2018 Midyear funding review: Digital health déjà vu in yet another record breaking half

On the heels of last year’s record funding for digital health startups, venture dollars continue to flow into the sector at unprecedented levels. The continued upward trajectory of the first half of 2018 is not a fluke. Rather, two forces are at work: First, this sustained growth is indicative of the maturation one would expect from a stable, emerging investment sector. Digital health is increasingly defined by stalwart, repeat investors and a cohort of emerging, dominant companies backed by larger, later-stage funding rounds. Second, venture investors (across all sectors, including digital health) are deploying capital at the fastest pace since 2006.

It’s worth taking a moment to look beyond the funding momentum, where we’ve seen remarkable shake-ups and announcements across the healthcare industry. Recent acquisitions by incumbents (Optum of DaVita Medical Group and Sound Inpatient Physician Holdings, Humana of Kindred Healthcare) exemplify a growing trend of vertical integration. By owning a greater share of the care continuum, large players hope to improve efficiency and better outcomes. And a couple of healthcare mega mergers on the horizon (CVS-Aetna and Cigna-Express Scripts) just got more likely thanks to the court’s affirmative ruling for AT&T and Time Warner’s vertical merger. Time will tell if current consolidation fulfills the promise of better population health at lower cost—or if sheer size will make it more difficult for incumbents to innovate.

Is there one area in the last 30 years where the initial innovation was driven by an institution of any sort? I couldn’t think of a single area where innovation—large innovation—came from a big institution. Retailing wasn’t disrupted by Walmart, it was by Amazon. Media wasn’t changed by CBS or NBC, it was by YouTube and Twitter. Cars weren’t transformed by Volkswagen and GM—and people said you can’t do cars in startups—but then came Tesla.

Vinod Khosla, Khosla Ventures

At Rock Health’s recent Enterprise Insights Forum, Vinod Khosla noted he has never seen a disruptive innovation come from an industry incumbent. It’s no surprise, then, that newcomers to healthcare, often driven by frustration with the status quo, are taking disruption into their own hands. Over the past few months, the healthcare world waited with bated breath to hear who would spearhead the Amazon-Berkshire Hathaway-JP Morgan initiative (aka Berzerkshire Morgazon). Now, all eyes are on renowned healthcare thought leader Dr. Atul Gawande to pioneer a solution with the potential to send ripple effects across the industry. Meanwhile, Apple advanced its healthcare strategy to drive interoperability and API-driven access to health records; Google continued to make headlines touting advances in artificial intelligence; Salesforce launched new software for payers; Microsoft deepened its commitment to healthcare, onboarding additional leadership within Peter Lee’s Microsoft Healthcare team; and not to be outdone, Amazon just announced an acquisition of PillPack, making its official and much-anticipated debut into the world of prescription drugs.

Perhaps more so than in other industries, the future of healthcare startups is inextricably linked to the strategies of large, enterprise-scale healthcare players—as customers, partners, investors, and even potential acquirers. Todd Pierce, a board member of Dignity Health and Rock Health, recently noted that “adoption and uptake on the buy-side is killing innovation.” His greatest worry is healthcare incumbents adopting new solutions too slowly to sustain startup growth. Rock Health’s research has examined this topic—and the likely path forward. We’re excited to continue to track the expected—and surprising—partnerships as they emerge.

Want access to our comprehensive analysis of this half’s funding, along with every tracked digital health deal since 2011? Become a Rock Health partner.

Looking back on digital health venture funding in the first half of 2018, here are five key takeaways you need to know:

