Q3 2023 digital health funding: Smaller but mighty

If Q1 and Q2 2023 charted the course for a brave new venture market, Q3 gave clear signals of the world emerging. While the digital health sector experienced significant reductions in funding and deal volume, quarterly trends are stabilizing within a new investment cycle. Investors are funding startups exploring new treatment pathways and tackling nonclinical workflow solutions. And though 2023 has witnessed some notable bankruptcies of former IPO darlings, public market performance of the full digital health cohort has steadied. Taking this all together, digital health’s new reality is “smaller but mighty.” In this piece, we’ll walk through what this new sector mindset requires of founders, funders, and healthcare organizations.

The “new normal” within a new funding cycle

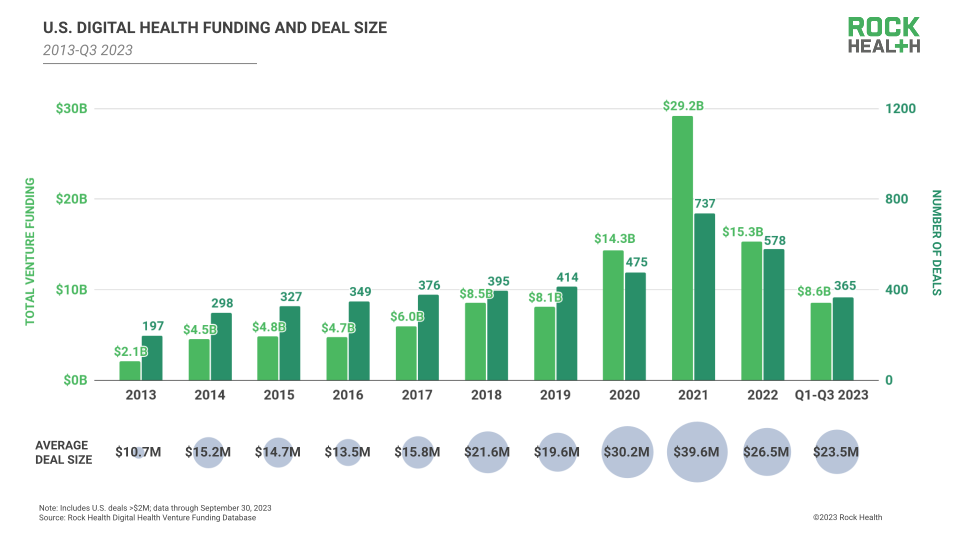

In Q3 2023, U.S. digital health startups raised $2.5B across 119 deals, the second-lowest quarter by funding total since Q4 2019. This brings 2023’s totals to date to $8.6B raised across 365 deals.

Notably, Q3 2023 is the fourth of the five past quarters to log funding in the $2B range, joined by Q3 2022, Q4 2022, and Q2 2023. Additionally, all five of the past five quarters have logged deals in the low 100s, topping out at 131 deals in Q1 2023. These past five quarters help to establish new quarterly funding and deal count norms within this emerging digital health funding cycle.

Contributing factors to this lower level of funding are varied and intertwined. Anticipation of a slower economy and the arrival of high interest rates impacted venture funds’ ability to raise capital, reducing funding for startup investment. Lower startup valuations and limited IPO activity reduced funds’ portfolio valuations and delayed distributions to limited partners (LPs), fundamentally reducing capital available for new investments. These forces fostered a more conservative mindset among investors (particularly generalist and crossover funds), who are now doing fewer deals and negotiating harder on deal terms—further feeding a lower funding cycle.

These funding dynamics make the startup fundraising environment anything but easy. Down rounds remain a concern, and startups and their investors are having difficult conversations about financing the next phases of growth at the expense of founder and prior investor dilution. In a trend we discussed last quarter, some founders (particularly at early- to mid-stages of their business) may be trying to reduce these dilution risks by raising extension or otherwise unlabeled rounds. This is a likely contributor to 2023’s sparse mid-stage series announcements, with only 34 Series B raises so far this year (compared to last year’s 82) and 11 Series C raises (compared to last year’s 35, and the lowest number we have on record since we began tracking digital health venture funding in 2011).

“Healthcare is radically changing but the overall capital markets have changed profoundly too. Transitioning from a low-interest environment is hard for early-stage startups, but it’s even harder for mid-stage companies that have to pivot to a new game in real time. It’s like going from football to playing soccer—the rules will be different, and the teams and strategies will also need to shift.”

— Emily Melton, Founder and Managing Partner, Threshold Ventures, shared at Rock Health Summit

Ultimately, we expect this incipient funding cycle will bring with it a new market equilibrium where startups and investors are both able to find upside. In the meantime, as digital health companies transition between the old equilibrium and new, founders and investors will need to continue navigating difficult conversations around valuation adjustment and ownership dilution.

