Highway to health: Unlocking whole patient care through data interoperability

Health IT doesn't have a lot in common with the U.S. interstate highway system, but there are similarities. Both are (semi) governed networks of exchange. Their pathways come in various ages and conditions, which can make or break the experiences of the people that rely upon them as infrastructure. And whether it’s providers using health IT software or drivers on an interstate, it’s not comfortable when things are bumpy.

Healthcare providers—top travelers along the health data highway—are facing some potholes indeed: the COVID-19 pandemic spotlighted difficulties exchanging health information across federal, state, and private systems, and up to 25% of U.S. health system spending may be considered waste, much of which relates to information breakdowns. Most acutely, today’s healthcare staff burnout epidemic is, in part, an interoperability problem. According to 2021 research from Wakefield and Olive.AI, 36% of clinicians spent more than half their day on administrative tasks and 72% expected this time allotment to increase over the next 12 months. KLAS Research reports that clinicians’ likelihood of leaving their organizations is correlated to dissatisfaction with their health IT software.

But the healthcare industry is gearing up for a data interoperability overhaul. Health systems and insurers are rushing to comply with Cures Act data portability requirements before 2022-2023 deadlines, while digital health companies are feeling pressure from enterprise buyers to corral the “Cambrian explosion” of point solutions into unified or interoperable care platforms. Not to mention, data-first technology players are stepping more meaningfully into healthcare, as exemplified by Oracle’s acquisition of EHR vendor Cerner. In concert with all this industry activity, funding for U.S.-based health data infrastructure and interoperability startups totaled $2.2B in 2021, nearly tripling the $736M raised in 2020. Following broader digital health funding trends, venture cash for health data infrastructure and interoperability startups has tempered in 2022, despite logging a solid $260M through May 2022.1

In this piece, we’ll review the interoperability-focused digital health players and solutions helping providers exchange and integrate patient data, while also guiding innovators toward areas where interoperability innovation stands to unlock new business models and opportunities for care delivery.

Navigating patient data along the care journey

The average patient generates at least 80 megabytes of clinical data each year, encompassing sensor readings, clinical notes, lab tests, medical images, medication lists, and insurance information. As patients know too well, that data is dispersed across multiple care providers and settings, ranging from primary and specialty care appointments to hospital and urgent care visits—making it difficult for patients to manage and providers to see the full picture at any given encounter. According to a 2021 study of 2017 data, primary care physicians spend an average of 16 minutes each appointment reviewing, adjusting, and charting patient notes, nearly equivalent to the 18 total minutes spent with each patient.

Almost all U.S. providers access patient data within electronic health record (EHR) systems, which are designed to capture longitudinal views of the patient care journey for clinical, administrative, and billing purposes. Thanks in part to policy pushes, EHR adoption across U.S. care settings is nearly universal, with 96% (2015) of hospitals and nearly 90% (2019) of office-based physicians using EHR software.

However, widespread EHR adoption doesn’t mean that providers have access to complete patient data profiles at the point of care. There are hundreds of EHR products in use across the country, and vendors tend to specialize within different care settings (e.g., Epic supports 33% of the nation’s acute care hospitals, while athenahealth caters to the ambulatory space). This means patient data may be stuck in different EHR systems that don’t integrate with one another. Historically, hospital systems and EHR vendors have limited data interoperability due to HIPAA privacy laws and competitive dynamics; however, consumer advocacy groups and policy measures are starting to shift this siloed status quo.

Another interoperability accelerant is the boom in healthcare application programming interfaces (APIs): software protocols that allow different digital health applications to interact with each other. As of 2019, 84% of U.S. hospitals and 61% of clinicians reported using certified API technology enabled with FHIR, the current national health information standardization format. By streamlining and standardizing the code needed to integrate software programs, APIs greatly improve efficiency and safety when exchanging health data, opening the door for process improvements and new innovation.

