Q1 2021 funding report: Digital health is all grown up

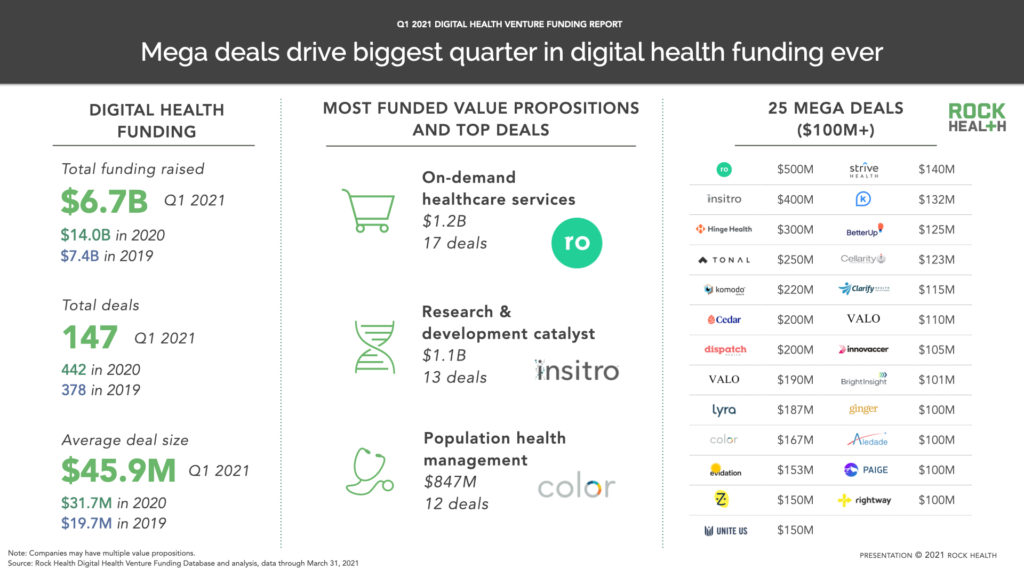

Ten years ago, we at Rock Health published our first report on digital health venture investment, highlighting an annual haul of $1.1B from investors into the emerging sector. In each of the last two weeks of March 2021, investments in digital health topped $1B+.1 And with $6.7B invested across Q1 2021, the largest quarter of funding ever, the digital health sector is on track to significantly outpace 2020’s $14B+.

In other words: We’re all grown up.

The pandemic prompted an acceleration in the adoption and mainstreaming of digital health. The surge in venture funding over the past twelve months likely reflects investors’ appraisal of the opportunity this acceleration creates. And it parallels some of the rapidly-maturing fundamentals of the sector in terms of consumer adoption, clinical impact, and of course, digital health’s role in responding to the pandemic. Over the past decade, private digital health companies have also captured a larger share of overall venture capital dollars, moving from just 2% of all venture investment in 2011 to 9% in 2020.2

Digital health is in a pivotal moment. Innovators, investors, and buyers are rightfully exuberant for digital health to transform discovery, care delivery, and well-being. But adults still have to wear their seatbelts—especially on fast rides.

Bursts of heightened activity—particularly from an investment and exit standpoint—must also be examined with caution. This means closely evaluating untested business models, new investment vehicles, skyhigh valuations, and funding trajectories that don’t match the recent past. These departures from a more tempered market will enable breakthrough winners and impact. But we also anticipate some Icarus-esque endings. In this growing market, exercising judgment will be critical. Stakeholders will need to separate long-term value creation from short-term financial opportunity, and distinguish between individual company hype cycles from overall sector fundamentals and growth.

Across this Q1 funding recap, we dive into the factors that have led us to this moment—and share our perspective on emerging dynamics (mega deals, roll-ups, and SPACs, oh my!) that are shaping the steep slope of growth in digital health. As always, if you agree, disagree, or just want to chat, reach out.

“We’re kind of a big deal,” said 25 $100M+ mega deals.

