H1 2026 funding and market overview: Durable roots, shifting routes

Generative AI is earning its place as a generation-defining technology reshaping global society and economies. With the accelerating pace of model improvements, experimentation for better and for worse, oscillations in sentiment from radical optimism to growing distrust, the contours of that transformation are still coming into focus. The more we know about AI, the more it seems we don’t know.

In the digital health sector, as in all software-centric markets, AI has reset expectations around what’s possible and what’s replaceable (overnight). What once seemed futuristic is already here as clinical reality. Familiar landmarks are becoming less reliable: a great SaaS product isn’t the moat it once was; AI put a twist on the build-versus-buy equation; cracks are emerging in the dominance of healthcare-specific solutions over generalist ones.

As AI changes what’s easy to build, competitive advantage increasingly comes from qualities that are difficult to replicate. Innovators are returning to first-principles thinking. Investors point to the evergreen but never-more-essential importance of selecting for agile teams with deep domain expertise and a knack for recognizing the new opportunities AI creates, rather than just doing the “same old” better. And the sector is embracing a renewed focus on measurable outcomes as true north—a standard that will hold no matter how quickly the technology changes.

What follows is our quarterly read on these signals across funding, company strategy, and the public markets. We look at where investors and startups are continuing to honor enduring fundamentals, with an eye toward how those fundamentals are taking new forms.

Lay of the land

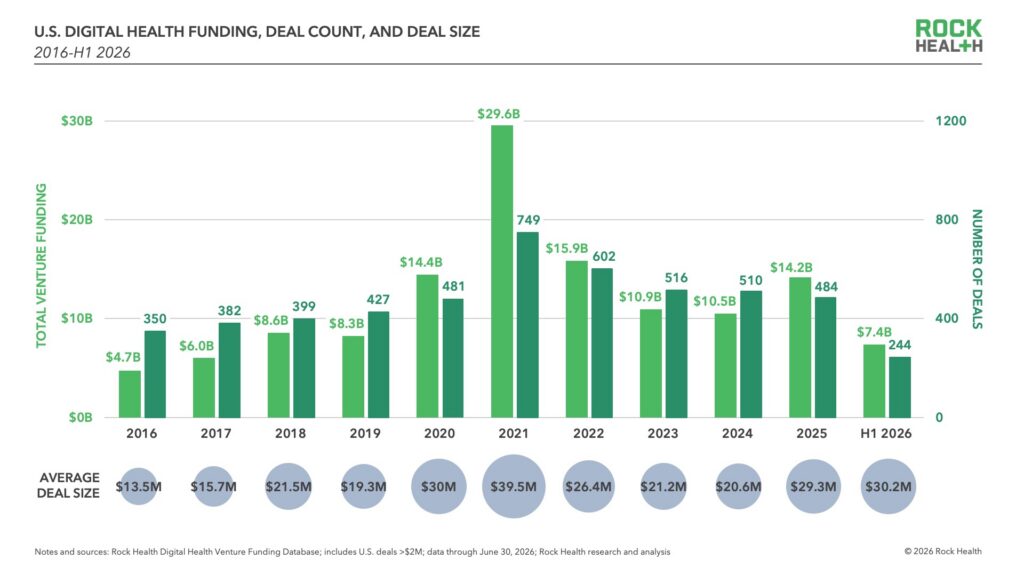

Venture funding for digital health is up this half, and capital concentration continues. U.S. digital health startups raised $7.4B across 244 deals in H1 2026, surpassing last year’s first half by $1B ($6.4B) on about as many deals (245). This year, Q2 accounted for $3.2B of that total, shy of Q1’s $4.2B, but not far off from last year’s second quarter ($3.4B). The overall median deal size rose from $12M in 2025 to $14M this half, a high since 2022. All told, this year’s funding is on track to continue a recent upswing, as the market makes an AI-powered rebound from its post-pandemic reset in 2023 ($10.9B) and 2024 ($10.5B).

