2023 year-end digital health funding: Break on through to the other side

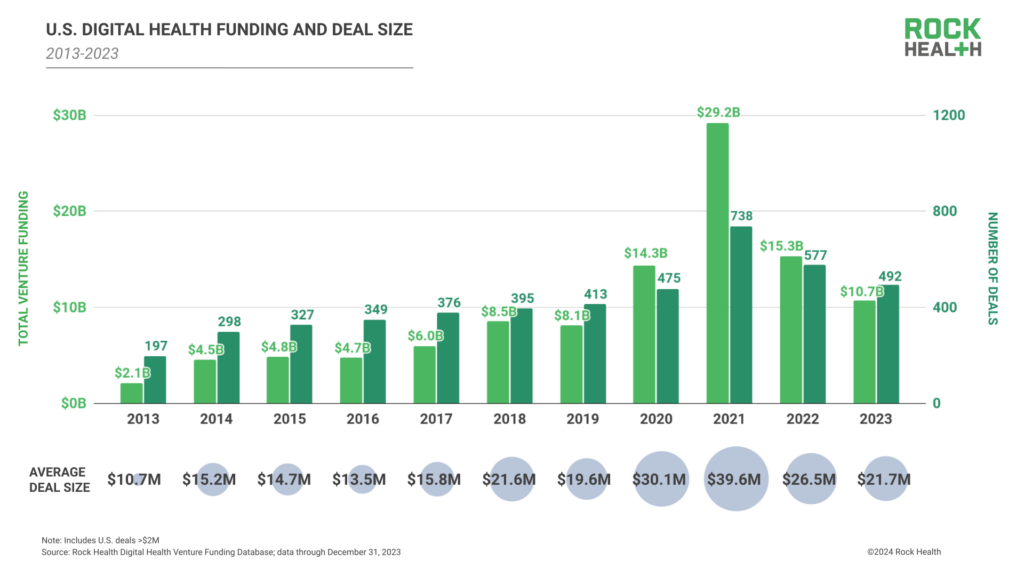

Following trends in the broader venture market, 2023 saw venture funding dive in digital health—continuing the downhill trajectory that began in 2022. Annual venture funding for 2023 closed out at $10.7B raised across 492 deals, the lowest amount of capital invested in U.S.-based digital health startups since 2019.

