Glitter or gold? What the SPAC trend means for digital health

Q1 2021 is barely wrapped, and public exit announcements in digital health have already far exceeded last year’s total. The vast majority (>80%) of this activity is SPAC-related and (agnostic to digital health’s corner of the private and public markets) the SEC is taking note. SPAC talk has infiltrated digital health airwaves, news feeds, and collective conversation. Opinions abound, but we’re not satisfied with mere speculation—we wanted to understand what the data had to say. Below, we share our analysis and observations on SPACs in digital health, and explore what they mean for sponsors, entrepreneurs, investors, enterprise healthcare companies, and the digital health ecosystem at large.

Hang on to your hat, we’re talking exits.

SPAC 101: Art of the exit

Whether through access to public markets or acquisition, private companies often exit as a way to continue to grow, scale, and secure new capital. Early investors rely on exits as a path to liquidity for their funds, and public entrances offer opportunities for the broader market to participate in ownership.

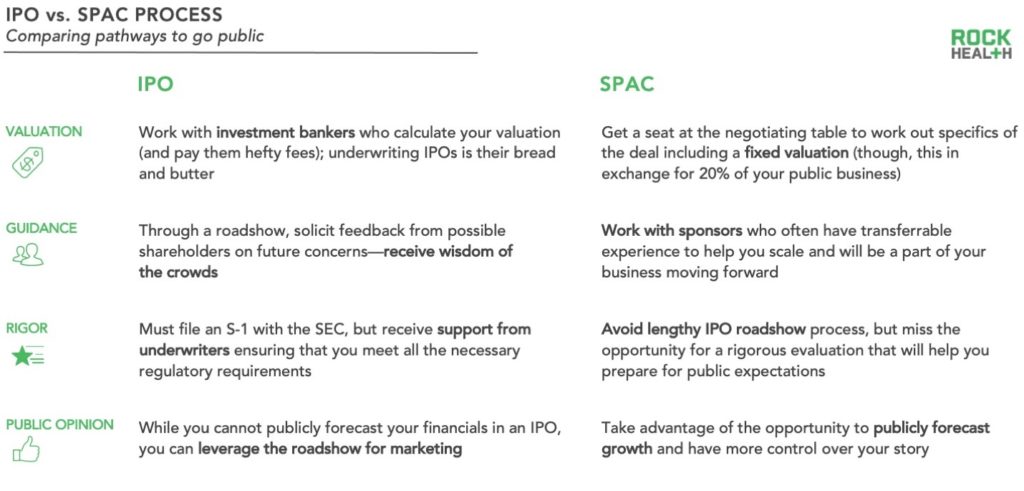

If companies want to access capital flowing through the public markets, there are a few vehicles they can consider. The classic initial public offering (IPO) is a ~6 month process underwritten by investment banks involving a lengthy investor roadshow (which can double as a marketing campaign). Direct listings involve companies simply listing existing private shares on an exchange to make them public. Another option is the recently popular SPAC, or special purpose acquisition company, which involves a public entity merging with a private company to take it public. Those public entities—the “SPACs”— are blank check companies (shell companies without operations) that go through an IPO in order to raise money, with the intent to use these funds to acquire a privately held company. They generally have up to two years to make an acquisition, and they must acquire a target with fair market value of at least 80% of the SPAC’s funds. After acquisition, the target company is traded on a public exchange.

