Q1 2019: The end of the digital health IPO drought comes into sight

Stay up to date with the latest headlines in healthcare technology and new Rock Health content. Subscribe to the Rock Weekly to keep your finger on the pulse of digital health.

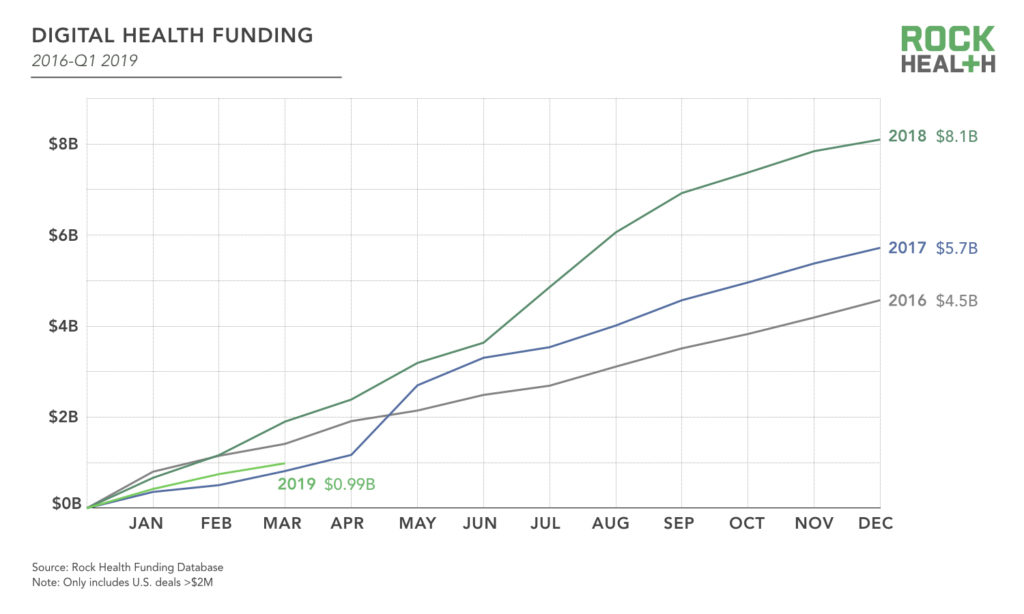

Funding for digital health companies moderates in Q1 2019

After 2018’s record-setting year in which US companies raised $8.1B, $986M was invested across 61 digital health deals in Q1 2019. That’s a about half of what was raised a year ago in Q1 2018 but roughly in line with 2017 and 31% below 2016.

Funding was stable over the prior six month period, making the middle of 2018 something of an outlier. Investors poured $3.3B into the sector at a blistering pace in Q3 2018 alone, compared to $1.2B in Q4 2018. Excluding the sharp influx of dollars in mid-2018 during digital health’s hottest summer, quarterly funding has averaged $1.4B over the past two years (Q1 2017-Q1 2019). This puts the $986M invested in this past quarter somewhat below recent trends.

Signaling ongoing, strong valuations, two new digital health unicorns grew their horns in Q1 2019. Meditation app-maker Calm hit a $1B valuation with its $88M Series B round, which it plans to use to develop new content and expand internationally. Health analytics platform provider Health Catalyst also reached a $1B valuation with a $100M Series F round. The company plans to continue building out its platform that helps hospitals link and analyze siloed databases—and is now said to be planning an IPO.

Digital health investors represent a mix of tech and healthcare expertise

The list of digital health investors includes well-known VC firms, tech companies, and enterprise healthcare companies. Andreessen Horowitz, Khosla Ventures, New Enterprise Associates, Y Combinator, Novartis, Merck, and GV all made digital health investments in Q1 2019, and have consistently been investing in the space over the past few years.

Over the previous five years, corporate venture capital (CVC) has consistently participated in around a third of digital health deals. This stands in contrast to overall (non-healthcare) US corporate venture capital activity. During the same five year period from 2014 through 2018, corporates participated in 13% to 16% of venture deals—about half the rate of CVC investment in digital health. Given that around 85% of funded digital health companies sell to enterprise, we are not surprised to see sustained corporate interest in digital health investments as a means of leveraging external innovation for growth and profitability.

