On the road to impact: Mile markers for early-stage digital health startups

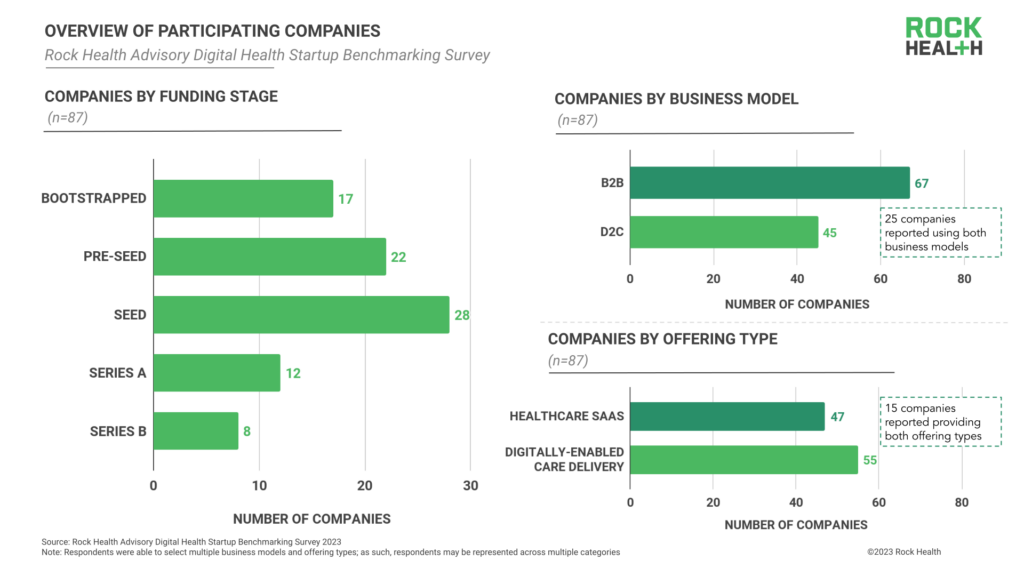

Running an early-stage company is a tough business. Unlike for public companies, there are no robust performance indicators to support financial planning and benchmarking across measures like profitability, customer acquisition cost, lifetime value, or business expenses. This challenge drove us to launch the 2023 Rock Health Digital Health Startup Benchmarking Survey (referred to as “the Survey”)—a survey across a collection of performance markers designed to serve as guideposts for early-stage digital health companies across funding stages, business models, and solution types. We’re grateful to the 87 bootstrapped and early-stage U.S. digital health companies (referred to as “respondents”) who participated.1,2

We hope this data will help light the way for innovators to come, and contribute to the growing knowledge base of how digital health businesses succeed in private markets. In this piece, we’ll share five top insights about early-stage startup performance in digital health from the survey:

