H1 2021 digital health funding: Another blockbuster year…in six months

The digital health investment climate in one word: Up.

Funding, up.

Deals, up.

Deal sizes, up.

Acquisitions, up.

Public exits, up.

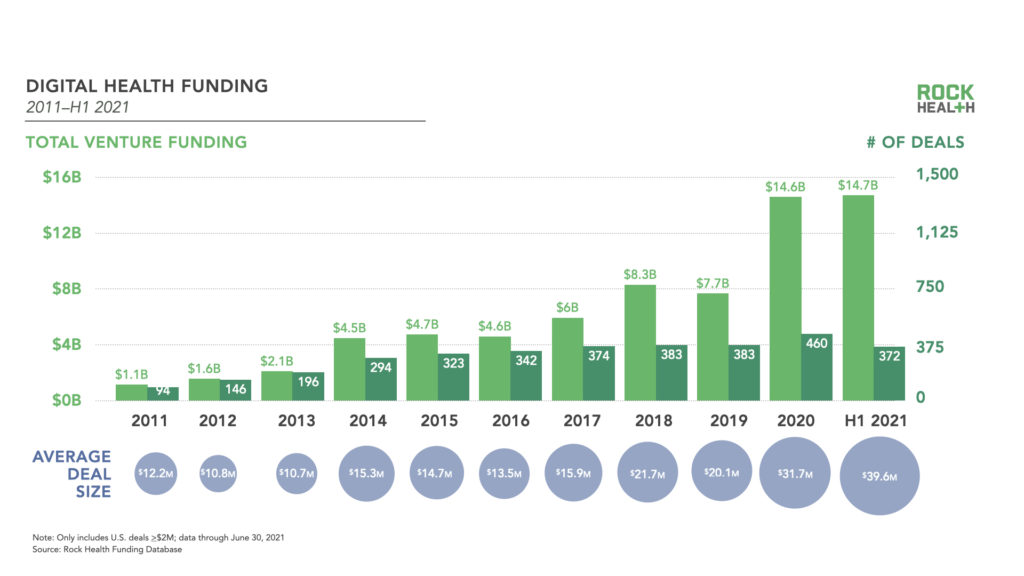

It’s been quite a ride this past year watching digital health catapult from a niche sector to a mainstream market. Seismic shifts from the COVID-19 pandemic launched digital health into high gear, and the momentum has only accelerated. The first half of 2021 closed with $14.7B invested across 372 US digital health deals with a $39.6M average deal size. Fifty-nine percent of that funding came from 48 mega deals ($100M+), including one of the largest single rounds of investment in digital health history: Noom’s $540M Series F round.

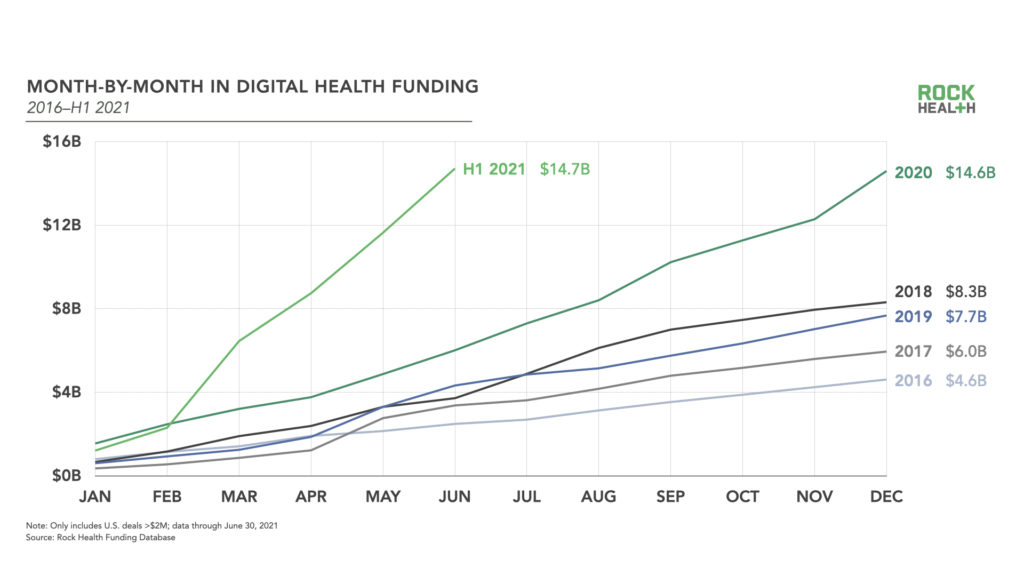

Even at its six-month mark, 2021 already surpassed 2020’s overall funding record.1 Monthly funding in June 2021 ($3.1B) was almost triple that of June 2020 ($1.1B), when digital health funding numbers began to accelerate after the first COVID-19 shutdowns.