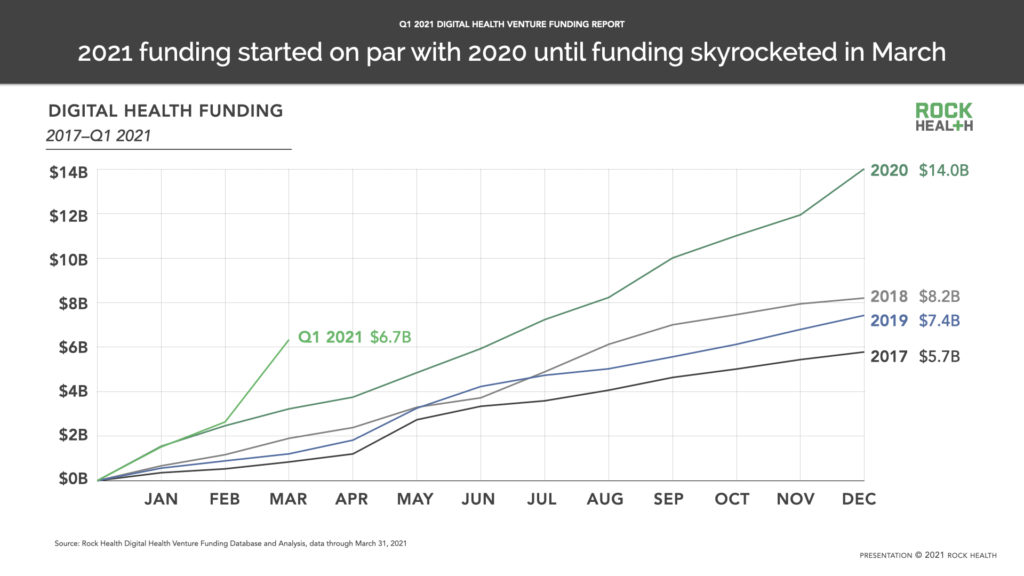

The $6.7B invested in Q1 2021 dramatically quickened the pace of digital health investment, even compared to Q3 and Q4 of 2020 ($4.1B and $4.0B raised, respectively). Q1 2021 also saw more deals completed (147) relative to the quarterly average of 110 deals throughout 2020. Taken together, this massive increase in funding and moderate increase in deal count led to a Q1 2021 average deal size of $45.9M, a 1.4x increase from 2020’s $31.7M. Of note, funding across Q1 has not been stable—as shown in the figure below, 2021 venture funding started largely on par with 2020, but ramped up significantly in March, producing 5.2x funding compared to March 2020.

