Building comprehensive women+ digital health: Eight sectors serving women+ needs

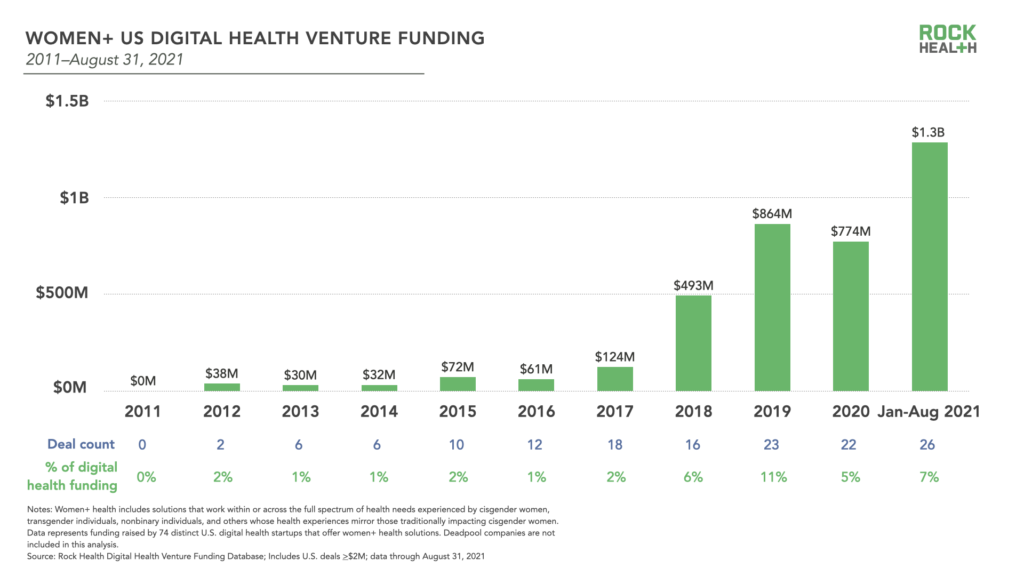

Turbocharged 2021 digital health venture funding and greater awareness around health equity gaps are boosting support for companies addressing underserved care needs, including specialized care for women and individuals with female biologies.1 We use the term “women+ health” to describe the space to encompass the full spectrum of health needs experienced by cisgender women, as well as others whose health needs relate to those of cisgender women but may identify as transgender or nonbinary. Just this year, US digital health startups serving women+ raised $1.3B through August 31, 2021, nearly doubling all of 2020’s $774M funding across a similar number of deals. Women+ funding accounts for 7% of this year’s US digital health funding through August 2021, though still below the high mark of 11% in 2019. Building on our 2020 thought piece on the space, we take a renewed look at women+ digital health, examining companies that exclusively address women+ care needs (such as Dorsata and Maven) as well as companies that support women+ health in addition to other communities (Ro, LetsGetChecked, Hims&Hers). Our analysis shows a continued focus on pregnancy and fertility support, but also a concerted effort to build and fund digital health companies that integrate primary, sexual care, and fertility support for women+.

While 2021 showcases the most funding ever recorded for the space, US women+ digital health dollars make up just 5% of all digital health funding secured since Rock Health started tracking in 2011. We expect the share of funding to women+ companies to increase, as women+ health is growing at a nearly identical pace to the digital health industry as a whole. Comparing the January to August periods of 2020 and 2021, women+ funding increased by 2.2x, while overall digital health funding increased by 2.3x. We’re grateful to the thoughtful ways leaders are driving that momentum, creating greater awareness of the persisting care gaps for women+, from investor Christina Farr’s market segmentation to The Commonwealth Fund’s insight report.

Read on to learn: (1) the current utilization of digital health solutions by women+, (2) the funding trajectory for companies serving women+ needs, (3) an updated analysis of the US women+ digital health marketplace, segmented into eight sectors, and (4) where we see opportunity for greater growth, expansion, and impact to make comprehensive health for women+ individuals a reality.

