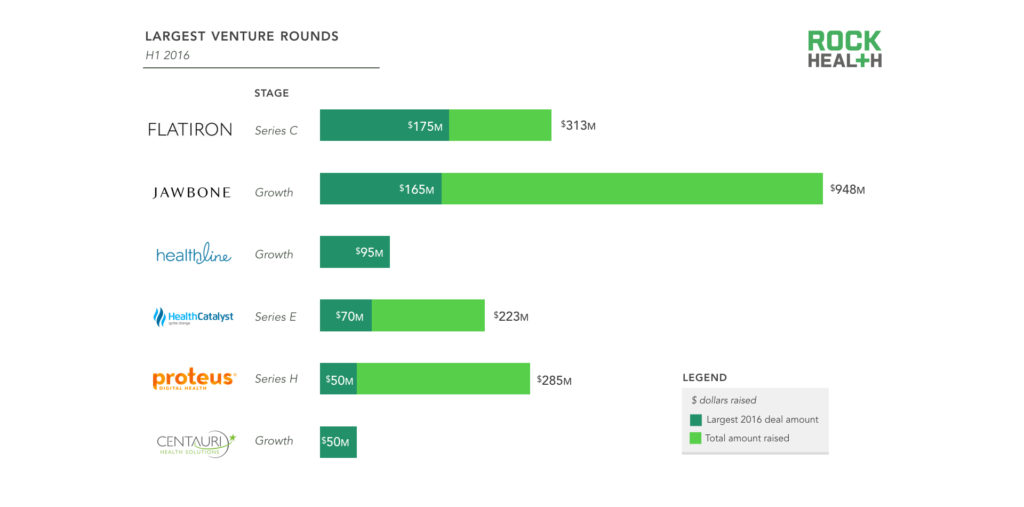

The six largest rounds of the year represent just under a third of all funding in 2016.

Source: Rock Health Funding Database

Note: Only includes U.S. deals >$2M; data through June 30, 2016

A diverse set of companies made up the largest venture deals of the year. Jawbone, a mainstay in these rankings, closed the second-largest round of the year, bringing its total amount raised to just under $1B. The company shuttered other business lines to focus on health products as investors continued to inquire about further growth.

Healthline Media (a spinoff from Healthline Networks) and Centauri Health Solutions (founded 2014) took on their first round of outside capital from growth equity investors Summit Partners and Silversmith Capital Partners, respectively. This isn’t the first time we’ve seen this happen–in 2015, Virgin Pulse raised their first round of outside capital after being funded by the Virgin Group for over a decade.

Roche led Flatiron’s investment, which was the largest deal of the year. Interestingly, this Series C deal (the biggest Series C in the history of digital health), was funded by the Fortune 500 company directly, rather than through their corporate venture fund. Late-stage deals for Health Catalyst (Series E) and Proteus (Series H) rounded out the top six.

Other high profile deals this year include Quartet Health (which raised a $40M Series B from Google Ventures and Oak HC/FT Partners), Pathway Genomics ($40M Series E from IBM), and Livongo ($49.5M Series C led by Merck Global Health Innovation Fund).

