2023 Q1 digital health funding: Investing like it’s 2019

2023 started off with the hallmarks of a rebound year. While Q4 2022 signaled the tail end of the digital health funding cycle, January and February funding numbers began to suggest that sector investment was slowly but surely inching back upwards. Inflation was easing ever so slightly. Investors were rediscovering their confidence and launching new projects, signaling optimism in the sector.

However, March’s titanic news—the collapse of Silicon Valley Bank, the seizure of Signature Bank, Moody’s downgrading of bank credit ratings, another Fed rate hike—was a stark reminder that the choppy waters of 2022 aren’t over yet. And with the IPO market still closed and regulators a-chompin’, digital health startups are holding on (to fundraising opportunities), hanging tight (to liquid assets), and making the most of existing resources (because cash may be worth less soon).

In this piece, we’ll review the venture, banking, and policy waves breaking within digital health. We’ll also talk about how the volatility of today’s regulatory landscape and financial market feels different based on the ship you’re in—with smaller startups and funds facing the rockiest passages.

Q1 inches forward, but 2023 funding may drop below 2019 levels

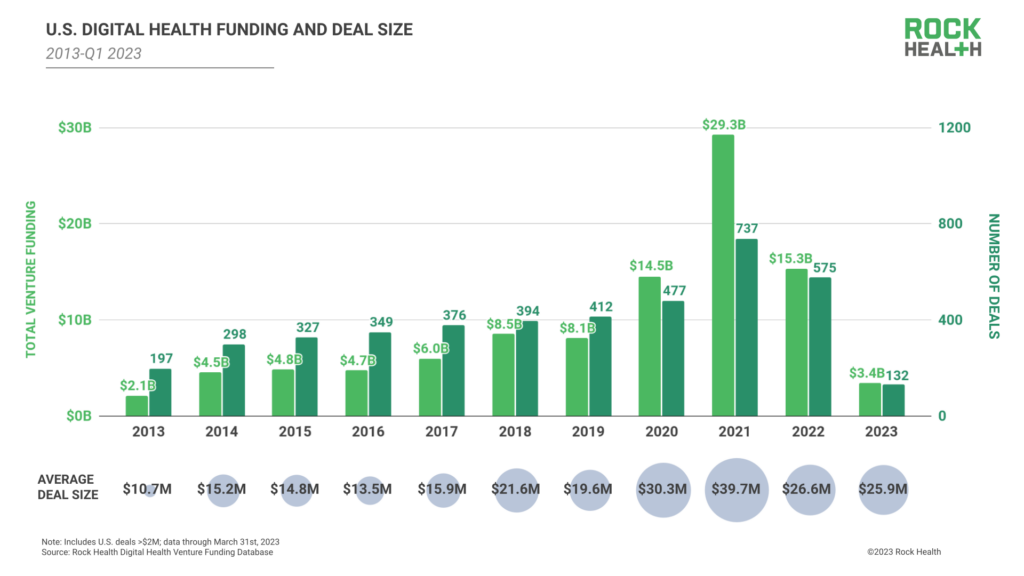

Q1 2023 U.S. digital health funding closed with $3.4B across 132 deals, with an average deal size of $25.9M. While this quarter exceeded both Q4 2022’s $2.7B and Q3 2022’s $2.2B funding pots, Q1 isn’t enough to signal a new “bull run.” If funding for the next three quarters matches the average funding across the prior three quarters, 2023 is on pace for the lowest level of annual funding since 2019. The truth remains that the founder-friendly market of 2021 and early 2022 has tilted sharply toward investors.