$2B in 2 weeks, $800M in just 48 hours

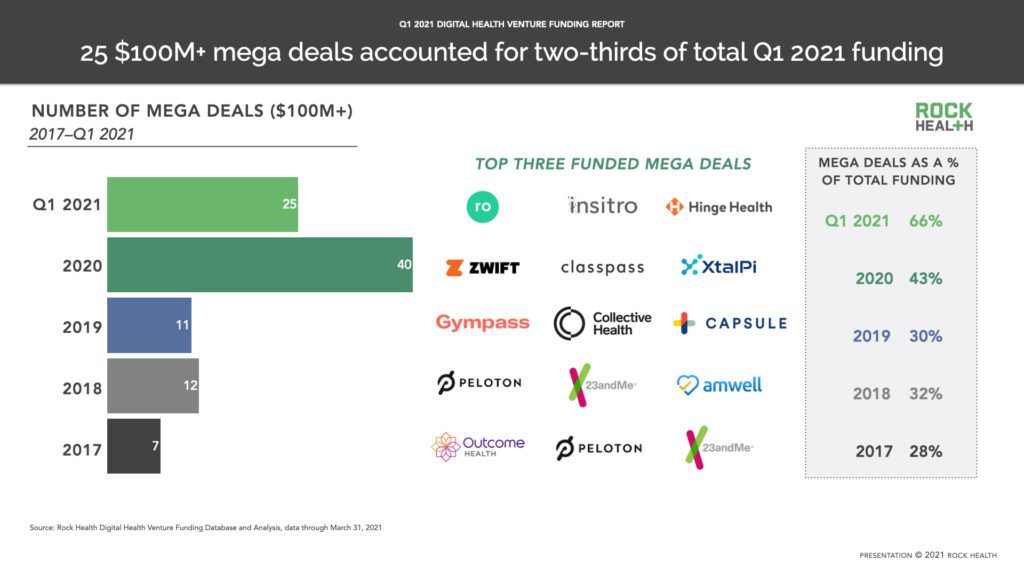

We wouldn’t be seeing billion-dollar venture weeks or a record-setting quarter without an abundance of mega deals.3 Twenty-five digital health companies closed deals larger than $100M in Q1 2021, compared to a total of 14 mega deals in Q1 and Q2 of 2020, and 40 across all of 2020. Perhaps the biggest firework among this explosion in mega deals was the announcement of four $100M+ deals in rapid succession across two days (Clarify, Unite Us, Strive Health, and Insitro)—equating to $805M in funding, or 12% of total funding in Q1 2021. Though companies raising mega deals are tackling a variety of challenges, the most common value propositions were research and development, and population health management, with five deals apiece.

Not only are more startups raising mega deals, they’re also doing so at a faster pace. The average age of startups at the time of their first mega deal raise has been cut in half over the past few years, from 12 years in 2017, to just six years among the Q1 2021 mega deal companies. Among the Q1 2021 mega deals, Valo Health observed the shortest time to its first mega deal (1.5 years), and they raised two mega deal rounds this quarter. This overall decrease in time to raise is profound, especially in a regulated industry known for long enterprise sales cycles. The quickened pace of fundraising is showing up not just in the time between founding and first mega deal but also time between rounds. Within the last 12 months, 55 companies have raised at least two venture rounds. With a 15-month lookback (since January 2020), that number grows to 88 startups.

Rising tide (capital) lifts all boats (deals)

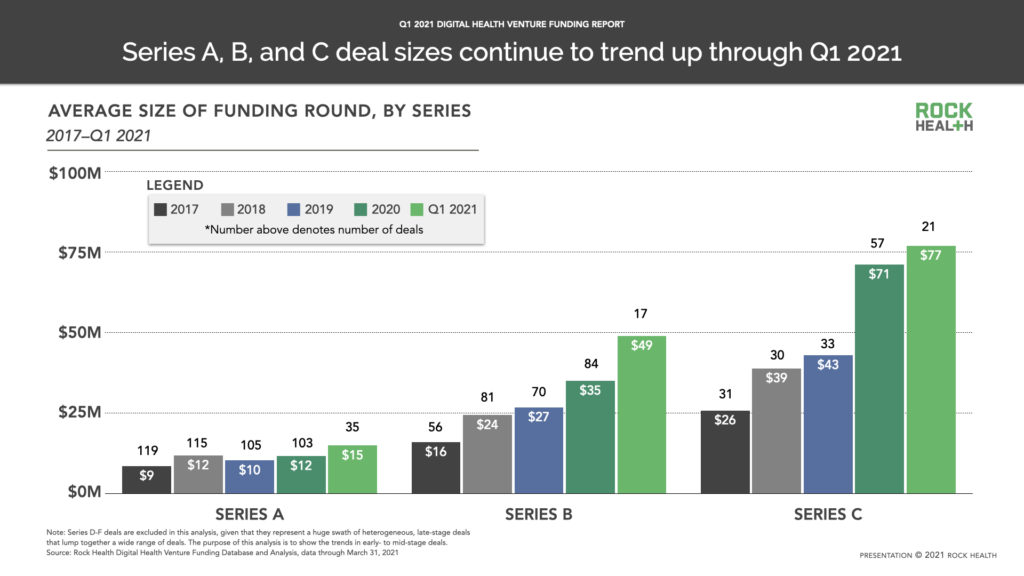

It’s not just more mega deals contributing to massive funding increases—deal sizes across all stages have increased over the past few years. In the graphic below, we plotted deal size by stage of investment (for Series A, B, and C investments) for the past four years and Q1 2021. Following an upward trend, Q1 2021 deal sizes are substantially larger at every stage of investment compared to preceding years. For example, Series A rounds grew by 1.6x from 2017 to Q1 2021.

Entrepreneurs are capitalizing on momentum for change in healthcare (and dry powder). And as others have noted, the infrastructure required to more quickly build a digital health company is growing increasingly robust—ranging from regulatory compliance support, to EHR integration, to pharmacy services. Available capital, infrastructure, and a growing cohort of experienced entrepreneurs (many battle-tested in enterprise sales and consumer design architecture), are contributing to the accelerated pace—and size of—the next deal.