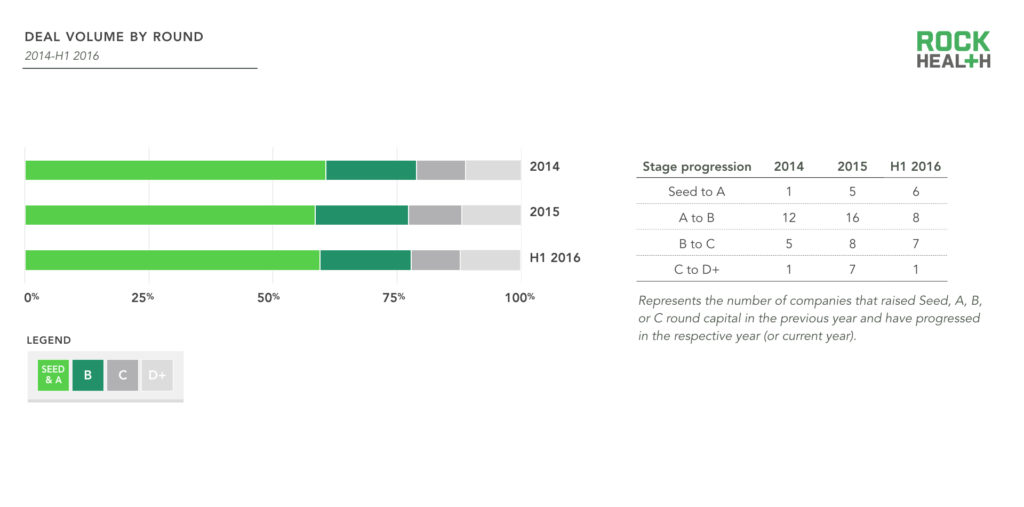

Seed and Series A stage deals represent most of deal volume; later stage deals (Series C and beyond) account for slightly more than one-fifth of all deals

Source: Rock Health Funding Database

Note: Only includes U.S. deals >$2M; stage progression excludes bridge rounds; data through June 30, 2016

As was the case during the past two years, Seed and Series A deals continued to account for the majority of deals in the first half of 2016. Series C and later stage deals are slightly lower, accounting for just more than 22% of all deals.

In the previous three-year period, we have tracked “on-time” and progressive raises to determine if companies are growing at an appropriate rate. In 2015, 24 out of 221 companies (11%) that closed a deal raised subsequent capital in 2016. LeanTaas and Greatist were the only two companies that closed a Seed round in 2015 and subsequently raised a Series A in 2016; Stride Health, Pager, Joyable, and Lyra Health raised both Seed and Series A Capital within 2015. Only three companies announced round-to-round progress in later stage deals–Gly Sens (Series C to Series D), and Modernizing Medicine and Health Catalyst (Series D to Series E).

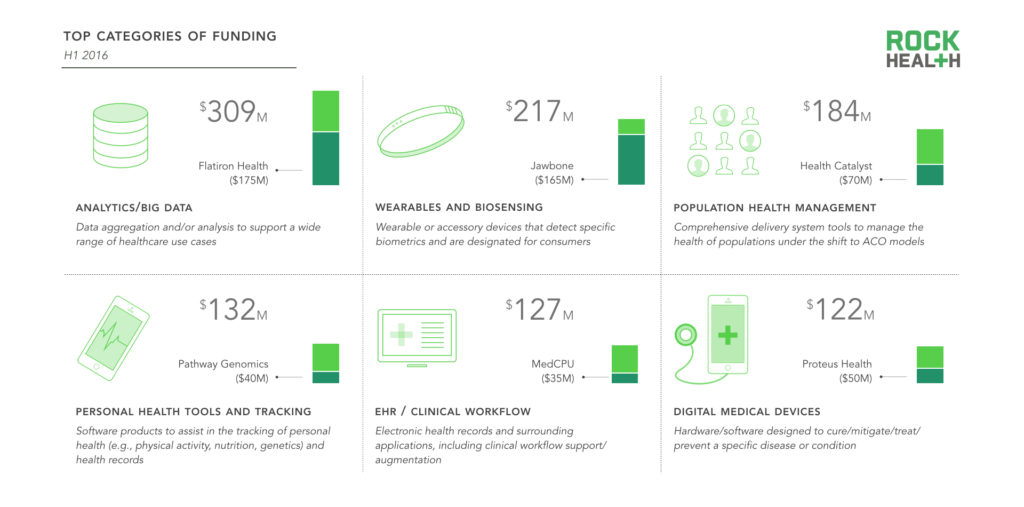

These top six categories accounted for more than 50% of all digital health funding in 2016; only wearables and biosensing and personal health tools were ranked in 2015’s top six.