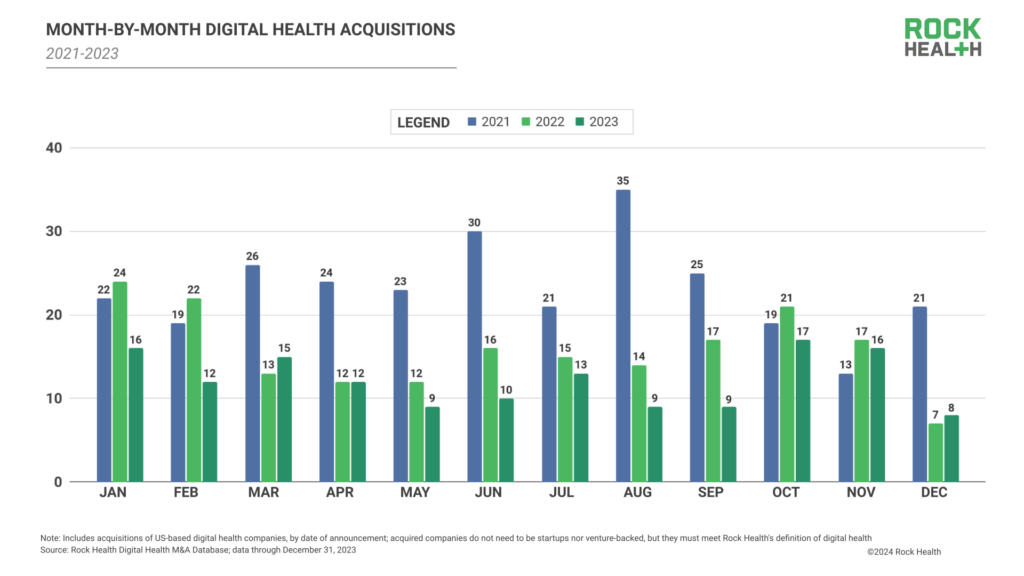

This year, the new beginnings of a macro funding cycle marked a year of transition. While we predicted 2023’s low funding numbers, some of the other activities we anticipated as a result of tough market conditions didn’t materialize. In 2023, M&A activity did not increase, even though cash-strapped startups were expected to look for buyers. And despite tightening capital availability and a sluggish exit market, there wasn’t a pronounced spike in startup shutdowns,1 though there were some notable bankruptcies and asset sales.

Why didn’t the startup market pan out as expected in a capital-constrained environment? For many players, 2023 was a year of looking for and locking down lifeline measures. To buy time, startups sought out creative financing measures such as extension rounds, unlabeled raises, and “silent” deals from existing investors. Most companies also made operational adjustments that reduced reliance on outside capital.

But if 2023 was a transition year defined by creative moves to stay afloat, 2024 will require some startups to face the music (raise at a reduced valuation, seek an acquisition or exit, or shut down). While hard on teams, investors, and customers alike, these shifts can set the sector up for brighter days ahead—a smaller cohort of stronger players, synergies through consolidated offerings, and a more successful IPO class. In this piece, we’ll reflect on the notable financing moves startups used to break on through 2023 and explore what may lie on the other side in 2024.

What 2023 showed us—and didn’t

In early 2023, we foresaw that high(er) interest rates and conservative investor behavior would mean that the year’s total funding would look more like 2019 than 2021-2022. Overall, 2023 digital health venture funding totaled $10.7B across 492 deals, the lowest annual total in four years. Q4 2023 was the lowest funding quarter since Q3 2019, with U.S. digital health startups raising $1.9B across 122 deals.

However, 2023’s low funding numbers likely don’t tell the whole story. Based on recent historical trends, venture-backed companies tend to raise every 12-18 months. However, the Rock Health Venture Funding Database shows that 81% of currently active venture-backed US-based digital health startups that raised a round in 2021 or earlier did not raise a subsequent labeled (i.e., designated by a letter, such as “Series A”) round by the end of 2023.2,3 How have many venture-backed companies survived two-plus years without a series raise? It’s possible that many startups got lean and mean to extend the cash they already had. But as we’ve written before, it’s also likely that a significant portion of startups that did not raise a labeled round in 2022-2023 turned to creative financing measures to stay afloat, which aren’t fully reflected in the annual funding numbers. To recap those measures and give some year-end perspective:

- Series extensions: 2023 saw a wave of extension raises, particularly at the A and B deal stages. Some examples include Mantra Health’s Series A extension (March 2023), Levels’ Series A extension (January 2023), Heard’s Series A extension (June 2023), Keona Health’s Series A-1 (August 2023), CarePredict’s Series A-3 (July 2023), Axuall’s Series B-1 (August 2023), and Genome Insight’s Series B-2 (November 2023). Extension raises, particularly at early stages, can sustain startups that haven’t yet nailed down key maturity markers like product-market fit or go-to-market strategy but need additional cash. For others, extension raises help startups compete, leveraging new financing to generate outcomes data or secure strategic investor guidance before the next raise. But extension rounds carry risks of their own. Because extension rounds are typically dilutive, these moves risk reducing founders’ and early investors’ ownership in proportion to the amount of new capital being raised. After an extension, the pressure is on for startups to nail down strategies against a ticking clock of the next raise cycle.

