2020 Market Insights Report: Chasing a new equilibrium

It’s hard to believe that nearly a full year into the COVID-19 pandemic, the crisis is still not over. While two vaccines have been authorized for emergency use in the US, new confirmed cases and deaths continue to rise. And although the unemployment rate peaked at nearly 15% in April 2020, the most recent official rate as of November 2020 remained at 6.7% (whereas it was 3.5% in February 2020). The pandemic’s toll on human lives and livelihoods will remain the somber legacy of 2020, and the disequilibrium introduced by the pandemic—into the healthcare industry and every aspect of life—has not yet stabilized into a new normal.

As the pandemic laid bare many of the healthcare industry’s vulnerabilities, it also accelerated adoption of digital health—from virtual care models to data-driven drug discovery. In response, both incumbent healthcare institutions and entrepreneurs demonstrated tremendous leadership and innovation. The pandemic also spurred widespread change in provider and consumer behavior and led to an unprecedented influx of investment in digital health.

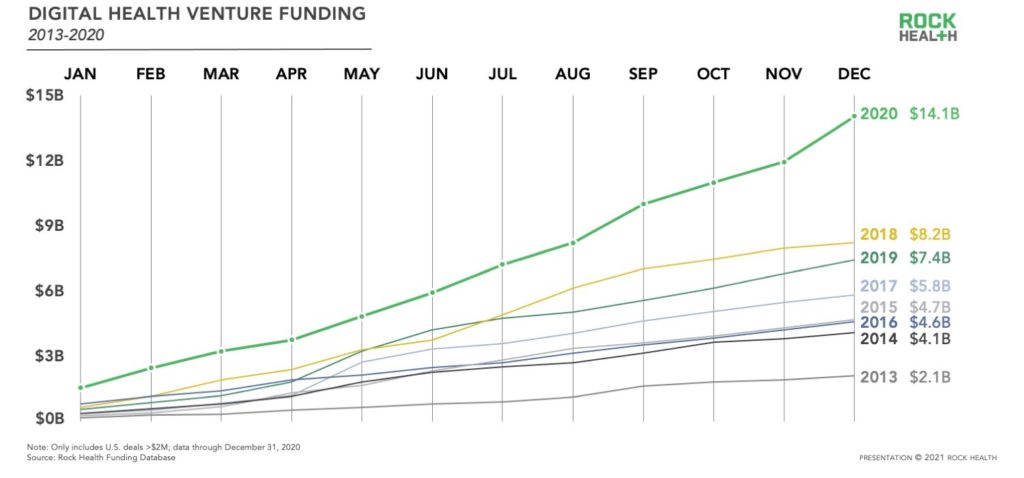

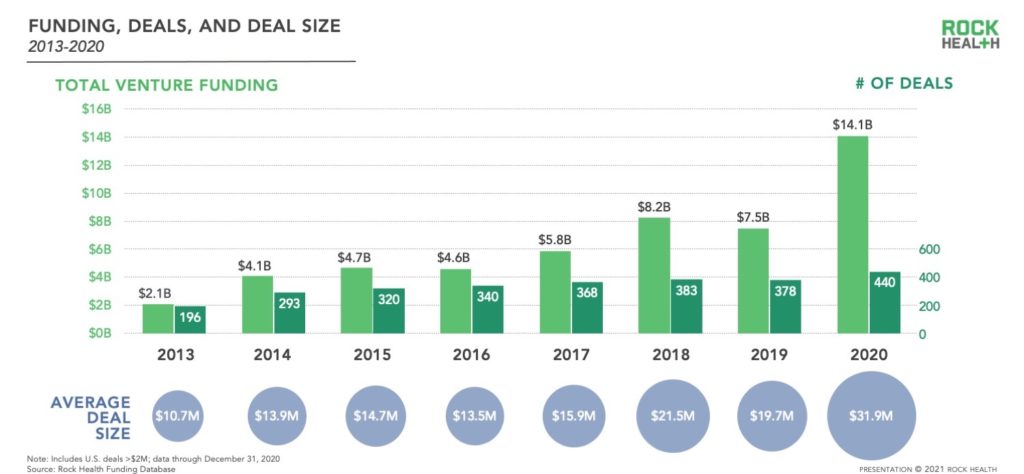

Across 2020, US digital health companies raised $14.1B in venture funding, the largest amount of capital deployed in a single year since Rock Health began tracking funding in 2011. This amount represents a 72% increase from the previous high water mark set in 2018. $5.9B was raised in the first half of 2020, with H2 delivering the most funding in a half-year ever with $8.2B. Investors also closed more deals than ever before, with 440 deals in 2020 compared to 378 in 2019 and 383 in 2018—15% growth in investment activity over the past 36 months.