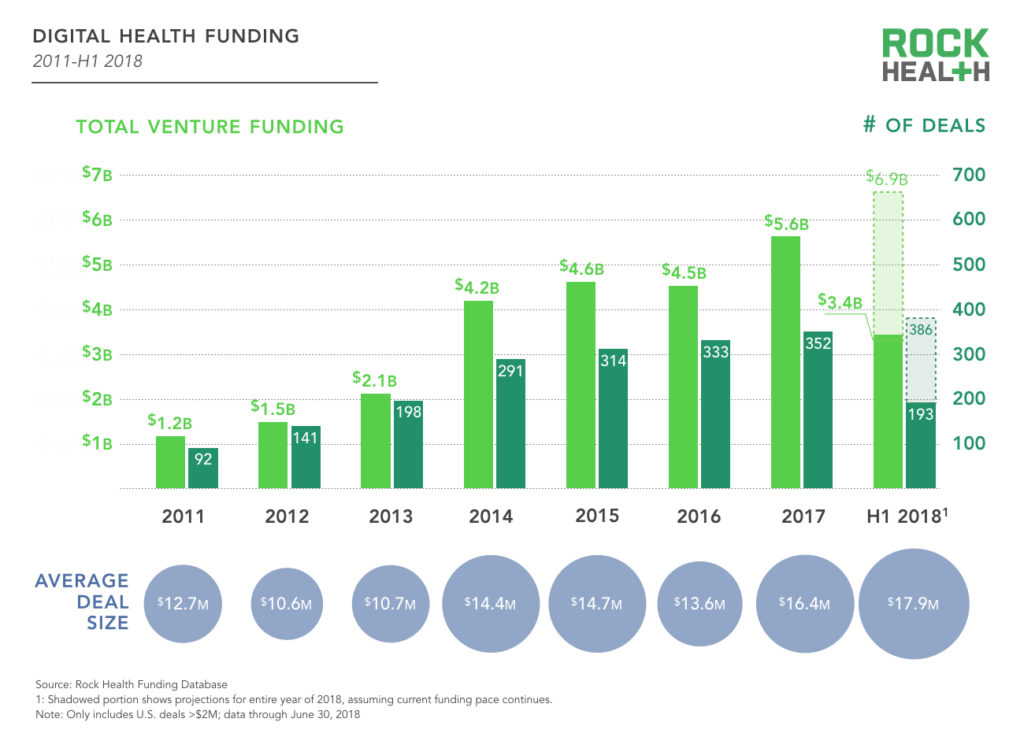

1. A capital-rich market, coupled with a large number of maturing digital health companies, leads to another record first half with $3.4B in digital health funding.

From January 1 through June 30, 193 digital health deals closed for a total of $3.4B invested. If funding continues at this pace, 2018 will surpass 2017 for both dollars raised and number of investments. Rather than concentrating capital in fewer startups, investors are betting on more companies with larger deals. Consequently, the average deal size significantly increased to a record $17.9M.

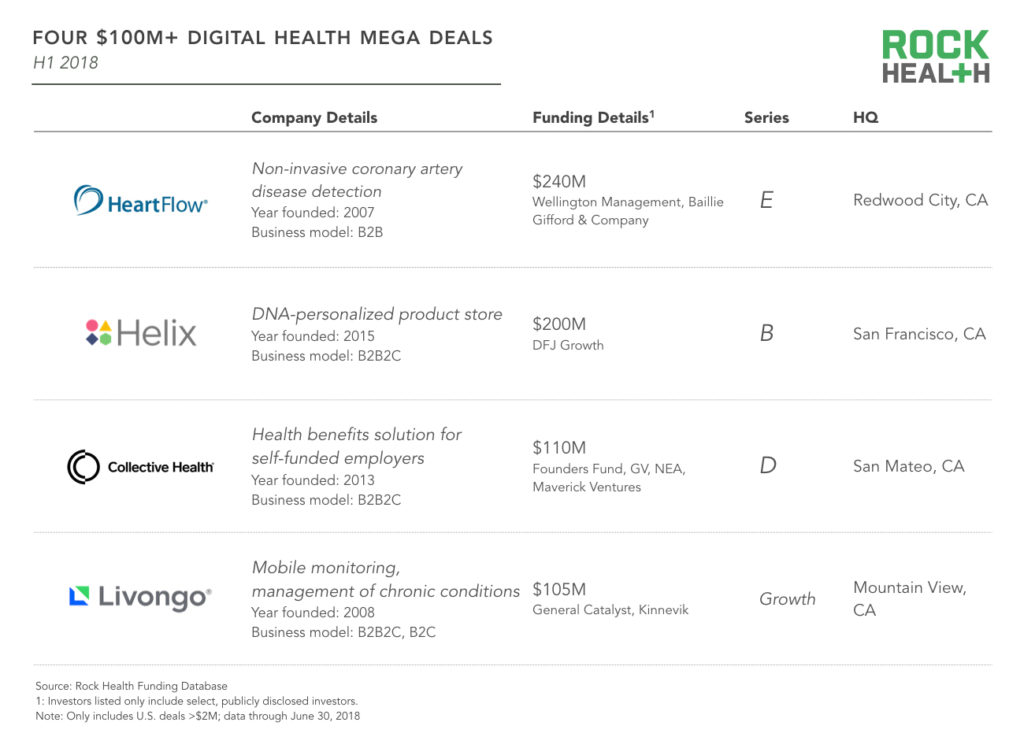

As the space matures, more later stage companies are raising sizable rounds. In the first half of this year, four companies raised mega deals over $100M. Collectively, these deals represent about one-fifth of total funding so far in 2018, and were all raised by companies in the Bay Area.