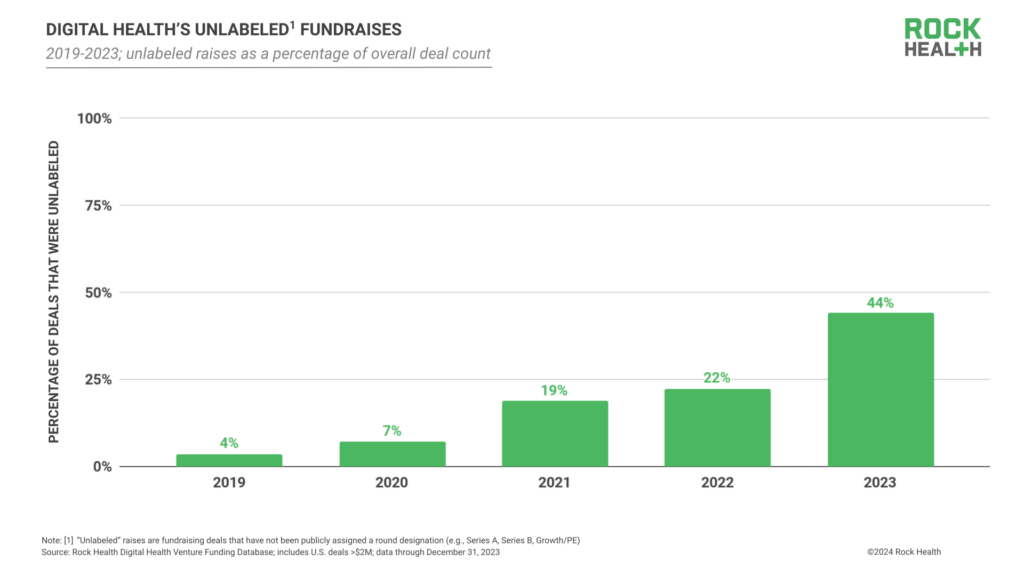

- Unlabeled rounds: In a new annual record, 44% of 2023’s fundraising deals were unlabeled (i.e., not designated by a letter, such as “Series C”). We previously reported on the rise of unlabeled rounds and noted that they, like series extensions, can serve up new capital to startups that haven’t yet reached the benchmarks expected for their next labeled raise. However, unlabeled funding leaves open questions about startups’ future raise timelines and these companies may need to raise again soon or risk folding.

- Silent rounds: We’ve seen and likewise heard from other digital health investors across the ecosystem about companies that have quietly accessed additional funding from their existing set of investors. There is no way to systematically track rounds that aren’t reported, but we surmise from the anecdata we have that 2023 saw more than its fair share of unannounced, inside-round financings. On the one hand, “silent rounds” can be more efficient, since only insiders (i.e., the existing VC investors who already know the company well) are investing in the round. On the other hand, when existing investors double down in a silent round, a company does not get feedback (or independent pricing) from the broader VC investment marketplace. In this respect, silent rounds may merely defer or even compound risks and difficult conversations they’re sometimes intended to avoid.

“Builders have been focused on weathering the storm in 2023. It’s always important to keep relationships with strategic investors warm. Even for companies who don’t need funding today, we want to ensure we’re setting ourselves up for successful conversations when the market presents opportunities again.” —Yoona Kim, Co-Founder and CEO, Arine4

For some companies, extension, unlabeled, or silent rounds may have bought just enough time to hit key commercial and outcome benchmarks. We also acknowledge that some outwardly operational companies might be on the path to shutdown, ramping down operations but not yet having officially closed doors.

For startups continuing forward, these creative financing measures are realistically one-time assists, and can’t be continuously relied upon if additional financing is needed. Startups that aren’t able to leverage funding to reach the requisite standards of their next deal stage will face tough decisions in 2024.

Facing reality in 2024

With transition funding options exhausted, startups won’t be able to avoid or delay major moments like fundraises or exits for much longer. For some, the next step will be returning to labeled fundraises, but at adjusted valuations. For others, it’s making a (public or private) exit, possibly with a lower price tag than expected. And for a final cohort, it means closing up shop. Here are our hunches for what’s to come in 2024.

