A coat of paint or new construction: What’s really happening in care delivery?

The focus of care delivery innovation is shifting from the bookends of the care journey—wellness and complex care—to the center: primary care and routine specialty care. Reflecting that shift, virtual, retail, and at-home care settings are growing while traditional settings are declining. This raises the question of how care will be coordinated across new and traditional sites; emerging startups and established players are both rising to the occasion.

New modes of care delivery like virtual, retail, and at-home care have taken the industry by storm–sometimes in dramatic fashion. The action has raised a question of what, where, and how care will be delivered in the future. It’s obvious that emerging players are chipping away at established providers’ dominance. Are they just giving traditional care models a new coat of paint—or are they building new foundations?

In search of answers, we tapped into Rock Health’s Digital Health Venture Funding Database and publicly available data on healthcare visit volume. We focused on three questions:

- What stages of care are being reinvented?

- Where is care being delivered?

- How does care connect across settings?

Our observations can help providers, payers, and tech enablers create their own strategic blueprints.

What stages of care are being reinvented

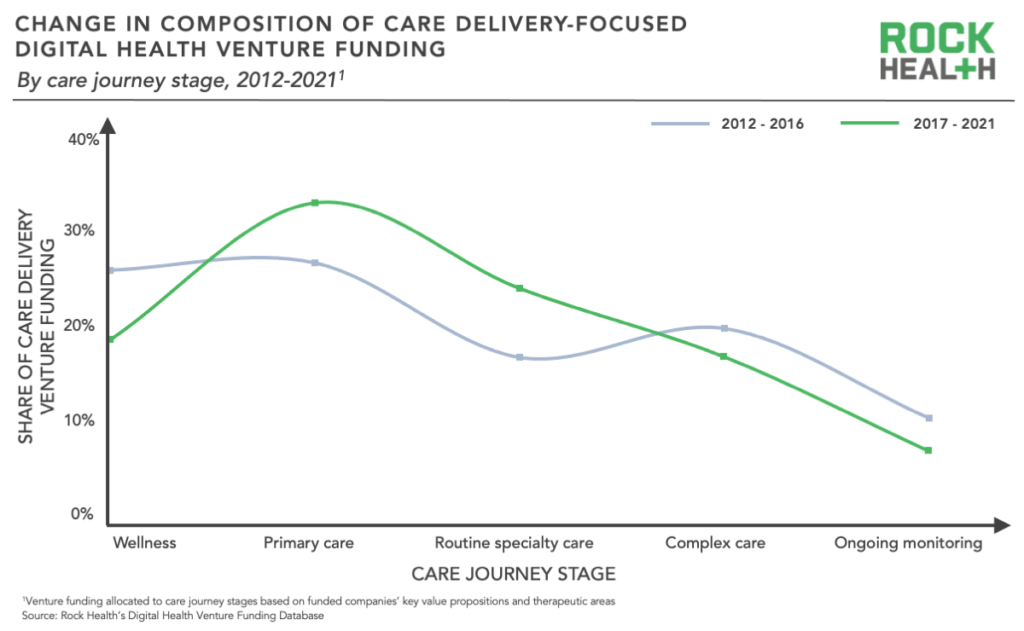

To understand the focus of emerging care delivery innovation, we examined how digital health funding across the care journey has shifted over time using Rock Health’s Venture Funding Database.1 The result: across the last decade, care delivery innovation has shifted away from upstream and downstream interventions. Innovators are increasingly focused on the center of the care journey: primary and routine specialty care.

Pioneering care delivery players focused on the bookends because they seemed to promise sizable cost savings, which attracted venture investment. Wellness startups aimed to prevent downstream care needs, while complex care startups sought to cut the cost of downstream care.

For many players, the bookends were just an early horizon. Wellness often catered to relatively healthy patients versus those at higher risk, which limited its impact. On the other end of the spectrum, cutting spending on complex cases achieved less than reducing them entirely. As a result, many companies at both bookends shifted to primary and routine specialty care to more directly impact outcomes and cost. Headspace Health, for example, shifted from wellness app to on-demand care provider by merging with Ginger in 2021. Biofourmis shifted the other way by developing digital therapeutics for non-acute heart disease alongside its complex care monitoring capabilities.