Digital health and the case of the SPAC

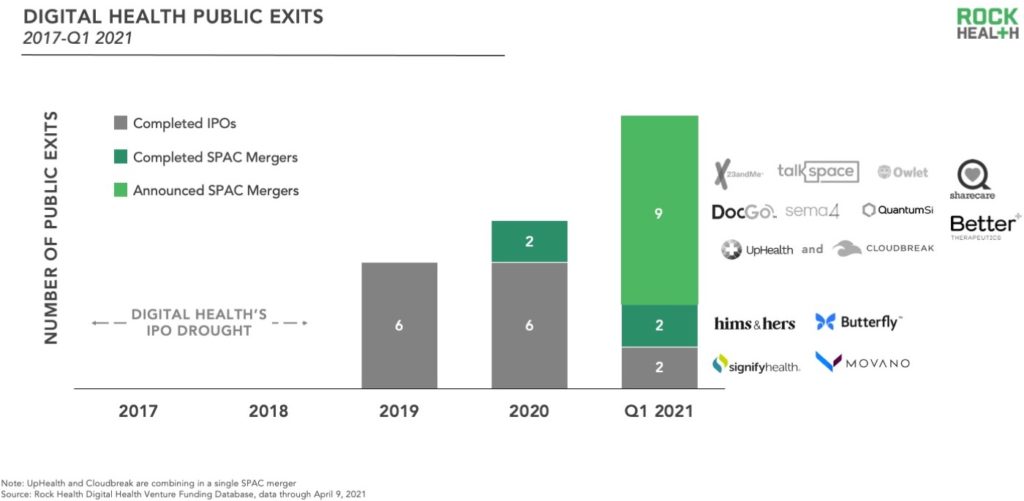

Public exit activity in digital health is center stage right now, and SPACs are grabbing the lion’s share of the limelight. The first three and a half months of 2021 have already seen more completed or announced public exits by digital health companies than in all of 2020. Digital health companies have been the target of 13 completed or announced SPAC mergers over the past 15 months, with 11 of these completed or set to close in 2021. There’s no denying it, SPACs are officially a “hot” exit vehicle for digital health companies.

There are several possible reasons for this burst of SPAC-triggered digital health exit activity:

- High growth sectors are most attractive to SPACs, and digital health as a sector is forecasting booming growth through the pandemic and beyond.

- Lingering pressure to exit pent up from digital health’s IPO drought in 2017 and 2018 could be fueling some of this activity.

- Prolonged market volatility increased the appetite for SPAC activity: SPAC deal-making is quicker than IPO preparation, so exiting via SPAC can mitigate fear that demand for an initial public offering will not be around six months from now.

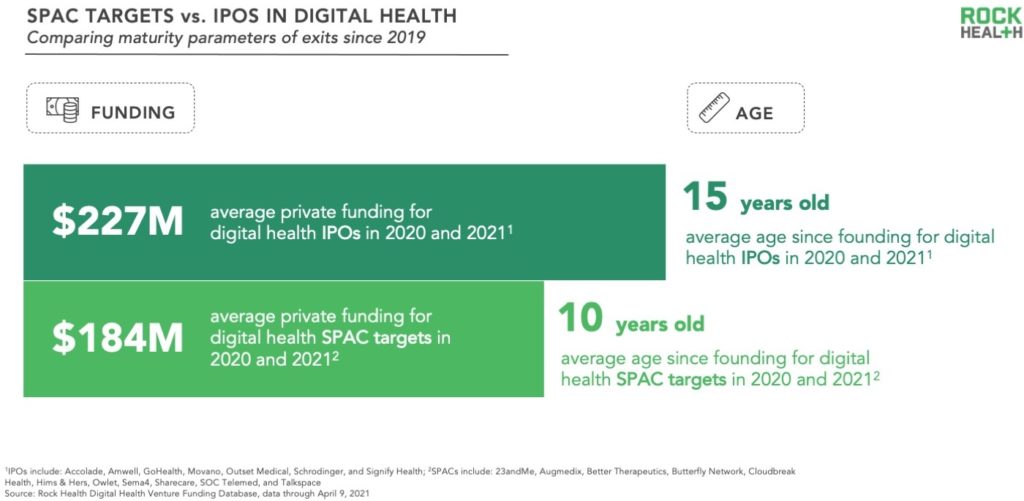

Regardless of rationale, we were curious to see if the companies exiting via SPAC share the same characteristics as those exiting through an IPO. Are both pathways seeing companies at the same readiness for exit? To answer this question, we compared the maturity of digital health SPAC targets with digital health IPOs in 2020 and 2021 through two parameters: total private funding and age of the company.

On average, the digital health companies going public through a SPAC have raised $43M less in total funding than those going public through an IPO in 2020 and so far 2021. The SPAC targets are also, on average, five years younger than the IPO class.

These data support the idea that SPACs are targeting companies at slightly earlier stages of maturity than the sweet spot for IPOs. Though, a 19% difference in total private funding is not as significant as it may first appear when less than a year ago digital health IPOs were raising an average of $187M in pre-IPO funding.

SPAC implications by stakeholder group

Which risks and opportunities are introduced by the SPAC phenomenon for digital health stakeholders—including SPAC sponsors, digital health startup founders, private investors, and healthcare enterprise organizations?