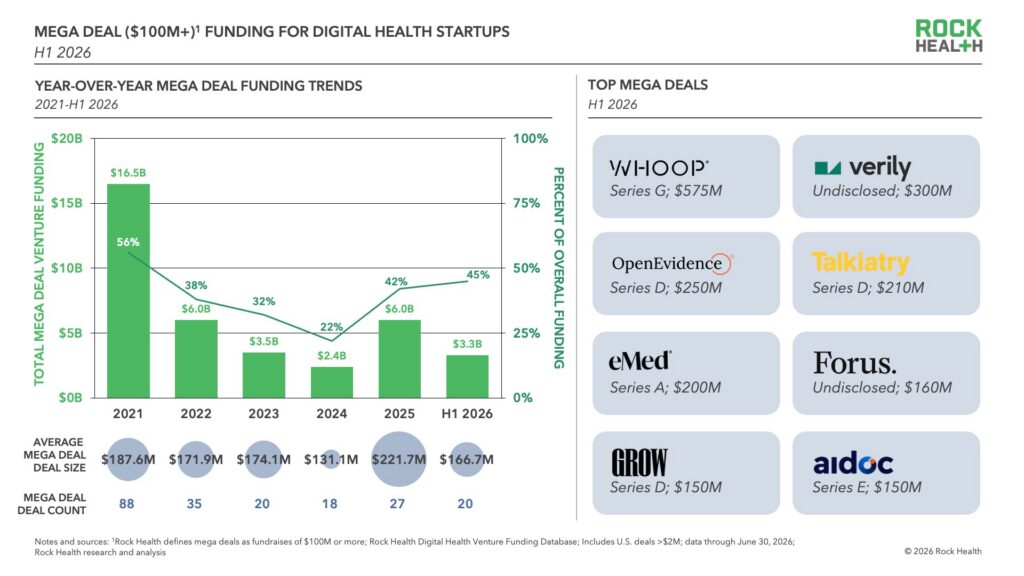

Mega deals (financings of $100M+) remain a defining feature of today’s digital health market, and the portion of funding they represent continues to grow. Nineteen companies raised 20 mega deals in H1, representing 45% of all capital invested—a big leap from the 22% of funding that mega deals accounted for in 2024 (and up from 42% last year). In other words, just over 8% of deals absorbed nearly half of all capital deployed. Though most of this year’s $100M+ raises went to first-time recipients (13 of 19), back-to-back mega deals are still in the mix—this past quarter saw employer-focused care navigator Garner Health secure a $100M Series E just three months after its $118M Series D, while clinical AI platform Aidoc clinched its second $150M check in less than a year.

Let’s get clinical (indications)

For the seventh consecutive year, mental health is the top-funded clinical indication. The category’s persistence at the top reflects not only continued investment in mental health startups like Talkiatry ($210M) and Grow Therapy ($150M) but also in the delivery infrastructure needed to make behavioral health services more scalable, like provider marketplaces. Given the gap between demand for care and mental health provider capacity, the potential to scale care delivery through AI is especially compelling. But alongside that big opportunity are big challenges, including concerns about safe use and appropriate guardrails. As such, investors are betting on purpose-built solutions with dedicated clinician oversight and third-party safety evaluations like those offered by Jimini Health ($17M) and The Path ($14.3M). However, the use of dedicated mental health chatbots pales in comparison to the rapid consumer adoption of frontier labs’ general purpose chatbots for mental health support, which are increasingly incorporating safeguards for users during mental health conversations. As startups compete for adoption based on differentiated expertise and validation, the category faces competing policy currents in the months ahead, with the Trump administration signaling growing support for psychedelic-assisted therapy alongside increasing scrutiny of psychiatric medication prescribing—the latest shift in a category that has repeatedly reinvented itself as both public attitudes and technology have evolved.

Weight management/obesity is the second most-funded clinical indication, driven by the insatiable1 GLP-1 market and the ecosystem scaling around it. Three mega deals anchored the category—eMed ($200M), Nourish ($100M), and Midi ($100M), each expanding an existing platform into GLP-1 care—alongside Signos’ $20M raise for its over-the-counter continuous glucose monitor and partnership with Dexcom. The funding reflects a market that is maturing its commercialization strategy. This year, pharma has made significant moves to get closer to the consumer through direct-to-patient channels, including partnerships with digital health companies to roll out oral GLP-1 options and new access pathways. Those efforts are extending into public coverage: the Medicare Bridge program, a pilot set to offer $50/month GLP-1s, opens a more affordable path for Medicare recipients. The success of GLP-1s is also drawing investor attention to adjacent peptide categories, including experimental peptides for wellness and longevity—with companies like Superpower ($30M), Protocole ($6M), and Feel Peptides ($3M) all raising capital in H1. We’ll be keeping an eye on the FDA’s peptide reclassification meeting scheduled for late July 2026, given its implications for how peptide products are marketed and distributed, particularly for leading weight management companies expanding their existing infrastructure in preparation for broader peptide access.

