In 2019, digital health celebrated six IPOs as venture investment edged off record highs

Let us help with your upcoming presentations! Feel free to download and use our market insight slides on the venture funding and exit landscape in digital health by clicking above. And stay up to date with the latest headlines in healthcare technology and new Rock Health research. Subscribe to the Rock Weekly.

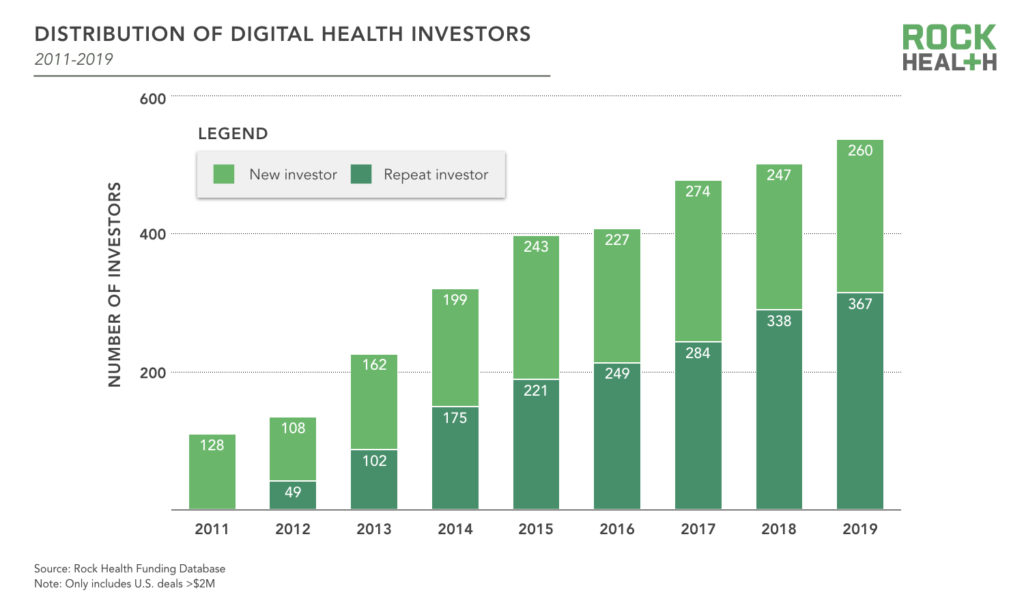

Though investment in digital health declined, veteran investors demonstrated steady commitment to the sector