Women+ Health and the Role of Digital Health

In many respects, women historically have utilized more healthcare than men—they use preventive care services at a higher rate, and working-age women incur healthcare expenses at least 80% higher than their male peers. Not only has this not translated into better outcomes, but this behavior has shifted, with women more likely to forego care during COVID. And, despite our strongly held belief that digital health offers immense opportunity to improve women+ health, women are not utilizing digital health at the same rates as men.

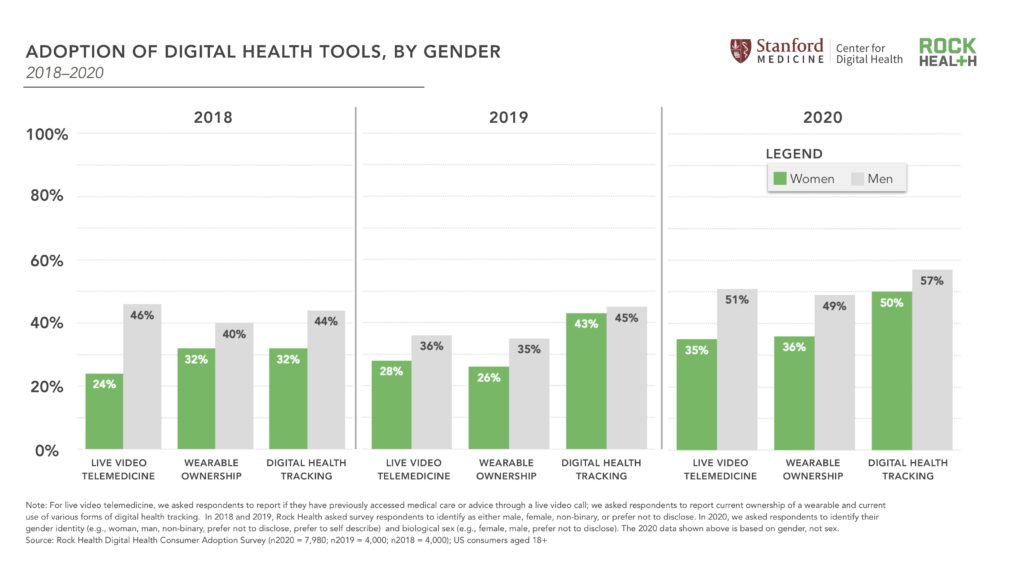

Rock Health’s Consumer Adoption Survey2 data from 2018 through 2020 show that women3 used particular digital health tools at lower rates than men—specifically live video telemedicine, wearables, and digital tracking of health metrics. And while women respondents have increased their adoption of digital health tools over time, men respondents reported greater year-over-year increases. The gender gap in digital health usage in 2020 remains pronounced: 35% of women respondents reported previous use of a live video telemedicine call compared to 51% of men respondents, and 36% of women respondents owned a wearable versus 49% of men respondents.

What’s more, in 2020, fewer women respondents (66%) accessed at least one form of telemedicine (video, phone, text, etc.) compared to 2019, representing a reduction in use of 11 percentage points. Men respondents also reduced their telemedicine use from 2019 to 2020 by three percentage points (and we dig into the “why” of that overall reduction here)—but the larger reduction in women utilization is pronounced.

Rock Health’s 2020 Consumer Adoption Survey also suggests that there may also be gender differences in the utility derived from digital health tools. For example, 66% of women respondents who owned a wearable reported that it helped them achieve their goals compared to 76% of men respondents. This helps underscore a message we’ll keep promoting—it’s imperative to build digital health solutions specifically with women+ values, wellness and care priorities, and daily behaviors in mind.

Several studies suggest that lower digital health utilization among women+ may correlate to systemic health inequities, many of which were exacerbated during the pandemic. For instance, a 2020 report in JAMA suggests that, because women are bearing a disproportionate burden of childcare during the pandemic, they have limited time to seek out or engage with virtual care for their own needs. Rock Health’s 2020 Consumer Adoption Survey data and the 2020 Kaiser Family Foundation Women Health Survey both found that women were more likely to forgo healthcare at the height of the pandemic in 2020 compared to men. More specifically, the Kaiser survey found that women with health and economic challenges prior to the pandemic experienced worsening health conditions in 2020, due to forgoing necessary care.

