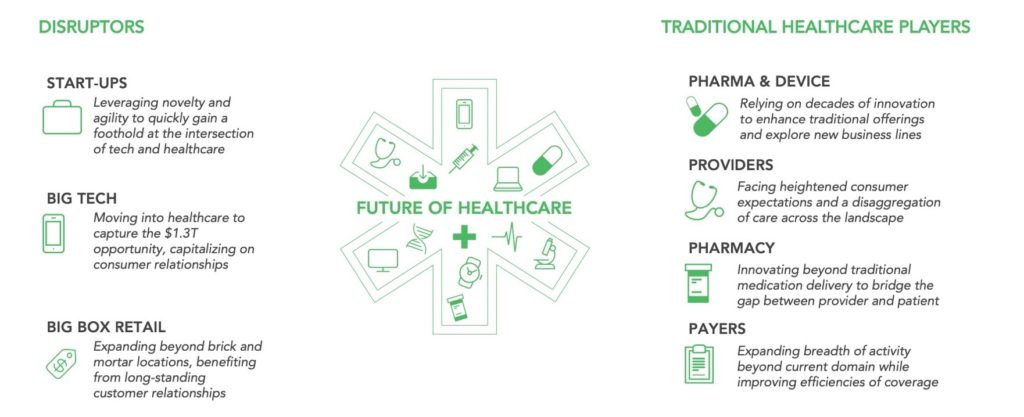

Where will you stand in healthcare’s new world order?

The fact that the healthcare industry is on the verge of disruption has been the topic of conversation for a long time. If there’s anything 2020 has taught us, it’s that the digital disruption of healthcare is inevitable, in fact it’s already here. All players, incumbents and disruptors alike, are now including digital as a cornerstone of their strategy, but the open question remains, who will be the winners in the new world order? Disruptors—startups, big tech, and retail—have the advantages of agility, and non-healthcare assets to bring to the game (think consumerism, AI, retail footprint), but incumbents have years of experience battling with the beast that is the US healthcare system.

To compete in the future of healthcare incumbents need to be agile enough to recognize emergent threats to their business and understand the strengths of those with whom they are competing (both fellow incumbents and disruptors) so they can adjust their strategies accordingly. Determining where to play and how to win on a different playing field requires hard strategic choices and consideration of the capabilities and assets needed–which can be built or acquired, and which will require partnerships.

Disruptor 1: Digital health startups coming of age

The digital health ecosystem, with over $49B invested in the last ten years, 12 digital health IPOs in the past eighteen months, and 24 $100M+ digital health venture deals so far this year has come of age1. Look no further than the IPOs, SPACs and mega rounds this year, most recently Outset Medical, Amwell and GoodRx via SPACs, and Ro with a $200M Series C.

These startups, now maturing healthcare companies, are well funded, have scaled and are now making bigger strategic moves. Earlier this year, the dramatic $18.5B Teladoc Livongo megadeal served as the starter pistol for what we anticipate to be a virtual care platform arms race (stay tuned for our next blog post in the series to go deeper on the platform wars). Since then, Amwell went public and experienced 80%+ growth in valuation from its IPO price of $18 to trading at around $33 per share2. Now all eyes are trained on other leading digital health startups – including Doctor on Demand, MDLive, and Omada Health–as speculation abounds on what could be next.

“It’s still very early in digital care, and it’s under-appreciated how big some of these companies can become.” —Sean Duffy of Omada Health

For incumbents looking at startups and wondering what is driving that growth, we’d highlight strengths in innovation, risk taking, and agility. As an example of that agility, with the arrival of COVID-19 digital health companies such as Collective Health quickly pivoted to creating solutions to support the back to work market. As early as May, Collective Go was announced to provide employee health screening and enterprise software for monitoring symptoms, test results, and compliance reporting.

Disruptor 2: Big tech’s big announcements turn into traditional infrastructure land grabs

Big tech started off with strategies to upend the healthcare system, however, a few high profile lessons learned for Microsoft and Google, has most Big tech companies now focused on creating the tech infrastructure and backbone that others can build upon. Recently, the focus has landed most prominently on cloud computing that will power the ecosystem including Microsoft’s Cloud for Healthcare and Google’s $100M investment in Amwell, which will use Google Cloud.

In addition, these organizations have been flexing their big data and analytics capabilities, developing algorithms to enhance both research and development and clinical platforms. Alphabet subsidiary, Verily, has been focused in R&D—crunching the data gathered from their study watch to develop digital biomarkers. Microsoft has been focused on digitally-enabled tools for clinical practice, developing artificial intelligence solutions through partnerships with Nuance, Humana, and Providence–while also launching a $40M initiative AI for Health. Apple is also in on the game with FDA cleared atrial fibrillation detection and other biomarkers integrated into the Apple Watch.