In addition to closing more deals, digital health companies also raised more per deal. Over the past 36 months, average deal size increased from $21.5M in 2018 to $31.9M in 2020. Average deal size was largely bolstered by 40 mega deals, rounds of $100M or more, which accounted for more than half (57%) of total 2020 funding.

Digital health entrepreneurs, investors, enterprise healthcare leaders, and even non-healthcare companies took advantage of this moment to sprint towards digital health innovation at an unprecedented pace.

But, the question at hand is: With so much and such rapid change, what will last? What will digital health’s new equilibrium look like? The answer will be revealed in months and years to come. For now, we at Rock Health examined four factors that underpinned the accelerated transformation of 2020 and suggest the contours of a future equilibrium:

- Investor and investment activity

- Consumer behavior change

- Enterprise buyer behavior

- Exit and public market activity

1. Investor and investment activity

With the digital health sector springing into action to ensure healthcare delivery and discovery didn’t grind to a halt, investors pumped more dollars into startups than ever before. They slowed investment activity at the onset of the pandemic to reassess and focus support towards their existing portfolios, but investment rebounded with renewed force as signals from consumers and B2B buyers trended towards engagement and adoption for digital health services.

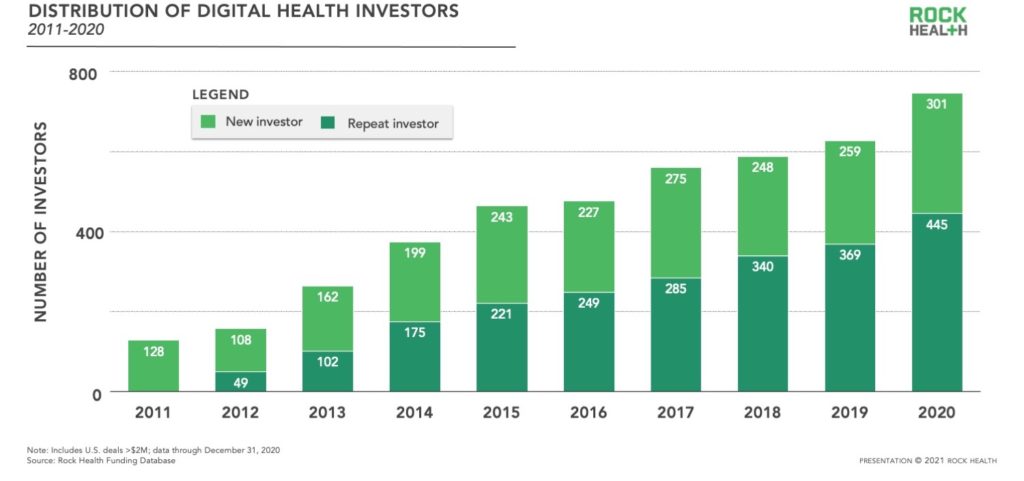

With healthcare in the spotlight—and the potential of digital health strikingly evident—more new investors (and entrepreneurs) rushed to the space than any year prior. Three hundred and one investors made digital health investments for the first time.

This year definitely challenged my discipline to be a thoughtful investor, especially as investors are sitting on so much dry powder and we are playing in an area everyone is interested in.