Labeled raises will return

The cohort of startups that bought time in 2023 with creative financing will likely need to raise more substantial funding via labeled rounds in 2024. As these startups consider the case for their next raise, some will find themselves well-positioned for success; solid financials, exceptional founding teams, and proven outcomes data will set this class apart. However, others will find themselves less prepared to demonstrate the commercial maturity expected at their next labeled round and will need to evolve strategies to meet the mark and attract investor attention. Some may bolster their offering menus with new products or integrations in hot innovation areas like obesity care or generative AI, others will align themselves with new opportunities created by federal policy changes, and others will refine their go-to-market strategies to attract more revenue. If these startups ultimately can’t showcase the outcomes and growth expected to raise their next round, they are likely to face less attractive labeled funding opportunities at adjusted valuations (see: down rounds) or via restructured cap tables.

“The bar for healthcare AI due diligence is rising, thanks to federal transparency requirements as well as risk concerns from industry players like health systems. AI-enabled digital health startups that are more transparent about model training data sources, risk of model features, and data privacy & security practices will have a competitive advantage.” —Stanford Byers Center for Biodesign team; special thanks to Kavita Patel, Oliver O. Aalami, Paul Schmiedmayer, and Roderick (Rory) Thompson

M&A pace will accelerate

At the end of 2022, we expected M&A activity to take off, given startups’ depleted cash runways and more opportunities for acquirers to “buy low.” While there were some notable transitions across 2023—including acquisitions of startups such as online psychiatry provider startup Minded (November 2023) and sexual health testing solution Binx Health (December 2023) in Q4—an overall M&A swell didn’t materialize. Likely due in part to a combination of “higher for longer” interest rates and volatile capital markets early in the year, 2023 M&A volume was 23% lower than in 2022, with 146 total announced mergers/acquisitions of US-based digital health companies this year, compared to 2022’s 190. It’s worth noting that, just like funding data, our 2023 M&A data is likely incomplete, as some startups may have taken buyouts sans announcements, when deal terms weren’t exactly favorable.

In 2024, selling will be a potential path for cash-strapped companies, even if those sales come at lower-than-once-ideal prices—negotiations may drag on as parties face valuation sticking points. Others may pursue partial M&A, following in the footsteps of companies like Cano Health and divesting parts of the business to focus energy on winning initiatives. Startups working with enterprise customers may find themselves with acquisition offers from those partners. These types of arrangements could mutually benefit both parties, helping founders find a viable path forward and ensuring enterprises can sustain their work with valuable partners.

The public market cohort will recalibrate

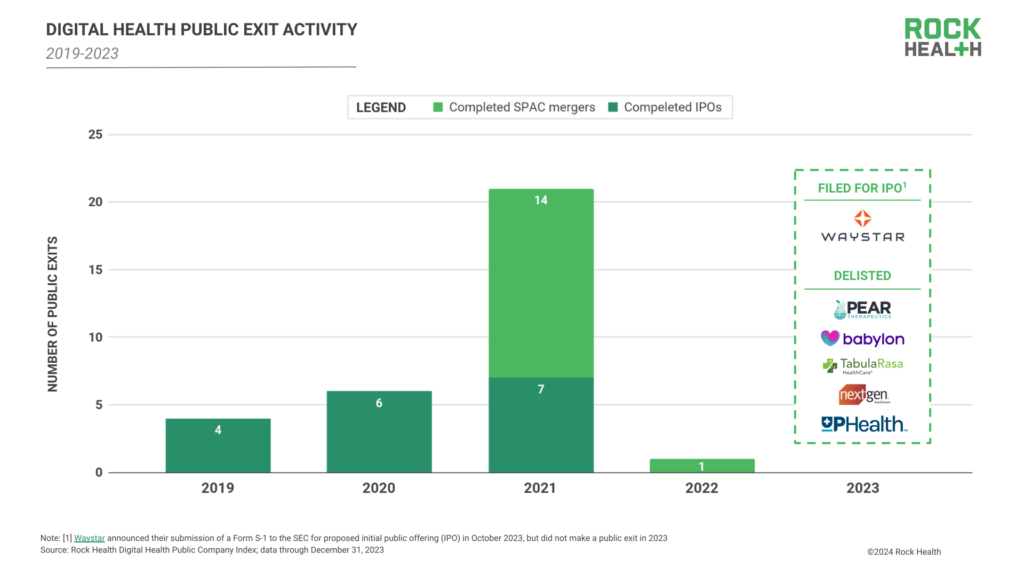

After a year without a single digital health public exit, a recomposition of the digital health public market in 2024 seems increasingly likely; faltering public companies will likely delist while late-stage players finally take aim at public exits.