Consumers have reservations about big tech’s infrastructure and insights play. Multiple tech giants have faced backlash for collection of identifiable personal health data—for example, the public outcry following the discovery of Google’s Project Nightingale. This should come as no surprise given only 10% of consumers would be willing to share health information with tech companies. Despite headwinds, tech giants are going to be principal players in developing technologies that the rest of healthcare depends on.

Disruptor 3: Big Box Retail treating patients like the consumers they are

Big box retailers have been making big bets on healthcare. Best Buy has been focused on serving healthcare’s youngest and oldest consumers–selling Tyto Care’s telehealth platform and Kinsia smart thermometer for use in pediatrics while acquiring GreatCall and launching a flip phone for seniors. Meanwhile Walmart Health has launched 13 retail clinics (with plans for 22 more), acquired CareZone’s prescription management platform, formed a partnership with Oak Street Health to incorporate primary care services, and announced Medicare health plans in time for 2021 open enrollment.

“Walmart’s healthcare strategy is about enabling patients to ‘choose their own adventure’ for how they access care: in the way they want to, and at a price they can afford.” —Marcus Osborne, SVP Walmart Health3

Big box retailers have foot traffic that gives them a leg up against their digital-first competitors in serving populations who don’t have or don’t want to access care virtually. Pre-pandemic around 140M customers visited a Walmart in person or online every week. According to Marcus Osborne, Senior Vice President of Walmart Health, “Even with COVID, [we’ve] seen people who don’t want to go through a telehealth channel or a digital channel”. With more than 5,000 stores and clubs nationwide, and a growing online and mobile footprint, Walmart’s existing omnichannel presence provides the kind of reliable, trusted experiences traditional provider systems struggle to replicate.

“You already trust us to install tech, a refrigerator, to set up smart homes. That smart home ports easily to tech-enabled healthcare. With things like sensors that collect clinical data, that environment is ripe for care delivery.” —Daniel Grossman, CMO Best Buy3

Amazon: an anomaly

Each time Amazon lists a job description that even squeaks of a healthcare background there’s a new theory of how Jeff Bezos is going to change the industry. First it was the Amazon, Berkshire Hathaway and J.P. Morgan joint venture (now known as Haven Healthcare), then the acquisition of PillPack, the launch of employee health clinic Amazon Care, and most recently a new health-tracking smartwatch, Halo.

What makes Amazon so unique though is not simply its gargantuan size but rather that the organization is essentially a hybrid between a tech giant and a big box retailer–benefiting from the advantages of both archetypes. With AWS Cloud services and natural language processing associated with Alexa, Amazon is positioned just as well as other tech giants to offer new data infrastructure and AI-enabled applications. Amazon–like other big box retailers–also has a national footprint in the form of an expansive distribution network inclusive of fulfillment centers, a fleet of delivery vans, and even its own airline. The company has also established consumer-centric relationships of trust through its Prime membership with perks.

Incumbents moving to capture the emerging opportunities

Healthcare incumbents’ people-heavy service models, long development timelines, and risk-averse nature do not make them the best fit for digital innovation. There is a graveyard full of unused digital solutions developed by incumbent healthcare companies (we won’t name names). However, prescient incumbents have been making bold moves into the digital health realm, often leveraging partnerships with disruptors to expand into uncharted (for them) territory.

For example, UnitedHealth Group’s Optum subsidiary continued its march into care delivery when they acquired telemedicine company AbleTo. Parent company UnitedHealth launched level2 a digital health program for type 2 diabetes and acquired DivvyDose to compete in the digital pharmacy space. There’s even been recent speculation of a potential deal with AmWell.

Pharmaceutical companies too are exploring ways to expand their role in healthcare. Multiple organizations have formed partnerships with digital therapeutics start-ups, for example, Novartis partnering with Pear Therapeutics to co-develop two digital therapeutics for multiple sclerosis and schizophrenia. More recently, Boehringer Ingelheim announced a $500M deal with Click Therapeutics to co-develop and commercialize treatments in schizophrenia.

Finally, health systems are also getting in on the action with digital spinoffs. For example, Providence launched Xealth, a digital health marketplace which uses patient data to recommend services, and Intermountain established Castell, which uses digital analytics to help providers, payers and other stakeholders transition to value-based care.

The “so what?”

Healthcare is notorious for disappointing new entrants looking to carve out space in the market through transformational business models. Given the current economic environment, between the pandemic, the national debt, and the unaffordability of healthcare, that will be even more challenging as innovators will need to prove their value to a cautious set of customers paying the check. One certainty is that digitally-enabled services are at the center of everyone’s plan to deliver value. Clear strategic choices on where to play, how to win, and a hard look at the capabilities needed to get there will separate winners from also-rans.

Footnotes

1Source: Rock Health Venture Funding Database

2Source: Rock Health’s Digital Health Public Company Index as of October 26, 2020

3Source: Rock Health Summit