Hindsight is 2021: Looking back and forward at key themes shaping digital health

Happy new year, digital health!

Before everyone gets comfortable saying “2022,” we wanted to do a quick look-back on 2021 to see how our previous predictions fared and share what we expect from digital health this year.

As fun as prediction season is, it’s challenging to make predictions that aren’t fluffy or too provocative for their own good. Our goal isn’t to stir the pot, but to provide a perspective on a few themes in digital health that we’re paying attention to at the turn of the year. In this post, we’ll assess the performance of our previous predictions across 2021 and look forward to the new year with three types of hypotheses. In terms of past predictions, some of these we nailed (bullseye), some were not far off (close), and some we got partially right, but not quite (mixed). And here’s how we’re thinking about 2022’s themes: “Full steam ahead” is something that is already going on that we expect more of. “Gaining traction” is a development we’re starting to see now that will accelerate in the new year. “On the horizon” is a newer prediction that will begin to take shape in 2022.

For the full story on 2021, keep an eye out for Rock Health’s complete year-end recap of digital health funding coming next week. In the meantime, here’s a roundup of what we predicted last year and nine anticipated developments for 2022.

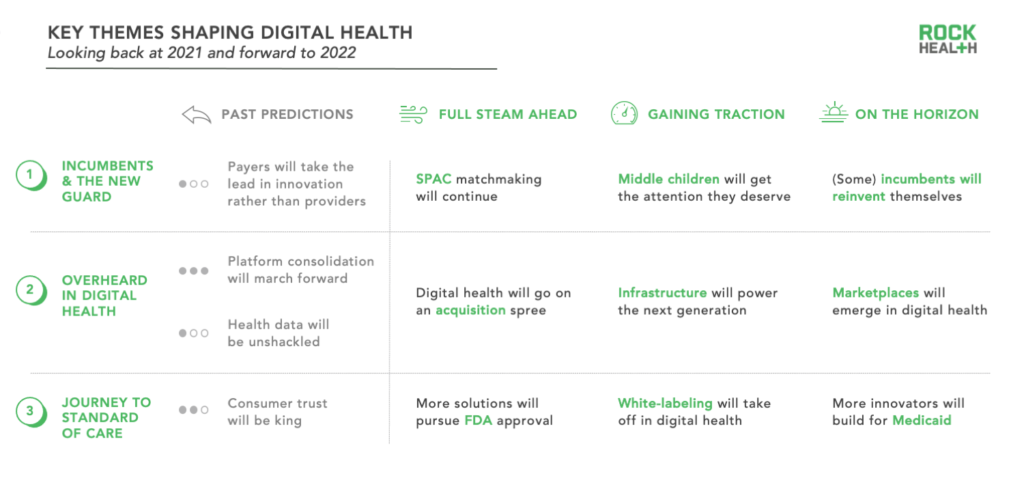

Theme 1: Incumbents and the new guard

We’ve been talking about healthcare’s new world order for a while. Among other shifts causing the next normal, the stakeholder makeup of healthcare is changing. Those involved in healthcare innovation today are not the same group as they used to be. How are incumbents adapting to these conditions and who is disrupting the playing field?

Our prediction from last year:

Payers will take the lead in innovation rather than providers | Score: mixed

Last year, we predicted that payers would take the lead in innovation, rather than providers, given the budget crunch that resulted from COVID-19 fallout. Yes, payers are helping to drive adoption of digital health through activity like a burst of new virtual-first plans and practices, and CMS’ evolving CPT codes. However, we were wrong to underestimate providers—they doubled down on creating new digital initiatives with focuses like digital health equity, AI advancements, and novel datasets; they also spun off new companies like Anumana and Avaneer Health.

What we’re watching this year:

Full steam ahead: SPAC matchmaking will continue

The number of public exits in digital health in 2021 almost tripled 2020’s record, with the majority choosing the SPAC vehicle. Although SPAC activity overall is now slowing down, cuffing season isn’t over yet. There are still plenty of searching SPACs with the intent of merging with digital health companies, and many highly capitalized potential targets. Whether the SPAC vehicle has a long-term future in digital health is up for debate, but 2022 will still see more deals from the already-public SPAC funds.

Gaining traction: Middle children will get the attention they deserve

A major, overlooked entrant into healthcare are the middle children: large retail, fitness, and tech companies that have not been labeled “big,” but are still a force to be reckoned with. Players like CrossFit, Kroger, and AAA are all getting into healthcare, following the footsteps of other middle children like Best Buy and Dollar General. As digital health matures, we will keep seeing new entrants like these come into the space.

On the horizon: (Some) incumbents will reinvent themselves

Digital health FOMO runs deep, and large organizations that have been in the same business for a long time are looking for ways to stay competitive (ahem, the metaverse). Incumbents—if they’re smart—will respond to startup-led innovation in digital health, and reinvent their own business models (we have our eyes on a few to watch).