Source: Rock Health Funding Database

Note: Only includes U.S. deals >$2M; data through June 30, 2016

Where did all of this money go? Analytics and big data finished the first half with over $300M in funding and over 118% year-over-year (YoY) growth. This category has been a buzzword in technology for some time, but we continue to be excited about the impact of large-scale data science in healthcare. Chronic diseases like cardiovascular disease and diabetes result in over half a trillion in healthcare costs per year. Both of these disease states are heavily influenced by individual behavior (versus solely genetics) and can be impacted by using large sets of data for measurement, reminders, and personalization of care. Near universal smartphone adoption and the surge of affordable sensors will promote further success in this arena.

Consumerization also continues to receive consistent investor attention–two of the top three digital health “unicorns” (23andMe, ZocDoc) are consumer-focused companies. Among these top six, we consider both wearables and biosensing and personal health tools and tracking consumer-focused categories. While healthcare consumer engagement didn’t make the top six for the first time ever, it did experience significant YoY growth (127%). We’ve talked about why the focus on consumers is important, but it’s imperative to restate some of the facts. Over one-third of adults are now covered under high deductible health plans (HDHPs) and are required to spend out of pocket for a majority of their healthcare services. This shift in coverage also transfers more of the burden to the consumer, making consumerization an area still ripe for disruption by digital health startups. Tools that focus on transparency in price, quality, or experience or that allow consumers to guide their own healthcare journey (choosing their own treatment or provider) will continue to grow in popularity.

Investors

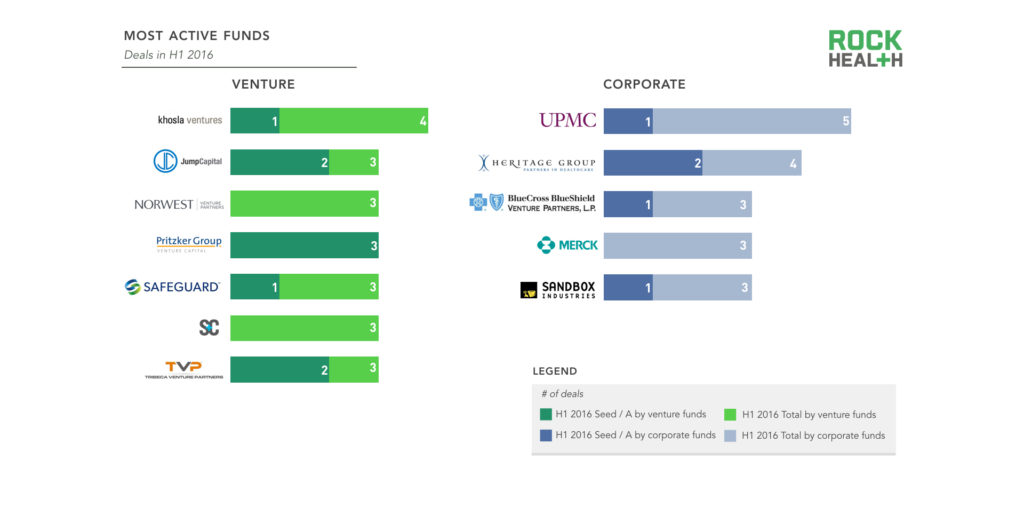

New names jumped to the top of the active investor ranks as digital health continues to be supported by a variety of funds.

Source: Rock Health Funding Database

Note: Only includes U.S. deals >$2M; data through June 30, 2016

2016 saw new (and old) names jump to the top of the list of most active investors, with corporate investors outpacing traditional venture funds in number of deals. New names on the list of most active investors include Jump Capital, Pritzker Group, Safeguard Scientifics, and Tribeca Venture Partners. Khosla Ventures also returned after a two-year hiatus, backing AVA, CrossChx, Lumiata, and Neurotrack.

New investors UPMC and Heritage Group joined the ranks of top corporate funds in 2016, while stalwarts like GE Ventures and Google Ventures were surprisingly inactive.

We tracked 248 distinct investors in 2016, with nearly 40% of those being “first timers” (doing their first and only digital health deal since 2011). Welcome!