SPAC sponsors

SPAC sponsors—or the folks establishing a SPAC—tend to be business executives or private investors who have a track record of execution in their target space, usually with experience running public companies. SPAC sponsors need to attract investors to their IPO by drumming up confidence that they can choose a winning target. They also need to attract targets to their deal with money on the table and reasons to believe that they’re a worthy partner. SPAC economics can be highly attractive to sponsors, who generally receive 20% of the target’s shares in return for an upfront investment of 3-5% of the IPO proceeds. Though, with short positions in SPACs increasing, SPAC funds may be vulnerable.

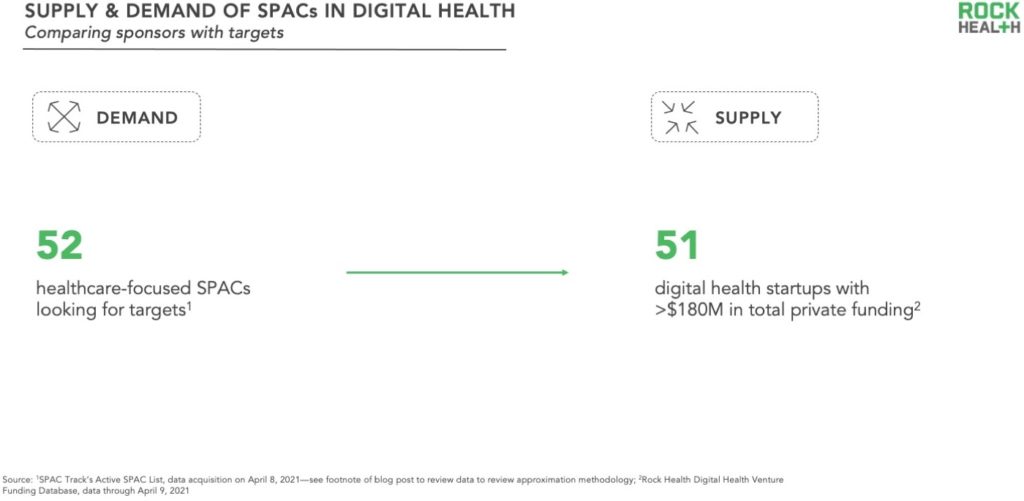

Like anything else involving buying and selling, SPAC deals revolve around the concept of supply and demand. In this case, the central question is: what is the supply of potential targets to meet the demand of SPAC sponsors facing a time-sensitive deal window?

On the demand side, we looked at the number of public SPACs which have a stated focus in healthcare. We found approximately 521 healthcare-focused SPACs, at least three of which have publicly stated an interest in digital health targets. The average trust value2 (or funds raised by the SPAC) of the 52 relevant SPACs comes to $234M. Per the 80% requirement, they’ll need to spend a minimum of $187M on a SPAC target.

To assess supply, we looked at the most highly-capitalized digital health companies, assuming that this is the cohort most likely to be planning an exit. According to Rock Health’s Digital Health Venture Funding Database, 51 digital health startups have raised at least $180M in total private funding to date (as shown above, $184M is the average capital raised by recent SPAC targets).

With approximately 52 SPACs in healthcare who could be targeting a supply of 51 capitalized, mature digital health companies, this spells a potential mismatch for SPACs staring down a limited time to acquire. Of course, it’s worth mentioning that this is an apple-orange comparison since the SPACs are not certain to target digital health nor venture-backed companies. Plus, SPACs outside of this pool of 52 may choose to target digital health companies—for example, outside of the 52 on our list, 17 additional SPACs listed healthcare among many areas of focus. The bottom line is that SPAC sponsors will have to dig deep, and it’s possible they could dip into the supply of earlier stage companies not necessarily ripe for a public entrance. The SPACs in this group contain trust values ranging from $50M to $862M—those with less in the bank will have to dig the deepest to find appropriately mature targets at the right price.

Digital health founders

With the clock ticking, SPAC sponsors are actively approaching management teams of digital health startups to work out a deal. Quick reminder—SPAC mergers always result in the target companies going public, so the most appropriate candidates for a SPAC are companies that were already considering going public through an IPO (or direct listing) before negotiating a SPAC merger. Companies that did not consider going public until approached by a SPAC team (running low on time to acquire) might be jumping the gun.

For founders considering whether to go public through a SPAC versus an IPO, each process has its own advantages. SPAC deals can allow management teams to exercise more control over their public entrance, while IPOs create more exposure to future shareholder expectations.