Same themes, different year—investors double down.

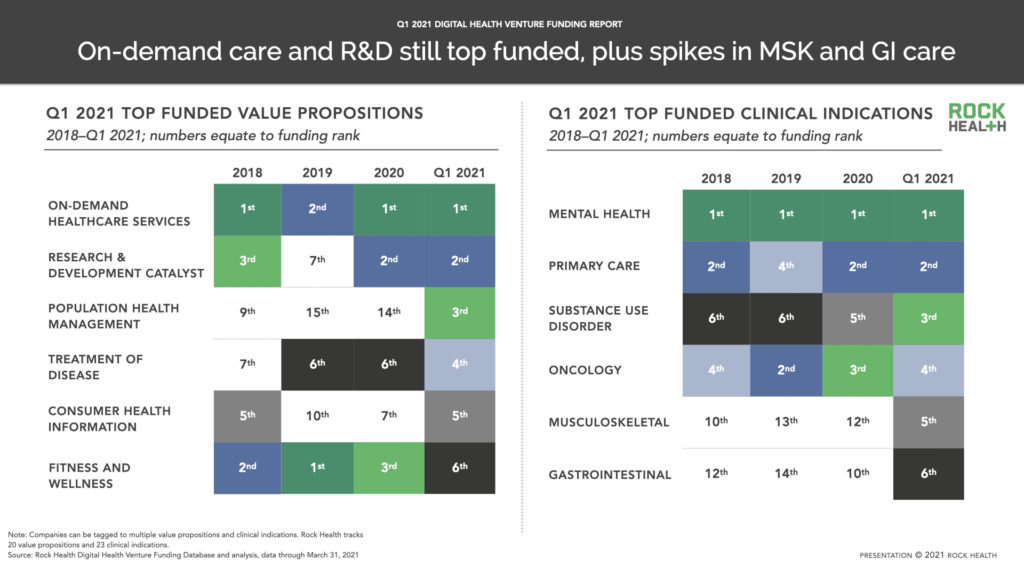

Across 2020, investors stayed the course on their investment theses, rather than making a hard pivot in light of the pandemic. This sentiment remains true so far in 2021 as well. Startups offering on-demand healthcare services ($1.2B across 17 deals) and biopharma research and development catalysts ($1.1B across 13 deals) secured the most funding across 2020 and 2021. The top deals included Ro ($500M), Dispatch Health ($200M), and Lyra Health ($187M) for on-demand healthcare, and Insitro ($400M), Valo Health ($190M), and Evidation Health ($153M) among R&D catalysts. Additionally, just two of Q1 2021’s top six investment themes weren’t among the top six in 2020: population health management and consumer health information.

Meanwhile, Q1 2021 saw an uptick in investment activity for certain clinical issues. Among companies supporting a specific clinical condition, mental health companies garnered the most amount of funding in Q1 2021 (for the fifth year in a row), in large part because of mega deals raised by Lyra Health ($187M), BetterUp ($125M), and Ginger ($100M).4 Companies offering primary care brought in the second most funding in Q1 2021, driven by a handful of deals: Ro ($500M), DispatchHealth ($200M), and Eden Health ($60M). Musculoskeletal (MSK) and gastrointestinal (GI) companies are newly among the top six funded clinical indications. The increase in MSK and GI funding may be indicative of the rise in virtual care clinics such as Hinge Health ($300M) and Vivante Health ($5.8M), as well as an expansion into these areas among startups such as DispatchHealth.

Right now is one of the best times to fundraise from an entrepreneur’s standpoint—there’s eager investors with capital, and more coming. But whether 2021 will maintain the sky-high mega deals and deal sizes of Q1 2021 remains to be seen—and will likely be informed by happenings in the exit market (up next).

The performance of today’s SPACs will have undue influence on future liquidity, in all its forms.

And you get a SPAC!