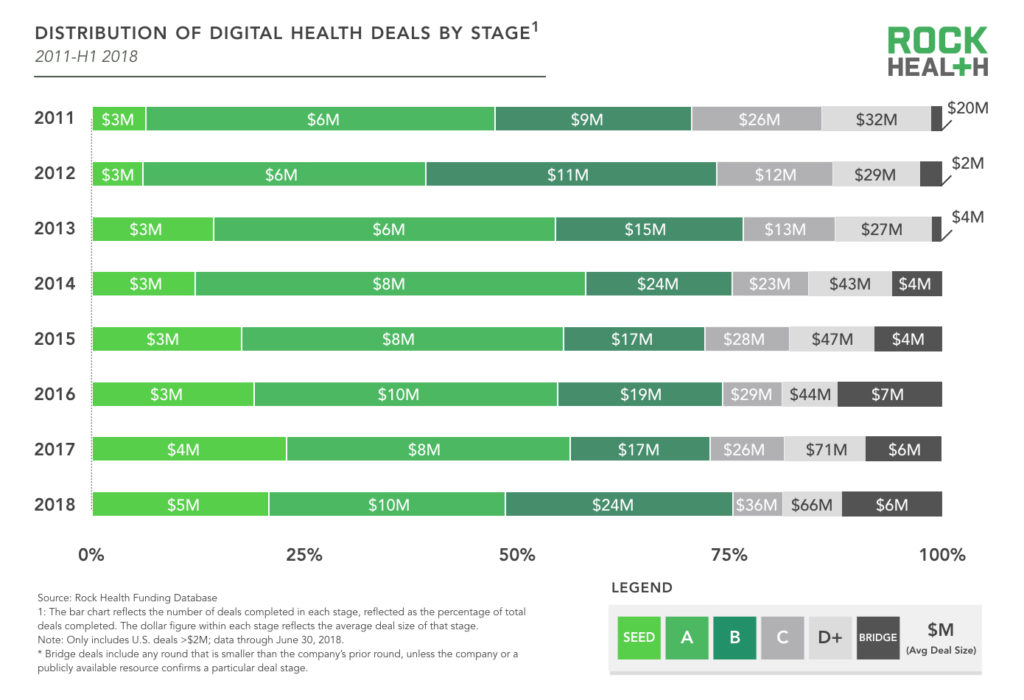

It’s not just the big deals getter bigger. Indeed, across almost every stage, the average deal size has increased since last year. Additionally, the percentage of seed stage deals contracted from 23% in 2017 to 21% in H1 2018, while the number of B rounds grew.

2. Digital health rallies for evidence-based product validation.

Record levels of dry powder in venture and private equity funds create upward pressure on valuations and deal sizes across all sectors. But, looking beyond the numbers, it’s clear that growth in deal size within digital health is also a result of the steady maturation of a young sector in which digital health companies are increasingly hitting key validation milestones—and are being rewarded by investors for it:

- Virta, which released one-year results from its clinical trial, raised $45M in Series B funding

- Propeller Health raised $20M in Q2 to expand its longstanding commitment to clinical research

- Omada Health, which has 10 peer-reviewed studies demonstrating the efficacy of its digital health programs, received full recognition from the CDC in June—and has raised over $127M in total

- Pear Therapeutics closed a $50M Series B months after the FDA approved its app to treat substance abuse

- Akili Interactive Labs closed a $55M Series C round in anticipation of FDA submission of its video game-based digital therapeutic candidate for ADHD

Though the stories of company progress and impact are heartening, one saga continues to cast a shadow over the digital health ecosystem. David Shaywitz characterized Theranos’ downfall—and Elizabeth Holmes’ recent federal criminal charges—as a “hit to hope.” In our view, this story instills a “back to basics” mentality for digital health companies and investors who wish to avoid repeating history: scrutinize data and evidence, and seek appropriate validation.

More companies are pursuing validation at an earlier stage and investors have elevated their expectations, creating a competitive environment based not on hype, but on proven outcomes. This greater “demand” for validation comes at a time when the FDA is working to streamline its review process for digital health companies via the pre-cert program. The agency is even considering input on rules that account for the specific needs of AI and machine learning algorithms. (We are gathering feedback for the FDA on this topic now!)