You shouldn’t go public in a SPAC if you’re not ready to IPO, and the right SPAC partner is critical especially for digital health. It’s not gaming. It’s not energy. It’s not cars. It’s healthcare. As a digital health platform, we have a complex and comprehensive story and the SPAC process allows us to explain it in detail. Additionally, the SPAC vehicle allows us to focus on the look forward financials and the potential growth in our model. We selected a partner with great experience in capital markets and very successful SPACs who understands our mission and business.

— Dawn Whaley, President, Sharecare

Digital health private investors

Exits are part of what keeps the world turning within the lifecycle of investment-backed innovation. Simply put, SPACs in digital health are a chance for private investors to achieve return on their investments.

With SPACs as a vehicle to earlier exit, investors have a potential opportunity to access liquidity sooner. However, the SPAC phenomenon also has the potential to create a higher appetite for (already skyrocketing) venture funding. The more competitive the marketplace for venture deal-making, the harder it is to get in on the hottest deals.

Another key risk to keep in mind with the SPAC vehicle is that it places less scrutiny on companies that want to go public, (though, with the SEC’s new guidance, we are likely to see increased diligence associated with the SPAC process). With no IPO roadshow, there is less time for public investors to rigorously examine opportunities. High profile fraud allegations have surfaced after SPAC deal announcements in a couple of cases. While new paths to liquidity are fundamentally advantageous for private investors, a few sour apples could leave a bad taste for digital health in the public markets.

SPACs allow companies to potentially go public earlier, and from an overall industry awareness perspective, more public companies is a win for digital health. But it’s crucial for these companies to ask: what is encouraging me to go through this SPAC rather than the IPO process? Do I have a strong product but just don’t have the revenue yet? If that’s the case, it’s a good path to consider. Just remember—that moment will hit when you have to do your quarterly reporting. You will have to face the music either way.

— Brent Granado, Managing Partner, Sweetwater Private Equity

Enterprise organizations

Historically, the vast majority of digital health exits are acquisitions, either by other digital health companies bolstering their strategies or by enterprise organizations entering the space. SPACs are a more seamless route to public exit in digital health, so they are a competitive exit opportunity for potential enterprise acquisition targets.

This is a wake-up call for enterprise organizations interested in entering digital health through acquisition, since desirable acquisition targets now have another path to liquidity. Healthcare enterprise organizations must move fast on deals where they have conviction, and that conviction will likely need to include appetite for higher multiples in strategic acquisitions.

Enterprise companies could also get a stake in the action by investing in the newly public digital health class. Seems like there’s an opportunity to create a digital health exchange-traded fund (ETF)—any takers?

What does this mean for the digital health ecosystem?

The SPAC phenomenon is delivering more liquidity in digital health, faster. In 2018, we graded the ecosystem as moderately bubbly attributed to “unclear exit pathways.” There had been no digital health IPOs in two years, and M&A was on a decline. It’s 2021, and we can confidently say these trends are no longer descriptive of digital health.

The fact that there are more public digital health companies is inherently exciting for the ecosystem: it heightens awareness for digital health, allows more folks the opportunity to get a stake in the action, and can help fuel the cycle of innovation. On the other hand, creating a “shortcut” to public markets for digital health companies creates a greater risk of companies that are not fully baked hitting the public exchange only to miss growth forecasts and see dramatic market cap drops.

SPACs may provide a fast pass to the public markets, but the toll is still the same. All stakeholders need to do their diligence on the fundamentals of the opportunities in front of them. This is not the time to place bets on shiny objects without looking under the hood.

Rock Health Advisory provides counsel on digital health strategy to innovators at enterprise companies through our consulting practice and membership programs. For more information, reach out to advisoryservices@rockhealth.com.

Footnotes

1To approximate this number, we counted SPACs from SPAC Track’s Active SPAC List with the following criteria:

- SPACs whose target focus included “healthcare,” “healthcare tech,” or “healthcare innovation” as one of up to three tags were included

- SPACs tagged with “healthcare” as a target focus within a longer list of non-related sectors (e.g. business services, consumer, sustainability, real estate services, media, industrial, etc.) were excluded

- Only SPACs post-IPO and currently searching were included

- SPACs with a specific geographic focus which did not include the US were excluded

- Data acquisition occurred on April 8, 2021

2To approximate this number, we averaged the trust values (from last filing) reported within SPAC Track’s Active SPAC List for the 52 SPACs determined to be relevant in footnote 1. Data acquisition occurred on April 8, 2021.