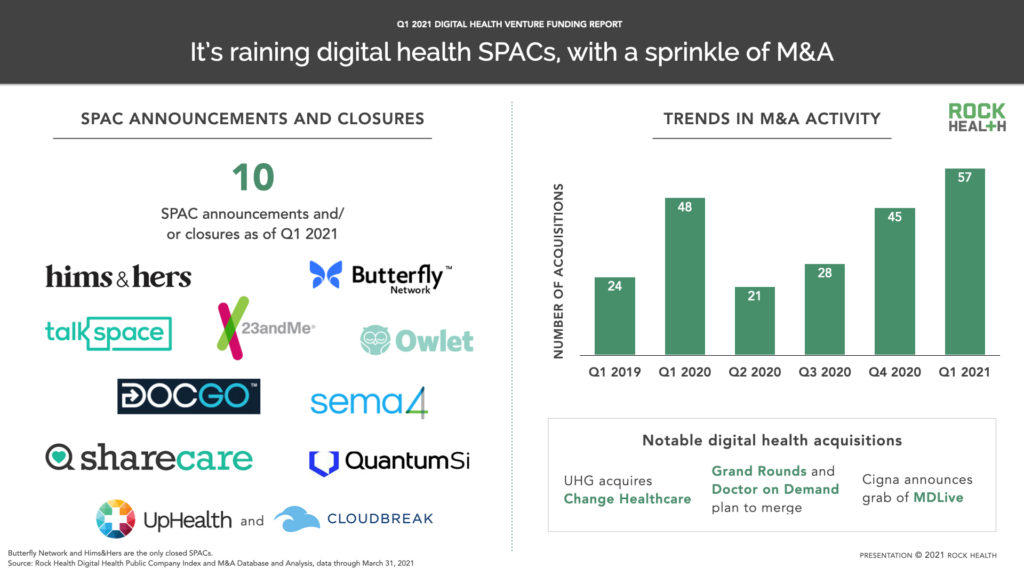

Arguably one of the biggest storylines of Q1 for digital health and the broader market is the rise of SPACs (Special Purpose Acquisition Companies), which offer an alternate path to going public compared to the traditional IPO. SPACs are shell companies that raise cash through an IPO and use that capital to acquire or merge with an active company, typically a privately-held, venture-backed startup. In doing so, the SPAC brings the startup public. A SPAC company must typically acquire its target within a two-year window.

In the first quarter of 2021, US SPACs across all industries raised more capital ($83.1B) than across all of 2020 ($82.6B). Amidst this activity, 2021 welcomed the announcement and/or closure of 10 digital health SPAC deals—Hims&Hers and Butterfly Network went public via SPAC, while Talkspace, Uphealth and Cloudbreak, 23andMe, Sema4, Sharecare, Owlet, QuantumSi, and DocGo announced SPAC deals which have yet to close.

During this uncertain time, exits via SPAC offer private companies a liquidity opportunity that allows them to sidestep a lengthy IPO process and exposure to market volatility. In the short-term, it’s possible the liquidity generated via SPAC exits will create confidence among venture firms to continue investing in digital health, perpetuating the cycle the market is currently in of high investment and valuations. In the long-term, however, SPACs may introduce new risks to the market, and the healthcare SPAC craze will remain tied to broader market sentiment. The boom-to-bust dynamics of reverse mergers might come into play—if market valuations of new SPACs go sour, this could trigger skepticism of SPACs as a viable exit vehicle. And recently, federal regulatory concern has struck a note of caution toward SPAC investments. All in all, focus will be on the performance of digital health SPACs as they will either showcase opportunity—or a cautionary tale—to private companies on the path to liquidity.

For more on SPACs, subscribe to the Rock Weekly and look out for a deep-dive coming soon.

Who’s next?

After 2020 closed with six traditional IPOs (Accolade, Amwell, GoHealth, GoodRx, Outset Medical, and Schrödinger), Q1 2021 saw two additional digital health companies opt for the traditional IPO process (Signify Health and Movano).