Theme 2: Overheard in 2021—”platform,” “hybrid,” “interoperability”

Remember when Clubhouse was the new happy hour? How 2021 is that? Last year’s talk of the town included words like “platform,” “hybrid,” and “interoperability” (that one has been on repeat for awhile). What does the jargon have to say about this moment in digital health?

Here’s what we predicted last year:

Platform consolidation will march steadily forward | Score: bullseye

Back in 2020, we predicted Teladoc’s acquisition of Livongo would be the starter pistol for digital health’s platform wars. 2021 saw a steady stream of related activity, with consolidation fueling vertical and horizontal integration. New platforms like Included Health and Headspace Health formed from mergers, and some later stage companies like Ro and Amwell went on acquisition sprees for the purpose of platform-building.

Health data will be unshackled | Score: mixed

We thought 2021 would see a step change in interoperability due to regulatory momentum, the adoption of FHIR standards, and an increasing number of relevant maturing startups. The road to (secure and regulated) data liquidity in healthcare still has a runway ahead, but last year did see some progress. Compliance deadlines for the Cures Act greased the wheels of interoperability via mandated open notes. There was also excitement within data aggregation from entrants like Truveta and Graphite Health, as well as new allegiances like the Ciox/Datavant merger and Invitae’s acquisition of Ciitizen.

Here’s what we expect to hear from the grapevine this year:

Full steam ahead: “M&A”

Three forces are coalescing to make this a major year for digital health M&A. (1) The platform wars continue as players compete by piecing together additional services into integrated systems. (2) A talent shortage is brewing in digital health, with the great resignation leaving executives and operators in need of new ways to acquire talent. (3) Venture-backed startups are now flush with more capital—and growth expectations—than ever before. In 2022, unrequited talent searching, capital overflow, and steep competition will lead to more M&A.

Gaining traction: “Infrastructure”

Digital health is growing up, and the next accelerant will come from the back-end. Moving forward, infrastructure companies will support interoperability and make it easier for first-time founders to launch new technologies in healthcare. Stay tuned—we’ll dive deeper into this in next week’s funding recap.

On the horizon: “Marketplaces”

With a rapidly growing market of both platforms and point solutions, buying decisions in digital health have never been harder. Customers need an easier way to access the best options. We expect to see more marketplaces for digital health solutions, both for consumers (e.g. Live Better With) and enterprise buyers (e.g. Collective Health).

Theme 3: Digital health’s journey to becoming standard of care

Securing digital health’s role within the standard of care requires patient, clinician, and payer trust in technology, cost effectiveness, and evidence generation. While all of the conditions will not be met in full in 2022, we expect progress on all fronts.

Here’s what we predicted last year:

Consumer trust will be king | Score: close

As the pandemic unfolded in 2020, consumers entered the conversation of healthcare in a central way, accelerating a shift in the consumerization of healthcare—we thought the enhanced role consumers were playing would cause earned consumer trust to become a high predictor of success in digital health. 2021 then saw the rise of the D2C business model. Consumers are now taking on more of the cost burden, and consumer-friendly retail companies like Amazon and Walmart upped their healthcare game over the last year. While consumers are gaining increasing exposure to digital health solutions, satisfaction in some services have taken a dip as they have become more mainstream than novel. Earned consumer trust in digital health still has a ways to go.

Some developments we expect to see this year:

Full steam ahead: More solutions will pursue FDA approval

With wider consumer understanding of the role of FDA in healthcare and continued iteration by FDA of its regulation of digital health solutions, we expect more innovators to pursue FDA regulation. Analysis of previous FDA clearances within AI/ML showed that some clinical specialties (like radiology) have seen far more approved technologies than others—there is significant white space within this regulated path to the market and the clinic.

Gaining traction: White-labeling will take off in digital health

Along with the rise of infrastructure companies, white-labeled solutions will allow already trusted brands to deploy new digital health services to their customer bases. Consider that Amazon Care could not have been released in 2021 without white-labeled telemedicine. We expect to see more of this unfold in 2022.

On the horizon: More innovators will build for Medicaid

A year out from Cityblock’s unicorn-crowning, there remains a wide-open opportunity in providing digital health services for Medicaid populations. Consumers with lower incomes continue to be less likely to adopt and access telemedicine. We’re with Sachin Jain and Alyssa Jaffee on this one—we think more digital health dollars and brain-power will (and should) go to this effort.

Reflecting upon 2021 with the wisdom of hindsight makes it clear—massive change is afoot in digital health. Back-to-back years of record-breaking funding and exits, increasing consumer adoption, and underlying digital enablers like policy shifts and data infrastructure are clearing the way for the future of healthcare.

2022, all eyes are on you.

Want to stay on top of all things digital health? Don’t forget to subscribe to the Rock Weekly.

Rock Health Consulting works with enterprise companies on digital health strategy and innovation. For more information, reach out to advisory@rockhealth.com.