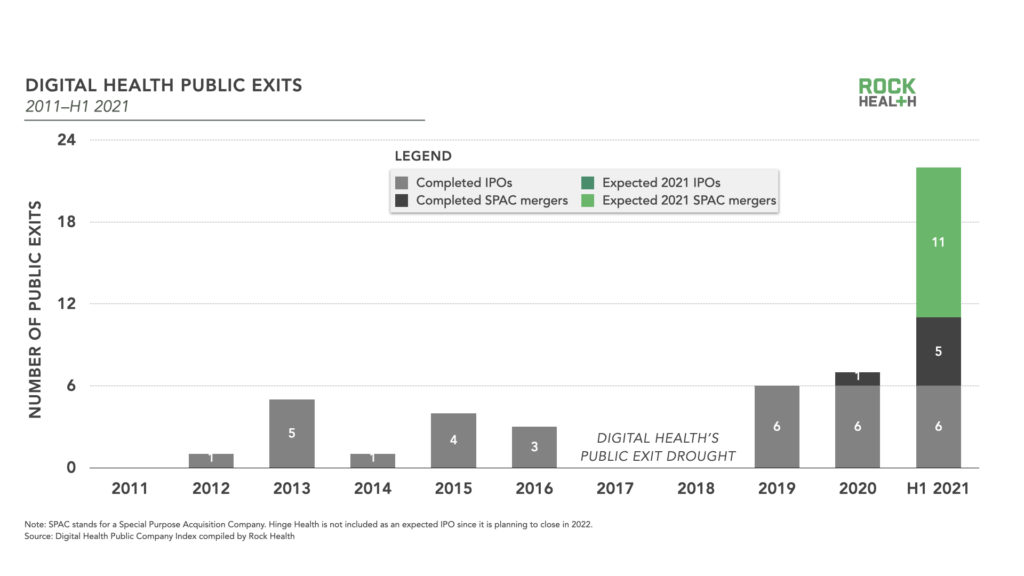

Digital health excitement isn’t limited to the private market, as public market investors, companies seeking acquisition targets, and special purpose acquisition company (SPAC) trusts are all looking to get in on the action. While seven digital health companies exited to the public markets in 2020, we’ve already seen 11 exits in the first half of 2021, with at least 11 more expected to close this year. M&A activity is heating up too: in H1 2021, each month saw an average of 22 acquisitions of digital health companies, compared to last year’s monthly average of 12.

“We’re seeing an increase in round sizes, new investors, and the pace at which funding is happening in digital health. There’s an acceleration of exits, as well as the emergence of combined companies that can address health care more broadly. It is exciting to see how quickly everything is happening this year.”

— Michael Pimental, Partner & Co-Founder, CVS Health Ventures

But the “mega momentum” of 2021 also introduces new risks for investors and entrepreneurs. This speed and amount of investment will test the marketplace’s current and future capacity to design and deliver digital health solutions, and then scale them into sustainable companies.

With our H1 2021 Digital Health Funding Report, we hope to help the healthcare community (and beyond) navigate these uncharted waters. Read on as we dive into the the rise of speedy funders dominating digital health investments (with, of course, an obligatory nod to Tiger Global), share strategies for founders navigating blitz-funding rounds and sky-high valuations, discuss the rising tides of D2C consolidation and M&A activity, and review public offerings and the rapidly-evolving SPAC environment.

Funding Booms In The Private Market

H1 2021 comprised the two largest quarters of funding activity in the US digital health market ever (sound familiar?). In addition to overall funding, 2021 is on pace to more than double 2020 in terms of both number of deals (372) and companies funded (359).

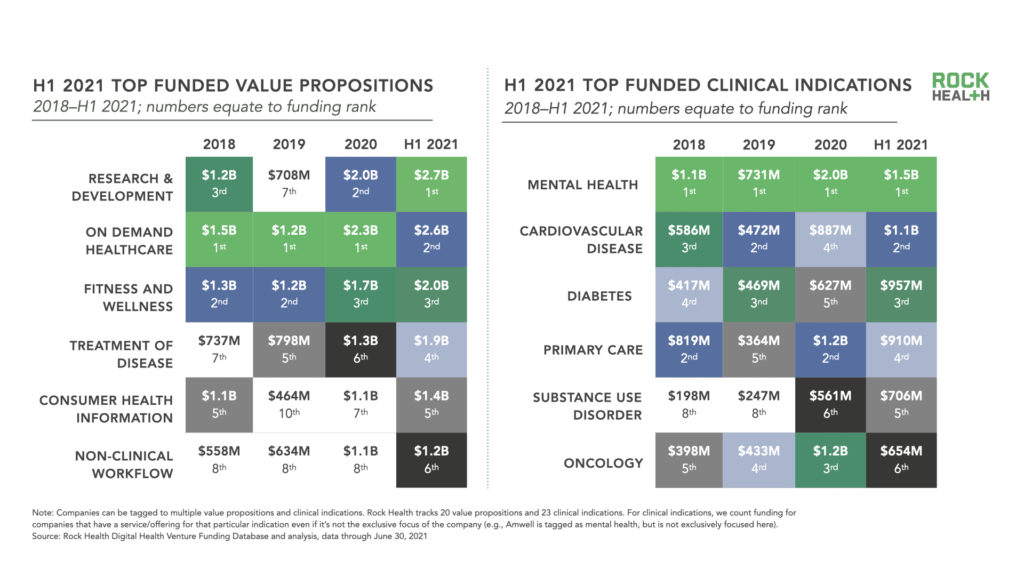

As we’ve noted in the past, investors didn’t change their overall strategies going into—or emerging from—the pandemic. Rather, they’re doubling down on their bets. The top-funded value propositions2 for 2020 and H1 2021 are consistent, with companies catalyzing biopharma/device R&D ($2.7B) and those delivering on-demand healthcare services ($2.6B) bringing in the most dollars.