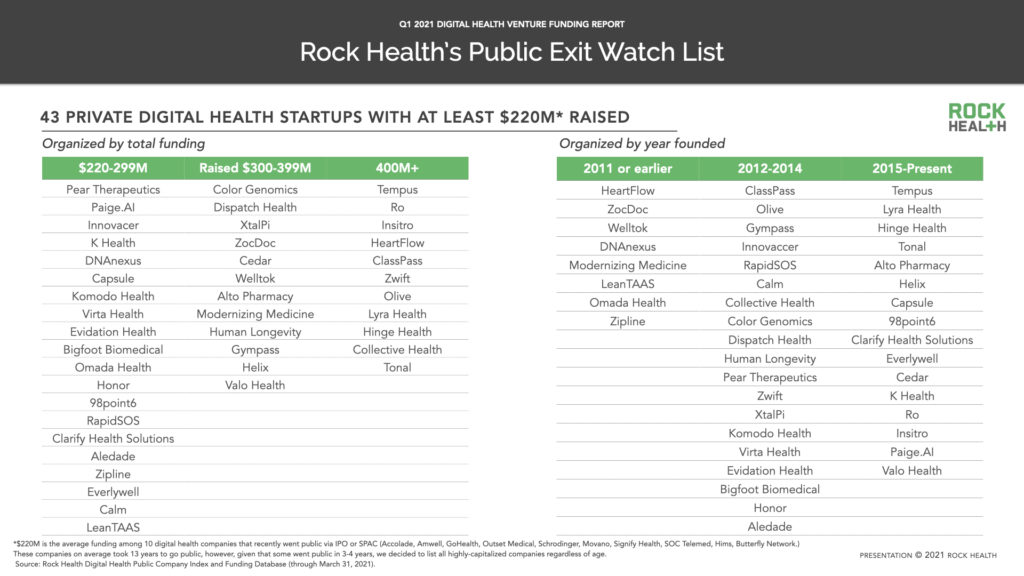

With a growing cohort of privately-held, highly-capitalized digital health companies, we decided to update our Public Exit Watch List to anticipate which private companies might be next in line to go public (via traditional IPO or SPAC) based on venture capital raised.

To build our current digital health Public Exit Watch List, we calculated the average private capital raised by the 10 digital health companies that most recently went public—this came to $220M. In the past when building this list, we’ve also applied an age criteria to reflect the average age of companies that have recently gone public. However, given the emergence of SPACs, mega deals for newer companies, and recent exits of younger companies, time-to-exit from the recent past may not be a good barometer for time-to-exit in this new environment. Therefore, we solely applied the $220M funding threshold to build the digital health public exit watch list of 43 private digital health startups. As exemplified in the graphic below, age of company doesn’t equate to most-funded—five of the 10 most-funded companies were founded in the past six years.

At least six companies on prior watch lists are now public or have announced their intent to go public: Amwell (IPO), Outset Medical (IPO), Butterfly Network (SPAC), Sharecare (SPAC), Hims&Hers (SPAC), and 23andMe (SPAC). Among companies that recently went public, time from founding to going public varied widely—Hims&Hers went public via SPAC after just three years, while Schrodinger spent 30 years as a private company.5

Behind door #3 of exit pathways: M&A!

M&A activity continued to boom through 2021, with Q1 closing 57 acquisitions of digital health companies, well over Q4 2020’s 45. Digital health companies continue to be the most common acquirers of other digital health companies.

Of note, the cardiac space saw a flurry of acquisition activity over the past four months. Following Philips’s $2.8B acquisition of BioTelemetry in December 2020, Hillrom announced a $375M deal for Bardy Diagnostics, and Boston Scientific shared plans to snap up Preventice Solutions for $925M in January 2021. All three targets offer connected patch devices to monitor and diagnose heart rhythm disorders.6

These acquisitions imply that when a standard of care may inevitably move to digital (in this case, for patients with heart rhythm disorders), the race to acquire may be speedy.

Additionally, the virtual care platform wars continued with quite a few recent examples of the battle for consumer acquisition. Grand Rounds and Doctor on Demand announced plans to merge to combine virtual care delivery and navigation services, while PatientPoint and Outcome Health are joining under a new name, PatientPoint Health Technologies, to offer a new tech-enabled patient engagement platform. Everlywell announced its acquisition of two healthcare companies to form Everly Health, offering services ranging from at-home lab testing kits and education to telemedicine. Meanwhile, health insurers continued to advance their virtual care capabilities, notably with Cigna acquiring MDLive.

