Healthcare’s middle children: Potential disruptors flying under the radar

There has been a lot of talk about big tech and big box retail entering healthcare. Many incumbents are shaking in their boots at the prospect that is now becoming a reality. But a major, overlooked entrant into healthcare are the middle children: large retail, fitness, and tech companies that have not been labeled “big,” but are still a force to be reckoned with.

We call these players “middle children” because they are in between their big tech & retail older siblings and startup younger siblings. Perhaps they will also share middle children qualities that will set them up for success.

The handful of anointed “big” players include Alphabet, Amazon, Apple, Facebook, Microsoft, and Walmart. Most of these companies have market capitalizations above $1T1. The “big” players have already begun to wade into the healthcare waters (with a few notable stumbles and reorgs along the way). They are seen as formidable potential entrants in healthcare because they have industry leading capabilities (e.g., technology, logistics, consumer experience), cash war chests that they can use in pursuit of new growth opportunities, and what we’ll call “innovative DNA”—histories of risk taking, entering new markets, and visionary leadership.

Intense focus on the big players’ potential impact on healthcare risks narrowing the industry’s aperture on the competitive landscape in healthcare’s new world order. There are potentially dozens of large (but not BIG) would-be entrants in the retail, fitness, and tech sectors who are (or should be) eyeing opportunities in healthcare.

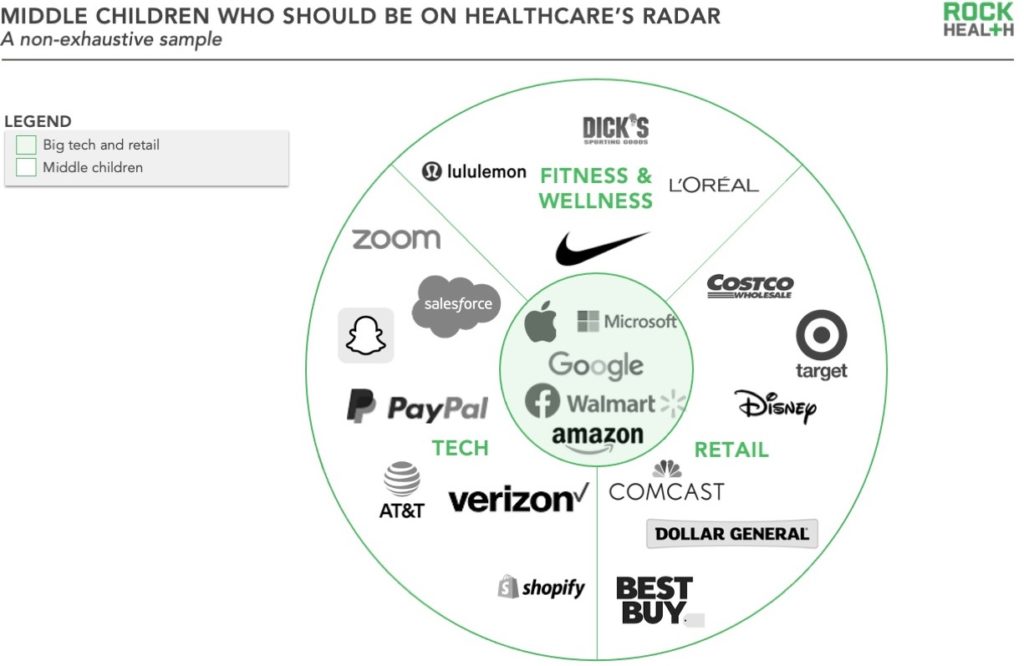

Who are the middle children?

We are defining middle children as tech, retail, and fitness companies with market capitalizations between $10B and $350B. They are big enough to make an impact at scale, but not so big as to be under the same scrutiny as “big” players. Middle children tend to be consumer-focused, and they have assets and capabilities that could be used to make a play into healthcare. We’ve seen examples of these middle children making plays in recent years, from Best Buy’s acquisition of Great Call to Lululemon’s acquisition of Mirror.

Middle children come in all shapes and sizes. At their biggest, they flirt with the “big” label. Giants such as Salesforce, Nike, and Disney all have multi-hundred billion market caps—any healthcare moves by such large players are on the industry’s radar. Large middle children such as these have the reach, deep pockets, and capabilities to go after big healthcare opportunities at scale.

Smaller middle children are the ones that typically fly under the radar. Companies with market capitalizations between $10B and $100B such as Garmin and Airbnb can bring their own well-suited capabilities (e.g., national footprints, strong consumer bases) to solve pressing healthcare challenges. Such companies can go after relatively smaller opportunities (compared to larger players) within the $3.5T healthcare industry and still achieve meaningful growth.

There are dozens of middle children that could take differentiated strategies in healthcare. In aggregate, the middle children represent a massive potential driver of change.

A huge set of competitors and potential partners

The middle children are motivated to enter healthcare by the same drivers that motivate their big competitors. The market opportunity is huge ($3.5T); healthcare is undergoing digital transformation; and the growing potential for healthcare consumerism. Yet the middle children have several distinct advantages as they enter healthcare:

- Smaller wins are big enough: for Apple or Walmart to make it worth entering a new market they need to do something big to make it worthy of their attention. These smaller players can capture a smaller market share and still benefit from a big growth opportunity.