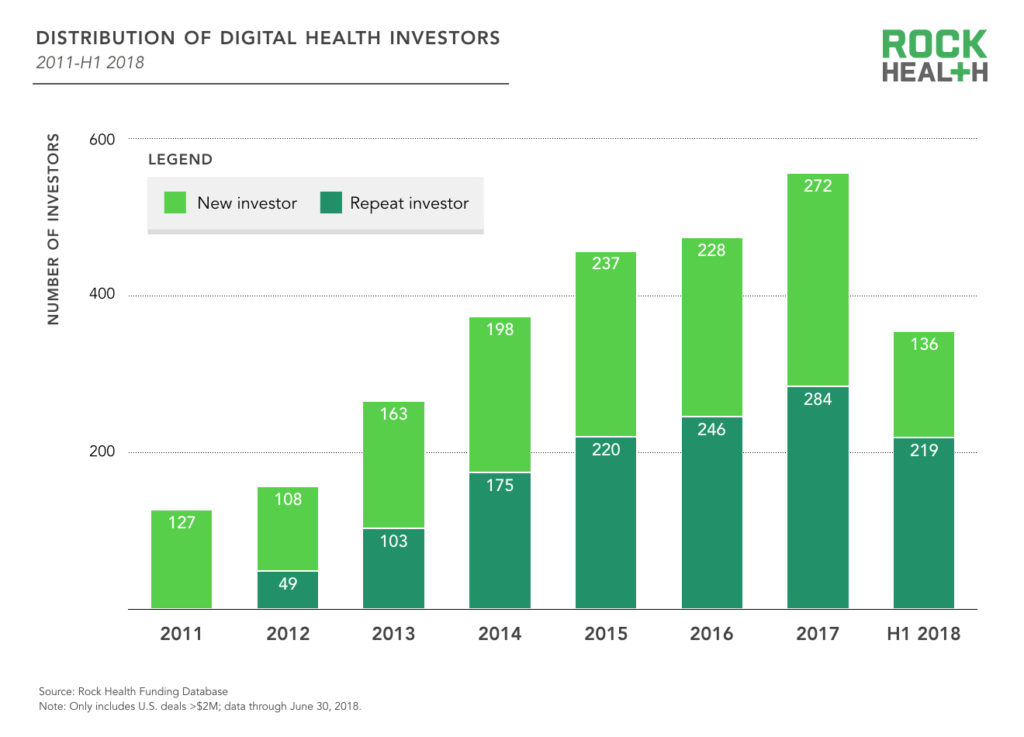

3. No longer tourists, investors are sustaining their commitment to the digital health space.

From 2011 through 2015, there were more investors making their first investment in digital health than there were investors returning to the space. In previous years, we questioned whether potential “tourist” investors, attracted by the hype and excitement surrounding digital health, would develop the conviction, patience, and expertise required to succeed in healthcare investing. The data are definitive—since 2016, there have been more repeat investors than new investors in digital health, and the spread between the two is growing.

Sixty-two percent of investors in H1 2018 had already participated in at least one digital health deal since 2011; last year, repeat investors represented 51% of total investors. This commitment likely contributed to the later-stage, larger deals completed this half as investors participate in follow-on rounds for their earlier investments.

There are also signs of healthcare incumbents and loyal digital health investors doubling down on investments in digital health. Founders Fund, the most active investor in digital health so far this year, has already made eight investments. Furthermore, Optum Ventures has begun investments from its new $250M fund—including co-leading a $13.8M Series B for specialty eConsult platform Rubicon MD—to support digital health companies that improve healthcare delivery, payment reform, and consumer-centric care. Bessemer Venture Partners, a prolific digital health investor, just launched a new $10M seed-stage fund to invest in AI-driven technologies for healthcare, in part inspired by Bessemer’s participation in Qventus’ latest $30M Series B round.