These signals do not deter our belief in the opportunity digital health offers to women+; if anything, they create even greater urgency to ensure that digital health tools are built to meet women+ needs. At the most basic level, digital health can reduce the time and energy it takes for women+ to attend in-person appointments—a critical benefit when 53% of US women report feeling burnt out by their everyday tasks. And women+ who experience social stigma or even legal barriers to certain types of procedures can turn to virtual channels to meet their needs. We believe digital health can unlock greater access and satisfaction in addition to improved outcomes, and that many women+ stand to benefit from the specialized care and broad provider networks that digital health companies enable.

Funding Trends for US Women+ Digital Health Companies

There’s still work to be done to help women+ access the full promise of digital health, and we’re seeing investors lean into this moment. From January through August 2021, US-based digital health startups developing products and services for women+ raised $1.3B, and average deal size for these companies jumped from $35.2M in 2020 to $49.4M.

Since 2011, seventy-four US-based women+ digital health companies4 have raised $3.8B across 141 deals. On average, these companies are six years old and have raised $51M. Median funds raised is $9M, with high outlier rounds pulling the average significantly up.

Funding gains aren’t new to women+ health—we saw similar jumps in sector activity back in 2018 and 2019—but 2021’s trends suggest maturity in the space. For comparison: in 2017, the average age of women+ companies was four years old, and no women+ health companies had reached Series C or later. Now in 2021, the average age of women+ companies is six years old, and from January through August 2021, 31% of women+ digital health deals were Series C or above.

Well-publicized 2021 late-stage investments in the women+ health space include Carrot Fertility ($75M), Tia ($100M)5, and Maven’s $110M mega deal that earned it the title of the first digital health unicorn exclusively focused on women+. Notably, 69% of the women+ health companies that raised capital from January through August 2021 are led by women6 CEOs, compared to 20% of all digital health companies funded in the same period. Larger companies are growing their focus in the women+ digital health category too. Ro acquired Modern Fertility in May, reinforcing the strategy of digital health companies making segment-specific acquisitions to target key populations—an approach adopted by LabCorp when it acquired maternity and family benefits company Ovia Health in August.

2021 is also seeing the formation of women+ digital health’s first public company cohort, with Hims&Hers and Sema4 exiting this year via SPAC mergers and Ro announcing a potential SPAC deal in February. These companies join women+ fertility benefits manager Progyny on the public markets, which exited via IPO in 2019. While Progyny is the only of the group exclusively focused on women+ care, these companies are setting a broad precedent for how public market investors could evaluate this category’s performance and potential moving forward.