Given their unique ability to leverage their clinical expertise to identify promising provider- and patient-facing innovations, health systems have been particularly active corporate investors. The most prolific provider organizations over the past five years have been Kaiser Permanente, Mayo Clinic, and Ascension—each making more than 10 investments since 2014. They are three of only 11 corporate venture arms overall whose number of digital health investments is in the double digits in that time frame (GV leads the pack with 31).

The IPO drought is over

The last IPO of a US digital health company was in 2016. The wait may be over soon. In Q1, Livongo, Peloton, Change Healthcare, and Health Catalyst were each reported to have plans to list on the public markets this year. Goldman Sachs and JPMorgan are leading all four IPOs. Livongo, Health Catalyst, and Peloton—three of the four IPO-ready companies—are on average1 10 years old with an average of $505M funds raised, each. This comports with the historical averages we’ve tracked in the past. Notably, Change Healthcare (CHC)—the fourth of the potential IPOs—was acquired in the largest reported digital health M&A deal in 2016 when it was majority acquired by McKesson for $3.3B. In addition to divesting CHC from McKesson, the IPO likely provides liquidity to Change Healthcare’s minority shareholders (which included Blackstone and Hellman & Friedman at the time of acquisition). While IPOs are critical milestones for early-stage venture investors, we’re watching closely to see how these IPOs enable companies to deliver for the patients, customers, and future public market investors they serve.

This spurt of potential digital health IPOs is happening amidst the anticipation of multiple prominent tech IPOs, with the likes of Uber, Lyft, Slack, and Pinterest getting ready to file publicly. Interestingly, in its IPO filing, Lyft specifically called out the opportunities of expanding its healthcare strategy to get patients to more appointments on time.