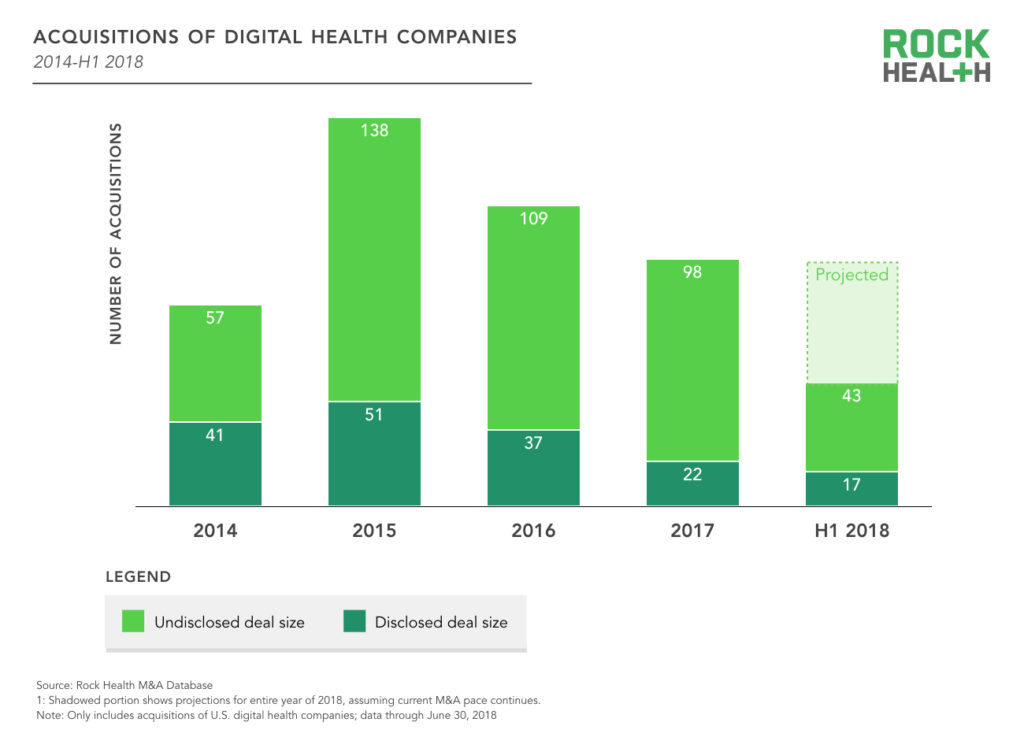

4. Digital health exits remain sluggish—though the problem isn’t unique to digital health.

Overall, M&A activity during H1 2018 is on-pace with 2017 with 60 disclosed digital health acquisitions. The sector is still down from the height of 2015, but this isn’t unique to digital health. PitchBook and NVCA reported that the startup community at large had the lowest Q1 exit value and count since 2013.