— David Kim, CEO, DigiTx Partners

A growing market and rush of interest could signal overeagerness in the market—and even a bubble, if that overeagerness is accompanied by conditions like unjustifiably high valuations, a flood of new entrants, and a poor exit market (based on Rock Health’s framework). Across H2 2020, there was some speculation about early signs of froth. But on the whole, market features in 2020 suggested that digital health is a maturing market, rather than a segment plagued by inflated expectations. These market features include:

- Continued activity from repeat investors, who made up 60% of total investors in 2020 (see chart above).

- A healthy mix of investment across early- and late-stage companies.

- Consistent investment themes, rather than a hard pivot in investment theses.

- A maturing digital health infrastructure, lowering barriers to entry, and enabling speed and scale.

Repeat investors

Repeat investors are those who have made at least two investments in digital health. In the early days of digital health (over a decade ago) the majority of investors were noobs and dabblers. Today, nearly two out of three investors are veterans of the industry who understand the opportunities and risks. Our data show that growth in venture investment in 2020 was largely driven by these veterans “doubling down”—rather than new entrants chasing a trend.

A healthy mix

Investor interest in digital health was matched by more companies seeking capital—as Julie Yoo, General Partner at Andreessen Horowitz, noted to us in the fall: “It was a pretty bonkers summer in terms of deal volume. We ran the numbers and year to date, deal volume through Q3 in 2020 is up nearly 22% compared to all of last year.”1

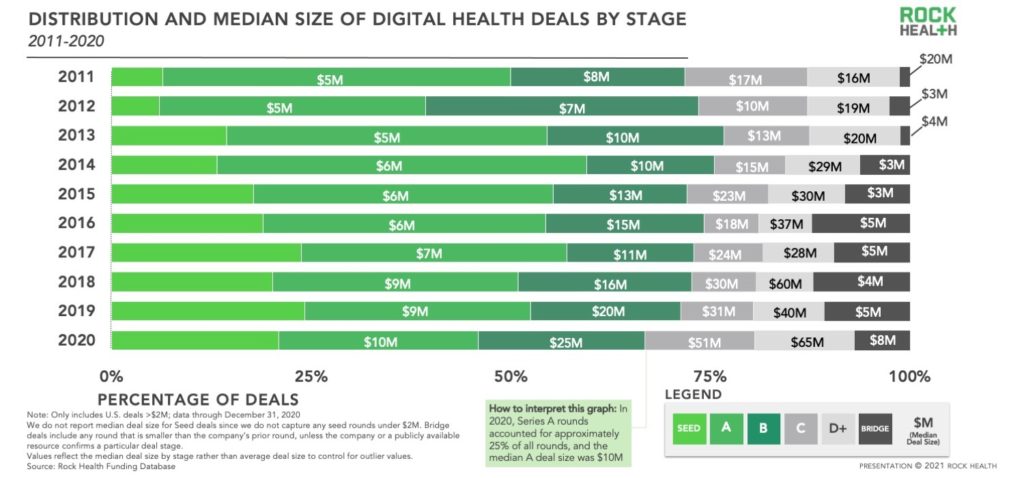

Despite 2020 bringing a greater proportion of large, late-stage deals compared to previous years, there is still a healthy balance between early, mid, and late-stage deals. The proportion of deals at each stage (Seed, Series A, Series B, etc.) has been relatively stable over the past five years with a modest increase in the proportion of Series C and D (late stage) deals in 2020.

Consistent investment themes

While pandemic-induced shocks changed all aspects of life, digital health investors largely stayed the course. Investments in areas such as on-demand healthcare and research and development catalysts remained among the top investment categories, as in recent years. Though priorities may have sharpened during this time, it appears that the pandemic heightened the urgency for existing areas of investment—rather than requiring a pivot to an entirely new vision.