1. Series B is a tipping point for growth, but not (yet) margins

2. Bootstrapping can be a viable path to profitability

3. CAC and LTV calculations are challenging for early-stage startups

4. Engagement metrics are the first step to robust outcomes

5. Navigating product versus sales and marketing spend is a balancing act

Series B is a tipping point for growth, but not (yet) margins

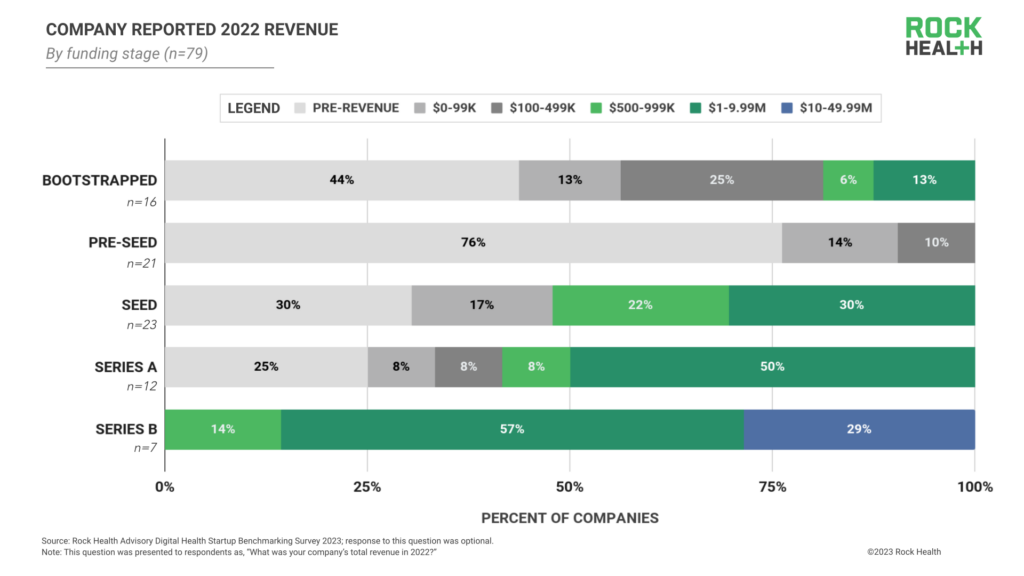

While Series A companies are generally building an MVP and testing product-market fit, Series B is a stage for growth, with funding deployed towards talent acquisition, scaling operations, business development, and sales. This dynamic was reflected in our Survey data, with Series B respondents reporting notable increases in revenue, recurring revenue, and higher rates of profitability relative to all other funding stages.

Series B companies reported greater and more consistent revenue relative to any other stage cohort. No Series B respondents reported being pre-revenue (compared to 25% of Series A respondents), and 29% reported annual revenues of $10M or more. Series B respondents also reported high levels of recurring revenue, a VC-revered metric. Across all Series B respondents, the average percent of revenue recurring was 81%, compared to an average of 54% within the Series A cohort.

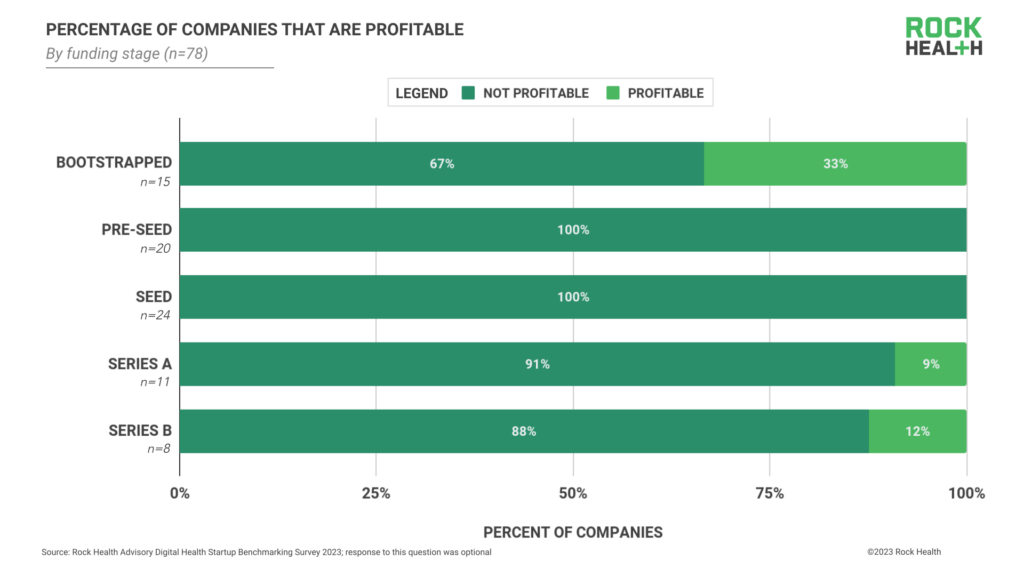

Whatever revenue footing Series B digital health startups gain is being reinvested into growth rather than focusing on profitability. Just 12% of Series B respondents reported being profitable, a small inch up from the 9% of Series A respondents reporting the same. While “growth over margins” has been a startup mindset these last few years, in today’s fundraising environment we may see more companies gunning for profitability sooner rather than later. It remains to be seen how investor expectations of growth versus profitability will evolve across early-stage digital health startups, and where negative cash-flow might still be tolerated.