The high flow of capital for startups in mental health and weight management coincides with their reliance on consumer-directed business models. Among digital health companies that raised in H1 2026, nearly two-thirds (64%) of mental health and weight management startups sell directly to consumers, compared to 29% of all digital health companies—a reflection of high, unmet consumer demand. The forces revitalizing D2C channels in healthcare extend well beyond these two areas, including rising consumer adoption of AI chatbots and wearables.

Want a closer look at the images in this recap? The slides are available for download—including an additional graphic featuring H1 2026’s top-funded clinical indications.

Navigating by the stars

Last quarter, we stopped labeling particular digital health startups as “AI-enabled,” as AI has become sufficiently ubiquitous and no longer a distinguishing product or strategy. As foundation models improve and AI capabilities become easier to build, technical differentiation is becoming harder to sustain. Investors and buyers are not asking, “Who has AI?” but instead, “Who has something AI alone can’t provide?” The question is especially acute as incumbents like Epic give customers more ways to DIY agents and solutions. As we looked across this year’s financings and spoke with investors, we saw the same four themes surface again and again. Though these moats are by no means exhaustive, together they offer a snapshot of how durable advantage is evolving in the AI-era.

Founder edge

We’re hearing from earlier-stage investors that domain expertise is more important than ever. As AI lowers the barriers to building, founders with deep experience inside the healthcare organizations they’re selling to often have a clearer view of where the most meaningful (and solvable) problems exist. Founders with clinical or administrative backgrounds can bring a nuanced understanding of care team dynamics or operational pain points, helping them “see through the buyer’s eyes” as they sell to familiar organizations. Investors also point to “good taste”—the phrase du jour standing in for discernment and sharp instinct—as a key characteristic of investable founders. This judgment, combined with empathy for the real tradeoffs buyers face, can help growing teams build trust and keep focused on the problems that matter most.

“None of us know what the world is going to look like two years from now. The primary attribute of any pitch that is most fundamental to diligence is the founder. Founder-market fit matters a lot right now. We’ve seen real advantages with founders who understand not just the business function they’re trying to improve, but also the culture and conditions that shape how their customers operate.”

—Sean Doolan, Founder & Investor, Virtue

Scaling to own

Some of digital health’s most well-capitalized companies are competing for greater ownership of the healthcare operating layer. The early wave of startups’ AI expansion looked a lot like typical commercial footprint expansion (i.e., moving from one area of specialization into adjacent categories). But as AI makes it easier to build competing, single-use-case products, and as agentic AI increases the value of orchestrating more of the workflow, startups have even greater motivation to scale. The more of the operating layer a startup oversees, the more context its products have to work with; the more context, the easier it is to coordinate across tasks rather than optimize each one in isolation. One open question is what will happen as these expanding roadmaps begin to overlap with one another (and Epic). As individual vendors move beyond their original footholds, their customers may increasingly find themselves evaluating redundant offerings.

Hands-on delivery

AI is raising the bar for what customers expect after signing a contract. Increasingly, buyers need partners who can help adapt their products to the way work realistically happens inside an organization, rather than vendors who roll out a new solution and leave the customers to figure out the rest. AI has made more tailored implementations possible, but has also flooded buyers with new options, raising expectations for measurable ROI and leaving little appetite for failed deployments. In response, some startups are investing in forward-deployed engineers (FDEs), a role that took hold in other industries before gaining traction in healthcare more recently. The rationale is that launching highly customizable systems requires white-glove service, one that sends FDEs to work directly with customers on an ongoing basis and co-develop custom workflows from within the client’s environment. Highly-capitalized infrastructure startups like Commure and Qualified Health have made FDEs a core part of their go-to-market; Anthropic and OpenAI have built out life sciences teams and are sending out FDEs of their own.

“Health systems are leading in AI transformation right now—it’s really quite incredible. To think, when we started Rock Health, very few startups sold into hospitals because the sales cycle was long, and most health systems didn’t have the infrastructure or culture to successfully absorb new innovation. Now, if you look at the big AI companies getting funded, most of them are building for health systems. It’s a sign of just how much has changed.”