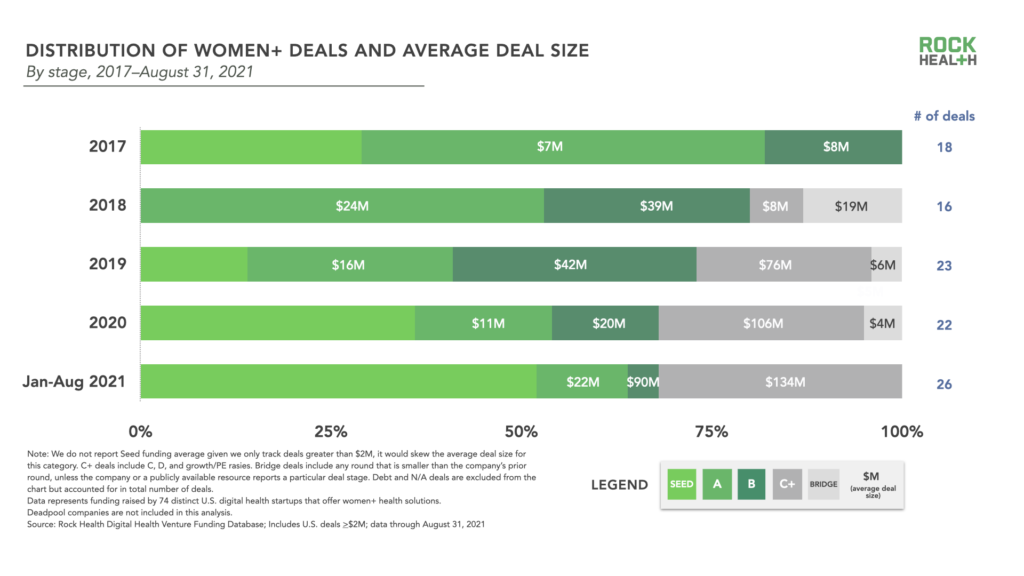

Even with 2021’s late-stage funding and public exits, the women+ digital health category shows promise of continued growth. From January-August 2021, seed-stage activity made up 50% of women+ digital health deals, and we’re looking forward to seeing entrepreneurs and investors bring these early products to scale. As we explore later in this piece, we’re also excited to see new innovation areas in the category emerge.

Eight Sectors Within the Women+ Digital Health Landscape

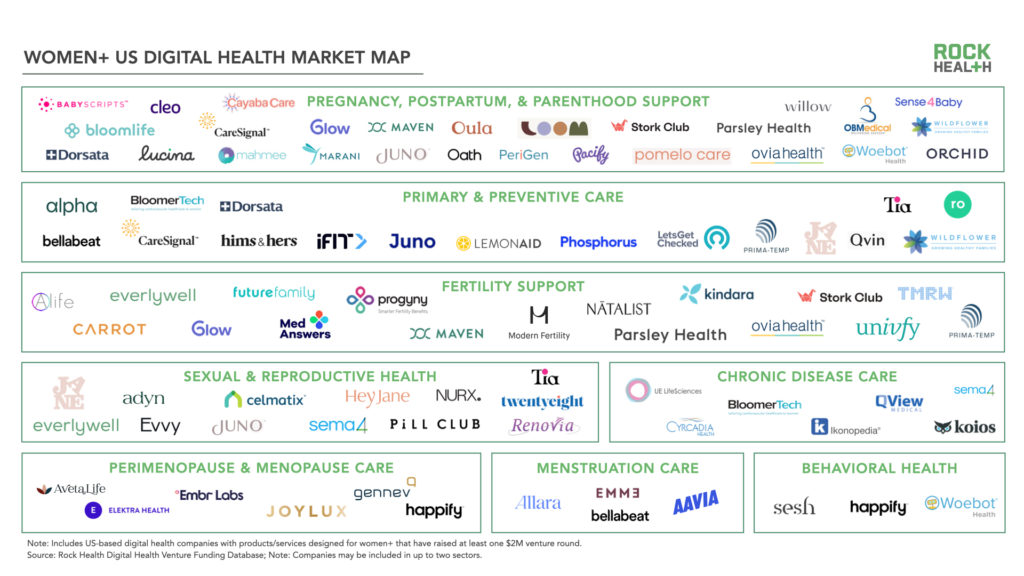

We’ve organized venture-backed women+ digital health companies into one of eight sectors, listed below in order of the number of companies operating in the space. While companies often address multiple segments we tagged each company with up to two of the eight sectors for this analysis.7

- Pregnancy, postpartum, and parenthood support (27 companies): Solutions that focus on assisting women+ parents through pregnancy, miscarriage, birth, breastfeeding, and postpartum support

- Primary and preventive care (16 companies): Solutions that target the spectrum of women+ primary care needs, such as annual wellness exams, general lab test screenings, and comprehensive screenings

- Fertility support (16 companies): Solutions that address health needs associated with conception, including ovulation tracking, intrauterine insemination (IUI), in vitro fertilization (IVF), intracytoplasmic sperm injection (ICSI), preimplantation genetic diagnosis (PGD), egg donation, and egg preservation

- Sexual and reproductive care (13 companies): Solutions that encompass women+ healthcare services related to routine gynecologic care, sexual education, abortion care, and sexually transmitted infections (STIs), and pelvic health

- Chronic disease care (7 companies): Solutions that target chronic conditions requiring ongoing care which are not exclusive to, but prevalent among, women+ individuals, such as breast cancer, ovarian cancer, and heart disease

- Perimenopause and menopause care (6 companies): Solutions that target treatment for perimenopause and menopause, including menopausal hormonal health, temperature regulation, and pelvic floor health

- Menstruation care (4 companies): Solutions that target treatment for menstrual health and hormone-related conditions, including period tracking, polycystic ovary syndrome (PCOS), and irregular periods

- Behavioral health (3 companies): Solutions that offer tailored support for women+ across mental health, substance use disorders (SUDs), and/or developmental disorders

In examining these segments, a few key insights emerged.