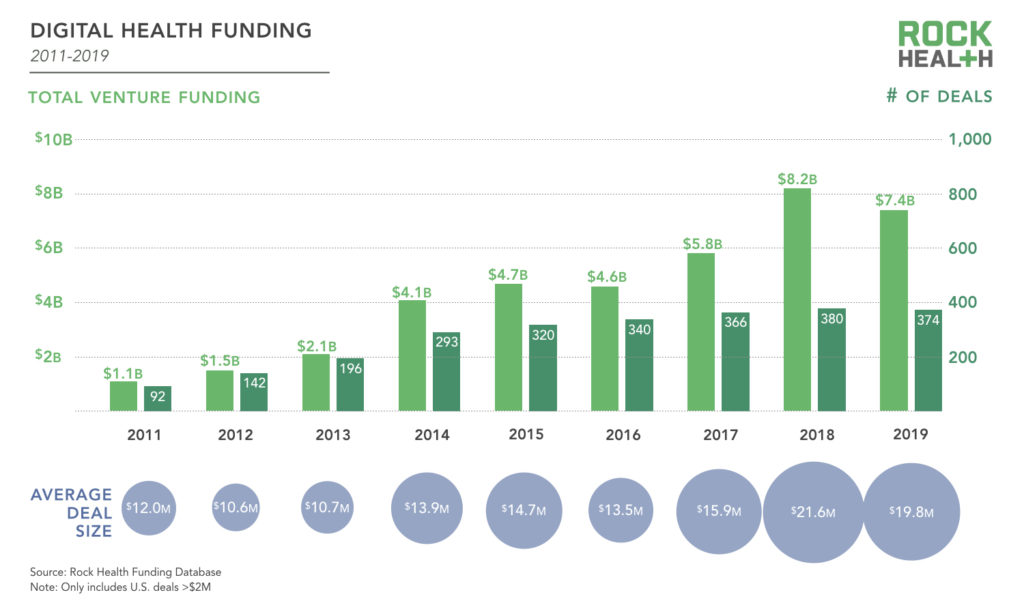

In 2019, US digital health startups raised a total of $7.4B—the second largest funding year ever. Deal count declined slightly for the first time since Rock Health began tracking this space in 2011. After jumping 32% across 2017-2018, average deal size dipped to $19.8M in 2019. Overall, digital health entrepreneurs continue to have access to near-historic levels of funding.

As we anticipated at the close of 2018, a record-breaking year, the growth trajectory of venture investment in digital health slowed in 2019. Total venture funding was 10% below 2018’s record-setting high of $8.2B. This drop was arguably driven by a small change in the number of late-stage deals year over year (YoY)—just two late-stage deals in 2018 accounted for the $0.8B YoY change in total funding. In an interesting twist, two of the companies in the IPO class of 2019—Peloton and Livongo—together raised $655M back in 2018; this accounts for 80% of the difference in funding between 2018 and 2019. Moderation, rather than contraction, best describes the trend going into 2020.

Nearly 60% of active digital health investors in 2019 had previously made an investment in the sector. Repeat investors have been in the majority in digital health for four years (compared to first-time investors), but 60% repeat investors is a new high. Independent, non-corporate venture capital funds and private equity (PE) are the most grizzled veterans of the bunch:

Venture capital (VC)

Has invested across all stages (Seed to D+ and growth rounds).

- 62% of VCs were repeat investors in 2019

- More than 50% of VCs have been repeat investors since 2014

Corporate venture capital (CVC)

Has invested mainly in mid-stages (B+) and later.

- 64% of CVCs were repeat investors in 2019

- More than 50% of CVCs have been repeat investors since 2018

Private equity (PE), growth, hedge funds and asset managers

Have invested mainly in later stages (D+ and growth rounds).

- 56% of later stage investors were repeat investors in 2019

- About 50% have been repeat investors since 2015

I am feeling more optimistic today than I have in all the years I’ve been investing. There is so much innovation advancing at a rapid clip, and smart minds are coming into digital health. There’s finally proof in the pudding—companies are proving outcomes and cost validation, so there’s real value being created. And exit pathways are no longer a pipe dream.

Alyssa Jaffee, Vice President, 7wire Ventures

Six digital health companies went public in 2019, representing new liquidity and return of capital to investors