“Today, investors have become more focused on cash management and profitability. At the same time, they’re less inclined to give founders the benefit of the doubt; they’re looking for more proof-points that founders can meet the milestones they set out to achieve. As a result, founders need to do more with less.

By Series A, we need to see undeniable evidence of product-market fit: that’s not always just revenue… it’s growth in the customer base, product usage, ACVs, and more. And by Series B, you better have all of that plus clear evidence of go-to-market fit, which should come with compelling unit economics.”

— Marissa Moore, Investor, OMERS Ventures

Bootstrapping can be a viable path to profitability

While venture-backed businesses are hunting for growth, bootstrapped ones are hunting for profitability. Rightly so—without a store of capital to draw from, profitability = viability. Survey data confirmed this dynamic, with more than 33% of bootstrapped respondents reporting profitability, compared to only 3% of all venture-backed Survey respondents.

In terms of revenue, 31% of bootstrapped respondents reported toplines between $100k and $1M in annual revenue, and 13% reported toplines between $1M and $10M. Bootstrapped respondents also reported 40% percent of total revenue as recurring—starkly different from their venture backed counterparts, where even the Pre-Seed cohort had a higher average of revenue recurring, with 47%. With lower recurring revenue, bootstrapped companies will need to contend with increased topline volatility relative to their venture-backed peers.

Although the reasons behind bootstrapping are different for each startup, necessity can drive invention. Financial constraints seem to be supporting boot-strapped companies in achieving profitability earlier–especially given that our cohort of bootstrapped respondents, on average, was approximately the same age as our Seed-stage respondents, none of whom had achieved profitability.

“With bootstrapped companies, you have to be very disciplined; even more in every single decision you make around spending. You’re thinking about each of the levers on your P&L from day one. If you have $0 to spend other than what you’ve put into the business, you have less flexibility to iterate and make mistakes.”

