Q1 2022 digital health funding: Staying the course in choppy waters

Coming off of 2021’s breakthrough year in digital health funding, it’s already clear 2022 has its own story to tell. Supply chain and energy disruptions, market corrections, and the Russian invasion of Ukraine are new variables entering public and venture funding equations—changing the calculus for startups and investors who extrapolated a path based on sector activity in 2021.

In this piece, we’ll review Q1 2022’s digital health venture funding trends and public market performance, while diving into emerging hotspots. We know we’re just getting settled into 2022, but if this quarter signals anything, it’s that the next nine months won’t be easy to predict.

Q1 2022 by the numbers

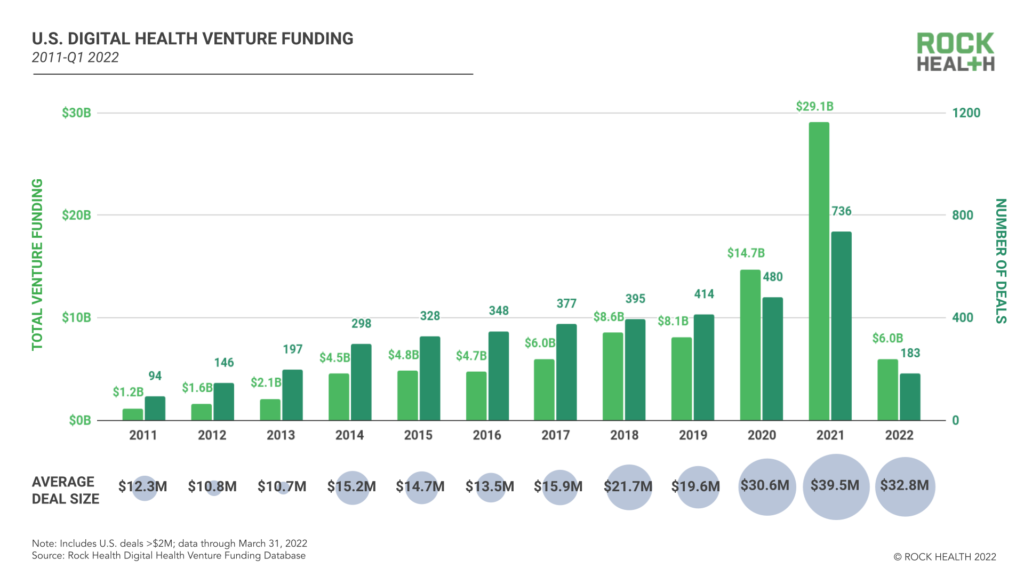

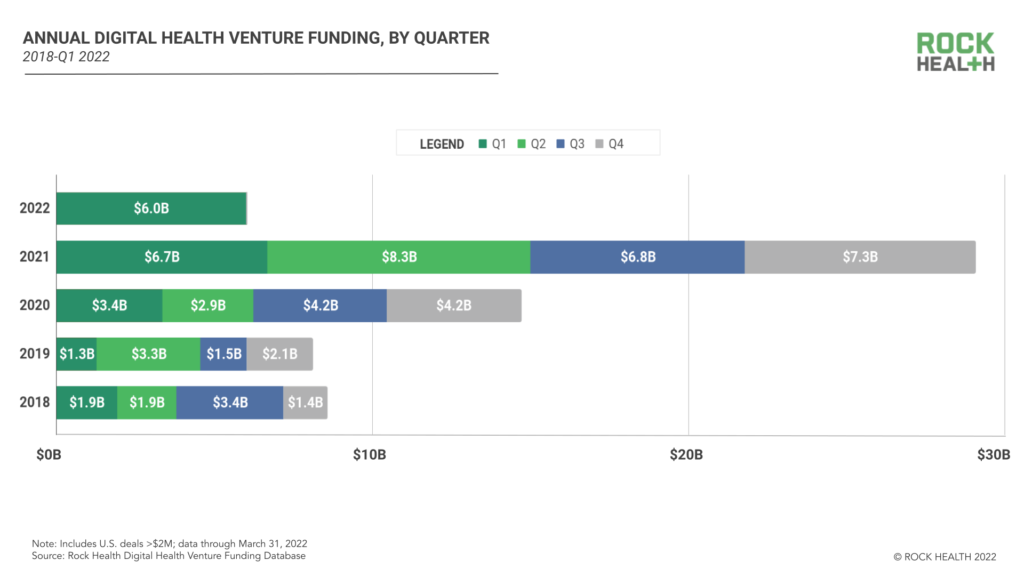

Q1 2022 U.S. digital health funding closed with $6.0B across 183 deals, with an average deal size of $32.8M. This quarter fell significantly behind Q4 2021’s $7.3B and the trailing twelve month quarterly average of $7.1B. It’s worth noting that Q1 isn’t usually a blockbuster period for funding: at $6.7B, Q1 2021 was the smallest quarter last year for digital health dollars, and three of the past five years (2017-2021) had Q1 as their lowest funding quarter, possibly signaling a seasonality to funding dips. However, in three of the five past years, Q1’s funding beat its preceding quarter (Q4 of the prior year)—which isn’t the case this quarter.

Q1 2022 also experienced some month-to-month volatility: in January 2022 companies raised $3.0B, while February only saw $1.4B and March, $1.6B. Again, this could be related to seasonality—February is a shorter month, and late stage deals can skew monthly patterns—but this quarter’s monthly funding numbers may be early indicators of a digital health venture funding correction.