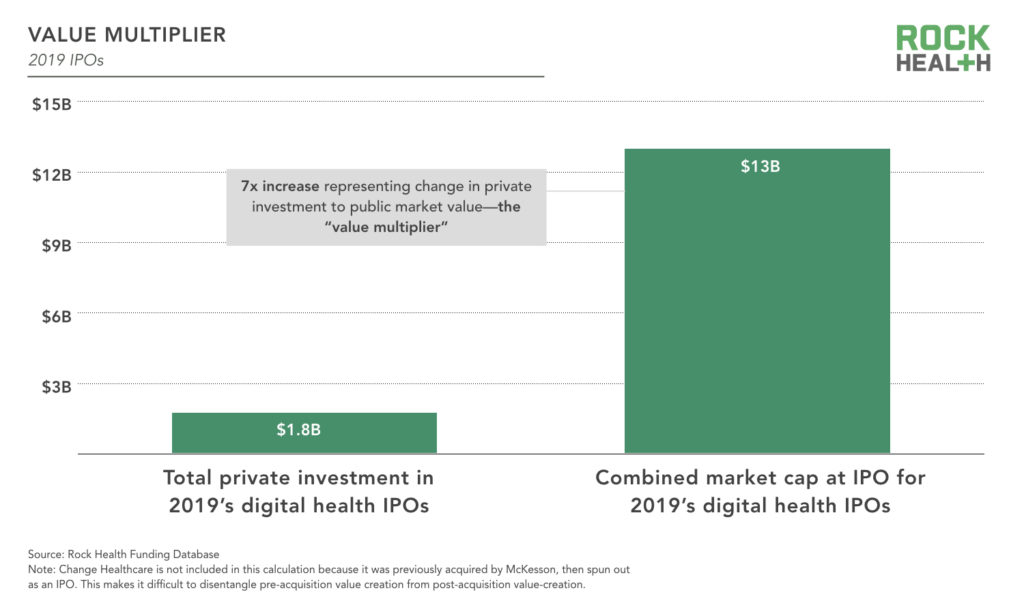

After a three-year IPO drought, six digital health companies entered the public market in 2019: Livongo, Health Catalyst, Phreesia, Change Healthcare, Peloton, and Progyny. As of January 1, 2020, the combined market cap of the six IPOs is $17B. The flurry of IPOs in 2019 is validating for the venture model of long-tail investing—a small number of companies generating a large share of the returns—in digital health.

Excluding Change Healthcare for a moment (since it was previously acquired by McKesson1), the founders and employees at the five other companies used $1.4B of investors’ capital, and their own sweat and tears, to turn five great ideas into companies worth $13B at IPO. This 7X increase is a helpful, if somewhat artificial, way of thinking about the total “value multiplier” these companies achieved with the capital provided by their investors.