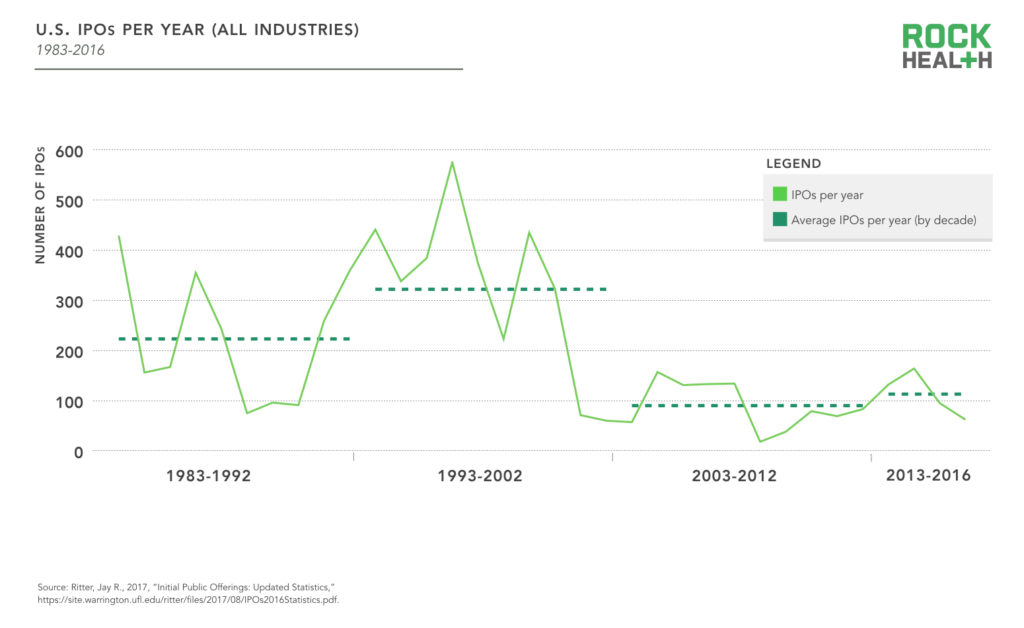

In April, Venrock released its second annual healthcare prognosis: Health Catalyst, followed by Grand Rounds, were voted the most likely next digital health IPOs. But an IPO drought has persisted since 2016 when iRhythm Technologies went public on October 20. The drought, however, is not due to a shortage of highly-capitalized companies. Historically, digital health companies have averaged $136M in funding from venture capitalists before going public—and there are currently 13 private digital health companies that have raised over $200M since 2011 that are still active today. But with greater access to capital, companies are staying private longer (for a median of 8.2 years, across all sectors).

On the surface, it may seem as though the digital health sector is bucking recent IPO trends. Recode noted that this spring was “a boon for the tech IPO,” and biotech companies are going public in 2018 at “a blistering” pace. However, taking the long view, IPOs are not nearly on par with the IPO boom of the 90s. By one measure, the propensity to list is now half of what it was 20 years ago. There are fewer publicly listed companies today than 40 years ago, and the number of IPOs per year have lagged since the dot-com bubble burst in 2002.

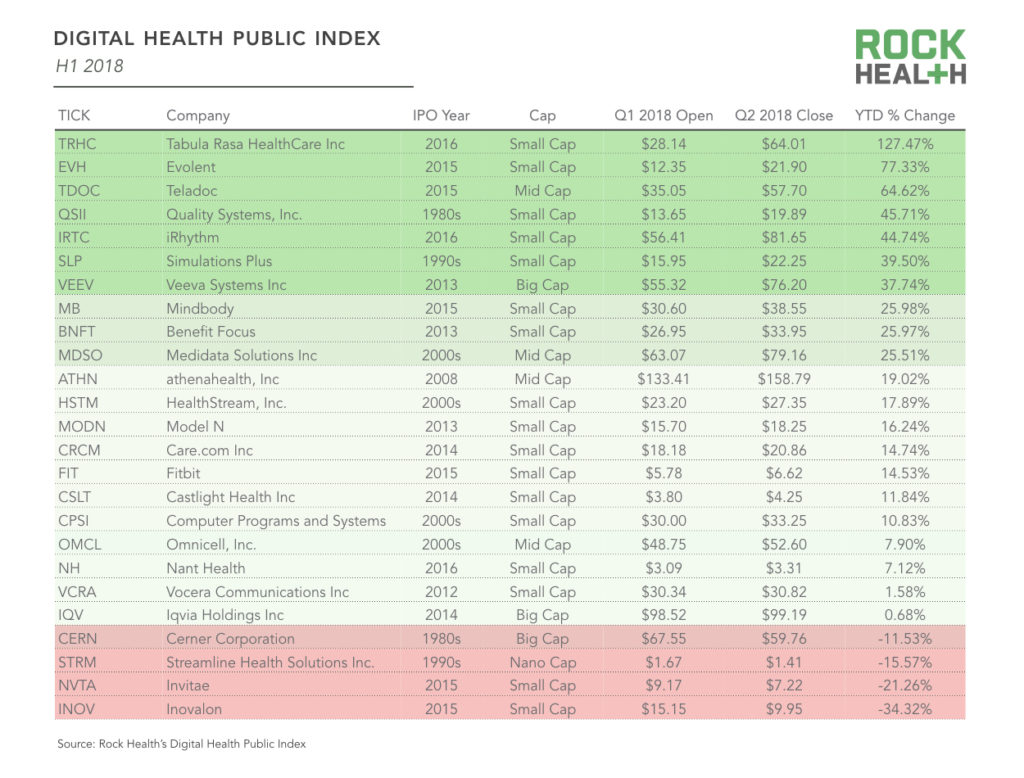

Despite a dearth of digital health IPOs, The Digital Health Public Company Index has had an outstanding run. In H1, stock prices were collectively up 22.2% from 2018 opening (compared to the S&P 500 Index which is only up 1.7% year-to-date). The companies with the biggest gains in stock price include Tabula Rasa HealthCare (up 127.5% YTD), Evolent Health (up 77.3% YTD), and Teladoc (up 64.6%). Only four of the 25 companies on the index are down YTD.

Digital health seems to be mirroring this longer-term trend of investors relying more heavily on M&A for liquidity “while IPOs have floundered.” As a result, industries overall—including healthcare—tend to be more concentrated with larger, older companies. With a plethora of potential acquirers (and an abundance of private capital), digital health startups may be offered a lucrative acquisition before they have reached predictable revenue, scale, and a growth trajectory to function as independent, public companies.