Improving health data interoperability isn’t just about simplifying the provider experience or advancing hospital IT goals—there are important clinical implications. Forty percent of patients have had a healthcare professional not know what medications other healthcare providers had prescribed due to a lack of access to patient information, including nearly a quarter of patients who have experienced this more than once. Overall, 95% of surveyed physicians believe that better data interoperability would improve patient outcomes, and 86% believe that it would reduce time to diagnosis. With these care improvement opportunities in mind, health IT leaders and startup cohorts are taking on the health data interoperability challenge.

The interoperability innovation landscape

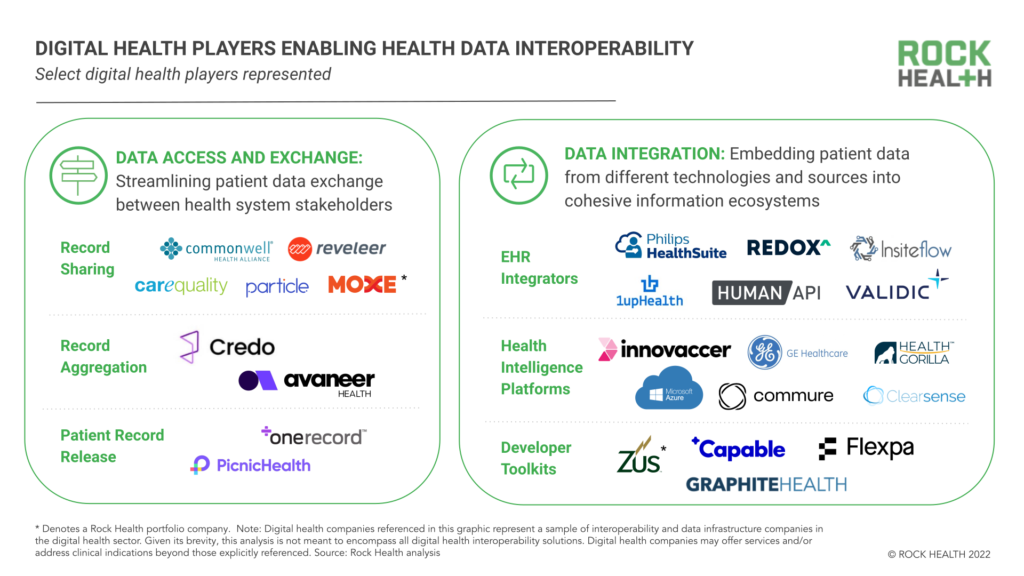

Alongside EHR vendors and tech enterprises, Rock Health has tracked 124 U.S.-based digital health startups2 that support health data infrastructure and interoperability innovation, many of which address interoperability in order to improve patient quality of care. At a high level, we segment patient-care focused interoperability players into two functional categories: (1) data access and exchange, streamlining data transference between stakeholders (especially providers and patients) and (2) data integration, embedding data from different technologies into broader information platforms that inform care decisions.3

Data access and exchange

Today, there is a foundational healthcare system need to exchange patient health records across care organizations that rely on different EHR vendors and IT systems. According to 2018 data, the average hospital must exchange data between 16 different EHR vendors across their affiliated provider organizations. When records are transferred or reconciled from one organization to another, providers risk information field mismatches, information drop offs, or other data gaps that impact treatment, research, billing, and public health decisions.

“We need to improve the accuracy of exchanging patient records and matching people to their records. Aligning patient records empowers providers to identify and deliver better, most holistic care—and that’s our end goal.” Deven McGraw, Co-Founder of Ciitizen and Data Stewardship and Sharing Lead, Invitae

Most EHR vendors facilitate record-sharing between their customer organizations, and many are joining industry-wide data sharing coalitions like CommonWell and Carequality in the name of patient care coordination. Meanwhile, some digital health startups are positioning themselves as point solutions that deliver on patient record retrieval and exchange. Particle Health, Moxe Chart Retrieval4 and Credo Health help locate patients across EHRs, import records, and reconcile complete patient profiles. Avaneer Health takes a different approach and secures data exchange over the blockchain ledger. Reveleer and Moxe ROI automate release of information between providers and aggregate patient records for hospital quality reporting processes.