— Steve Kraus, Partner, Bessemer Venture Partners

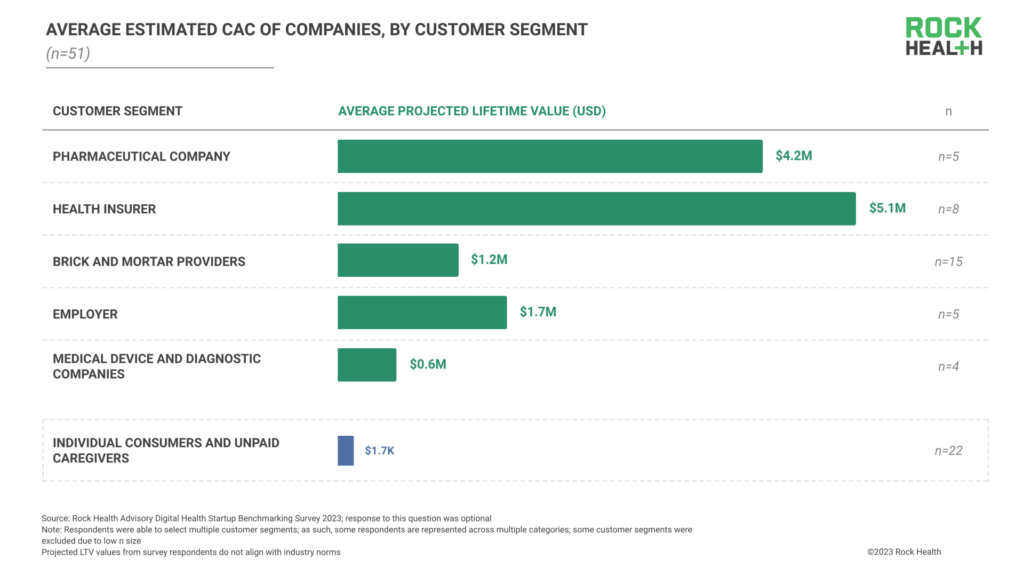

CAC and LTV calculations are challenging for early-stage startups

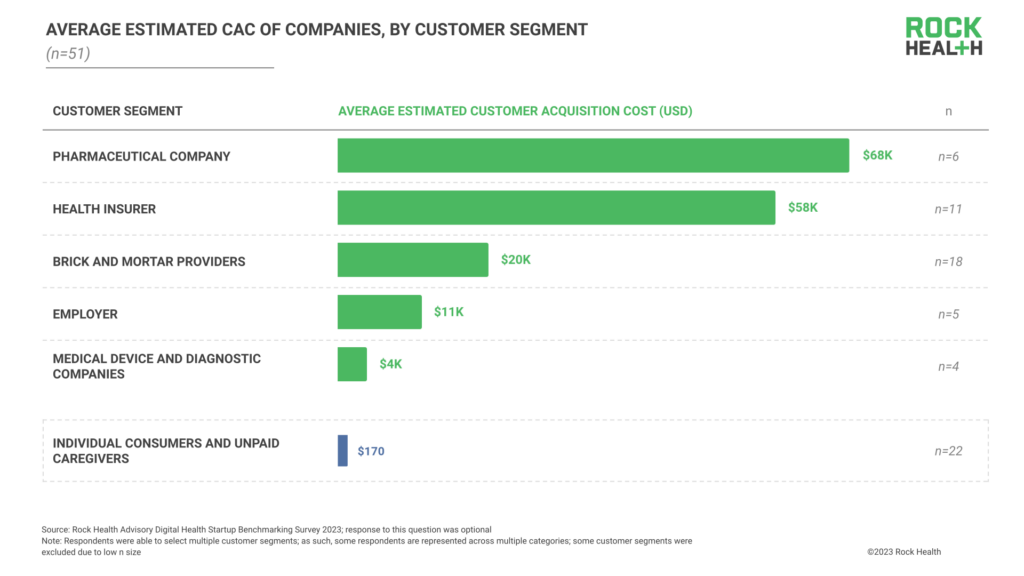

Across industries, customer acquisition cost (CAC) and customer lifetime value (LTV) are important metrics in evaluating growth trajectory and business model sustainability. Looking at CAC and LTV projections from Survey respondents, we noticed a few key things:

First, CAC varies significantly by type of customer. For respondents reported selling to consumers or unpaid caregivers, the average reported CAC was $170 and LTV—approximately $2k. Respondents serving enterprise customer segments reported significantly higher CAC and LTV than those selling to consumers directly, with wide variability among the types of enterprise customers served. Respondents reported spending $58k to acquire a payer customer and more than $68k to acquire a pharmaceutical customer, more than 3x the reported CAC for other enterprise customer segments like brick-and-mortar providers and employers. However, projected LTV for both of these customer segments were also the highest reported; respondents projected LTVs of $5.1M for each payer and $4.2M for each pharma customer.

Survey respondents’ reported LTV values for enterprise customers, as well as the resulting LTV:CAC ratios, far outpaced industry norms. For example, respondents projected an average LTV for employer customers at $1.7M alongside a CAC of $11k, generating a projected LTV:CAC ratio of 124x, or 25 times the industry norm. Our hypothesis is that early-stage digital health startups are underestimating CAC and overestimating LTV. Given that 38% of Survey respondents are pre-revenue, while others are early in their journeys, CAC and LTV projections are at-best an educated guess for that group of companies. For those generating revenue, early-stage startup operators are likely over-optimistic in predicting high customer spend and low customer churn, metrics that fuel investor pitches and raise company valuations.

“Building durable businesses that pair high quality care and patient experience with strong economics is essential in today’s market. You can’t have one or the other but need both. That means a return to first business principles — ensuring strong unit economics are in place and managing metrics such as payback on CAC is key to supporting profitable growth and is the new reality for companies and startups.”

— Carolyn Witte, Co-Founder & CEO, Tia

While realistic estimates are necessary for growth planning and go-to-market decisions, there is also a hesitance from founders to avoid undervaluing their business and its potential for market capture. For operators, investors, and enterprise partners, it’s important to be critical in calculating and evaluating CAC and LTV, and to align on how to interpret these measures in the context of different business decisions (e.g., investment, partnership, go-to-market).

Engagement metrics are the first steps to robust outcomes

While business performance metrics are strong indicators of a company’s financial success, outcomes metrics are critical for determining a solution’s impact. Of Survey respondents, 94% reported tracking some form of outcomes metrics, with 82% tracking more than one.