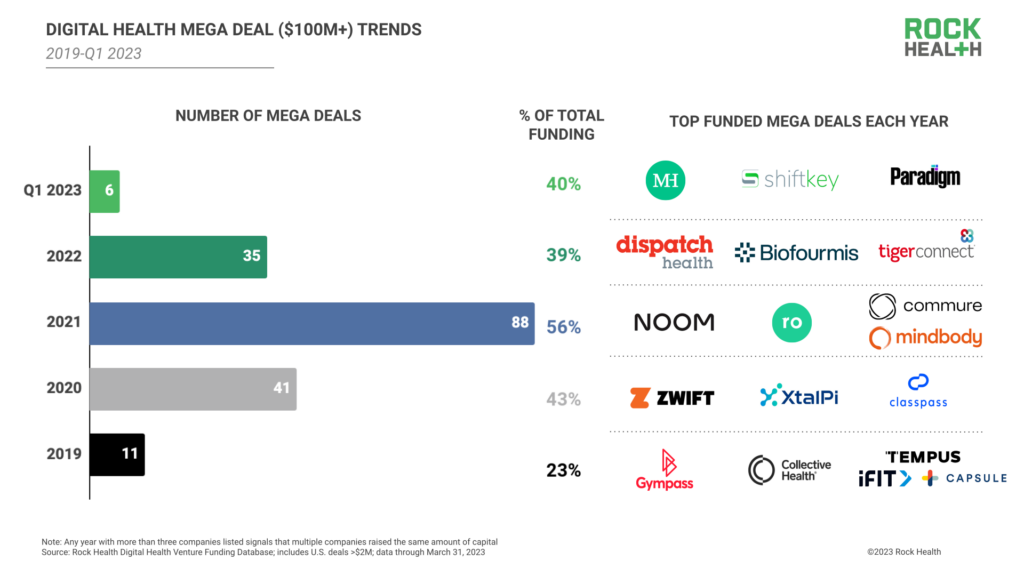

Notably, within its $3.4B raised, Q1 2023 saw heavy representation of mega deals. After only six digital health raises over $100M across Q3 and Q4 2022 combined, Q1 2023 logged six megadeals from Monogram Health ($375M), ShiftKey ($300M), Paradigm ($203M), ShiftMed ($200M), Gravie ($179M) and Vytalize Health ($100M)—accounting for 40% of the quarter’s total digital health funding.

The fact that six deals nearly equaled the funding brought in from the quarter’s 126 others signals that the current market is being driven by a select group of large, high impact transactions. Not to mention, many of these mega deals are being catalyzed by digital health’s deepest-pocketed investors—see ARCH Venture Partners and General Catalyst’s co-incubated startup Paradigm raising digital health’s largest ever Series A round ($203M) in January. Overall, Q1’s mega deal upticks don’t necessarily foreshadow a sector rebound. Rather, they indicate that the sector’s more established players and investors are trying to find their sea legs in this market, selectively deploying those dry powder reserves they’ve been stockpiling since 2021 into teams and projects they know.

Silicon Valley Bank’s collapse: Q1’s reckoning moment

Any funding momentum from January or February was put on pause following March’s collapse of Silicon Valley Bank (SVB), a major lender to startups, including those in digital health, over the last 40 years. We won’t rehash the factors that led up to the bank run and SVB’s acquisition by First Citizens Bank, but we’d be remiss not to discuss the impact of these events heading into the rest of 2023.

Digital health startups and funders of all sizes were depositors with Silicon Valley Bank. SVB’s collapse nearly precipitated a liquidity crisis in the sector, and concerns circulated that startups might need to engage in distressed debt buys or raise emergency bridges—possibly with “lender-friendly” terms or at slashed valuations—in order to secure working capital. While the initial threat of asset loss was felt across a broad range of SVB’s depositors (just ask Etsy and Roku), it’s worth noting that not all digital health startups carried the risk burden equally. Startups with well-established investors were more likely to have the assurances of cash floats and level-headed perspectives from advisors who have been around the block a few times, while those with greener syndicates were left unsure of whether their own funders could even weather the storm. After seeing their investors operate in crisis mode this March, several founders may feel compelled to re-evaluate their cap tables and possibly move forward with different investors for future raises.

Startups were left with another conundrum after SVB’s collapse—which banking institution to choose next. SVB was known to offer startups loans during high-growth periods and took on companies that were too early to demonstrate product-market fit. While late-stage startups likely have the capital and credit requirements to bank with high street institutions, nascent teams or those based outside of the US will need to turn to more restrictive and expensive alternatives to establish financial operations and secure loans. It’s hard to overstate just how supportive SVB was of the startup ecosystem, and the full ramifications of its closure and acquisition on technology innovation may not be felt until quarters later.

On the funding front, we expect that SVB’s collapse will contribute to the next few quarters of startup financing (debt and equity) moving more conservatively. Some companies may look for buyers as a result; in a small survey of digital health founders published by HTN in Q1 2023, 44% of respondents reported having less than 12 months of cash runway left. Other founders may feel pressured to fundraise due to inflation concerns, worrying that cash raised a few months in the future might not go as far as it could today. But one thing’s for certain: founders will be more intentional about how they build their investor and advisor communities. Because in rocky times like these, it matters who’s in your corner.

All quiet on the exit front

Another critical element that impacted digital health’s Q1 performance was the (still) closed IPO market. After a barren 2022, Q1 2023 logged another quarter with zero digital health IPOs. Digital health stocks started 2023 trading almost 50% lower than they did at the start of 2021, pushing some recently-exited players like Pear Therapeutics to explore going private. No later-stage digital health players felt compelled to venture into IPO territory this quarter, fearing that the market would yield bottom-barrel issue prices.