Public markets drop, while SPACs deflate

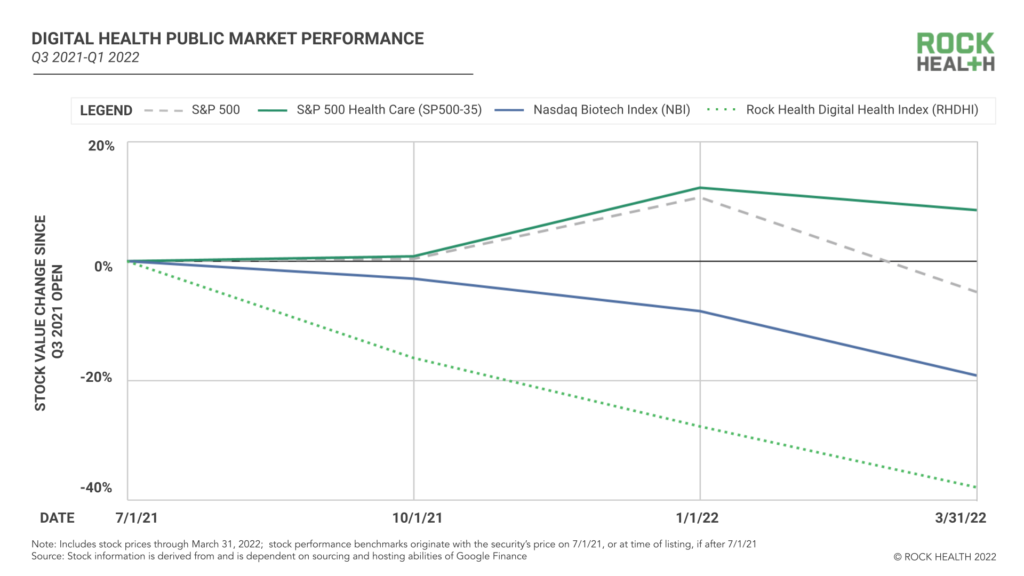

While it’s been a tough quarter for the stock market overall, it’s been a particularly no good, very bad time for digital health securities. From the beginning of Q3 2021 (July 1, 2021) to the close of Q1 2022 (March 31, 2022), the Rock Health Digital Health Index (RHDHI), our composite of publicly traded digital health securities, tumbled 38%, far below the S&P 500’s 5% dip over that same time period. RHDHI’s performance also deviated from other healthcare industry indices, such as S&P 500 Health Care (SP500-35)—which beat the S&P 500 over this time period—or Nasdaq Biotech Index (NBI).

Why have digital health companies had such a tough go in public markets? We observed that, at least in part, recent exits sunk RHDHI performance overall. Digital health companies that exited onto the public markets before 2020 saw, on average, a 17% drop in stock price from Q3 2021 open to Q1 2022 close (similar to NBI performance), while digital health’s 2020 and 2021 exit cohort saw a 55% drop in share value over the same timeframe.

One likely contributor to recent exits’ performance is their choice of exit vehicle: SPACs. While SPAC popularity boomed over the past two years—17 of digital health’s 31 public market exits from 2020-2021 were SPAC mergers—digital health’s SPAC exits’ average stock price fell 57% from Q3 2021 open to Q1 2022 close, while IPO exits’ average stock price fell 29% during the same time period. This suggests that digital health’s SPAC class exerted downward pressure on overall RHDHI performance.