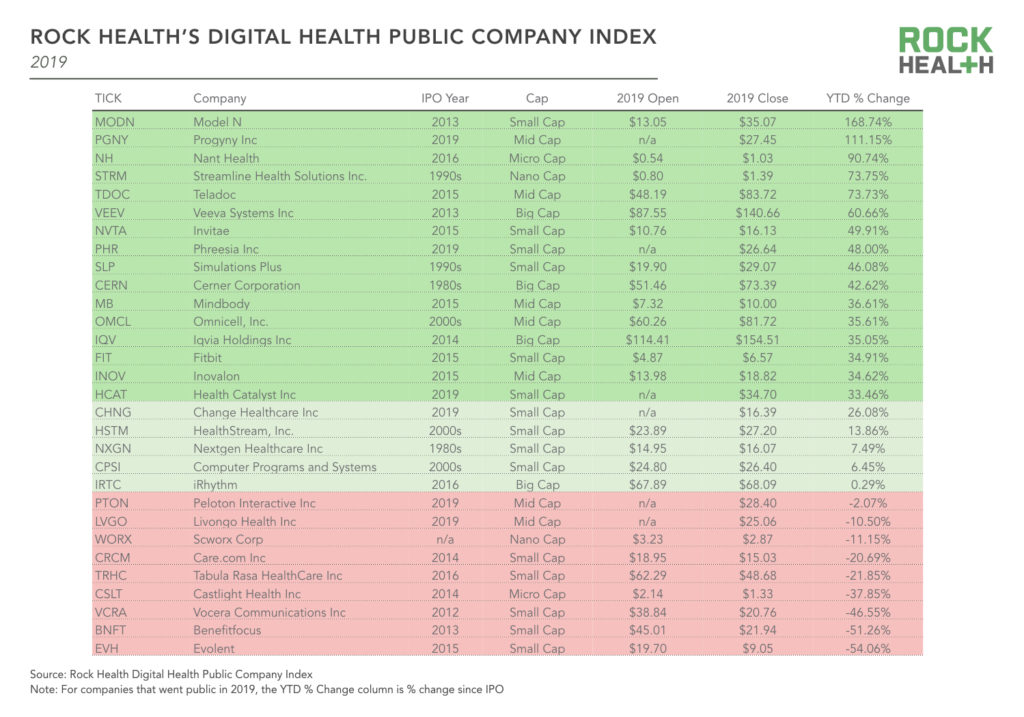

The Digital Health Public Company Index gained 31%2 in 2019—in line with the S&P 500’s performance. The list shrunk by two in 2019: athenahealth was taken private by Veritas Capital, a private equity firm, and Medidata Solutions was acquired by Dassault Systèmes, a European software company. Fitbit will fall off the list this year if the Google acquisition closes as anticipated.

M&A continues to provide most of the liquidity to digital health investors in terms of deal count. One hundred and twelve US digital health companies were acquired in 2019, 40% fewer than the 188 acquisitions at the M&A peak in 2015. Large healthcare incumbents and new entrants alike are buying their way into digital health:

- Amazon acquired Health Navigator, adding online symptom checking and triage tools to Amazon Care

- Google acquired Fitbit in a deal that gives the tech giant access to troves of personal health data and healthcare partnerships, in addition to health tracking hardware

- UnitedHealthcare’s Optum acquired Vivify Health, adding patient monitoring capabilities to the payer-provider behemoth

- Best Buy complemented its 2018 acquisition of Great Call with Critical Signal Technologies, a remote patient monitoring service

The macro picture beyond digital health is changing—a more cautious market may ripple across investment sectors

Over the final months of 2019, a dozen-plus conversations with fellow investors indicate that the peak of the current investment cycle is moving into the rearview mirror. Though anticipating broader market turbulence and a “less open” IPO window, investors expect to continue deploying capital—though potentially at a slower pace than in recent years—to technology companies that address the massive challenges and opportunities in US healthcare.

I worry that investor sentiment may have changed profoundly in the last month or two. I don’t think that’s been widely reported, and there is a real risk that entrepreneurs have not recalibrated for more hostile capital markets. These things come and go, but with an election coming, impeachment, trade wars—this could settle in for another year or two. So if you’re a company that’s missing its milestones, it could be a pretty frosty winter.

Michael Greeley, General Partner, Flare Capital Partners

IPOs may slow in 2020, following a spate of 2019 exits that didn’t live up to expectation

It was a hot market for IPOs in the first half of 2019. In Q2 alone, 62 companies across sectors went public, raising a total of $25B from public investors—the most active quarter by deal count in four years.

Lackluster performance in the first few months of trading by several high-profile IPOs, including Uber, Lyft, and Slack—as well as the WeWork drama—may be dampening public investors’ appetite for venture-backed companies. Investors are concerned that valuations of some later-stage startups are inflated in private markets, leaving little room for growth once those companies reach the public markets. Adding to this concern, the cohort of 2019 IPOs is among the least profitable since the tech bubble. These developments amount to headwinds against late stage digital health companies considering an IPO in 2020.

The 10-year bull market continues, though risks are on the horizon—the shockwaves of an economic slowdown would ripple into the private markets

Interviewed venture investors are bracing for a downturn as the 10-year bull market could be nearing a peak. While we won’t try our hand at economic predictions, the list of uncertainties—foreign policy escalation, trade wars, global economic slowdown, and an election—is weighing on the minds of venture capitalists.

Over the past decade, a strong economy and low interest rates have been a boon to venture firms raising new funds, contributing to the record levels of dry powder sitting in the coffers of VC and PE firms. While these funds may provide a buffer against a future contraction in funding (i.e., investors will still have capital to deploy to startups, even if the macroeconomic environment darkens), entrepreneurs should be prepared for tighter venture capital markets in the year to come.

The funding environment has definitely changed over the course of the year. Things at the beginning of the year were just bananas—it felt like risk was just not being priced in. By mid-year, it started to rationalize a little. Partly because of the tech unicorns that went public and struggled. Sentiment has become more toned down, but I don’t think it’s a correction. It just hasn’t continued to rise.