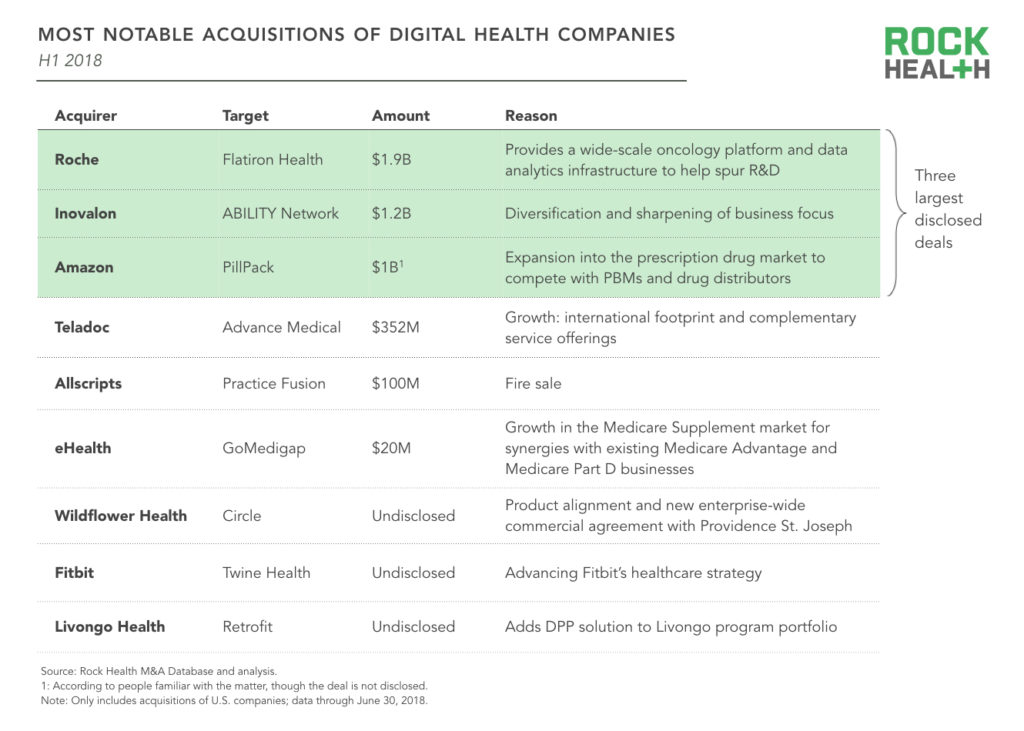

M&A makes sense for this emerging sector: digital health startups create novel, complementary innovation that incumbents cannot easily replicate. Case in point: Amazon just acquired online pharmacy startup PillPack for nearly $1B—PillPack’s digital pharmacy solution with nationwide contracting and licensure (including supply chain, home delivery, and medication adherence elements) allows Amazon to enter the prescription drug space. Roche’s acquisition of Flatiron in February (and its subsequent definitive merger agreement with Foundation Medicine in June) reinforce this view. It is likely many startups—rather than going public—will find their assets to be more valued by a healthcare incumbent, another larger digital health company, or a non-traditional player moving into the healthcare space. We can expect more acquisition rumors—like those around GoodRx, which offers people discount cards for drugs.

Digital health startups are most likely to be acquired by other digital health companies, which make up half the acquirers in 2018 M&A transactions. Flush with capital—and a desire to grow fast through product extensions and new hires—it’s not surprising to see a great deal of M&A activity amongst this group. There has been an influx of telemedicine acquisitions this year. So far, telemedicine companies TruClinic, Reach Health, Avizia, and Advance Medical were each acquired by larger digital health companies. With greater Medicare reimbursement and states passing new telehealth regulations, companies may be seeking to geographically expand their customer reach.