For many people in this space, they invested in trend lines this year that were already a part of their strategy. It’s like we’ve seen five years of natural evolution turn into three quarters of revolution. Many people were already believers and investors in digital health, to see the fruits of the labor is really exciting.

— Lynne Chou O’Keefe, Define Ventures

On-demand healthcare was the most funded value proposition2 in 2020, with $2.7B total funding across 68 deals. The top three funded deals in this category were: Alto Pharmacy ($250M), Ro ($200M), and Amwell ($194M). R&D catalyst companies (whose services accelerate drug and device research and development) raised $2.0B in funding in 2020, and jumped five positions in terms of most funded value proposition compared to 2019. This category experienced a drastic increase in funding this year, something we in part attribute to the sprint to develop a COVID-19 vaccine. The top three funded deals in the R&D catalyst category were: XtalPi ($319M), ConcertAI ($150M), and Insitro ($143M).

A couple of differences between 2019 and 2020 stand out. First, the amount of capital invested across these two value propositions dramatically increased from 2019 to 2020—on-demand healthcare companies raised 2.25x more capital and the R&D catalyst category grew 3x from 2019.

Second, specific types of virtual healthcare saw an increase in funding year over year. For example, a surge in demand for mental healthcare was met by a 2.9x increase in digital behavioral health funding compared to 2019, with $1.8B in funding across 55 deals in 2020 compared to $609M in 2019. The largest rounds for companies offering behavioral health services were raised by Amwell ($194M), Headspace ($140M), Lyra Health ($110M), and Mindstrong ($100M).

Finally, the stay-at-home and physical distancing measures in 2020 increased demand for at-home fitness and wellness care. Companies that support general fitness and health maintenance received the third-highest amount of funding this year, with $1.7B in total funding across 34 deals (compared to nearly the same amount of deals in 2019 but only $1.2B in funding). The top funded deals in this category included: Zwift ($450M), ClassPass ($285M), Tonal ($110M) and Strava ($110M).

Maturing infrastructure

Rather than individual companies having to build their own base technology and infrastructure, many building blocks are now available for digital health companies to leverage. For example:

- TruePill offers remote pharmacy infrastructure, enabling Nurx, Hims, and GoodRx, among others, to fulfill and deliver prescriptions nationally, freeing up these companies to focus on their bread and butter: consumer experience.

- Meanwhile, data integration is maturing, with companies such as Moxe, Redox, Datavant, and Particle Health creating linkages to EMRs across the country, taking the heavy lifting out of patient data exchange and enabling builds on top of health system data.

- Solutions to standardize biomarker tracking have emerged, with Apple Health Kit as a clear example. Evidation enables real world and clinical data aggregation, seamless data ingestion and processing, and a platform for algorithms and analysis. Elektra Labs provides operational and data governance support to organizations by helping them decide what they should measure and which technology to use.

- Companies like Enzyme and Aptible dramatically reduce the cost for digital health and life science companies to build compliant products and maintain regulatory compliance.

Many of the startups mentioned above raised capital this year—with GoodRx going public and Hims planning to do so—signalling investor excitement for infrastructure that is catapulting the rest of the ecosystem forward.

We are seeing valuation levels that we did not see 12 months ago, which underscores the enormity of the market opportunity and the accelerating pace of technology adoption. The theoretical market has always been enormous, but we are seeing reprioritization of budgets, the urgency for sophisticated solutions, and extraordinary growth for everyone involved in re-architecting the healthcare system.

— Michael Greeley, cofounder and General Partner, Flare Capital Partners

In many ways, 2020 validated the theses of many healthcare investors, and accelerated consumer adoption trends and enterprise buying behavior that are necessary ingredients for long-term sustainability. We take a close look at consumer and corporate buyer trends next.