SPAC stumbling is not unique to the digital health sector, and missed earnings aren’t the only red flag for this exit vehicle: Q1 2022 saw digital health SPAC deals canceled, SPAC exits taken private, and SPAC targets sued for misleading funders. Multiple factors may be contributing to SPAC turmoil, including that SPAC targets are, on average, three years younger than their IPO counterparts (suggesting that some SPAC targets may not have been ready for the public markets), and that incentives may be misaligned between SPAC sponsors and other investors (suggesting that stock price may be compromised at time of deal close).

In an optimistic market, SPAC deals contribute to—or perhaps are a reflection of—investor excitement, but in times of cautious trading, wariness pervades. We’ll be interested to see if digital health’s SPAC cohort stabilizes after a few more quarters of earnings reports. We’ll also be watching to see whether the 53 healthcare-focused SPAC shells still looking for targets continue forward with M&A moves, or if they follow other blank-check companies and call it quits before acquiring targets.

Big deals for digital health’s startup varsity class

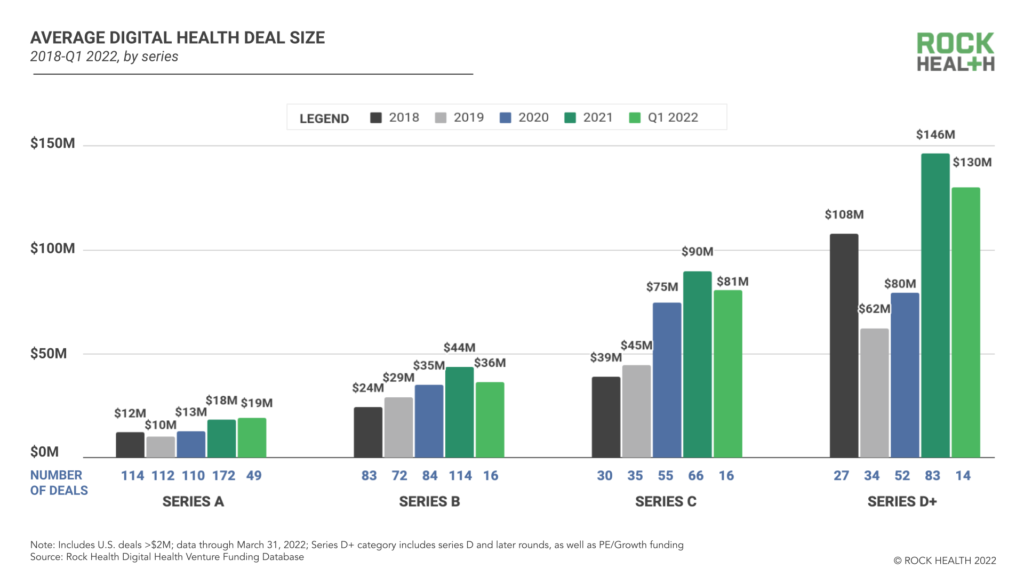

Back on the private markets, several companies from digital health’s blessing raised mega Series D+ deals in Q1 2022, including TigerConnect ($300M), Lyra ($235M), Alto Pharmacy ($200M), Rock Health port co Omada Health ($192M), and Ro ($150M). These announcements align with an overall upward trend in late-stage check size: while Series D+ raises averaged $80M in 2020, the past 15 months are tracking average D+ check sizes of $130M+. Notably, these larger late-stage checks can make for “lumpy” funding trends across time frames or service areas, so we’ll be watching to see if the numbers smooth out as 2022 progresses.

Q1’s Series D+ mega rounds hint at a few behind-the-scenes redirections happening in the broader digital health landscape. First, continued Series D+ activity might indicate that some companies are delaying their exits until public market conditions stabilize, or may be recalibrating away from SPAC exit roadmaps (or, in the case of Alto Pharmacy, scrapping SPAC plans already in the works) and possibly moving toward IPO pathways, which tend to take more time.

Late-stage rounds may also stem from the numerous venture firms that raised fresh capital on the upswing of 2021, building up the sector’s dry powder reserves. Investors might use this cash to pre-empt rounds for portfolio stars if a liquidity event is expected in the near future, or simply to box out competing funds. On the flip side, founders might feel emboldened to approach their existing investors for top-ups if they know reserves have been replenished. But late-stage startups shouldn’t get too comfortable relying on old friends, as key funders like Tiger and D1 say they’re pulling back from late-stage private deals and saving some of those dollars for early-stage investments.