Beyond healthcare organizations, clinical records may also be released to individual patients. The Cures Act Final Rule was in part motivated to enable patients to have more ownership of their health data—as such, this rule requires that healthcare providers offer patients access to their EHR data upon request and without charge. Startups are now offering patients support in accessing and aggregating their records. OneRecord helps individuals gather their patient records and organize them into digital profiles, while PicnicHealth enables patients to download and then de-identify their provider datasets to share with researchers.

“As a patient, I should be able to understand my health data and count on my clinical team to use my data to engage new care options.” Christopher Mack, Executive Director of Strategic Initiatives, Sutter Health

Data integration

While data exchange players meet one aspect of interoperability, another important component is interconnecting EHR data with other clinical, external, and administrative datasets to empower providers to do more for the patient at the point of care.

EHR vendors are competing on data integration, user interface, clinical platform builds, and network effects. Epic, Cerner, athenahealth and AllScripts all host their own app marketplaces, embedding external applications and data related to remote monitoring, digital therapeutics community support, clinical decision support, and preventative health into their native EHR workflows. Other companies are facilitating specific EHR integrations: Philips and Redox focus on medical device data integration, HumanAPI and Validic on wearable and real-world data, InsiteFlow on clinical surveillance and clinical decision support, and 1upHealth on population health.

The EHR itself is a dataset that can be integrated. There are several companies combining EHR data with other information streams (e.g., hospital inventory, population and mortality data, health insurance claims, staffing and security logs) and digital tools (e.g., workflow software) to create broader health intelligence platforms. These platform builders range from legacy names in healthcare IT (GE Healthcare and Microsoft both unveiled new health intelligence platforms at HIMSS 2022) to startups such as Commure, Health Gorilla, Innovaccer, and ClearSense. These platforms are designed to be used by entire provider enterprises to streamline care and business operations.

Last in this integration services category are developer toolkits, which are pre-connected data infrastructures that make it easier for companies (enterprises and startups alike) to build solutions that integrate with an EHR or health platform of choice. While EHRs often offer developer standards or support, developer toolkits go a step further by providing full tech stacks (bundles of programming languages, frameworks, databases, front- and back-end tools, and apps connected via API) that make the product development process nearly plug-and-play. Startup leaders in this space include Zus Health,5 Capable Health, Flexpa, and health system-led toolkit Graphite Health.

“You have to make interoperability easy for builders. There’s a huge education gap for builders in healthcare—getting to know different protocols, industry acronyms, and healthcare workflows. Diving deep into the developer experience, we realize how important it is to simplify their innovation process.” Andrew Arruda, Co-Founder and CEO, Flexpa

What comes next?

As the seeds of data exchange and integration grow into more streamlined, robust, and actionable information sharing at the point of care, we expect to see changes reverberate across the healthcare industry.

“Now that we’re well on the way to building infrastructure for true health data interoperability, we have earned the right to ask ‘what’s next?’” Nate Maslak, Co-Founder and CEO, Ribbon Health

Unlocked possibilities in healthcare analytics

Data integration doesn’t only stitch together patient profiles. In doing so, it also enables developers to build (and feed data into) complex analytical tools that catalyze healthcare innovation.

For example, artificial intelligence (AI)-enabled clinical support has long been promised; however, the usability and performance of AI algorithms depends on the volume and quality of data available. Large, high quality patient data sets are needed for AI algorithms to unlock high-value insights for providers—tying healthcare AI’s revolution directly to the health data interoperability roadmap. GE Healthcare and Microsoft are already designing their interoperability platforms to power suites of AI software. Given the symbiotic relationship between data interoperability and healthcare AI, we’ll likely see more interoperability players build or partner/acquire with AI-enabled solutions.

“We have a lot of waste in healthcare, a lot of missed opportunities to surface important health insights. Machine learning and other AI strategies can help us to be more efficient with the data we have.” Edwin Martin, Director of Technology, UCSF Center for Digital Health Innovation

Interoperability-enabled data analytics are also needed to structure, participate in, and monetize new reimbursement models such as value-based care (VBC). VBC arrangements align payments to the quality of care that providers administer, linking provider revenue to care efficacy and efficiency—two measures that require robust data analytics and outcomes reporting.