2. Consumer behavior change

Sparked by the pandemic and stay-at-home orders, and supported by reimbursement from commercial payers and CMS’s telehealth expansion, telehealth adoption surged, reaching a peak in April 2020. Though utilization has steadily declined since, adoption still remains well above pre-pandemic baselines. According to research from The Commonwealth Fund, telehealth visits made up 14% of baseline total outpatient visits at peak adoption in mid-April. The percentage of telehealth visits leveled off around 6-7% at the reporting of the latest data, which is still substantially greater than the pre-pandemic percentage of 0.1%. After the initial surge in adoption, it seems the pendulum is swinging back towards in-person visits, which begs the question: What will the new equilibrium of consumer adoption of virtual care look like?

It is hard to ignore the obvious signal that when patients were given the option to go back to in-person provider visits, many did. Though our 2020 Consumer Adoption survey indicated high levels of satisfaction with live-video telemedicine experiences (90% of respondents who reported using live video were extremely/moderately satisfied with their visit), most patients are choosing to resume in-person visits. Despite this return to traditional healthcare-seeking behavior, we believe the exposure of patients and providers to virtual care (many for the first time) will have a lasting impact on the trajectory of digital health adoption.

Is the COVID experience as good as or better than the experience they’re getting before? If the answer is not as good, telehealth won’t sustain. It’s a blip. If the answer is better, then it’ll actually persist. Most people are now choosing to get in-person care again. It’s still a better experience in person. This is an opportunity in telemedicine. How do we flip the script for telemedicine to be an unquestionably better experience?

— Ambar Bhattacharyya, Managing Director, Maverick Ventures

For one, recent levels of telehealth utilization are still dramatically higher than telehealth utilization pre-pandemic (see above, 0.1% of all visits). We at Rock Health believe that telemedicine adoption is following a step response: Accelerated by the “impulse” delivered by the sudden onset of the pandemic, telemedicine adoption levels initially overshot. Adoption levels will, we believe, decline from this peak and oscillate for some time before settling at a new, higher-than-before baseline. And with a second round of stay-at-home orders, a sluggish vaccine rollout, and fears about traditional healthcare sites, some of this newfound use of telehealth is likely to stick, especially if patients are having virtual experiences that offer convenience, availability, and safety at a level superior to in-person experiences.

The question is will we see deceleration of telemedicine if the pandemic starts to wind down? I do not think so. People approach the healthcare system differently now. Consumers are impatient if they are not getting on-demand services so the system has to retool to accommodate that. People will demand high levels of service from healthcare providers, whereas before we simply tolerated bad service.

— Michael Greeley, cofounder and General Partner, Flare Capital Partners

Second, at Rock Health, we believe the predominant form of telemedicine used by most Americans today does not necessarily reflect the future potential of virtual care. The bets made by other digital health investors this year signal they share this view. Much of the telemedicine used this year is akin to replacing an in-person visit with a virtual one, offering one-on-one care over the phone or a computer screen. These interactions look like the traditional synchronous, patient-provider model that has governed a reactive, episodic, and costly care model. This type of interaction and care will to some extent always be necessary, and when patients have both telemedicine and in-person options available, they are today largely choosing in-person.

But a number of the dominant digital health companies funded this year offer virtual care that is sustained, typically outcome-driven, and tech-enabled. These companies enable recurring interactions between a patient and a care team (synchronous and asynchronous), often with data flowing from connected monitoring devices, in support of disease monitoring and management. This model is being carried out by many of the most well-funded companies of the year, such as: Lyra Health ($110M), Virta Health ($93M in January and $65M in December 2020), Omada Health ($57M), Podimetrics ($25M), and Brightline ($20M). Teladoc has also made it clear, through its acquisition of Livongo, that they are betting on a virtual care model that combines face-to-face visits with programs that offer ongoing health management through connected devices, algorithm-driven recommendations, and virtual touchpoints with providers. Of course, many innovations still need to come to fruition so virtual care capabilities come closer to matching the capabilities of an in-person provider, including at-home diagnostics and remote patient monitoring. For example, TytoCare raised $50M for its at-home diagnostic and telemedicine platform, expanding the scope of services that can be safely and effectively delivered in the home. Additionally, Conversa Health raised $12M in 2020 to further its patient profiling and health signals AI platform, enabling personalized messaging, health reminders, and care to be delivered at-home. As investors, we believe pushes in this direction towards continuous, tech-enabled virtual care will yield a better and more efficient patient and provider virtual care experience.