Shakeups in funding allocation

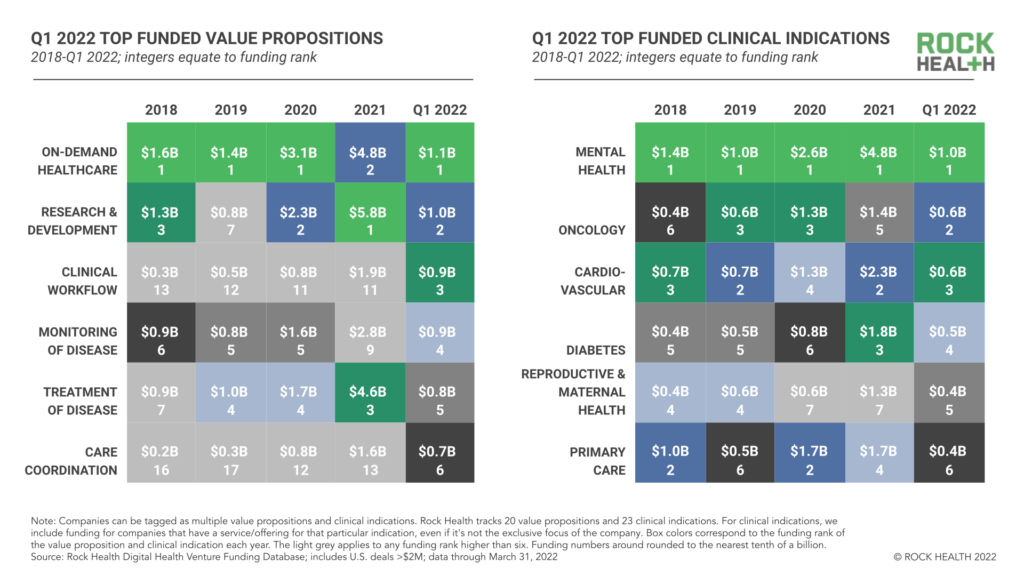

Notably, Q1 2022’s $6.0B of digital health funding is flowing to different cohorts of startups than we’ve seen in the past several quarters. Funding for digital health startups catalyzing R&D in biopharma and medtech ($1.0B) dropped slightly to second place this quarter, while funding for startups augmenting clinical workflow ($888M) rose eight spots to third place. This category includes several players that reduce or offload clinician tasks—think medical transcription (DeepScribe, $30M), complex care workflow (Memora Health, $40M), or clinical surveillance (Decisio, $18.5M)—a stark need during healthcare’s Great Resignation.

In terms of clinical focus area, startups offering mental healthcare kept the top spot with $1.0B, bolstered by employer-focused Lyra Health’s Series F ($235M) and Omada Health’s Series E ($192M), announced as Omada integrates behavioral health into all of its virtual care programs. Notably, funding for startups supporting reproductive and maternal health ($424M) reentered the top six for the first time since 2019. Q1’s reproductive & maternal funding went to heavyweights like Ro (which owns Modern Fertility and recently acquired male fertility startup Dadi), as well as new entrants like specialty maternal care marketplace Zaya Care ($7.6M) and virtual fertility clinic Turtle Health ($2.7M).

While Q1 2022’s investment distribution deviates from some of 2021’s patterns, funding numbers in each category are still too small to signal yearly trend shifts. And as we mentioned, mega deals like those from digital health’s late-stage players can throw off rankings in the first few months too. With that in mind, we’ll be watching whether Q2 funding reverts to old favorites or continues to chart in new directions.

What lies ahead

This overview of Q1 2022 wraps up just like the quarter—with key facts delivered, but with even more questions raised. The rise-and-fall of COVID variants, energy shocks, and inflation numbers signal choppy waters for digital health investors, and Q1’s somewhat restrained (dare we say rational?) funding numbers may reflect investor caution. But as we’ve shared before, entrepreneurs and investors are safest to place their bets on solutions that deliver tangible clinical and economic outcome measures. That, at least, seems like normalcy we can count on.

Rock Health’s venture fund continues to invest in entrepreneurs bringing unique and innovative technology to healthcare. We would love to hear from you. Get in touch!

Rock Health Advisory provides guidance on digital health strategy, access to proprietary funding databases, and in-depth perspectives on the digital health market. For digital health insights targeted to your needs, drop us a note.

Finally, stay up to date with the latest headlines in healthcare technology and Rock Health news by subscribing to the Rock Weekly.