Digital health exits 2016 YTD: 112 digital health acquisitions and two IPOs

As a follow-up to last week’s post on 10 things you should know about digital health funding YTD, we dug even deeper and found 10 key takeaways about the exit landscape for venture-backed companies in digital health.

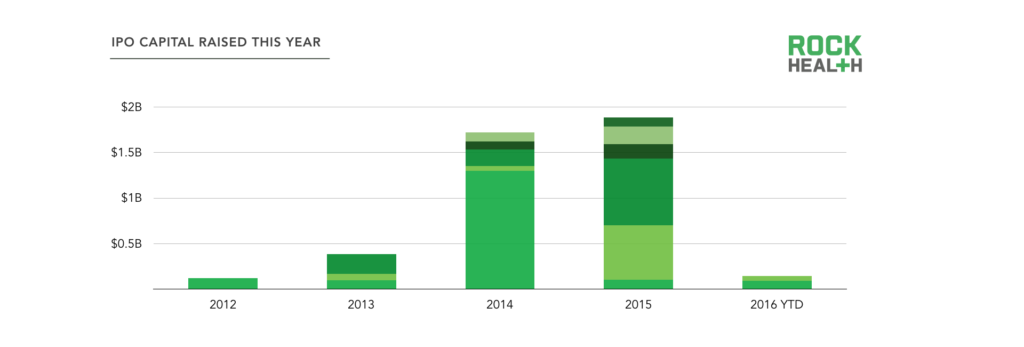

1. Only two digital health companies have IPO’d this year (compared to a total of six in 2015). Those IPOs include NantHealth ($91M offering) and Tabula Rasa HealthCare ($51.6M offering).

2. Together, these IPOs represent the smallest total amount raised in the public markets by digital health companies since 2012.

Variations in color denote separate public offerings. Two colors represent two public offerings, three colors represent three public offerings, etc.

3. The next digital health IPO will be San Francisco-based iRhythm (S-1 filed on 09/23/2016). The company claims it now has the world’s largest repository of ambulatory echocardiogram data with more than 125 million hours of heartbeats logged from 500,000 patients. They raked in $36M in 2015 from sales of their ZIO Service (mostly from commercial payers and government agencies), but ended the year with a $22.8M net loss.

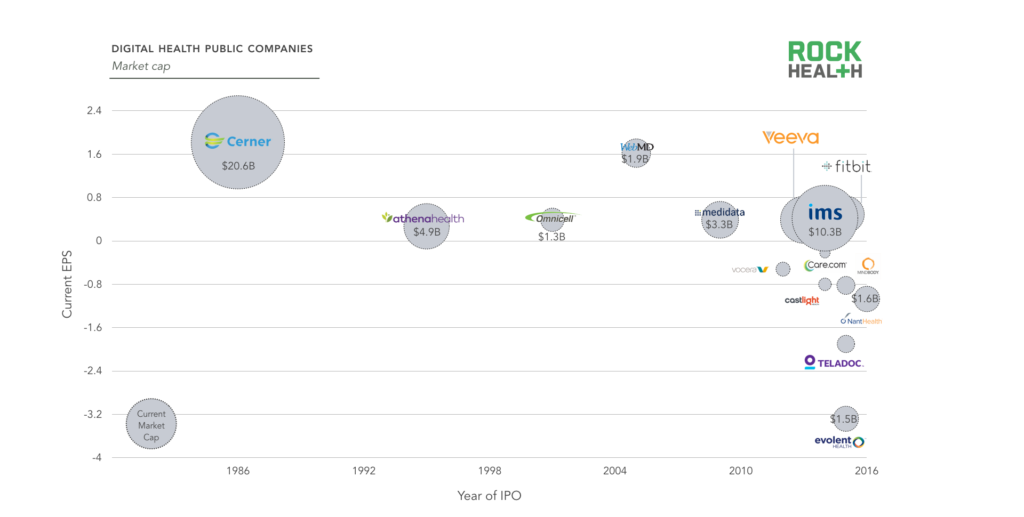

4. Half of the 30 companies in our Public Digital Health Company Index are profitable on a shareholder basis, with a positive EPS. Those that are profitable tend to be older firms, which have been public since before the turn of the century (and before the term “digital health” was popularized).