Additionally, digital health is offering consumers valuable healthcare experiences far beyond a virtual visit. Take digital pharmacy and delivery. Amazon Pharmacy made waves with their launch in November 2020, flexing their clinical, technical, and customer experience expertise to be a formidable player in this space. CVS, Walgreens, and Rite Aid are already feeling the impact, as evidenced by stock price drops right after Amazon’s announcement. Meanwhile, in the quest to make clinical assessments and prescription delivery more akin to the ease of grocery delivery, startups in the space Alto, Ro, and Hims all had big years between fundraising, acquisitions, and a SPAC announcement.

Telehealth visits may be down relative to their peak, but we anticipate a durable, new equilibrium well above pre-pandemic levels. And the next wave of virtual care solutions—which are set up to offer value beyond the limitations of episodic, in-person visits—are well on their way, with significant funding in tow. Enterprise buyers are showing interest, as evidenced by uptick in reimbursement and investment, outlined next.

‘Will the genie go back into the bottle?’ I’m not worrying about that. Healthcare stakeholders have had this wealth of virtual care experiences, good and bad, easy and difficult—that experience creates imagination, creates informed customers, who begin to really understand what is possible through digital health.

— Liz Rockett, Director, Kaiser Permanente Ventures

3. Enterprise buyer behavior

The enterprise buyers of digital health solutions—providers, payers (including government), pharma, employers—showed a commitment in 2020 to investing in and adopting enabling technologies and virtual care solutions, even in the face of uncertainty and budget tightening.

We were astonished by how unfrozen the budgets of providers, pharma, and payers became when they realized their traditional business models had to shift on a dime. For the first time, we saw sales cycles happen in weeks, not quarters.

— Ambar Bhattacharyya, Managing Director, Maverick Ventures

In March of 2020, the federal government unlocked perhaps the biggest driver of scale and sustained adoption of virtual care by covering video visits (on an “emergency basis” during the pandemic) and by offering flexibility on use of different platforms, even FaceTime. Regulators also began to allow physicians to practice medicine across state lines. While it’s unclear whether these policies will stick after the emergency authorization period, HHS has signaled ongoing commitment to marching towards virtual care and in November 2020 the Veterans Administration (VA)—America’s largest single healthcare provider—released an interim final rule that will permanently enable VA physicians to deliver care virtually. Regulation, as well as the buying behavior of the federal government, will continue to influence the reimbursement decisions of commercial payers—as well as offer reassurance to corporate and traditional investors of the growth trajectory of the digital health market.