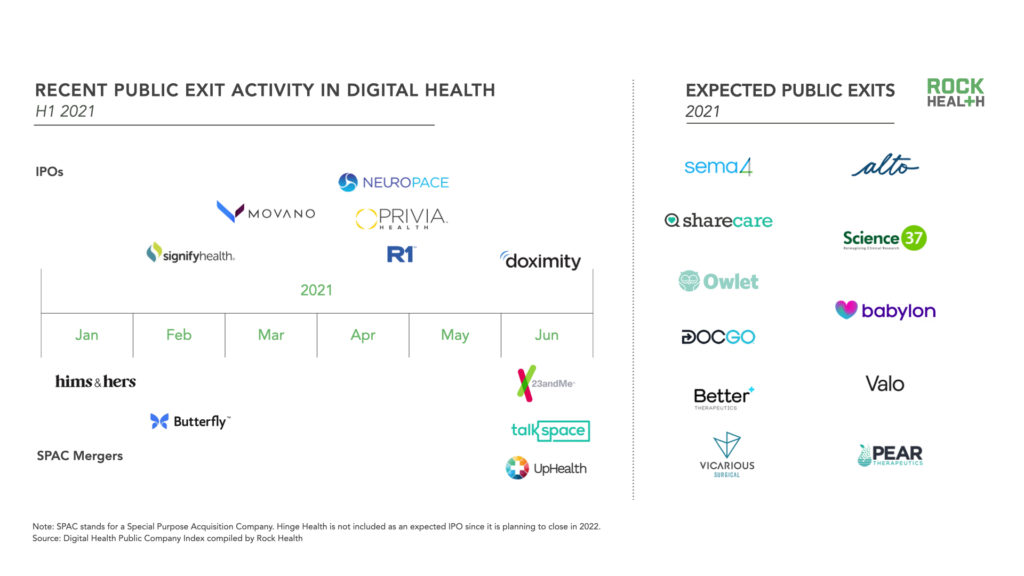

Mental health, cardiovascular disease, and diabetes are the top-funded clinical indications, with oncology investments dipping from third to sixth place since 2020. Funding for startups helping to manage substance use disorders steadily rose to fifth place, bolstered in H1 2021 by investments such as Pear Therapeutics’s $20M round in February—a company that also announced plans for a public exit via SPAC this June. Ongoing investment in mental health and substance use disorders tracks to our long-held belief that digital health helps to break down stigma and improve access to behavioral health support.

“We’ve seen continued investor interest in on-demand models, comprehensive primary care, behavioral health, fitness, and prevention. But what’s most refreshing to us is the sheer number of deals happening. It’s a great sign for the industry at large.”

— William Greineisen, Director of Strategy & Corporate Development, Cox Enterprises

Even though the distribution of funding to particular clinical indications and value propositions remains consistent, the amount of money flowing into these categories, and the pace of funding, is turbocharged. Total funding for each of the top six funded value propositions has already blown past funding for those categories across 2020, and we’re only at the half-year mark. The next section investigates what this market pace says about investor behavior.

Investors Or Speed Demons?

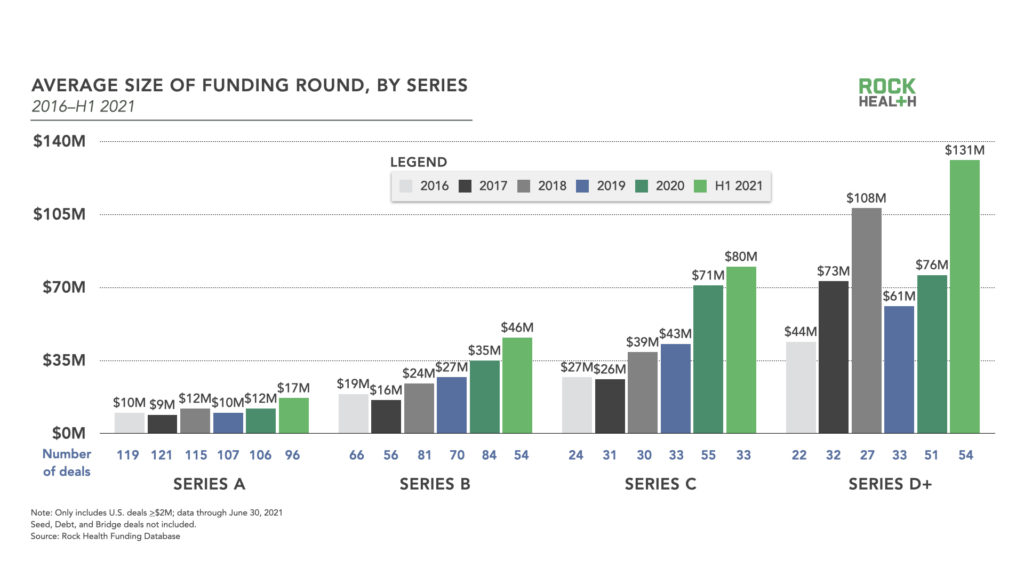

Let’s put the velocity of H1 funding activity into perspective: investors completed, on average, 11 deals totaling $548M each week in H1 2021, compared to H2 2020’s weekly average of seven deals totaling $285M.3 Funders are also investing more capital in later-stage rounds, as median deal sizes of Series C and D rounds increased by 1.1x and 1.7x compared to 2020.