Regardless of stage and business model, engagement outcomes were the most commonly tracked among respondents (82%), followed by clinical outcomes (77%), and economic outcomes (60%). On average, each respondent company reported tracking two engagement outcome metrics, two clinical outcome metrics, and one economic outcome metric.

Of engagement outcomes, customer satisfaction was the most commonly tracked metric (67% of respondents), followed by end-user experience (e.g., ease of use) (59%). For clinical outcomes, respondents most commonly tracked ability to reduce symptoms or improve a condition (56%), followed by quality of life measures (32%), and medication delivery and adherence (29%). These align with the traditional performance and outcomes metrics that have guided healthcare in the past. For economic outcomes, respondents most commonly reported tracking money saved per customer (40%), utilization (29%), and new customer revenue (27%).

It’s a non-negotiable that startups work toward demonstrating clinical impact and ROI, especially in today’s market environment. Though clinical and economic metrics are most likely to “move the needle” in investment and sales conversations, they can take years to collect and assess. For startups balancing speed-to-outcomes and quality-of-outcomes, an “engagement first, clinical/economic later” approach might help to toe the line.

“As an early-stage company, you might not have gold-standard outcome metrics like ROI or academic studies. But you can tell us about engagement and what clinical metrics would be important to track. How many users are engaging with your product? How long do they engage? Lay the pathway for how you’re going to build from engagement toward moving the needle in clinical outcomes and demonstrating ROI.”

— Sofia Guerra, Vice President, Bessemer Venture Partners

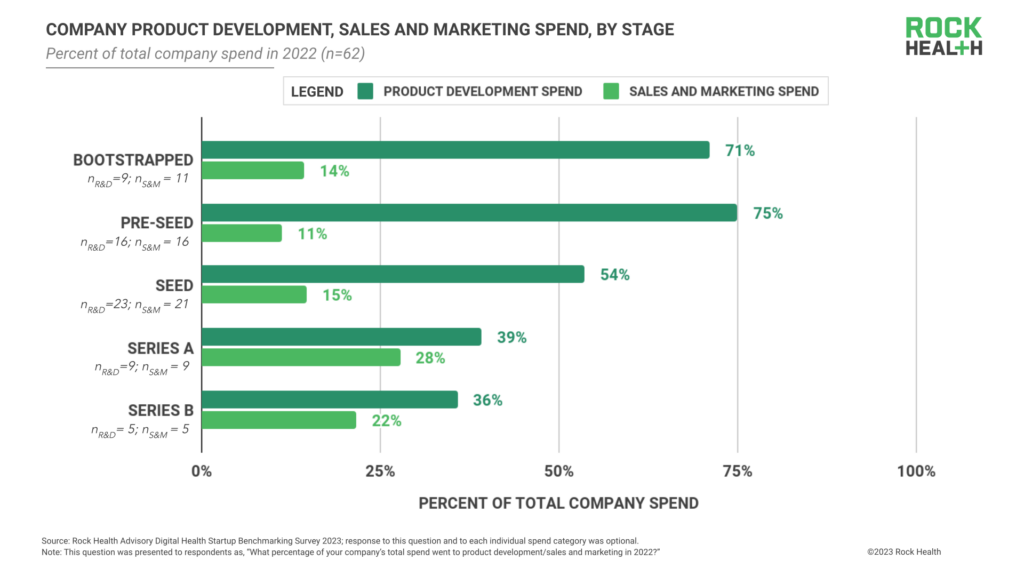

Navigating product versus sales and marketing spend is a balancing act

With limited pools of capital, early-stage digital health startups must make tradeoffs between investing in product research and development (R&D) and investing in sales and marketing (S&M). These tradeoffs are especially hard for digital health startups developing new technologies or care approaches, which require intensive product development and a head start on customer education and market pioneering.

As expected, bootstrapped and very early-stage respondents (i.e., Pre-Seed and Seed stage) reported spending more on product development than on sales and marketing, to the tune of 3-7x. Series A and B-stage respondents reported sales and marketing spend closer to—though still less than—product development spend. This data aligns with research from Bessemer Venture Partners, which shows that sales and marketing spend tends to surpass product R&D spend for companies with over $10M in annual recurring revenue (an ARR beyond most of our early-stage Survey respondents).