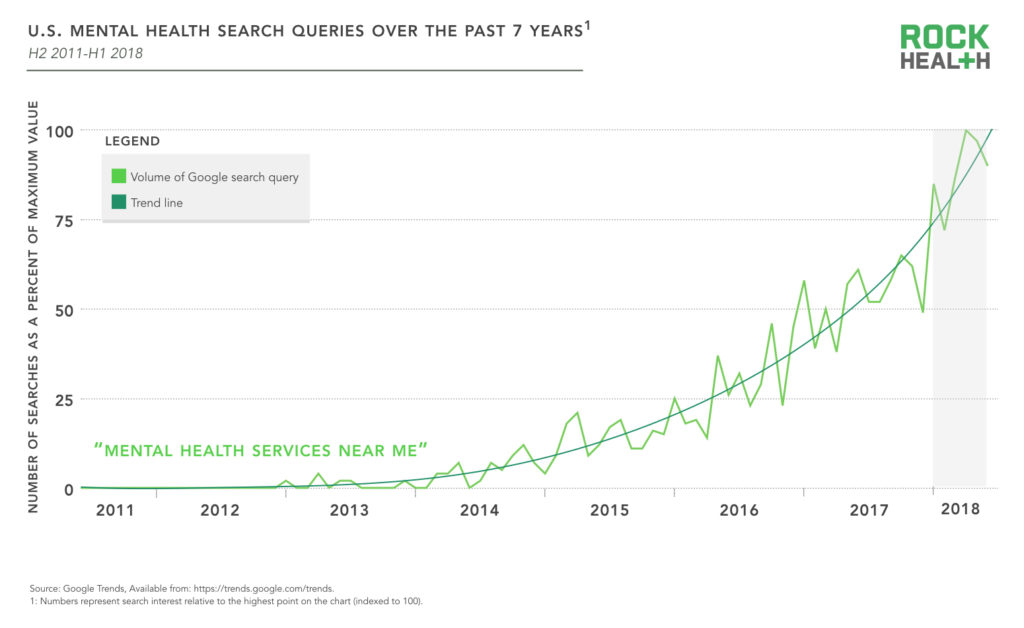

5. With national attention turning to mental health issues, technology-driven behavioral health solutions have received more funding than ever.

The high-profile suicides of apparel icon Kate Spade and celebrity chef Anthony Bourdain have spurred a tragic but important national focus on mental illness—and the stigma and access issues that leave many unsupported. In fact, the search query “mental health services near me” hit an all-time high on Google’s search engine, signaling demand for more accessible and on-demand services.

Fortunately, emerging digital health companies are finding more cost-effective, scalable ways to reach affected people. Behavioral health startups received more funding this half than in any prior six-month period, with a cumulative $273M for 15 unique companies (nearly double the $137M closed in H1 2016, the previous record half for funding of behavioral health companies). Of these 15 companies, more than half have a virtual or on-demand component.

With mental health apps, patients can receive a response instantaneously (especially important since securing a psychiatric appointment can take nearly 25 days). Apps offer a highly accessible, cost-effective service for people seeking to supplement face-to-face therapy—and can reach those who are uninsured and unable to afford traditional mental healthcare, or may be deterred from going to a traditional provider. For instance, behavioral health app maker Ginger.io reports seeing “significant traffic outside of the traditional 9-5,” and its machine learning algorithm can detect when a patient should be triaged to clinical care for therapy or psychiatry.

These approaches are not only convenient and scalable—they are also effective. Multiple studies demonstrate the effectiveness of online programs that use cognitive behavioral approaches, and companies are leveraging this literature when developing their solutions.

This half, Woebot, “your charming robot friend who is ready to listen, 24/7,” secured $8M, and leverages a machine learning chatbot to improve access to mental health services. Other companies, like Lyra Health (which raised a $45M Series B in May) and Regroup Therapy (which raised a $5.5M round in May), facilitate a human-to-human connection, pairing users with providers in-person or remotely.

Investors are supporting mental health solutions across the spectrum, from prevention to treatment. For instance, Calm.com and 10% Happier (which raised $27M and $5M, respectively) focus on general mental well-being via meditation. Meanwhile, Pear Therapeutics, which received FDA clearance for its digital therapeutic for substance use disorder, raised a $46M Series B.

Looking forward

We expect the momentum of the first half of the year to carry throughout 2018. Venture investment is on pace for another record-breaking year in terms of total funding, number of deals, and average deal size. With a robust and well-capitalized startup pipeline, and new enterprise entrants with big ambitions to grow their healthcare capabilities, we anticipate more exits in the near future.

To continue the discussion, join us for our seventh annual Rock Health Summit, a two-day digital health conference in San Francisco that brings together over 650 diverse minds from technology, medicine, policy, and beyond to tackle healthcare’s most challenging problems through interactive programming. Early bird tickets are on sale now—snag yours before they sell out!