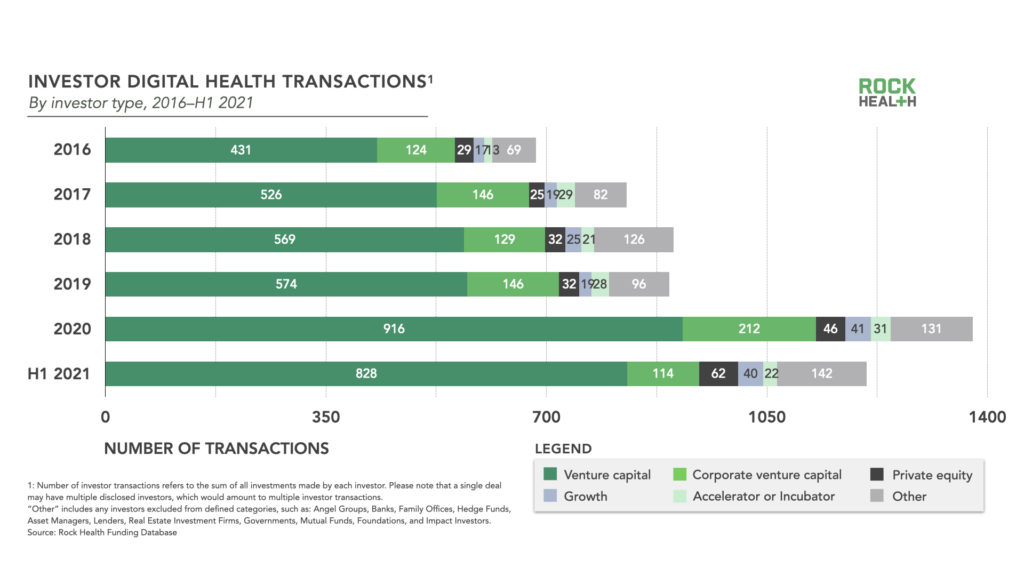

Bigger rounds and a faster pace of investment have understandably changed the mix of firms providing capital. In H1 2021, private equity firms and growth funds were more active in digital health venture investment than in the past. Only halfway into the year, private equity and growth funds have taken part in 102 digital health investment transactions, already exceeding last year’s total of 87. Other funders in the space included venture capital (828 transactions), corporate venture capital (114), and accelerators and incubators (22).

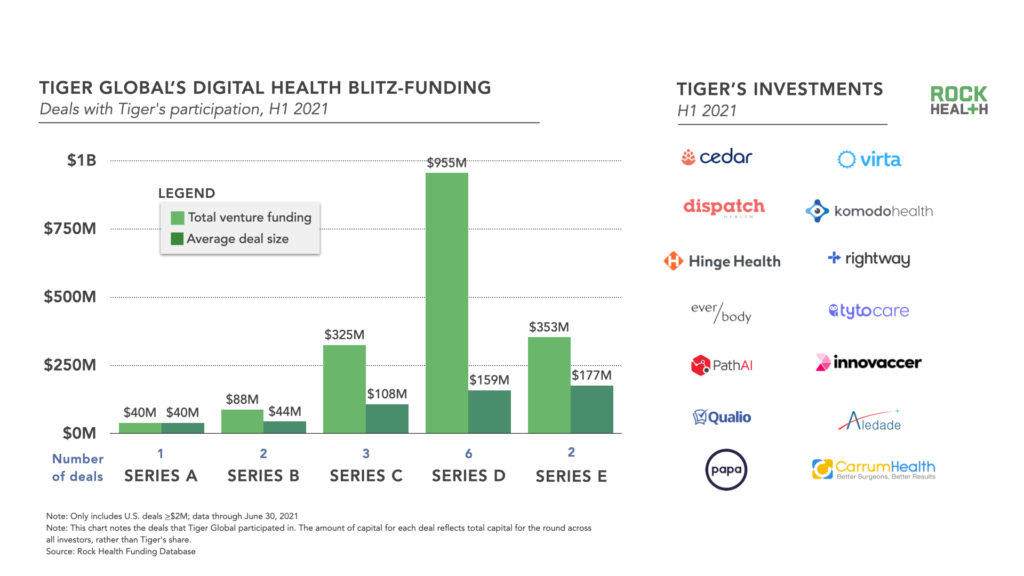

Among active funders, the elephant in the room is actually a tiger. Tiger Global, a tech-focused growth firm, has made no secret of their fund strategy: rapidly deploying capital through founder-friendly deals faster than other funds can keep up with. Tiger’s blitz-funding—our term for the venture capitalist version of the blitz-scaling entrepreneurial strategy made famous by Reid Hoffman—is a strategy that relies on the theory that the faster capital is deployed, the faster returns will (might?) be realized. Though Tiger updated the lyrics, this funding tune should sound familiar: Tiger is weaponizing investment speed in much the same way Softbank’s Vision Fund first weaponized scale just a few years ago. Assuming current venture investment market trends hold, there’s never been a better time for speed.

Tiger is blitz-funding across multiple industries, with a particular focus on digital health. Across this half, Tiger participated in 14 funding rounds for US digital health startups. These rounds amounted to $1.8B (12% of digital health funding so far this year). While information about Tiger’s share of these deals isn’t public, given their role as lead investor on many of them, it’s safe to assume Tiger’s betting big on the digital health venture market.

All but three of Tiger’s 2021 digital health investments came in at Series C or above, and some more established companies are using Tiger’s big check investments to fuel mega moves like acquisitions just a few weeks after their rounds close. Healthcare provider payment technology company Cedar nabbed a $200M Series D led by Tiger in March and then acquired health plan payments administration platform OODA Health in early May, while on-demand in-home care provider Dispatch Health closed a $200M Series D with Tiger in March, only to acquire Professional Portable X-Ray in April. Others are using Tiger’s funds to prepare for an IPO, like Hinge Health, which raised a $300M Series D with Tiger in January and announced plans to go public that same month. Since these investments are fueling not only startup growth but also acquisitions and public exits, Tiger has the power to influence the tides of the digital health investment ecosystem with just a few big bets.