“The down rounds are here, and we’re starting to see some recapitalizations as well. Today’s deal terms might be challenging for startups that are used to a prior world of 10-20x (and greater) valuations. But startups need to tackle these transitions head-on and possibly take the pain of down rounds. The focus should be on keeping terms simple and incentivizing operating teams.”

— Michael Esquivel, Partner, Fenwick & West LLP, shared at Rock Health Summit

Funding shifts to disease treatment, nonclinical workflow, and value-based care

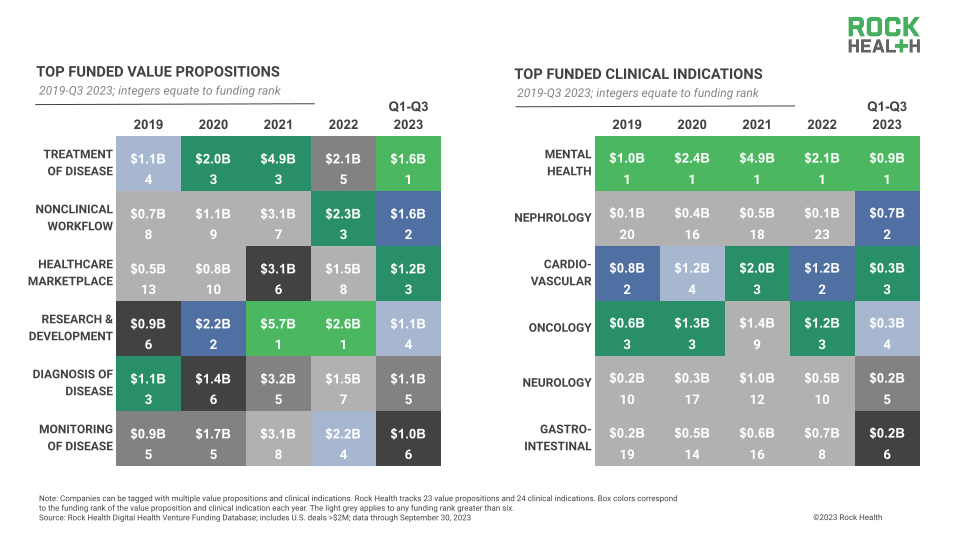

Despite a lower deal count and funding pot thus far in 2023, by Q3 clear patterns emerged among digital health investments. Notably, funding shifted away from pandemic-era focuses of on-demand healthcare and life science R&D catalysts (top investment areas throughout 2021 and 2022) toward digital health products and services that support disease treatment, nonclinical workflow, and management of complex conditions such as kidney disease.

Treatment of disease nabbed the top funding spot by digital health value proposition (type of product or service offered), with $1.64B raised from Q1-Q3 2023. Some fundraises in this category went to comprehensive virtual clinics like Rock Health port co Vivante Health ($31M), which offers integrated telemedicine, nutrition coaching, and self-guided modules for digestive health. Funding for nonclinical workflow solutions raised $1.59B from Q1-Q3 2023, claiming the number two spot. Players in this space are tackling tasks ranging from durable medical equipment management (Synapse Health, $25M) to revenue cycle management (Collectly, $29M), to patient scheduling and communication (Keona Health, $7M).

Mental health remained the top-funded clinical indication among digital health startups ($0.9B deployed year-to-date), while nephrology gained sleeper hit status, raising $0.7B so far in 2023 for second place—up from just $54M raised all of last year. Increasingly, investments across both specialties focused on digital health startups enabling value-based care (VBC) arrangements or taking on risk themselves. For example, Better Life Partners ($26.5M) has been recognized as a value-based leader in substance use disorder, mental health, and harm reduction, and Healthmap Solutions ($100M) serves payers and at-risk providers seeking VBC solutions for chronic kidney disease. As related policy initiatives gain momentum and large healthcare enterprises dig deeper into VBC models, VBC enablement will become an important component of startups’ commercial roadmaps and will drive enterprise partnerships. This will be particularly true in high-cost therapeutic areas like mental health, kidney care, cardiovascular care, and oncology—not-so-coincidentally the top four clinical indications by funding on our Q3 2023 chart.

“If a startup can drive down the total cost of care in a risk-based arrangement, that’s a huge value for payers and other customer organizations. Until recently, most digital health investors have focused on VBC enablement for primary care. Now investors are pursuing the white space of VBC enablement for specialty care needs.”

— Marissa Moore, Investor, OMERS Ventures

Digital health’s public market performance

In 2023, the entire financial market has been feeling the thirst from the IPO drought. Within the digital health sector the feeling was even more pronounced, exacerbated by two of its publicly-traded players (Pear Therapeutics and Babylon Health) filing for bankruptcy and another selling to a private equity firm (NextGen Healthcare).