As such, healthcare’s movement toward VBC can only go as fast as interoperability advancements that 1) unlock the analytical power needed to identify care delivery improvement opportunities, and 2) integrate the right data to demonstrate providers’ outcome measures at scale. As VBC and interoperability initiatives converge, we’ll be watching to see how today’s first-generation VBC analytics providers like VirtualHealth and Nanthealth work with (or even fold into) data interoperability solutions.

“Interoperability stands to help drive value-based care in two directions: building out patient risk profiles that then help connect folks to more care resources, and then identifying high-level insights for provider organization learnings.” Michael Kovach, Executive Director Deep Partnerships, Corporate Strategy, athenahealth

Meaningful integration of real-world insights

Despite the fact that 70% of hospitals draw data from outside sources into EHRs, health systems aren’t keeping up with the explosion of personal data—according to RBC Capital, the average person will log 5,000 daily interactions with digital devices by 2025. At that pace, clinical-only data ecosystems will leave gigabytes of health signals outside of provider purview.

Hospital-at-home programs and new reimbursement codes are upping economic incentives for provider groups to coordinate care in the home, and, as a result, we expect to see bigger initiatives around integrating real-world data into clinical settings. Leaders in medical devices and remote monitoring like Philips and Biofourmis are already pioneering real-world and clinical data integrations, while consumer-facing device makers Apple and Amazon Alexa are paving relationships into health systems and care facilities. We’re keeping our eye on how direct-to-consumer (D2C) diagnostics startups—which offer mail-order tests and on-demand lab draws—connect into clinical data ecosystems, with companies like Ash Wellness already positioning themselves as D2C-clinical infrastructure supports.

As more healthcare activities become location agnostic, market leaders in consumer data collection (e.g., Apple, Amazon) may change how they interact with health IT incumbents. For example, if Apple continues to build out its wearable health suite, will it keep signing individual data-sharing partnerships with EHR vendors, or will the company take on a larger role in health data aggregation and management? For legacy health IT players, the time is ripe to invest in at-home and real-world data collection approaches and integrate them at the point of care.

Changes to competitive strategies

With regulatory dynamics and tech innovations bringing new levels of health data transparency and interoperability to fruition, we’re likely to see health IT businesses move their strategies beyond proprietary data ownership—instead prioritizing data quality and real-time accessibility. As value delivery shifts to actionable information that clinicians and consumers can use to make decisions, business models will change and profit sanctuaries will rotate.

Incumbent EHR vendors are tackling this shift head-on, embedding external data and apps into their workflows and focusing on building up their communities of data exchange partners. Some are even proposing new offerings that extend beyond their core products and capabilities. Incumbents will likely double down on strategic partnerships and integrations, and we may even see a wave of M&A activity as legacy players scoop up relevant point solutions that extend their interoperability capabilities. Not to mention, these shifts may impact how Big Tech players like Google, Microsoft, and AWS—all of which offer cloud systems for health data storage and architecture—execute their next healthcare moves. Our bet is that they invest in “play-along” rather than “play-against” relationships.

Lastly, we’ll be watching to see how emerging players like Flexpa, which control no patient data but instead link data sources to one another via new patient access APIs, build out their competitive strategies. With value propositions that are all about data flow interoperability and clean translations into specific use cases, companies like these can chart a new course for what it means to be a health IT company (i.e., more highway than hub).

Addressing new and existing vulnerabilities

Healthcare has historically lagged behind other industries in cybersecurity, with only 6% of healthcare organizations putting more than 10% their total IT budgets toward cybersecurity investments. However, with health system cyberattacks on the rise and patients exercising legal action against hospitals for data breaches, provider organizations are reevaluating their cybersecurity strategies—just as interoperability innovations expose new system threats. For example, while most EHRs and API protocols offer relatively high data security, third-party apps and digital health products are more likely to have software vulnerabilities that offer hackers new entry points into health IT systems. And while cloud data infrastructures make it easier and more cost-effective for hospitals to store and manage data, more steps are needed to ensure the healthcare system can operate if the cloud goes down.