A cohort of remaining publicly traded players faces the risk (or reality) of delisting. As of December 31, 2023, at least 17% of public digital health companies trading on the NASDAQ or NYSE were noncompliant with listing standards, having traded at or below $1 for over 30 consecutive business days. Akili Interactive and several others received listing non-compliance notifications. Better Therapeutics appealed a delisting determination, while UpHealth, Inc. was removed from the NYSE for failing to meet minimum average market cap requirements. With continued macroeconomic uncertainty, we expect the year ahead may bring more delistings. Though some companies may attempt to avoid delisting by leveraging stock restructuring or cutting down operational expenses, we expect that a few additional digital health companies will leave the public market altogether in 2024.

But as we noted in Q3, the strong public performance of other publicly traded digital health players may smooth the path for newcomers to exit onto the public markets. We may see select startups that have eyed an exit and delayed their debuts finally take the plunge next year, especially those that have achieved strong financials. With the combined measures of delisting and new IPOs, we expect a recalibration of the private digital health market will result in a stronger and more stable publicly traded cohort in the years ahead.

Some startups close, and others are born

Looking ahead, 2024 will be a year of recalibration and consolidation. Some startups will rally, finding that high capital efficiency and exceptional offerings pay off to secure them their next major fundraise. Others will need to make the tough call to wind down operations or accept lower-than-hoped-for M&A offers, particularly in saturated segments.

“The tough reality is that we likely created too many digital health companies over the last 10 to 12 quarters. The capital provided to these companies may have afforded them 15 to 18 months of additional runway. Now, many of them are back in the market, and it’s unlikely that all will receive more funding.” — Michael Greeley, Co-Founder and General Partner, Flare Capital Partners

Even though we’ll see teams and startups wind down in 2024—always a challenging, but expected reality of venture—the talent and ideas will carry on. Individuals may go on to problem-solve in new ways, responding to market dynamics by launching new ventures or innovating at enterprises. Assets that were sunset may find second lives in new companies or as a part of new platforms.

We’re also keeping an eye on emerging and developing segments like digital obesity care and value-based care enablement—2023’s flurry of Series A activity in these spaces may give way to new darlings in 2024. Though the “other side” may still seem uncertain, we expect a coming reset to ultimately create a more efficient, sustainable, and innovative digital health ecosystem.

Tap into insights and strategic guidance for enterprise companies with Rock Health Advisory.

Get in touch with the venture team at Rock Health Capital.

Join us in building a more equitable future at RockHealth.org.

And last but not least, stay plugged into the Rock Health community and all things digital health with the Rock Weekly.

Footnotes

- Though some startup shutdowns were likely unannounced, Rock Health data reports that less than 5% of venture-backed U.S. digital health companies (i.e., have raised >$2M) are no longer operating as of December 31, 2023. This rate has held relatively steady over the past several years, signaling that the pool of startups no longer operating remained relatively consistent to the proportion of all startups.

- Rock Health tracks U.S.-based companies that have raised at least $2M in venture capital and meet our definition of digital health. The startups include companies that still have active websites and have not announced being acquired, going public, or shutting down operations.

- This proportion is higher than in prior years. In comparison, 70% of active venture-backed US-based digital health startups that raised a round in 2020 or earlier had not raised a subsequent labeled round by the end of 2022. Seventy percent of active venture-backed US-based digital health startups that raised a round in 2019 or earlier had not raised a subsequent labeled round by the end of 2021.

- Arine is a Rock Health Capital portfolio company.