—Halle Tecco, Rock Health Founder, Investor, Author of “Massively Better Healthcare”

Network effects

Healthcare buyers face no shortage of vendor options. Strategic partnerships can reduce the perceived risk of adopting a new product. Vendors that partner with organizations and standards buyers already trust can build on existing credibility rather than earn it entirely on their own. And every new integration or endorsement can make a product more trusted and harder to replace, giving customers even more reason to stay within the same ecosystem. Abridge’s most recent announcement, for example, brought a whole host of new partners to the table: beyond signing health systems, Abridge linked up with Nvidia on clinical foundation models, American Health Information Management Association (AHIMA) on coding standards, the American Diabetes Association (ADA), and the American Academy of Family Physicians (AAFP) on clinical validation, and companies like Artisight and hellocare.ai on smart-room integrations. OpenEvidence, meanwhile, has pursued partnerships with medical societies and publishers, giving clinicians access to trusted evidence within their existing workflows. Every trusted relationship makes the next partner and the next customer easier to win. These effects compound over time, as each partnership makes the product more valuable to customers and more attractive to the next prospective partner. As the ecosystem around a company grows, the harder it becomes for competitors to reproduce.

Checking the horizon

The (anticipated) public debuts of Anthropic and OpenAI are set to offer unmatched returns for investors and employees (just look at San Francisco real estate). And, SpaceX recently landed its record-breaking IPO raising over $85B and skyrocketing1 to a $2.2T valuation on its first day of trading before gravity1 caught up.

Digital health is still waiting for its own IPO spurt—after seven exits in 2025, the sector has yet to see one this year, despite a number of candidates waiting in the wings. First up: wearable ringmaker Oura, who logged the first and only S-1 filing for a digital health company this year, after a headline-filled few months. Plans for an IPO come on the heels of raising the largest digital health deal ever ($900M) last October at an $11B valuation, an ~11x multiple on reported revenue. This half also saw Whoop secure a $575M financing at a $10.1B valuation, as it prepares for its own public debut in the coming years. Wearables have come a long way since the Fitbit exit over a decade ago—their data moats are deeper, analytics more personalized, and recurring revenue more durable—with the addition of in-app care offerings alongside integrated lab results and medical records, their businesses have become a case study in consumer-facing platformization. Wearable giants aren’t the only ones eyeing the public markets. A growing number of late-stage digital health companies now have the scale and financial profile to support a public listing; many have also grown beyond the reach of most strategic acquirers, making a public listing the clearest path to liquidity.

The digital health companies that have made the leap to the public markets have seen valleys and peaks. This half brought delistings from GoHealth after the health insurance marketplace filed for Chapter 11 bankruptcy, and medical robotics developer Vicarious Surgical, which went public via SPAC in 2021. On the flip side, Tempus surpassed analyst expectations, reporting 36% year-over-year revenue growth in Q1 earnings, citing “immense value of [their] multimodal data and corresponding AI models.” Hinge Health, which went public last year, was a breakout performer and has more than doubled its IPO price as of the close of Q2 2026. With Q1 revenue of $182M, up 47% YoY, and 23% free cash flow margin, Hinge cleared the “Rule of 40”2 benchmark by a wide margin, with AI driving operating leverage.

While select companies wait for their IPO moment, most digital health startups are eyeing the exit field for acquirers. Aligned with the overall M&A market, digital health M&A activity is elevated. H1 2026 saw 115 acquisitions of digital health companies, just above 2025’s pace of 199 annual deals and well above 2024’s 121. Of the deals this half, 71 were announced in Q2, the busiest M&A quarter since Q3 2021. Revenue cycle management is where consolidation ran hottest: IKS Health purchased TruBridge to extend its RCM platform to rural communities, Med-Metrix completed back-to-back deals for Vitalware and CanAide, and Innovaccer folded CaduceusHealth into its platform. Private equity placed larger bets, with Matt Holt’s closely-watched Thoreau Group signing a $12B agreement to take control of RCM player Ensemble Health. Incumbents were shopping too, as Roche acquired PathAI to bolster its diagnostic capabilities and Dexcom acquired long-time partner Nutrisense to extend its consumer metabolic offering. We’ll see whether this pace holds through the back half of the year.

Where we go from here

The effects of a transformative technology extend well beyond its first use cases, reshaping the systems around it over time. The investments and partnerships being made today reveal what founders and investors believe will endure. The destination remains the same—to make healthcare better for all—but the routes are shifting. Expectations are shifting, relationships are evolving, and so are the ways companies build lasting advantage.

Tap into insights and strategic guidance for enterprise companies with Rock Health Advisory.

Get in touch with the venture team at Rock Health Capital.

Join us in building a more equitable future at RockHealth.org.

And last but not least, stay plugged into the Rock Health community and all things digital health with the Rock Weekly.

Footnotes

- No pun intended.

- Calculated using year-over-year revenue growth plus free cash flow margin, a commonly used variation of the Rule of 40.