Primary and routine specialty care innovation is now coming into its own. Many mature disease treatment and on-demand care companies have established their business models and value propositions, garnering meaty, later-stage funding rounds to help them scale (e.g., Omada Health’s $192M Series E, Ro’s $500M Series D). Some have even achieved sizable exits (e.g., Oak Street Health, Hims & Hers).

Where care is being delivered

As innovation priorities have changed, so have care settings: virtual, retail, and at-home care providers are emerging as viable alternatives to traditional sites. Urgent care facilities were first to gain momentum by differentiating on convenience. Retail clinics are actively following in their footsteps—Walgreens alone plans to open 600 primary care clinics by 2025 and 1,000 by 2027. Virtual and tech-enabled care have also boomed. Virtual visits now make up 13-17% of all outpatient visits and tech-enabled primary care companies are growing rapidly by helping payers lower downstream spend. Traditional providers are already feeling emerging players’ impact: office-based primary care visits, for example, are down over 20% over the past decade, according to data from the CDC.

Hospital and office-based care remain the bedrock of care delivery—virtual, retail, and at-home care won’t eclipse them anytime soon. Nonetheless, emerging players’ impact on traditional providers will still be felt. By working at the top of the care funnel, they'll erode hospitals’ carefully curated pathways to acute care (i.e., ownership or partnership with primary care providers). Even more importantly, they’ll reduce complex care demand—studies have found that retail and virtual-first primary care tap into latent demand among patients that historically skipped primary care. The result is greater access to prevention and early disease management.

How care connects across settings

The influx of new modes of care delivery also comes at a cost: it can disrupt care continuity, leaving patients to coordinate their care across different providers and settings.

Several types of startups have taken to the challenge. Care navigation startups (e.g., Memora Health, Transcarent) support patients by easing the administrative burden of connecting care across and within provider systems. Meanwhile, data interoperability startups (e.g., b.well, Particle, etc.) are working to close data gaps between providers across settings and organizations. Pure-play companies are not the only active ones—we’re also seeing more virtual and omnichannel providers incorporate navigation support within their existing platforms (e.g., Oak Street Health’s acquisition of specialty care company RubiconMD).

Incumbent organizations play a role as well. Many payers are building or buying in-house care delivery services (e.g., UnitedHealth Group’s acquisition of home health company LHC Group), enabling them to own a piece of their members’ care journeys and coordinate downstream care as needed. Meanwhile, value-based players are establishing upstream wellness and primary care capabilities to reduce downstream acute care episodes. Value-based care (VBC) is only becoming more prominent—60% of healthcare payments were linked to value in 2020. (Stay tuned for our VBC pocket guide coming out in a few weeks.)

So, what renovations do you need?

Understanding new care delivery priorities, sites, and coordination efforts is important—but just a first step. Organizations across industry sectors must use that knowledge to revamp their strategies to succeed in the emerging landscape.

- Established providers: Protect your referral streams by building consumer-friendly digital front doors and partnering with emerging primary and routine specialty care providers—who will increasingly own the top of the funnel to downstream care.

- Emerging providers: Strengthen your value proposition for payers and employers by supporting holistic, coordinated care through partnerships with established providers offering services you do not offer.

- Tech enablers: Generate solutions for challenges facing emerging primary and routine specialty care providers and revamp your go-to-market strategy to include sales to emerging providers.

- Payers: Determine the virtual, retail, and at-home care offerings that offer the greatest cost savings to add to your network and help facilitate linkages between providers to smooth care transitions.

Novel care delivery players and models will continue to emerge in the years to come. The winners will increasingly be those that reinvent care delivery’s supportive foundation in ways that meet patients needs.

Rock Health Consulting works with enterprise companies on digital health strategy and innovation. For more information, reach out to advisory@rockhealth.com.

Footnotes

1. For this analysis, we allocated venture funding raised by US-based digital health startups across the care journey stages based on the funded companies’ primary value proposition and therapeutic areas of focus.

- Wellness includes fitness and non-clinical prevention solutions (e.g., weight tracking)

- Primary care includes clinically-focused preventive treatment

- Routine specialty care includes management and non-complex treatment for chronic diseases (e.g., mental health, diabetes)

- Complex care includes treatment, diagnostics, and clinician support associated with acute stages of disease

- Ongoing monitoring includes management of complex conditions outside of acute care episodes