Should smaller digital health investors start shaking in their boots? We don’t think so. Tiger has been slow to target early-stage rounds in any sector, and their biltz-funding approach doesn’t fully encompass the high-touch support that other investment approaches can offer. Strategic support from investors is key for later-stage companies too, especially those who are navigating possible business model pivots, which we’ll cover in our D2C section below. Smaller investors can be great round partners to a firm like Tiger, supplementing its pace with industry connections, expertise, and boots-on-the-ground operations help—all of which is critical for digital health companies across different stages.

Founders, Start Your Engines For Mega Rounds

As investors pick up the pace and volume of funding, digital health founders are more likely to find themselves navigating an overwhelmingly rich investment landscape. Fifty companies raised multiple rounds in the past 12 months (end of H1 2020—end of H1 2021), double the 25 companies that did so in the 12 months prior (end of H1 2019—end of H1 2020).

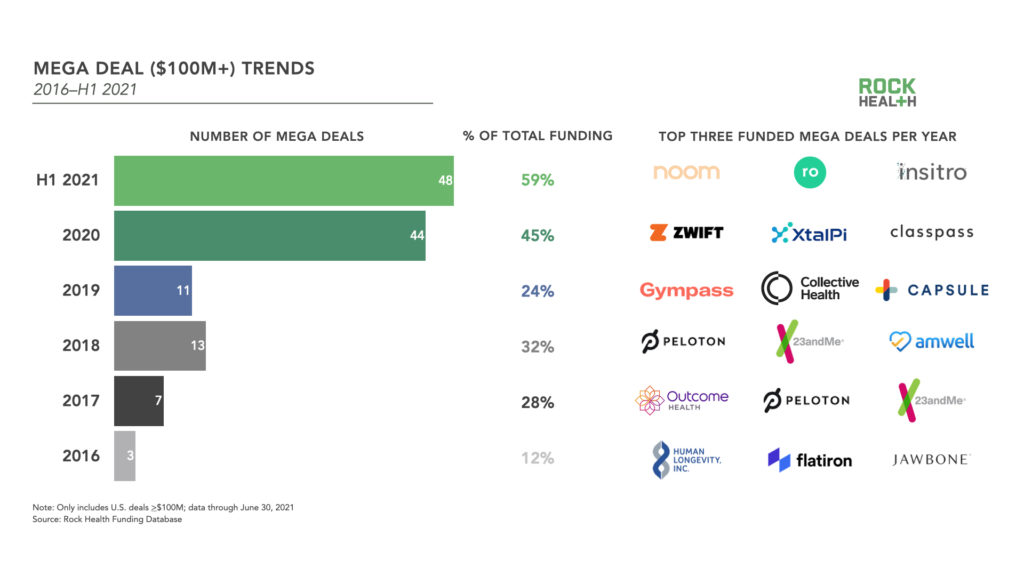

For founders today, landing a mega deal—a $100M check or greater—isn’t the Moby Dick that it used to be. The number of mega deals in H1 2021 (48) already exceeds the total number of mega deals in 2020 (44). On top of that, H1 2021 mega deal funding is blowing 2020 numbers out of the water by $2.1B, representing a 1.3x increase. Mega deals also accounted for 59% of total H1 2021 funding, 14 percentage points higher than in 2020.

With so much investment possibility, it’s crucial that founders maintain a healthy sense of valuation and investment cycles, and build a circle of trusted operating and funding partners to inform decisions. Thoughtful fundraising diligence for founders and investors alike can help prevent future challenges with “paying down the mortgage,” to paraphrase Sami Inkinen, Virta Health’s co-founder and CEO. In short, it’s important to have visibility into and confidence in your future projections and business roadmap, validated through product-market fit and economic model, before raising huge sums of capital.

It’s unclear how long this funding surge will last. As one experienced founder we recently spoke with put it, “Fill up when the appetizers are being passed around at the party because you don’t know how long you might have to wait until dinner.” For founders enjoying the current buffet of funding options, it’s a great time to hone in on partners that are mission-aligned and can add value in other ways, such as making key hires, thinking through problems, or contributing to strategic planning.

“A big value-add of fundraising is being in conversation with smart investors and folks who understand digital health. While we’re seeing a recent increase in mega-rounds happening very quickly, I try to pace fundraising by asking many questions of investors and advisors. Fundraising is fundamentally also a learning process for me and our team about what’s going on in the industry.”

– Naomi Allen, CEO and Co-Founder, Brightline

D2C Sprints Ahead (But Is It Sustainable?)