As cybersecurity becomes a central component of data transformation and interoperability, we expect the role of Chief Information Security Officers (CSOs or CISOs) to rise in the digital transformation arena. Market consolidation will also have an impact, as larger IT players can invest more in cybersecurity measures than the point solutions they acquire. Unfortunately, that means cybersecurity may arise as an equity issue. As well-funded hospital systems form partnerships with higher-quality data players and prioritize cybersecurity investments, small and rural hospitals will bear the brunt of data attacks and resulting operational interruptions.

With the influx of new players entering the health data landscape, concerns also rise around patient privacy and data protection. Even “de-identified” patient data (which can be brokered to third-party firms, per HIPAA guidelines) is increasingly re-identifiable, meaning that sensitive personal information is moving farther away from patient awareness and control. In response, startups like Datavant are exploring new de-identification methods, such as replacing private patient information with encrypted tokens that cannot be reverse engineered to reveal patient identity.

Emerging security and privacy risks stemming from health data interoperability have renewed calls for HIPAA modernization and increased FDA oversight of health data-collecting devices. Health systems will need to ensure their data practices prioritize patient privacy and institutional trust. Based on examples like Graphite Health’s Digital Hippocratic Oath, we’re interested to see how far provider organizations go in outlining mission-oriented approaches for patient data use and transformation.

Interoperability in service of care delivery

Sometimes health data interoperability successes, like increased data availability or newly-enabled analytics tools and processes, stand to challenge the very providers that they’re designed to support. According to a 2019 survey, 77% of healthcare executives observed their clinical staff appearing stressed or overwhelmed by technology at their practices, and 58% observed clinical staff having trouble navigating multiple data-driven alarms and alerts—signs of cognitive overload. Not only can cognitive overload lead to clinical care mistakes, but it can also burn out providers.

Advancing health data interoperability while protecting providers’ cognitive load is a balancing act, and solutions that focus on seamless integration with native workflows, curated communication and alerts, and well-designed (dare we say delightful) provider interfaces will come out on top. For example, athenahealth has named provider usability a top innovation goal and partners with provider workflow management tools like HybridChart.

For decision-makers at healthcare organizations, it’s important to remember that health data interoperability is an essential component, though still a “means to an end” toward larger care delivery goals—including improving quality of care, expanding access to care, and reducing cost of care delivery. While it’s possible to feel crowded by all the action in this space, health data transformation strategies rooted in disciplined prioritization and iterative changes and based on feedback from stakeholders (particularly providers and patients), are heading towards the road to success.

Rock Health would like to thank Andrew Arruda (Flexpa), Claire Aviles (athenahealth), Michael Kovach (athenahealth), Christopher Mack (Sutter Health), Edwin Martin (UCSF Center for Digital Health Innovation), Nate Maslak (Ribbon Health), Katelyn McCabe (athenahealth), Deven McGraw (Invitae), Jessica Sweeney-Platt (athenahealth), Peter Ross (athenahealth), and Stephanie Zaremba (athenahealth) for their insight and support in writing this piece.

Footnotes

1. Source: Rock Health Digital Health Venture Funding Database. Note: Includes U.S. deals >$2M; data collected through May 31, 2022.

2. Source: Rock Health Digital Health Venture Funding Database. Note: Includes U.S.-based digital health companies that have raised over >$2M; data collected through May 31, 2022.

3. Given this piece’s focus on patient care delivery, market maps and analyses only refer to interoperability solutions improving care delivery—not those focused on clinical research, or financial operations and insurance coverage. Digital health companies and products mentioned in this blog post represent only samples of digital health interoperability solutions, and companies mentioned may offer additional products or services beyond their description/categorizations here. Due to the brevity of this piece, its analysis is not meant to encompass all digital health interoperability players.

4. Moxe is a Rock Health portfolio company.

5. Zus Health is a Rock Health portfolio company.