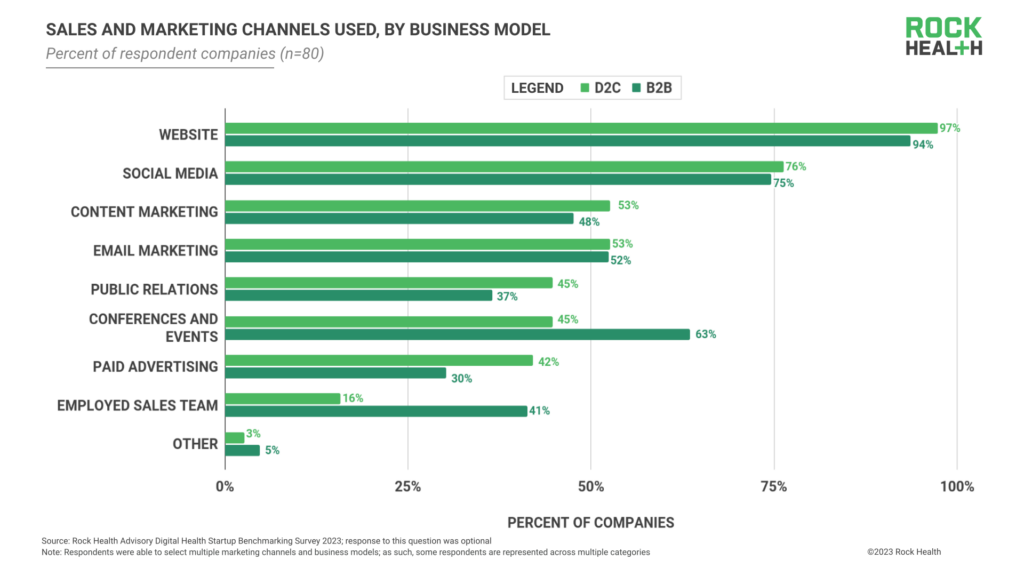

Within sales and marketing, startups must make more tradeoffs between the types of marketing channels they use. Seventy-five percent of startup respondents reported using websites and social media, while more than 50% of respondents reported using email marketing. Interestingly, content marketing was prioritized by roughly 50% of respondents utilizing both B2B and D2C business models, even though this approach was historically more common in D2C business models. However, B2B digital health sales and marketing strategies also still incorporate traditional enterprise marketing approaches, with 41% of B2B respondents utilizing an employed sales team and 63% selling and marketing at industry conferences or events.

While both sales and marketing and product development are key to launching a successful business, identifying the right balance between S&M and R&D spend can help protect margins while making the most of market appetite—and ensuring the ability to deliver on what’s being sold.

“Build it and they will come’ rarely happens in healthcare. Go-to-market is the hardest part of healthcare and separates new technology from sustainable companies. Being able to market and sell your vision is one of the most important criteria we look at when evaluating an investment.”

— Annie Collins, Investor, Bio + Health, Andreessen Horowitz

A starting point for early stage benchmarks

These insights reflect just a portion of the challenges and questions that digital health startups and their founders face, especially in a challenging funding environment and an increasingly competitive digital health landscape. We hope that these sector benchmarks for early-stage startups will help founders, investors, and enterprise partners alike orient themselves to practical, realistic milestones that better enable chances of viability and success.

Footnotes

- Survey respondents were recruited through direct outreach and completed the survey from March through August 2023. Outreach methods included direct contact (e.g., emails) to early-stage founders, secondary distribution between founders, and LinkedIn promotion. Data was cleaned to eliminate false responses and select for early-stage respondents.

- A number of Survey questions were optional. Cohort analyses were completed by the number of individuals who responded to a particular question, resulting in different n-sizes denoted in all visualizations.

Tap into insights and strategic guidance for enterprise companies with Rock Health Advisory.

Get in touch with the venture team at Rock Health Capital.

Join us in building a more equitable future at RockHealth.org.

And last but not least, stay plugged into the Rock Health community and all things digital health with the Rock Weekly.