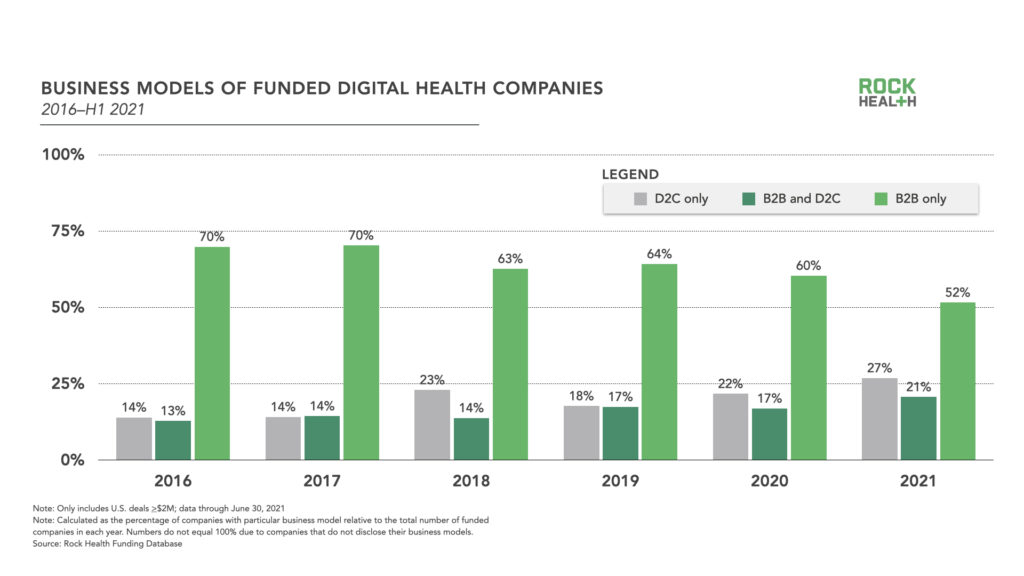

There’s more dry powder than ever before—but which types of businesses are most likely to see big checks coming through? While enterprise-facing companies are still the dominant players in the digital health marketplace, we were intrigued to see that over one quarter of all digital health companies funded in H1 2021 were direct-to-consumer (D2C)-only startups. This is the largest percentage in Rock Health’s ten-year tracking history, almost two-fold higher than the mid-decade baseline, and five percentage points higher than in 2020.

COVID-19-driven changes in consumer health behavior support the investment trend, as people have grown more comfortable using different virtual care and wellness products in their own homes. H1’s mega-mega D2C deals like Noom ($540M), Ro ($500M), and Capsule ($300M) signal investor confidence in this business model. There are some key benefits to the D2C approach: it allows companies to move upstream in consumer acquisition (marketing to individuals before they enter the healthcare system), meet consumers where they are (outside of a clinical setting), identify people’s most pressing needs (as Ro’s co-founder Rob Schutz explained), and personalize service for specific use cases, rather than to enterprise clients’ aggregate needs.

On one hand, a busy D2C market is a good thing: it fosters an array of specialized products and services that can meet the diversity of people’s health needs, and creates pressure for new and better product differentiators. Plus the benefits of D2C—direct consumer access, quicker transactions, and reduced regulatory/payment barriers—sum to a big advantage for startups entering the market and raising quickly. However, with limited total addressable market (when comparing consumer healthcare spend to enterprise healthcare spend) and high customer acquisition costs, D2C business models aren’t always conducive to achieving the scale and widespread impact that healthcare innovation can offer. Last but certainly not least, they often put the full burden of payment for healthcare onto consumers.

To realize the best of both markets, some digital health companies are adopting a dual approach; 21% of digital health startups funded in H1 are choosing to play in both the D2C and B2B markets. In June, ThirtyMadison—which consists of a portfolio of D2C digital health companies including Keeps, Cove, and Picnic—announced a $140M Series C round alongside plans to build out its B2B offerings.

As more D2C options become available, we expect consumers may start to feel some decision fatigue when allocating dollars and attention to different health products and platforms. For that reason, we’re anticipating some consolidation in the D2C market, with Ro’s acquisitions of D2C players Modern Fertility (in May) and Kit (in June) sending signals in this direction.

“It’s powerful to see D2C digital health companies serve specialized communities and provide some of the missing pieces to consumer healthcare. However, in some cases, consumers would find it easier to engage with a few consolidated platforms rather than flipping between brands.”

– Christina Farr, Principal Investor, OMERS Ventures

Consolidation Through M&A

If individual consumers may soon feel the avalanche of digital health offerings, enterprise customers are already saying, “we are inundated.” As such, these customers are pushing digital health companies to bundle services, integrate complementary offerings, and build out one-stop shops that reflect all the best the market can offer.

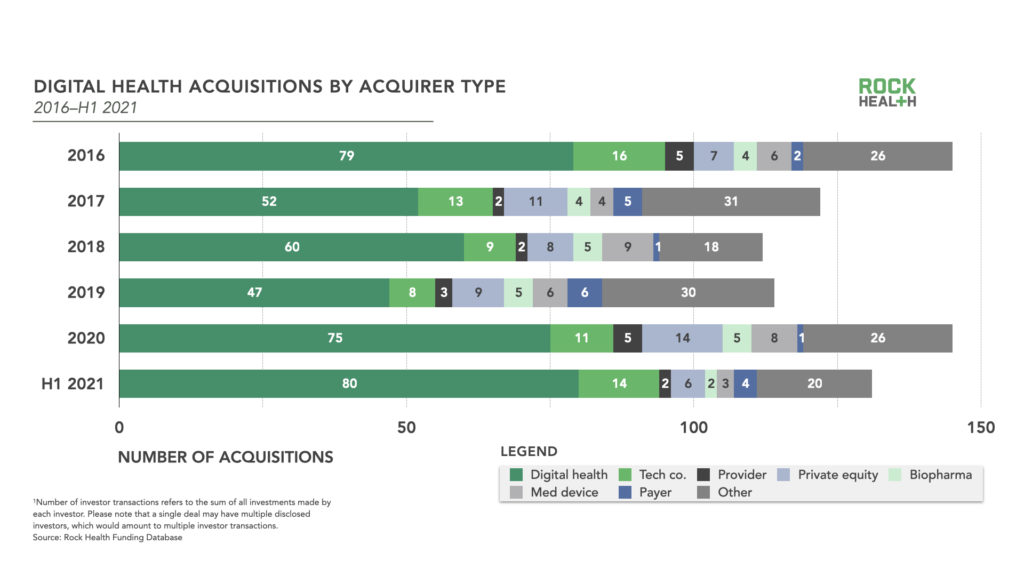

In this case, too much of a good thing (i.e., digital health activity) leads to consolidation through acquisition. H1 2021 saw 131 digital health M&A deals with an average of 22 deals each month, compared to last year’s monthly average of 12. Overall, 2021 is on pace to set a 1.8x year-over-year increase in M&A deals relative to 2020. Notably, digital health companies remain the largest acquirers of other digital health companies, another indication that market consolidation is a driver of at least some of the recent fundraising activity.