Most activity still lies in pregnancy, postpartum, and parenthood

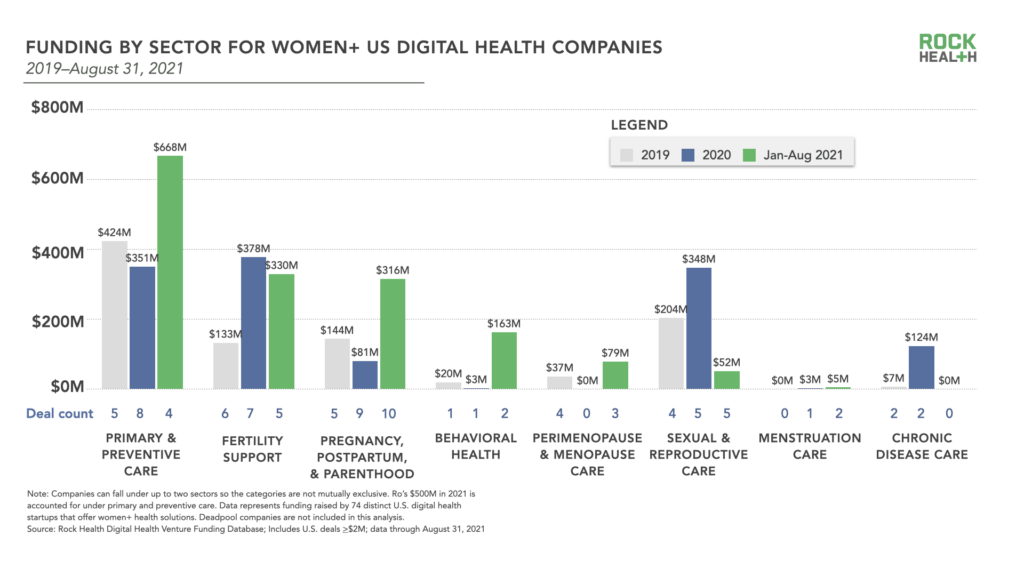

The pregnancy, postpartum, and parenthood sector still attracts the most attention in women+ health, accounting for 37% of women+ health companies founded in the past five years. High levels of funding and exit activity in this category aren’t surprising as women+ health has historically been tied to pregnancy care. In fact, half of women+ digital health companies that have exited via acquisition or public markets are in this sector (i.e., Lucina Health, OBMedical, Ovia Health, Perigen, Sense4Baby).

Industry focus on bringing pregnancy, postpartum, and parenthood solutions to market is having an impact—our 2020 Consumer Adoption Survey data show that 73% of pregnant respondents reported prior use of live video telemedicine compared to 35% of all women respondents. However, with less than 45% of the US female population at reproductive age, and the US birth rate at its lowest record to date, equivocacy between pregnancy, postpartum, and parenthood support and women+ health can leave the majority of women+ deprioritized in the current scope of digital health innovation.

Integrating primary care, sexual wellness, and fertility

In 2021, the top three funded women+ health sectors are primary and preventive care ($668M), fertility support ($330M), and pregnancy, postpartum, and parenthood ($316M), largely driven by four mega deals from Ro, LetsGetChecked, TMRW, and Maven. Several companies offer solutions at the intersection of these three sectors, building comprehensive experiences for women+ whose needs span general health, sexual wellness, and family planning. Key examples include LetsGetChecked’s diagnostic offerings for women+ sexual wellness, fertility, and vitamin deficiency, as well as Rory’s (a Ro brand) portfolio of skincare, sexual wellness, and daily health support.

Destigmatizing menopause health

We’re excited to see that funding into the perimenopause and menopause sector doubled from 2019 to 2021. Publicity and funding for digital health solutions addressing menopause is a promising sign for care that has historically been stigmatized in professional and social settings. Key players in digital menopause care include virtual coaching services Elektra Health, Gennev, and Evernow8, as well as digital pharmacy support from Rory. And in July 2021, mental health platform Happify launched the app Kopa to support women+ navigating midlife health needs.