5. The digital health stocks with the biggest returns YTD are Evolent Health (up 114%) and Vocera (up 54%).The biggest losses YTD are FitBit (down 53%) and Computer Programs and Systems (down 47%). Thirteen of the stocks in our index are down, while 17 are up from the start of the year.

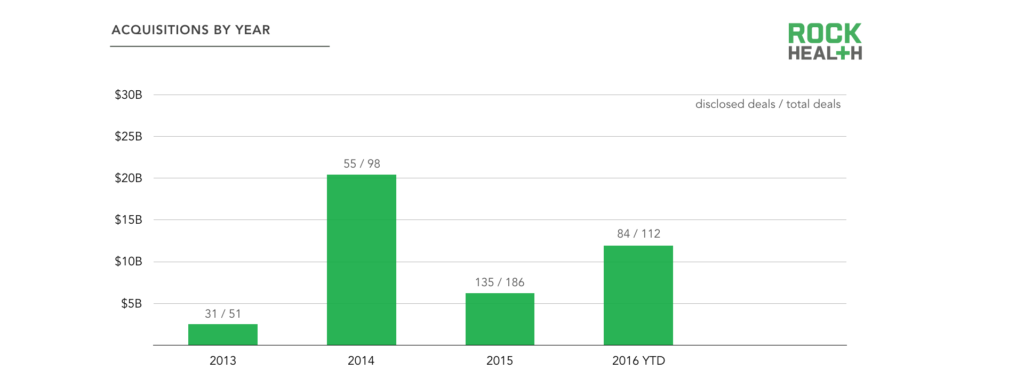

6. While IPOs only brought in $142M in value, acquisitions brought in at least 80x that amount. We counted 112 digital health acquisitions YTD, of which only 28 had disclosed amounts. Year over year (YoY), the number of deals is slightly down (compared to 146 at the end of Q3 2015), but the amount of disclosed funding ($12B) is already almost twice that of all of 2015.

7. Other digital health companies continue to be the most active acquirers of digital health companies, representing over half of all acquisitions in 2016 (51%). Technology companies, like Apple and IBM, rank second, having completed 14 deals this year (12%). Twenty percent of acquired companies were scooped up by companies outside of healthcare. While this number is slightly down on a YoY basis (26% in 2015), it shows that there is still significant interest in digital health beyond the traditional industry stakeholders and reiterates the importance of health in every part of the market.