Amy Belt Raimundo, Managing Director, Kaiser Permanente Ventures

Looking beyond the money, tailwinds for digital health continue as policymakers extend the foundation for a connected healthcare system

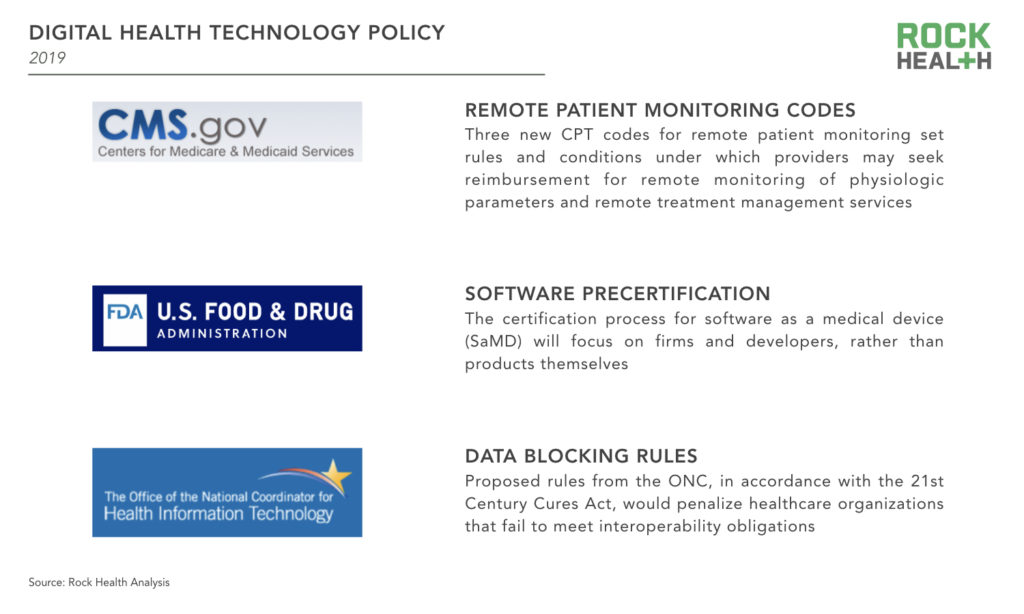

Federal policy can sustain the direction of innovation by setting rules and standards and reducing regulatory uncertainty. In 2019, CMS, ONC, and FDA continued to establish the rules of the game for the connected healthcare system:

- CMS set reimbursement codes for remote patient monitoring (RPM)

- FDA completed retrospective testing of the Precertification program

- ONC finished collecting public comments regarding its proposed data blocking rules

Collectively, these policies are building blocks of the federal government’s digital health technology policy, adding to the foundation laid out by the HITECH Act one decade ago. The long-term commitment to the digitization of healthcare lends the sector some resilience to short-term market fluctuations.

A special thank you to our generous corporate partners for their continued support. For access to this year’s full Digital Health Market Update and investment databases, get in touch about becoming a Rock Health partner.

Thank you to our contributors

This report would not have been possible without the help of a number of individuals who have graciously shared their expertise:

- Alyssa Jaffee, Vice President, 7wire Ventures

- Amy Belt Raimundo, Managing Director, Kaiser Permanente Ventures

- Michael Greeley, General Partner, Flare Capital Partners

Stay up to date with the latest headlines in healthcare technology and new Rock Health research. Subscribe to the Rock Weekly.

Footnotes

1Change Healthcare is not included in this calculation because it was previously acquired by McKesson, then spun out as an IPO. This makes it difficult to disentangle pre-acquisition value creation from post-acquisition value-creation.

2This is a measure of the return an investor would have received if they bought a number of shares proportional to the market cap of each company in the index and held it from January 1, 2019 to December 31, 2019. Only companies that were publicly traded for the entire year are included in this calculation.