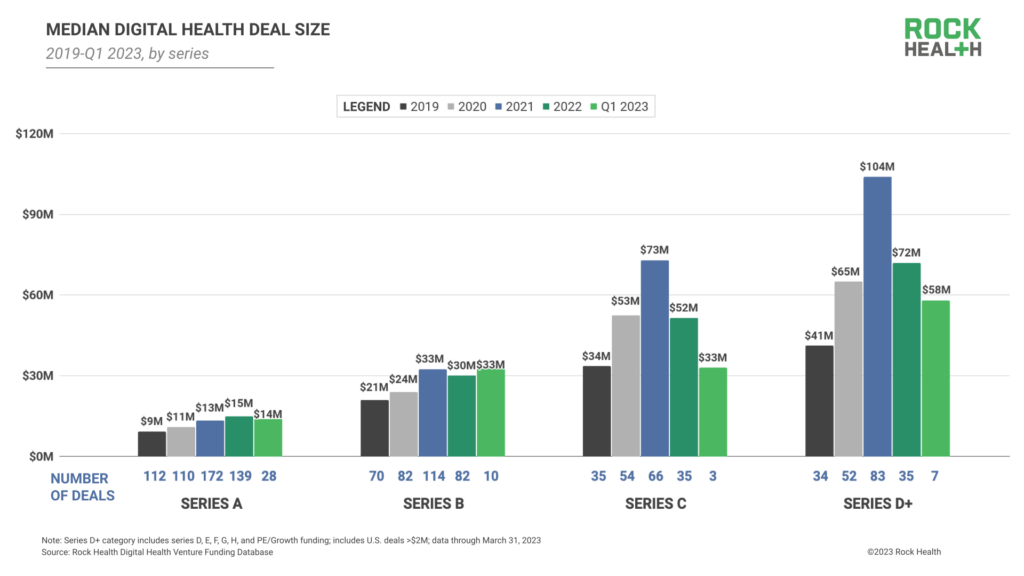

For late-stage digital health startups stuck in pre-IPO limbo, the time is likely approaching to re-engage investors for cash infusions (one contributing factor to the aforementioned mega deal boom). Q1 2023 saw an increase in the proportion of Series D+ investments relative to other deal stages compared to 2022, although median Series D+ deal size dropped to $58M, down from 2022’s $72M.

Private funders aren’t exactly welcoming late-stage startups with open arms; in fact, many of their deal terms include valuation adjustments and operational revamps to ensure responsible resource utilization. In December 2022, healthcare data startup Komodo Health raised $200M alongside a restructuring plan that laid off 9% of its workforce. In January, hybrid care provider Carbon Health closed a $100M Series D while also trimming its RPM and chronic care divisions and completing its second round of layoffs.1 That same month, nurse staffing solution Shiftkey announced its $300M raise, accompanied by a quartet of new executives. Connected fitness startup Tonal is rumored to be pursuing private funding at a $200M-$300M valuation, a nearly 90% decline from the $1.9B valuation it floated back in September 2022.

For late-stage players that aren’t turning to the private markets, there are other ways to seek out cash. Startups can pursue alternative exit pathways (e.g. becoming a Public Benefit Corporation) or turn to good ole’ debt financing. Others might sell parts of their business in exchange for capital infusions like 98point6, or sell off their assets as part of a broader shutdown like Mindstrong. Interestingly, these discards of partial acquisitions and company closings (think: tech assets, laid-off employees) may be the seeds and nutrients that will grow into the next generation of digital health startups and solutions. We’ll be watching closely to see if any of these assets turn to treasure, where they take hold, and if the market environment is tenable enough to support their growth.