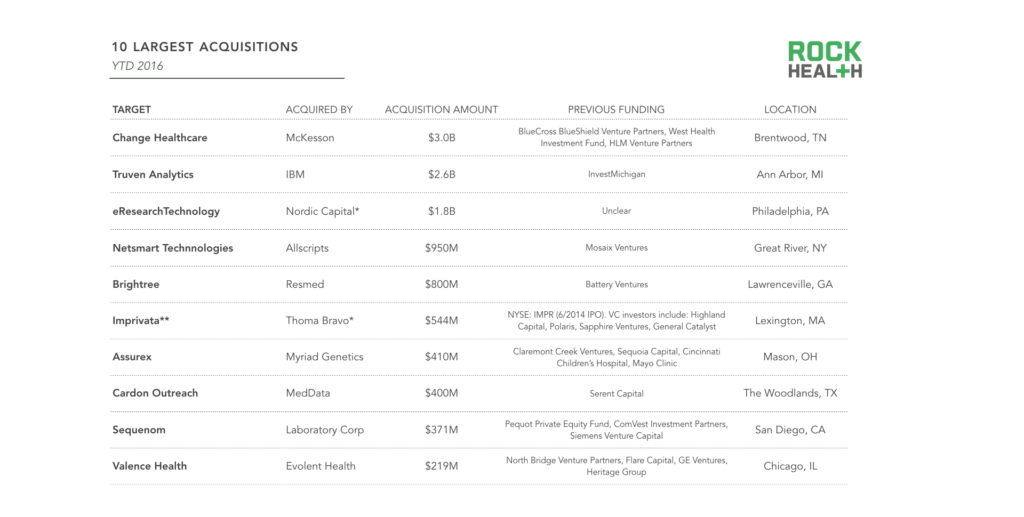

8. The 10 largest acquisitions have brought in just over $11B for shareholders. Multiple name-brand VCs saw handsome returns from these acquisitions, along with several non-profit groups, including West Health Investment Fund, Invest Michigan, Cincinnati Children’s Hospital, and Mayo Clinic. Interestingly enough, none of these acquisitions happened in the Bay Area, New York City, or Boston—the traditional digital health ‘hubs’ for funding.

*Private equity funds

**Imprivata was a publicly traded company at time of acquisition (7/2016)

9. More than a third of digital health acquirers are publicly traded, and a large majority (90%) are US-based companies. But interest from international acquirers does seem to be growing—this year we’ve counted 10 acquisitions from non-US companies, including Japanese-based Asics scooping up RunKeeper and Royal Philips from Amsterdam acquiring Wellcentive.

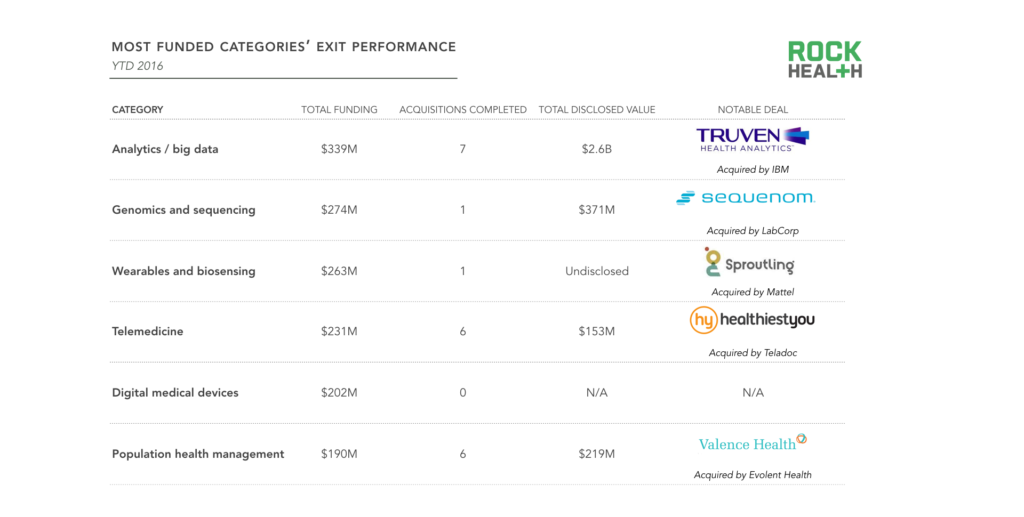

10. There’s a misalignment on where venture dollars are going and where they’re getting returned: None of the top six categories for funding also rank as the top exit category by dollar or number of deals in 2016. Healthcare consumer engagement has returned the most money to investors YTD with a disclosed $3.03B in exits. EHR and clinical workflow companies continue to be the most popular targets—another 18 deals in 2016 (16% of all deals), bringing the total to 58 in the past three years.

This year marks our sixth year tracking the digital health industry and the sentiment is mixed. Private venture investors continue to put their money and confidence behind fledgling startups, but there seems to be a clog in the public markets. We can’t blame digital health: the tech industry has seen only six venture-backed tech companies go public in 2016 compared to an average of 37 annually between 2001 and 2015. We know that there are valuable businesses being built in the digital health industry—we work with them everyday. But until the public markets catch up, shareholders will have to rely on acquisitions for any liquidity.

We’re excited to see how the industry closes out the year. Follow along with us and subscribe to the Rock Weekly.