“With everything going on, we’re going to see more M&A. Private capital is priming companies to make acquisitions, and others to be targets of [public or private market] acquisitions.”

– Brad Weinberg, MD, Partner, Blueprint Health

Many of these consolidation moves are fueling digital health’s platform wars, where companies are acquiring other players to offer streamlined end-to-end navigation, services, and fulfillment for customers and end users. In an emerging front of these platform wars, broad digital health providers are snapping up startups focused on segment-specific verticals, such as Ro acquiring Modern Fertility (fertility and reproductive care) and Grand Rounds Health acquiring Included Health (LGBTQ+ care).5

Big tech companies like Amazon, Microsoft, and Google are also getting in on the acquisition action, working to integrate digital health features into their all-encompassing software solutions for enterprises. For example, in April, Microsoft acquired AI medical transcription technology Nuance to bolster its capabilities for healthcare customers.6 To us, acquisitions like these hint at traditional tech companies’ strategic plans for digital health, using relationships they’ve already established within enterprise teams (from email servers to cloud storage) as entry points for expanded service relationships.

These mergers and acquisitions—whether between digital health companies, or between big tech and digital health—ride on the promise of integrating value for customers, but this promise doesn’t always translate to reality. In the past, we’ve seen how consolidation in healthcare can actually hurt customers by raising prices and reducing benefits stemming from competition. We’ve also watched companies like Apple, Google, and Amazon, which made billions (or trillions) successfully integrating value in other sectors, run into hurdles developing healthcare offerings. Even as digital health’s M&A activity heats up, for the time being, we plan to sit tight on our predictions about who the eventual market leaders will be.

Public Market Exits Pick Up (Especially SPACs)

As digital health valuations continue to rise, it follows that more digital health companies are going public. Between 2013-2020, the average number of digital health public market exits per year was three, but in H1 2021 alone, 11 companies exited, and we’re tracking 11 announced or reported exits by the end of the year. Currently, all of these 11 announced or reported exits are choosing the SPAC route as their exit vehicle, which we discuss later in this section.

H1 2021’s uptick in public exits is a signal of the sector’s maturity, highlighting founders’ sustained access to capital, investors’ faith that more companies’ revenue models are “public market ready,” and rising consumer confidence in the long-term value of digital health solutions. Recent macro market conditions likely have an impact too: several studies have shown that IPO exit “waves” are usually triggered by positive market conditions in the previous 6-12 months, like the second half of 2020 (when stimulus measures from the Treasury Department and Federal Reserve reached their peak).

While exits are huge milestones for founders, employees, and investors, they don’t always equate to public market success. Listing on a stock exchange comes with regulated public reporting obligations and corporate governance requirements that inevitably create re-prioritization of leaders’ time and focus. Add on exogenous factors like market speculation, politics, and other hard to predict market activity that can shake or sway the entirety of the public markets, and ultimately public digital health companies are vulnerable in new and often unfamiliar ways.

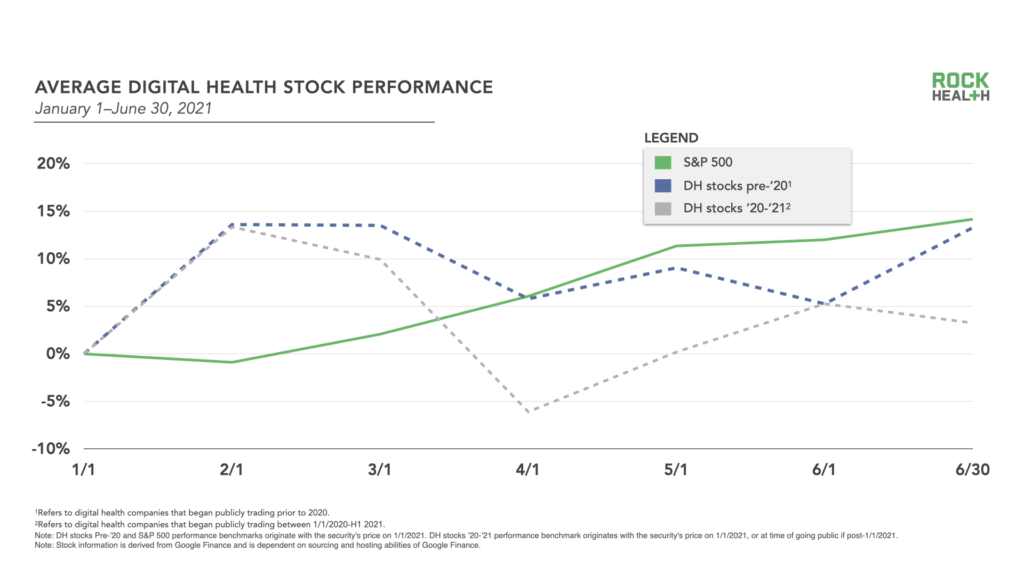

Some of these factors are already impacting digital health securities’ performance, especially for newer publicly traded companies. The 18 digital health companies listed on the NYSE and NASDAQ since January 2020 spent Q1 2021 beating the S&P 500, on average. However, their Q2 average stock returns fell below S&P 500 levels. It might take some time for these newly-listed companies to get their sea legs—just look at digital health securities listed before January 2020, whose average tracked or beat their younger counterparts for all of H1 2021. Pre-2020 exits’ average stock performance also beat the S&P 500 in Q1 2021, and closely chased the S&P 500 in Q2.