Geographies

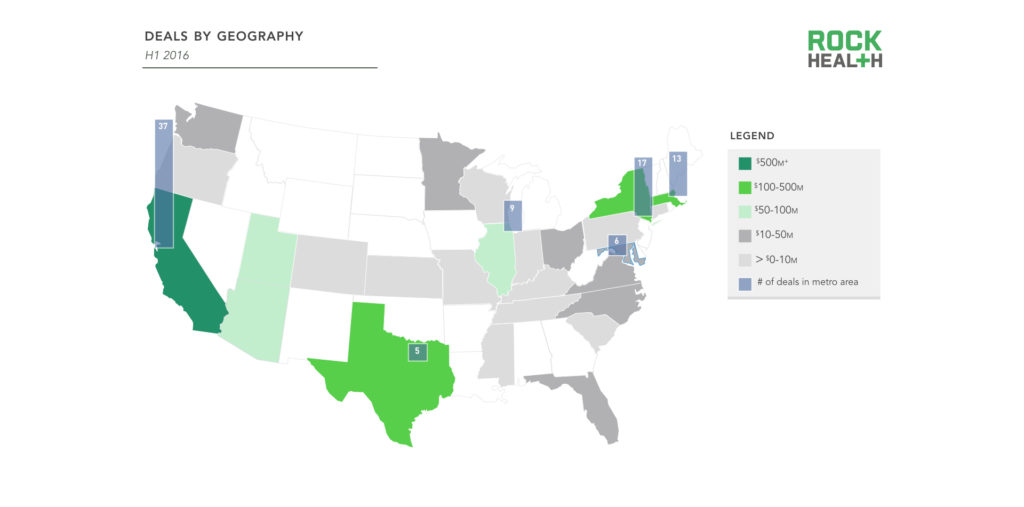

Digital health companies headquartered in California continue to garner the majority of funding, with Bay Area-based companies receiving over 36% of all dollars raised.

Source: Rock Health Funding Database

Note: Only includes U.S. deals >$2M; data through June 30, 2016

Digital health investments reached companies in 27 states (compared to 23 and 27 states at the midyear mark in 2015 and 2014 respectively), with California staying in the lead with over 41% of total dollars. For the first time, Texas joined New York and Massachusetts in the second tier of funding ($100-$500M).

As expected, the Bay Area continues to be the digital health hub, receiving nearly as many deals (37) as the next three metro areas combined (39). Funding continues to spread to other hubs, including Chicago, Houston, Phoenix, Salt Lake City, and San Diego; each area brought in more than $45M in total funding.

Exits and public markets

Eighty-seven M&A deals were closed by the 2016 midpoint, slightly below 2015’s midyear mark, with total disclosed dollars eclipsing $10B.

Source: Rock Health tracking and analysis based on news reports

Note: M&A transactions totals and lists are not meant to be comprehensive; deals through June 30, 2016

Halfway through 2016, we have already tracked 87 digital health deals, ranking slightly below the midyear mark for 2014 and 2015 (92 and 96 respectively). Other digital health companies continue to be the most acquisitive, acquiring more than half of companies we tracked.

The most notable transactions of 2016 include McKesson’s purchase of Change Healthcare for $3B, IBM’s purchase of Truven Analytics for $2.6B, and Nordic Capital’s purchase of eResearch Technology for $1.8B.