Considering the exit market across 2021, we anticipate all eyes (and news coverage) on newly-closed SPAC acquisitions. Without a nuanced look at newly-public digital health companies’ products, teams, and business models, it’s possible that investor confidence could be shaped by a “broad brush” effect even if companies that rise or fall aren’t representative of the sector in full. In other words, the pace of growth of the sector will likely be influenced by the performance of a select few making the public market leap. Additionally, with SPACs as an alternate (and faster) path to liquidity, enterprise acquirers may need to prepare for higher multiples on digital health startups who have more exit options at their disposal.

A look ahead

At this pivotal moment of growth in digital health, we maintain a cautious optimism. Amidst the unprecedented flow of capital, we are weighing the following questions as we anticipate the trajectory of 2021:

-

- As we move closer to the light at the end of the pandemic tunnel, what will the future look like for virtual care? Without the urgent necessity to adopt telemedicine, patients and providers may soon shift back to pre-pandemic behaviors—and in some ways this has already taken place. However, we expect the exposure to digital health solutions to prompt some sustained shifts in virtual care adoption, though perhaps not quite at peak pandemic levels. Shifting from urgent telemedicine adoption to the next wave of virtual clinics and omnichannel approaches will require care model and business model redesign, including a favorable post-pandemic regulatory and payment landscape.

- Can enterprise buyers consume innovation at the rate it’s being funded? Healthcare enterprises, particularly providers, were expected to turn on a dime in 2020 to adopt tools to deliver care, sell products, and educate providers, all remotely. They will need to balance the competing needs of smoothing internal operations around existing technologies, while also embracing new digital transformation. If they can’t do both, this could ultimately impact the pace of adoption of digital health solutions—while accelerating rolls-ups and acquisitions.

- Will regulations, reimbursement, and validation keep pace with funding and innovation? “Move fast and break things” was never going to be the motto of digital health innovation—though admittedly, the sector is moving faster than ever before and concern is reasonable in a number of areas: data privacy, cybersecurity, clinical validation, and more. Investors and enterprise buyers should continue to apply a discerning eye toward startup investment and partner targets. We are excited to see emerging assessment models that raise the bar on expectations, as well as startups that continue to support compliance and validation.

- How will digital health companies going public via SPAC fare in the public markets?

With all eyes on digital health, we hope SPACs offer companies the opportunity for liquidity, but not at the expense of long-term value creation. Our next piece will explore how SPACs are being used to take companies public earlier than they might with a traditional IPO, and what this means for the industry.

We expect a continuation of Q1 across the remainder of the year—an entrepreneurs’ market that rewards fast growth with unprecedented capital and exit opportunities. Big shifts related to the considerations above could temper the pace of funding—but this will not slow the vital transformation offered by winning solutions. Our advice? Buckle up for the ride.

Rock Health’s venture fund continues to meet with companies virtually and invest in entrepreneurs bringing unique and innovative technology to healthcare. We would love to hear from you. Get in touch!

Rock Health Advisory provides counsel on digital health strategy to innovators at large-scale companies through our consulting practice and membership programs. For access to Rock Health’s investment databases and in-depth insights on the digital health market, drop us a note at advisoryservices@rockhealth.com.

Finally, stay up to date with the latest headlines in healthcare technology and new Rock Health research by subscribing to the Rock Weekly.

Footnotes

- Shoutout to Grand Rounds CEO Owen Tripp for beating us to this visit down memory lane.

- This analysis is based on Rock Health’s Digital Health Venture Funding Database and Pitchbook-NVCA’s venture funding analysis.

- Rock Health uses a specific definition of digital health to track venture funding, which is why some mega deals from healthcare companies such as Cityblock or Crossover Health are not included in our list.

- Mental health was the most-funded clinical indication 2017-Q1 2021. A likely reason for this is mental health services are often paired alongside broader product offerings (e.g., Doctor on Demand, Amwell, Omada Health, Livongo). We include these “generalist” companies in the mental health funding total because they offer mental health services, even though not exclusively so. For a look at funding for companies that exclusively focused on mental health indications, please see our recent post.

- Among the 10 recently closed SPACs and IPOs, the median company age was 13 years, and the average was 13.5 years.

- Hillrom ultimately reversed course on the BardyDx acquisition—litigation is still ongoing.