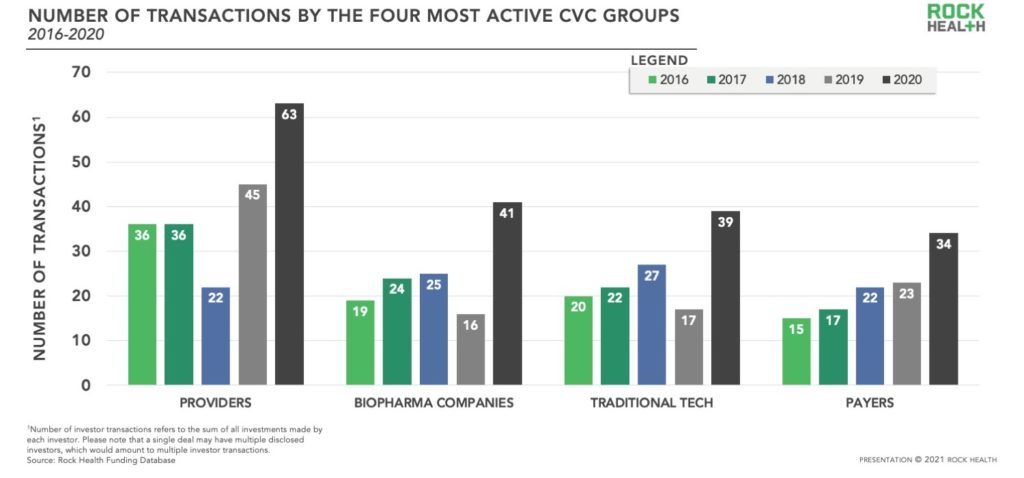

In 2020, corporate VCs (CVCs) accounted for 15% of all investor transactions, compared to 14% in 2019, and participated in 212 investment transactions, compared to 144 in 2019 and 129 in 20183. Among CVC transactions, provider organizations were the most prolific, accounting for 30% of CVC transactions.

Whereas providers’ and payers’ investment pace held steady from 2019 through 2020, biopharma companies and traditional tech reawakened their digital health interests, with a 2.6x and a 2.3x increase respectively in transactions completed since 2019.

Seventy percent of the deals CVCs participated in were later stage deals (Series B or later), compared to 56% among all investors and 53% among non-CVC investors. CVCs completed 149 transactions at Series B or later, compared to just 42 Seed / Series A transactions.

Despite uncertainty and for some, tightening budgets, the rise in CVC participation in deals signalled a more rapid embrace of digital innovation among enterprise healthcare.

4. Exit and public market activity

2019 was a breakout year for digital health IPOs. After public market gyrations induced a lull in H1 2020, the IPO market resumed in the latter half of 2020, rounding out the year with a total of six traditional digital health IPOs (Accolade, Amwell, GoHealth, GoodRx, Outset Medical, and Schrödinger) and one digital health SPAC (or Special Purpose Acquisition Company) now traded on the public market (SOC Telemed). SPACs raise cash through an IPO, and use capital raised in its IPO to acquire or merge with an active company, typically a privately-held, venture-backed startup. The combined market cap for the seven 2020 IPOs at the end of 2020 was $37B.

When it came to exit activity, the traditional IPO was joined by the resurgence of a different exit vehicle (and acronym) in town: SPACs. Notable 2020 SPAC transactions included:

- Following 91% year-over-year growth, Hims & Hers announced a merger agreement with Oaktree Capital Management’s SPAC Oaktree Acquisition.

- Clover Health, the Medicare Advantage startup, announced plans to go public in a $3.7B SPAC deal with Social Capital.

- Augmedix, a Rock Health company, went public through a reverse merger with Malo Holdings.

Additional SPACs included MultiPlan, SOC Telemed, Cano Health, and Uphealth and Cloudbreak Health, while Lux Health Tech and former Livongo executives each announced new SPAC investment vehicles.4

Although SPACs offer a convenient, less costly alternative to the traditional IPO process to achieve returns and liquidity, some investors and founders have expressed a preference for the traditional IPO path, which typically offers more infrastructure and wraparound support.

Meanwhile, public digital health companies saw significant increases in valuation across 2020. Seventy-six percent of companies in the Rock Health Digital Health Public Company Index increased their share prices in 2020, and the seven newly-minted public digital health companies gained 31% in total market capitalization since going public.

The increase in the number of digital health companies going public—and the durability of valuations in the public index—represents a thematic shift in liquidity for digital health venture investors. Not long ago, private market investors (including us!) actively voiced concerns over a 2+ year “IPO drought” (during 2017 and 2018). In those years, the influx of venture investment into digital health significantly outpaced the flow of liquidity, or exits, for venture investors and entrepreneurs. However, we posited that the industry simply wasn’t yet ready—in terms of the maturity of the venture-backed startups funded to that point in time—for a surge in IPOs. And although we acknowledged that public market liquidity was lagging private-market fundamentals, we nonetheless made the case that private investors were still acting in a largely rational manner. The storyline we anticipated (and the decisions we made based on it along the way) is more or less bearing out in the present day.