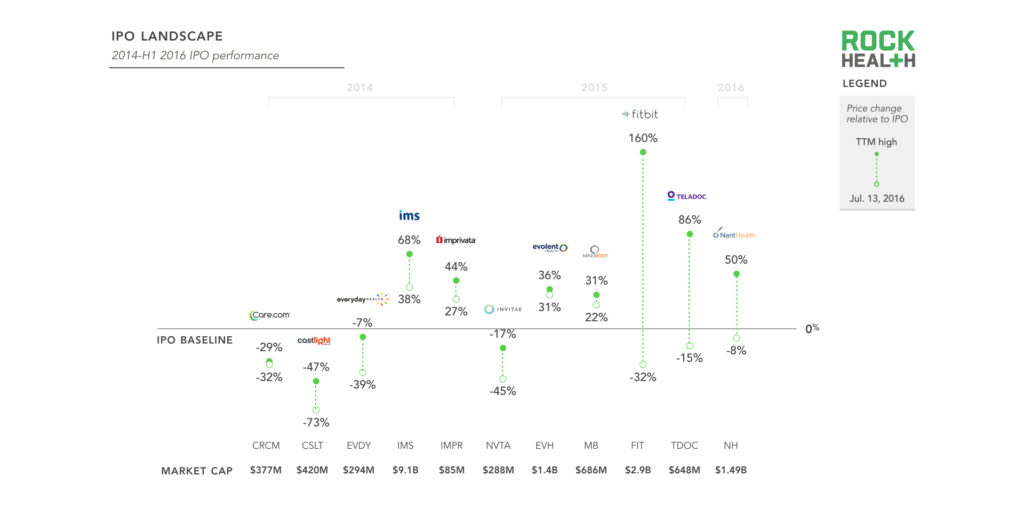

IPO performance hasn’t kept pace with funding: only one digital health company went public in 2016 and nearly all are trading below their initial share price.

Source: Public market performance from NASDAQ and Google Finance as of market close on July 13, 2016

In 2014 and 2015, ten venture-backed digital health companies went public. Thus far in 2016, only one company has filed for an IPO.

NantHealth’s market cap of $1.5B makes it one of four companies within the last three years to maintain that mark post-offering. Four companies (IMS Health, Evolent Health, Imprivata, MindBody Media) are currently trading above their IPO price.

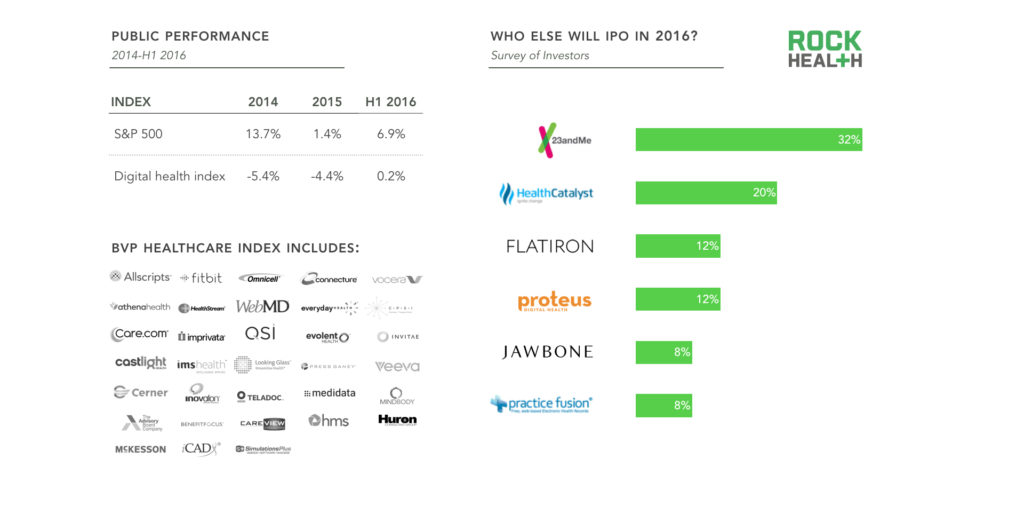

Despite improved performance from previous years, publicly traded digital health companies are still underperforming the broader S&P 500 public market index.

2014 and 2015 represented by The Digital Health Public Company Index by Rock Health and is available from: https://www.motifinvesting.com/motifs/the-digital-health-index-by-roc-O7xghiOF#/ . 2016 data represented by BVP Healthcare Index (as of market close on July 13, 2016); Available from: https://www.bvp.com/strategy/healthcare/index Investor survey was conducted on May 6, 2016 at the Fenwick Investor Summit (n = 29)

Bessemer Venture Partners’ digital health public company index is comprised of 33 companies, totaling over $115B in aggregate value (McKesson, Cerner, IMS, and Athena hold almost 65% of the value). This index is the best gauge of how digital health companies are performing against the broader public markets. With a recent market upswing, the digital health index has improved, but still lags behind the broader S&P index.

