Q1 update: Unlike tech, 2016 digital health funding on record pace again

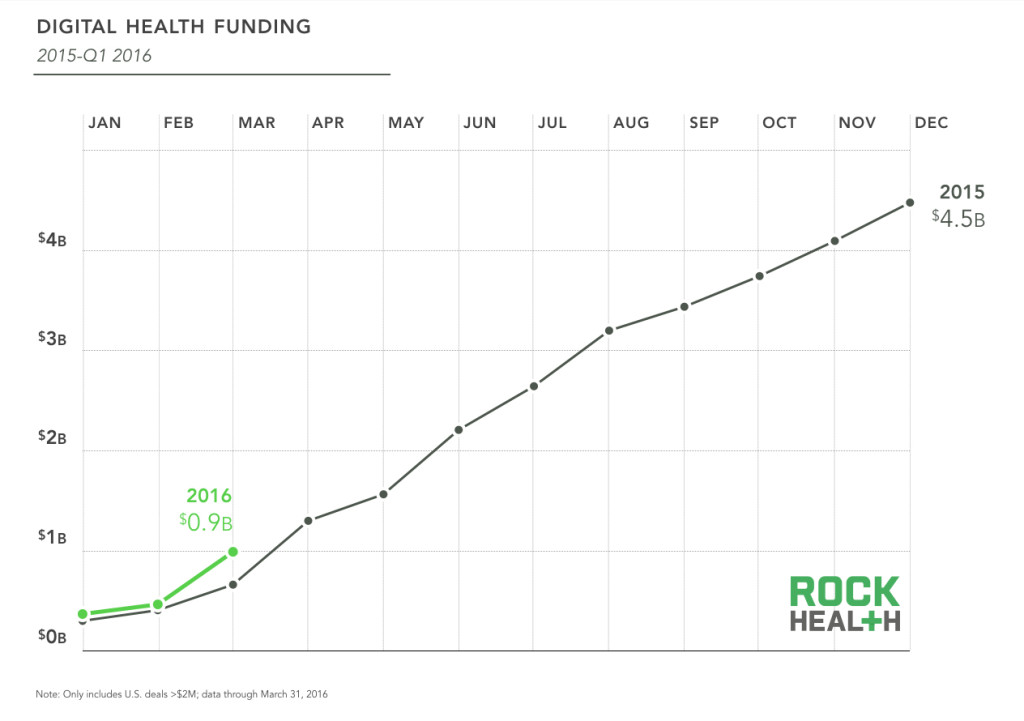

If you spent the first quarter of this year listening to investors, founders, or the tech media, you heard the same thing we all did: the market is experiencing a correction (or downturn, depending on your perspective), valuations are crashing, and VCs are generally acting with more caution. While some of that may be true for the tech industry at large, digital health may be immune. Our data shows digital health funding experienced an uptick with 13% TTM growth and almost 50% YoY growth (when compared to 2015’s first quarter—a record year itself). Total funding for Q1 2016 reached $981.3M, the highest first quarter total since we started tracking deals in 2011.

Source: Rock Health Funding Database

The two largest deals of the quarter represented over 34% of the quarter’s transaction value and contributed to the largest average deal size ($18.2M) since Q2 2015. While dollars and average deal size grew, the number of deals is down 11% compared to last year. During this first quarter, seed stage and Series A deals represented 54% of all deal volume, comparable to what we saw in 2015 (50% of volume), and there was a slight increase in the percentage of Series D+ deals (10% to 13% of total deal volume). Note: Our venture funding data only includes disclosed US deals over $2M. Companies that are sector-agnostic with a healthcare vertical are excluded.