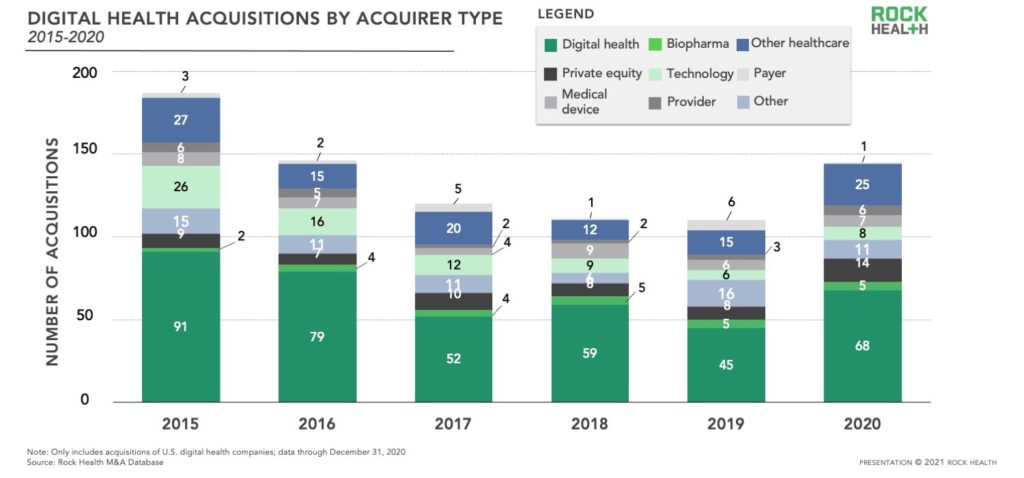

Alongside the resurgence of public market interest in digital health, it is worth noting that privately-held digital health companies are still more likely to exit via merger or acquisition. In 2020, there were 145 mergers or acquisitions (compared to 113 in 2019), including the largest acquisition in digital health ever with Teladoc purchasing Livongo for $18.5B (paid almost entirely with shares). Other notable transactions included: Centene’s acquisition of AI healthcare analytics company Apixio and HealthStream’s grab of Change Healthcare’s scheduling business for $67M. More recently, Optum announced its intention to acquire Change Healthcare in a $13B deal. In line with previous years, digital health companies continue to be the most frequent acquirers of other digital health startups.

What’s next?

We would not wish 2020 upon anyone, ever again. But the stress test to our healthcare system created what felt like a fast forward button for digital health, with unprecedented growth in funding, adoption, policymaking, and national attention. As we watch the pendulum swing towards a new equilibrium, the industry will remember this year for the kick (or punch) it gave the healthcare industry to explore, iterate, and test avenues for new care models, digital experiences, and enabling technologies. We look forward to working cross-industry to make sure the best solutions stick.

Rock Health continues to meet with companies virtually and invest in the entrepreneurs bringing unique and innovative technology to healthcare. We would love to hear from you. Get in touch!

We also want to extend a special thank you to our generous members for their continued support and partnership—even through one of the rockiest years to date. Email us to learn how your organization can work with us and receive full access to our digital health market updates and databases. Subscribe to the Rock Weekly to stay up to date with the latest news and Rock Health research.

Footnotes

1Julie was referring to the deal volume at Andreessen Horowitz, rather than deal volume across the entire sector.

2 Value proposition refers to the value that accrues to the buyer directly, irrespective of the mechanism used to deliver the value, and ultimately, the reason why a buyer would purchase the product/service.

3“Investor transaction” refers to an investors’ participation in a venture funding deal. Please note that a single deal may have multiple disclosed investors, which would amount to multiple investors transactions.

4Some of these SPACs (Clover Health and MultiPlan) do not fall under Rock Health’s definition of digital health for inclusion in our funding database, but we included them given their focus on technology. Some SPACs (that fit Rock Health’s definition of digital health) are not yet publicly traded and therefore were not included in our analysis of combined market cap.