As we’ve written before, H1 2021 featured an increase in SPACs as exit vehicles for digital health companies. SPACs accounted for five of the 11 digital health public exits in H1 2021 and are slated to make up all of the currently-expected public exits for the remainder of this year. Additional SPAC exits in the sector are likely, considering there are currently 39 SPACs7 actively searching for healthcare or digital health targets (collectively, $9.5B in trust). Upon creation of a trust, each SPAC has approximately two years to make an acquisition.

Which digital health companies might become future SPAC targets? While there are many factors that play into target selection and deal negotiation, prior funding serves as one clue to help (imperfectly) estimate which companies might be public market-ready. Since 2020, digital health companies acquired or announced to be acquired by SPACs raised, on average, $212M in private funding before their acquisitions. According to Rock Health’s Digital Health Venture Funding Database, 47 active digital health startups have raised that amount so far, making them potential targets for healthcare SPACs.

This data suggests little daylight between demand (39 SPAC trusts targeting healthcare/digital health) and supply (47 highly-capitalized digital health startups). Sharp elbows are likely to emerge as SPAC trusts compete for sought-after targets, and the competition could increase even further if SPACs not explicitly focused on healthcare start picking up digital health targets. For example, Pear Therapeutics is being acquired by the Thimble Point trust, which was seeking “high-growth software and technology-enabled companies that are disrupting large and established industries.”

Additionally, as SPAC sponsors compete with enterprise companies jockeying for acquisitions, this could mean even higher negotiated valuations for SPAC and M&A deals, and larger later-stage funding to offer yet another alternative to startups’ public market considerations. The implication: SPAC sponsors may be broadening their search criteria to include earlier stage, less capitalized companies in order to close an acquisition within their two-year window.

Moving forward, increased SEC scrutiny and hikes in SPAC investment insurance premiums are poised to make additional SPAC formations more cumbersome (maybe even as cumbersome as good ol’ IPOs or direct listings?), which makes us wonder how long SPACS will remain the top public exit vehicle for digital health companies. In the long term, we expect that lessons from this year’s SPAC activity, as well as associated regulatory changes, will lead to a more sustainable, though varied, digital health public market entry environment overall.

Reaching New Heights

Just six months ago, 2020’s full year digital health funding numbers blew us away, and by Q1 2021, we staked our claim that digital health was all grown up. It’s been a wild ride watching Q2 2021 blow Q1 out of the water. We’re most inspired by the digital health companies making the most of this momentum to leap forward in the direction of massively changing healthcare for the better.

From our perch, we’ll balance our excitement with a vigilant eye toward the real world implications of digital health’s fast-paced activity in the private and public markets. We know today’s environment presents as much opportunity for entrepreneurs and investors as it does risk, and it’s important that neither party gets caught flat-footed once digital health settles into a new funding stride.

The fundamentals—new solutions to big problems, high-quality teams, laser focus, and strong investment syndicates—will endure as the driving forces of digital health’s maturation and impact on the entire healthcare sector. As we look forward, we know that digital health’s journey to impact is a marathon, not a sprint.

Rock Health’s venture fund continues to invest in entrepreneurs bringing unique and innovative technology to healthcare. We would love to hear from you. Get in touch!

Rock Health Advisory provides guidance on digital health strategy, access to proprietary funding databases, and in-depth perspectives on the digital health market. For digital health insights targeted to your needs, drop us a note.

Finally, stay up to date with the latest headlines in healthcare technology and Rock Health news by subscribing to the Rock Weekly.

Footnotes

1 Our Rock Health venture funding database is constantly refreshed with new information and SEC filings, including deals closed in the prior year. This accounted for an increase in 2020 funding relative to our EOY 2020 reporting.

2 Each company in the Rock Health Funding Database is tagged with at least one and up to three “value propositions.” Since each company may fall into multiple value propositions, the sum of the funds raised across value propositions does not sum to the total funds raised.

3 When SEC filings are unavailable, Rock Health relies on publicly available funding announcements to determine the date of a closed deal. This can be an imprecise measure that lags the actual deal completion, but as an approximation, it offers a clear signal on the volume and pace of funding.

4 Investor transactions refers to investments made by each investor. Please note that a single deal may have multiple disclosed investors, which would amount to multiple investor transactions.

5 Grand Rounds Health is itself the product of a merger between two digital health companies, Grand Rounds and Doctor on Demand.

6 It’s worth noting that traditional tech’s digital health pipeline starts well before M&A in the venture market: traditional tech players accounted for 22% of corporate investor transactions in 2021, up four percentage points since 2020.

7 To approximate this number, we averaged the trust values (from last filing) reported within SPAC Track’s Active SPAC List for the 39 SPACs tagged to be looking for “healthcare,” “healthcare tech,” or “healthcare innovation” targets.