The five largest deals of the quarter

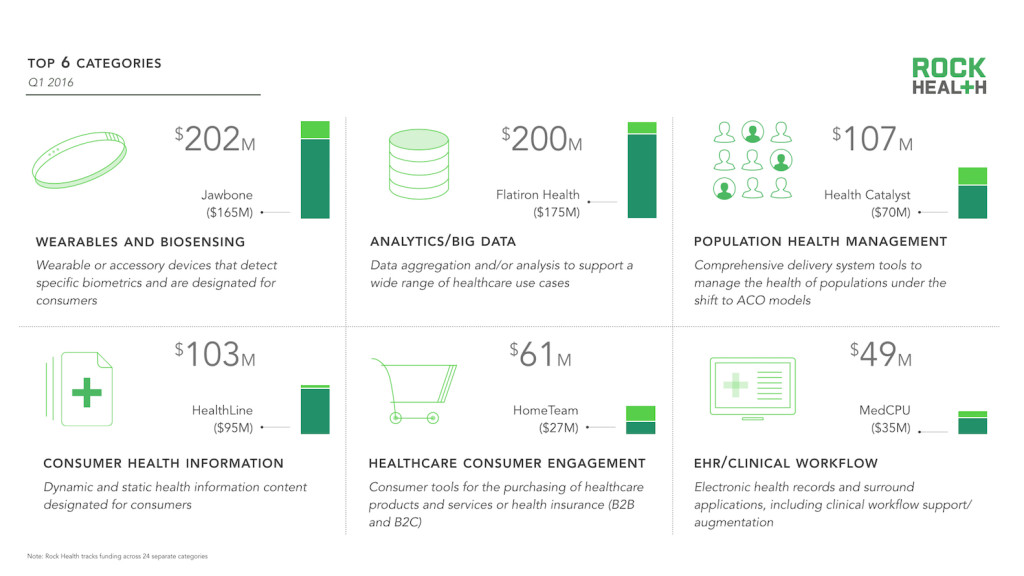

- Flatiron Health ($175M) is a business and clinical intelligence platform for cancer care providers

- Jawbone ($165M) develops and sells wearable technology that provides personalized insights into how users sleep, move and eat

- HealthLine ($95M) uses a taxonomy-driven search platform to provide intelligent health information to individuals

- Health Catalyst ($70M) is a healthcare data warehousing provider

- Higi ($40M) provides kiosks that screen for a user’s blood pressure, weight, pulse, and body mass index

The top 6 categories of Q1

Although investors continued to favor a few popular categories, we saw new digital health darlings emerge this quarter. The top six categories accounted for over 77% of the deal value for Q1 2016; only wearables and healthcare consumer engagement maintained a place on the list from the end of 2015.

Source: Rock Health Funding Database

Similar to 2015, we saw a continued investment focus on companies offering consumers three types of services: accessing health information, tracking data points, and providing context for what that data means and how it can impact care. With increased access to consumer data through ubiquitous smartphones and new and cheaper sensors, collecting data points has been the easiest part of this spectrum. We continue to be excited about interesting methods of pairing this data with actionable insights and allowing providers and payers to create more personalized care plans.

M&A Activity

Given the relative youth of the digital health industry, the state of the market as it relates to venture-backed IPOs (0 tech IPOs during Q1), and public digital health performance in these markets (down 9.6% YoY), M&A appeared to be the most common route for exits. We tracked at least 187 M&A deals in 2015. First quarter highlights include:

Asics acquired Runkeeper: Japanese sportswear brand Asics started off the year by keeping pace (get it?) with an acquisition of Runkeeper for an undisclosed sum. This continues a 2015 trend, when we saw Adidas (Runtastic) and Under Armour (MyFitnessPal) both make splashy acquisitions of fitness platforms. Looking ahead, it seems clear that fitness brands are interested in bridging the digital gap and being more involved in the consumer sports experience. Fun fact: Asics are the most popular shoe on the Runkeeper platform.

One Medical Group acquired Rise: Mobile app meet provider. While not a typical provider, One Medical picked up Rise to add to its mobile health offering and increase the value it can provide to its patients through telemedicine and access to nutritionists. For Rise, this is a chance to get in front of more users in an era when consumer distribution is becoming more and more difficult and less than 8% of users are willing to pay for healthcare expenses out-of-pocket. Perhaps a win-win.

Our takeaways

- It’s only the first quarter after a(nother) record year of funding. With all the talk of a correction or impending bubble pop, it’s still early to declaratively say what happens for digital health funding for the rest of 2016. But we’re optimistic.

- We think that M&A deals will continue to be the most popular liquidity event in digital health. The IPO market remains uncertain; overall digital health performance is down, and digital health stocks are trading well below their first day prices (see: industry standout Fitbit, which is trading almost 50% below its first day price). On the other hand, M&A deals continue to grow, nearly doubling from 2014 to 2015 in transaction volume (95 deals to 187 deals). Which venture-backed startup will get scooped up next?

Interested in seeing the data for yourself? Check out our database here.