While some of these headlines may feel like notes of the same worrisome chord for publicly-traded digital health companies, it’s important to consider their individual circumstances. Pear’s closure reflected the company’s difficulty securing payer reimbursement for its prescription digital therapeutics. Babylon folded after losing major contracts, in part due to operational scrutiny. Meanwhile, NextGen’s decision to go private was motivated by the desire for more strategic flexibility and possibly by concerns stemming from a federal investigation. While a challenging financial climate likely exacerbated each company’s headaches, their situations were distinct from one another.

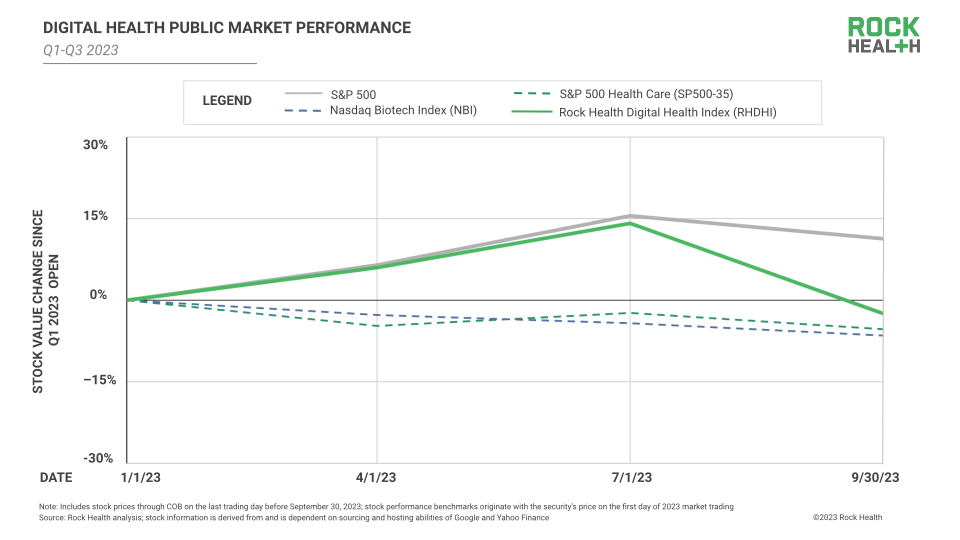

Rather, these headlines may be diverting attention from the digital health cohort’s overall public market performance trajectory. From the opening of Q1 to the close of Q3 2023, the Rock Health Digital Health Index (RHDHI), which averages the stock performance of digital health companies trading on the NASDAQ and NYSE1, underperformed the S&P 500, but beat out the S&P 500 Health Care (SP500-35) and Nasdaq Biotechnology Index (NBI).

RHDHI’s Q1-Q3 2023 trajectory was buoyed by strong performances from companies like Teladoc Health, whose Q2 2023 earnings beat Wall Street expectations—thanks to productivity investments for its BetterHelp therapists (improving the business line’s gross margin), as well its whole-person approach to GLP-1-assisted weight loss treatments (an enticing proposition for payer customers). Similarly, in its Q2 earnings report, Hims & Hers raised its full year 2023 outlook, given 70%+ year-over-year increases in its number of subscribers and topline revenue as well as the anticipated launch of its weight loss business line by the end of the year. And let’s not forget medical documentation player and Rock Health port co Augmedix, which grew revenue and improved gross margins year-over-year in the second quarter while preparing for the commercial rollout of its generative AI medical scribe technology, Augmedix Go.

Relatively stable stock performance, in part fueled by new innovation opportunities (GLP-1s, generative AI), helps instill confidence in the public market’s ability to value and support the overall digital health cohort. For some players like Akili Interactive, public market pressures may contribute to commercial pivots that ultimately help shore up long-term business viability. And with new (non-sector) public market players like Instacart dipping their toes into health initiatives, digital health companies may begin to consider reviving their plans for the public market.

Small(er) and steady wins the race

Q3 2023 delivered a steady stream of small(er) wins for the digital health sector: a stabilized funding cadence, investment shifts toward high-priority needs of workflow support and value-based care enablement, and signals of budding confidence from the public market. This mindset shift doesn’t mean things feel comfortable, particularly for founders who are navigating important transitions in fundraising and commercialization strategies. However, it’s our hope that investors and entrepreneurs can start finding a more predictable rhythm, knowing what this tighter market requires.

Tap into insights and strategic guidance for enterprise companies with Rock Health Advisory.

Get in touch with the venture team at Rock Health Capital.

Join us in building a more equitable future at RockHealth.org.

And last but not least, stay plugged into the Rock Health community and all things digital health with the Rock Weekly.

Footnote

- Pear Therapeutics (PEARQ), Babylon Holdings (BBLN), and NextGen Healthcare (NXGN) were all included within the RHDHI until their exits from the NYSE or NASDAQ were announced. NextGen Healthcare was removed from the RHDHI even though it is still trading, in line with Rock Health’s methodology of tracking M&A deals by date of announcement rather than by date of deal close.