“Despite the inevitability and breadth of menopause, women encounter a shocking lack of resources and personalized treatment options to manage their often-debilitating menopausal symptoms. Fortunately, the tides are turning as cultural shifts, tech innovation, and increased venture funding paves the way for a new suite of products and services addressing the distinct needs of this digitally-savvy generation of menopausal women.” – Stephanie Siepman, Venture Principal, Rock Health Capital

Low support for behavioral health, chronic conditions

Despite an overall surge in behavioral health funding, only 4% of that 2021 funding went to companies that offer tailored solutions for women+ needs related to anxiety and depression, postpartum mental health, substance use disorders, and other behavioral health conditions.10 We also see room for improved digital health tools to help women address chronic disease care, an area that hasn’t received funding so far in 2021.

White Space for Women+ Digital Health Innovation

Forecasts indicate miles of innovation runway ahead for women+ digital health—Emergen Research projects that the global market for women’s health will reach $60 billion in 2027, compared to its $18.75 billion valuation in 2019. In addition to reviewing venture-backed startup activity across the US market, our perspective on the future of women+ health is also shaped by the budding startups we see as active early-stage investors. With continued growth and attention in the marketplace, we’re watching five big areas of opportunities for women+ digital health innovation.

- Digital therapeutics for women+ health

Women+ health is a growing field within digital therapeutics (DTx), delivering evidence-based software programs to prevent, manage, and/or treat medical conditions. Early digital therapeutics in women+ health included software-based contraception tool Natural Cycles (FDA approved in 2018) and digital pelvic floor health exercise tool Renovia (FDA approved in 2019, with $17M raised in April 2021).Growth areas for women+ digital therapeutics include medication adherence, virtual coaching, biophysical stimulation, and side effect management related to fertility treatments, pregnancy, PCOS, hormone health, menopause, mental health, and gynecological cancers.

-

Expanding the scope of women+-minded conditions

The digital health marketplace has started to address once-stigmatized conditions including menopause, sexually-transmitted infections, and pelvic floor disorders. But there are still meaningful gaps in care around health needs related to miscarriage, abortion, and women+ surgeries such as hysterectomies and mastectomies. Startups such as Brilliantly, a company creating wearables and exercise plans for women+ who undergo mastectomies, Hey Jane, a virtual clinic for abortion care, and Pregnancy After Loss, an app that helps navigate conception after a miscarriage, are paving the way. - Applying a women+ lens to primary and chronic care

In 2020, we highlighted the importance of addressing women+ needs in broad care spaces such as Alzheimer’s and heart disease. We’re glad to see big players adopt women+-specific care lenses in 2021, including Ro, which acquired Modern Fertility in May; CVS Health, which unveiled specialized digital resources for women+ mental health in May; and iFit, a digital fitness network that acquired women+ exercise platform Sweat in July.However, there’s still opportunity for primary and chronic care digital health companies to tailor their solutions to women+. For example, experiences such as menstruation have varied impacts on a person’s mental health, energy levels, and nutrient intake, and integrating these insights can make primary health tools more effective. Women+ also have unique presentations for serious conditions such as stroke and diabetes, and gender-based protocols could help to customize digital care responses. Especially in the realms of digital therapeutics and remote patient monitoring, companies will need to keep close tabs on how women+ health factors affect overall health needs and integrate these learnings into digital interventions.