Responding to regulatory developments

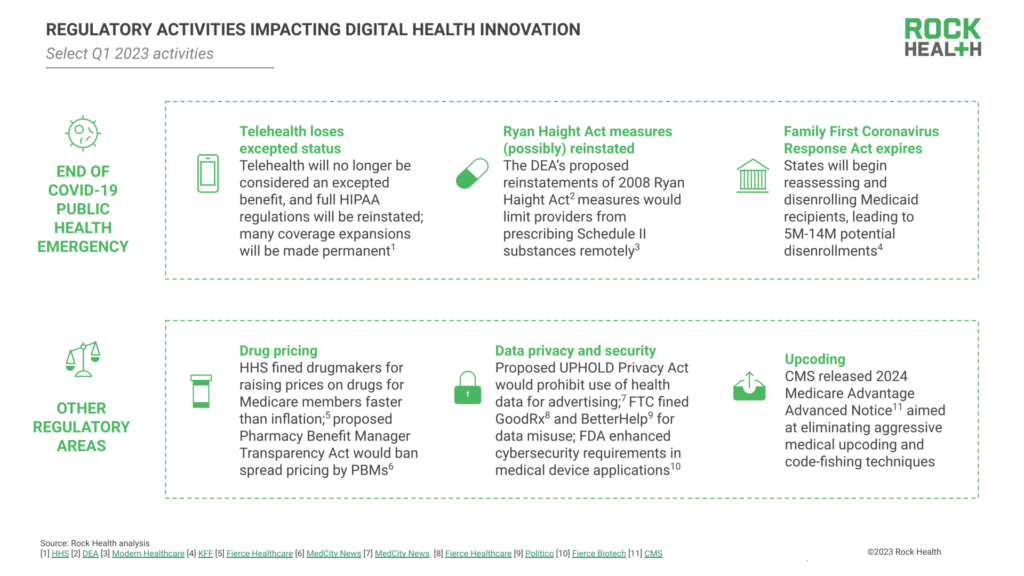

If circumstances weren’t treacherous enough, digital health startups are bracing for impending regulatory changes. In Q1 2023, an acronym soup of federal agencies (FDA, CMS, DEA, FTC) announced preliminary steps and timelines for refining policies across digital health. These revised guidelines have far-reaching impacts, affecting telehealth reimbursement, controlled substance distribution, healthcare service pricing and rebates, and patient data management.

Top of mind is the announcement to end the COVID-19 public health emergency (PHE), which is slated to expire on May 11, 2023. In the realm of telehealth delivery—perhaps the biggest area of healthcare expansion during the pandemic—telemedicine will officially lose its status as an excepted benefit2 and certain federal penalties for HIPAA non-compliance of telehealth platforms will be reinstated. However, many pandemic-era telehealth reimbursement expansions will be made permanent or extended through 2024, including CMS coverage of audio-only telemedicine visits, which has been extended through next year.

In alignment with PHE’s conclusion, other government bodies are rolling back pandemic-era measures. State agencies are beginning to unwind expanded Medicaid coverage in conjunction with the expiration of a 2020 federal provision requiring continuous enrollment. As states resume disenrollments, anywhere from 5 to 14 million Americans stand to lose Medicaid coverage and associated benefits, with the hardest-hit populations being low-income youth and working individuals without employer-sponsored plan access. The PHE’s expiration also catalyzed the Drug Enforcement Agency (DEA) to propose reinstatements of Ryan Haight Act prescribing measures suspended during the pandemic. The measures would require in-person visits for prescribing Schedule II substances including OxyContin and Adderall, while Schedule III-V substances like Ambien and buprenorphine (a medication used to treat opioid use disorder) could only have initial 30-day doses prescribed virtually.

As we approach the horizon of post-pandemic healthcare regulation, certain digital health startups that relied on COVID-era measures as business catalysts will be forced to adjust their modi operandi. In response to the DEA’s proposed reinstatements, Cerebral closed its medication-assisted treatment program for opioid use disorder and laid off 15% of its staff, while virtual clinics prescribing ketamine found their operational pathways in limbo. However, these new regulations also open doors for new innovation opportunities, making room for digital programs supporting Medicaid navigation and new startups that can streamline compliance practices.

Beyond PHE-related measures, Q1 saw regulators make moves in other healthcare focus areas. Relevant to drug pricing, HHS fined drug manufacturers for hiking medication prices faster than the rate of inflation, while Congress proposed legislation to spread pricing in Medicaid programs. In terms of data privacy and security, Congress introduced the Upholding Protections for Health and Online Location Data (UPHOLD) Privacy Act to regulate companies’ use of health data, the FTC settled investigations into BetterHelp and GoodRx with hefty fines, and the FDA enhanced cybersecurity requirements in regulatory applications for medical devices. Finally, on the billing and coding front, CMS issued its 2024 Medicare Advantage Advance Notice to root out aggressive upcoding practices.

While regulatory changes might seem like another boulder in 2023’s rocky path, we’re optimistic about the protections these policies and procedures will provide for healthcare consumers and the ways they’ll foster sector longevity more broadly. While some may mourn the Wild West of 2021 digital health—unbridled demand, lax rules, cheap money—the next era will foster digital health entrepreneurship and intrapreneurship with guardrails that guide innovation rather than stifle.

Waiting for daybreak

There’s no denying that Q1 2023’s economic conditions, bank scares, and regulatory changes have digital health startups of all sizes nervous, whether they’re trying to raise their next funding round or waiting for the right time to exit. Either by personal choice or business requirements, we are likely to see some startups give in to turbulent waters—seeking out buyers or shutting down completely over the next several months. Those that make it to daybreak (though we can’t predict exactly when that’ll be) will come out with patched up ships and resilient mindsets. So grab the right crew and compass. We’ll see you out there.

Footnotes

- Carbon Health operates physical locations, so Rock Health does not track the company in our digital health funding databases.

- Excepted benefits do not count toward an individual’s insurance coverage limit.