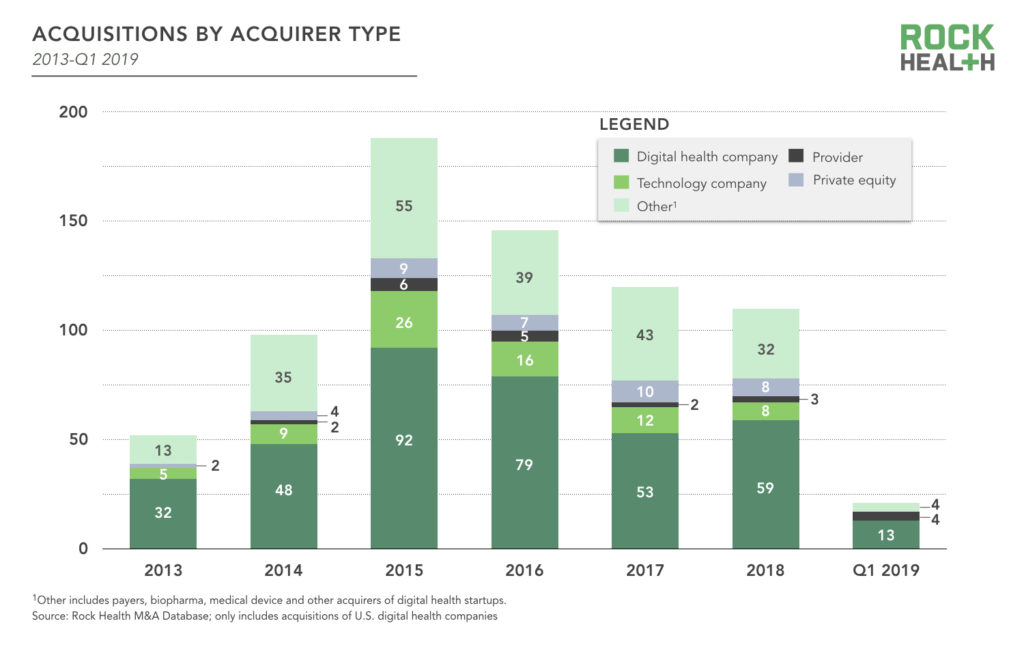

Q1 2019 was a slow quarter for digital health M&A with 21 startup acquisitions—32% below an average of 31 acquisitions per quarter aross 2016-2018. Consolidation within digital health continued with 13 startups (more than half of all M&A for the quarter) acquired by other digital health companies. Behavioral health companies were a particularly hot commodity. AbleTo, a provider of virtual behavioral healthcare acquired Joyable, which offers users coach-supported programs to overcome anxiety and depression. Meanwhile, Livongo acquired MyStrength, a company that offers evidence-based and clinically reviewed tools like cognitive behavioral therapy (CBT). The MyStrength acquisition is Livongo’s third in 18 months and representative of a trend we expect to continue—a rolling up of multiple offerings into broader solutions that benefit from a shared, platform-driven commercial channel. This is particularly true as payers and employers look for a simplified buying process among a sea of standalone offerings.

A peek into our venture deal flow

As an early-stage investor and a participant in the digital health venture investment market we’ve reported on above, we continuously review companies spanning the entire spectrum of digital health services and technologies. Time and again, we’ve seen trends in our deal flow emerge later in our funding reports.

Calling all digital health entrepreneurs with outcomes-focused business models

Through the first three months of 2019, we saw a significant portion of our deal flow focused on care coordination and monitoring of disease—about 25% of our Q1 pipeline falls into those two categories.

This focus appears to be, at least in part, a response to improved reimbursement for digital solutions, specifically remote patient monitoring (RPM) and chronic care management (CCM). In particular, the Center for Medicare and Medicaid Services (CMS) went live with three new CPT codes2 for remote patient monitoring on January 1st, 2019. These billing codes set rules and conditions under which providers may seek reimbursement for remote monitoring of physiologic parameters and remote treatment management services. There are synergies between RPM and CCM services, and these new billing codes represent an acknowledgment of the value delivered by digital health companies that provide telemedicine, chronic care management, and other forms of virtual care.

In this respect, they’re a huge step forward for the industry—largely because providers can get paid for a broader range of services without requiring those patients to travel to the doctor’s office. When executed well, this represents a win for all stakeholders, and we are seeing more companies stepping up to help providers deliver remote care.

However, we have seen a few companies whose services may overly emphasize short-term “revenue capture” under these new CPT codes (by enabling more billing)—without a commensurate level of emphasis on innovation and transformation in their RPM/CCM services. We doubt many startups are deliberately pursuing “RPM revenue capture” as a pure-play strategy. Rather, there is likely a temptation for early stage companies to chase short-term revenue in the belief that investors will reward near-term revenue more than long-term potential and vision. To the contrary, we believe in the long-run the healthcare market will harshly penalize short-term rent-seeking. That’s why we are inspired by companies who embed a long-term, outcomes-focused mindset into their business model—like our portfolio company Virta that puts 100% of its fees at risk. Our recent investment Marigold Health is another great example. Their service enables specific reimbursement codes for care coordination—built on an an evidence-based program that rigorously measures and manages outcomes around substance use relapse and readmission rates.

If you’re building a sustainable digital health business around improved health outcomes, let us know.

Footnotes

1Includes Livongo, Peloton, and Health Catalyst. Change Healthcare is excluded because it grew out of a series of acquisitions and a spinoff from McKesson. It’s difficult to compare Change Healthcare’s total funding with other VC-backed companies, but it’s a mature (33-year-old) company nonetheless.

2Current Procedural Terminology code

Partner with us!

A special thank you to our generous corporate partners for their continued support and commitment to advancing meaningful innovation in healthcare. For full access to the funding report and database, become a Rock Health partner. Get in touch to learn more about how your organization can work alongside Rock Health.

Want to stay up to date with the latest headlines in healthcare technology and new Rock Health content? Subscribe to the Rock Weekly—your ticket to being well-informed in digital health.