- More irons in the fire: there are more middle children than big tech players—they can make more bets across healthcare and compete, which will spur innovation and catalyze the ecosystem.

- Consumer loyalty, minus the baggage: middle children already have sizable, loyal customer bases. This is something that D2C digital health entrants are spending vast sums of venture dollars to win (e.g., Hims, Roman, and Nurx). Middle children may be able to arbitrage their consumer bases into healthcare without setting off as many tripwires as the big tech and big retail companies.

- Assets often lacking in healthcare: middle children have a wide range of assets that they can bring to healthcare, such as logistics expertise, data analytics, large geographic footprints, or consumer experience.

- Innovative DNA: like their big tech and retail siblings, many of these companies have histories of risk taking, entering new markets, and visionary leadership which will make them formidable challengers to today’s status quo in healthcare.

Some middle children like Best Buy have been on the digital health ecosystem’s radar for a while now, while others like Dollar General have recently piqued interest by hinting at future healthcare entry. Looking ahead, we see opportunities for middle children across several types of healthcare plays:

Become a new front door

Middle children can turn existing consumer touchpoints into care delivery or triage opportunities. Today we see companies like Kroger pursuing this strategy by offering basic medical exams at health kiosks located in its supermarkets through a partnership with Higi.

Hypothetical future front door plays:

- Sephora could offer skin cancer screenings by embedding diagnostic imaging technology within its Virtual Artist app

- Activision Blizzard could passively monitor for behavioral health conditions among children while they play video games through a partnership with Akili Interactive

Develop new products or services for healthcare

Middle children can build new offerings to sell into the healthcare market. One recent example of this approach is Bose’s recent launch2 of an FDA-cleared hearing aid.

Hypothetical future new product or service plays:

- Disney could use its existing AR/VR capabilities and deep expertise in creating experiences for children to build a VR pediatrics anxiety management solution, potentially for use before medical procedures

- Paypal could create an HSA offering to make it easy for consumers to manage their healthcare spending

Enhance consumer products and experiences with health and wellness tracking

Middle children can incorporate wearables, lab tests, and patient-entered health and wellness data to enhance current consumer experiences and create new ones. Nike was an early mover in this area with its Nike + iPod Sport Kit, launched in partnership with Apple in 2006. Nike discontinued its last health tracking offering in 2014 but continues to provide digital fitness offerings through its Training Club app with workouts, nutrition tips, and wellness guidance.

Hypothetical future health and wellness tracking plays:

- Ford could monitor biometrics such as heart rate by embedding sensors into the steering wheel and play soothing music for drivers who are at risk for road rage

- Tiktok could offer exercise dance videos

Power consumer health personalization

Middle children can leverage data they already collect to deliver tailored consumer insights. Personalization plays might include:

- Hello Fresh could offer insights on your health and recommend other food products

- Uber could recommend that you stop your ride 10 minutes from your destination to get steps in, which earns you Uber rewards

How will this play out?

Middle children eyeing opportunities in healthcare will do well to recognize the challenges that lie in their road ahead. Key hurdles we’ve seen retail, fitness, and tech entrants in healthcare face include:

- Building a sustainable business model: new entrants to healthcare may stumble in identifying stakeholders that are willing to pay for their offerings—end users are often not the customer

- Understanding the rapidly changing ecosystem: not only is healthcare complex, it’s also evolving—entrants need to understand who their competition is today and in the future

- Navigate regulatory complexity: healthcare’s web of regulations can be a maze for new entrants; middle children need to be strategic and forward looking in their regulatory approach

Middle children that successfully overcome these challenges will displace traditional incumbents, and even digital health startups, in healthcare’s current world order. What might this mean for different stakeholders in the healthcare ecosystem?

- Consumers stand to benefit from greater personalization of healthcare products and services. These companies understand who their consumers are and how to fulfill their needs. At the same time, consumers may experience care and health data fragmentation.

- Enterprise healthcare organizations will face competition from a new front, in addition to already-on-radar competitive threats posed by big tech, big retail, and digital health startups. Enterprises must continue to be agile enough to recognize and respond to the emerging fronts for competition; in some cases, enterprises will form creative partnerships with middle children.

- Digital health startups must navigate the rapidly shifting lines of competition to identify the threats and opportunities posed by middle children. Some of these non-healthcare entrants will go after the same market share that digital health startups are vying for. Others will enter healthcare with highly complementary assets to those that digital health startups bring to the table—acquisitions by middle children will emerge as a viable exit pathway. Expect to see a growing set of integrated digital and physical care platforms as digital health startups and middle children team up to deliver care in novel ways.

So who are we betting on? Winners in the future of healthcare will be those players with strong innovation and product development teams that can crack the nut of creating great experiences for healthcare consumers and commercialize them in the healthcare space. Successful execution will require humility as these entrants get up to speed on the complexity of the healthcare market. Personally, we’re excited to see this new future play out.

Rock Health Consulting advises enterprise companies on digital health strategy and innovation. For more information, reach out to advisory@rockhealth.com.

Footnotes

1 Walmart tends to attract the “big” retail label due to its $500M+ in annual revenue, 1.5 million employees despite having market capitalization around $400B.

2 Bose is not a public company, so market capitalization is not available.