- Acknowledging intersectionality in women+ health experiences

Gender is increasingly acknowledged as a social determinant of health in the US, and healthcare inequities are compounded for women+ who are Black, Latinx, or Indigenous, identify as a sexual minority, live with a disability, or are low income. Digital health companies should address women+ health from an intersectional lens, focusing on how different identities and experiences shape healthcare attitudes and needs. Leading players here include Cayaba Care, a community-based maternity platform for underserved women+, and Sesh Therapy, a mental health platform that holds group sessions for Black women+ and other identities. We’re seeing some fresh activity in the space from companies like Mae11, who provide resources to Black expectant mothers to combat the historically high maternal mortality rate, but a larger movement to invest in intersectional women+ care remains yet unrealized. - Women+ representation in healthcare research

Innovation in women+ care requires that women+ are well represented in health research. Unfortunately, representation gaps still exist. For example, despite making up 51% of all cardiovascular patients, women+ account for 39% of cardiovascular clinical trial participants. The same is true for HIV research—women+ are 44% of all HIV patients but account for 39% of clinical trial participants.Bringing in more women+ to health research is a multi-step process. First, there’s room to evolve how women+ are recruited, matched, and compensated for clinical trials. There are also opportunities to use digital health tools to collect de-identified women+ patient data for real-world evidence research. Lastly, new research channels may need to be built. For example, after realizing the lack of data around vaginal microbiome health, startup Evvy launched this July to collect and test vaginal microbiome samples from women+ at home.

Looking Forward

At Rock Health, we’re hopeful that women+ digital health will increasingly get the talkspace, attention, and funding from investors it deserves to continue to serve the complex, evolving needs of the women+ population. The digital health ecosystem is changing at lightning speed, and while funding for nearly all areas within digital health has increased since the start of the pandemic, digital health founders and investors have yet to realize the full potential in designing equitable and comprehensive care offerings that serve women+.

As the women+ digital health sector matures, we expect more unicorns to follow Maven, and for enterprises to continue engaging with women+ digital health companies to offer segment-specific care. Just as importantly, we look forward to the emerging class of women+ digital health startups receiving early funding today, which are well positioned to address remaining opportunity areas in the market, including digital therapeutics, intersectional care, chronic care, and clinical research.

If you’re interested in learning more about securing enterprise access to the full Rock Health research library and datasets, please reach out.

If you’re building a women+ digital health company and looking for early-stage funding, our venture team would love to chat! Send us your pitch deck to share how you’re working to improve the health of women+ individuals.

Footnotes

- Since August 2020, we have evolved our thinking and methodology on how we address the health needs of individuals who identify as women as well as those with female biologies. Rock Health now uses the term “women+ health”—rather than “femtech” or “women’s health”—to encompass the full spectrum of health needs experienced by cisgender women, as well as transgender individuals, nonbinary individuals, and others whose health needs relate to those of cisgender women.

- In 2019 and 2020, we collaborated with the Stanford Center for Digital Health team in the analysis of trends and writing of the reports. We particularly appreciate the support from Clark Seninger, MBA, Natasha Din, MD, Krishna Pundi, MD, Alex Perino, MD, and Mintu Turakhia, MD.

- In 2019, Rock Health asked survey respondents to identify as either male, female, non-binary, or prefer not to disclose. The 2019 survey did not explicitly ask respondents to identify as a trans identity. In 2020, the survey asked respondents to identify their gender identity (e.g., woman, man, non-binary, prefer not to disclose, prefer to self describe) and biological sex (e.g., female, male, prefer not to disclose).

- The companies are US-based that have raised $2M and above rounds, explicitly but not solely address the women+ population, and fit Rock Health’s definition of digital health.

- Tia’s latest round is not included in reported funding data since it was completed in September.

- The Rock Health Digital Health Venture Funding Database tracks each company’s CEO and assumes gender based on LinkedIn photos and public pronouns. This measure only accounts for one CEO and assigns one of two options: male or female.

- Companies such as Hims&Hers and Ro strategically develop or acquire new capabilities to offer a wide range of services that stem from their primary care offerings, including sexual/reproductive health, behavioral health, and mental health. We have therefore exclusively tagged these companies to the “primary and preventive care” sector.

- Evernow has not yet raised an individual funding round $2M or above, and so was not included in the reported funding amounts and women+ venture-backed digital health market map.

- Companies such as Hims&Hers and Ro strategically develop or acquire new capabilities to offer a wide range of services that supplement their primary care focus, including behavioral health. We have exclusively tagged these companies to the “primary and preventive care” sector, and they are not included in the behavioral health analysis.

- Mae has not yet raised an individual funding round $2M or above, and so was not included in the reported funding amounts and women+ venture-backed digital health market map.