A recent survey of digital health investors revealed varying answers to the question: who will be next to IPO? The companies on the list are pursuing a diverse set of sectors (from personalized genomics and healthcare data warehousing, to a cancer analytics platform and ingestible biomedical sensors) with large market opportunities, suggesting a robust IPO pipeline for the rest of 2016 and beyond.

Summary of findings

Funding and deal volume: Venture funding for digital health companies in the first half of 2016 reached $2.0B, closely mimicking previous years. TTM (Q3 2015-Q2 2016) growth in funding has flattened out to -0.67% compared to Q3 2014-Q2 2015. 153 deals, across 151 companies, closed with an average deal size of $13.3M.

Major themes: The top six themes of the year that received 54% of all funding included: analytics and big data, wearables and biosensing, population health management, personal health tools and tracking, EHR and clinical workflow, and digital medical devices. Only wearables and biosensing and personal health tools and tracking remained from 2015’s top six categories. Analytics and big data and digital medical devices returned after a one-year hiatus.

Most active funds: Two hundred forty-eight distinct investors funded digital health companies in 2016, including 95 investors that backed a digital health company for the first time since we began tracking in 2011. New investors jumped to the top of the active list in 2016–six out of seven institutional investors that funded more than three deals were new to the rankings and one corporate investor (UPMC) ranked as the most active with five total deals (two of which were early-stage).

Exit activity: M&A activity dominated the exit landscape in 2016. There were 87 tracked M&A transactions, slightly below the 95 and 92 deals done in 2014 and 2015 respectively. Disclosed deal value is notably higher than last year ($10.4B in H1 2016 vs $6B in 2015). Digital health companies continued to be the most active acquirers of other digital health companies, with technology company acquirers coming in second. The public market appetite for digital health remains in question as there was a single IPO (NantHealth) in the first half of 2016 (compared to 5 each in the first half of 2014 and 2015).

Methodologies

What is digital health?

Rock Health defines digital health as the intersection of healthcare and technology. This means that the venture funding tracked only includes technology-enabled health-related companies, whether they focus on the administration of healthcare, the delivery of healthcare, or the process of bringing breakthrough new healthcare products to market (both R&D and commercialization).

Healthcare companies that aren’t digital. Health insurance companies, such as Oscar, or healthcare providers, such as One Medical, are pure services companies (that employ technology, certainly, as does every company). This is in direct contrast to a technology-enabled services business such as telemedicine, that simply could not exist without digital. Molecular diagnostic companies, such as Guardant Health, that perform testing and render a definitive diagnosis to physicians are also excluded. Similar to biopharma companies, molecular diagnostic companies are significantly more capital intensive than software-based companies and would skew funding.

Technology companies that aren’t healthcare. Companies diversified across industries are not included. Software companies focused across human resources (and not solely health benefits), such as Zenefits, are not included.

How we track digital health funding

Rock Health funding data only includes disclosed US deals over $2M. Deals under $2M would be impossible to track comprehensively since companies often do not file their small seed rounds with the SEC or disclose to press. We also believe that deals under $2M generate noise in key statistics, including deal count and average deal size. Disclosed deals under $2M represent less than 5% of the total we report, giving us confidence in our overall figures.

In prior years, we have attempted to include international companies that were funded by U.S. investors, monitoring the portfolios of hundreds of VCs. In reviewing this data, we have concluded that it is challenging to track all international deals and beginning with this 2014 year end report, we are no longer tracking or reporting any international deals. All numbers in this report are for U.S.-based companies only.

Funding tracked includes debt, venture rounds, and growth equity but excludes lines of credit (working capital) and cash/equity associated with merger or acquisition activities.

Deals data is gathered based on publicly available resources (press releases, news outlets, SEC filings, etc.) and supplemented with CapIQ’s venture data.