Patterns in capital concentration among digital health startups

Stay up to date with the latest headlines in healthcare technology and new Rock Health content. Subscribe to the Rock Weekly to keep your finger on the pulse of digital health.

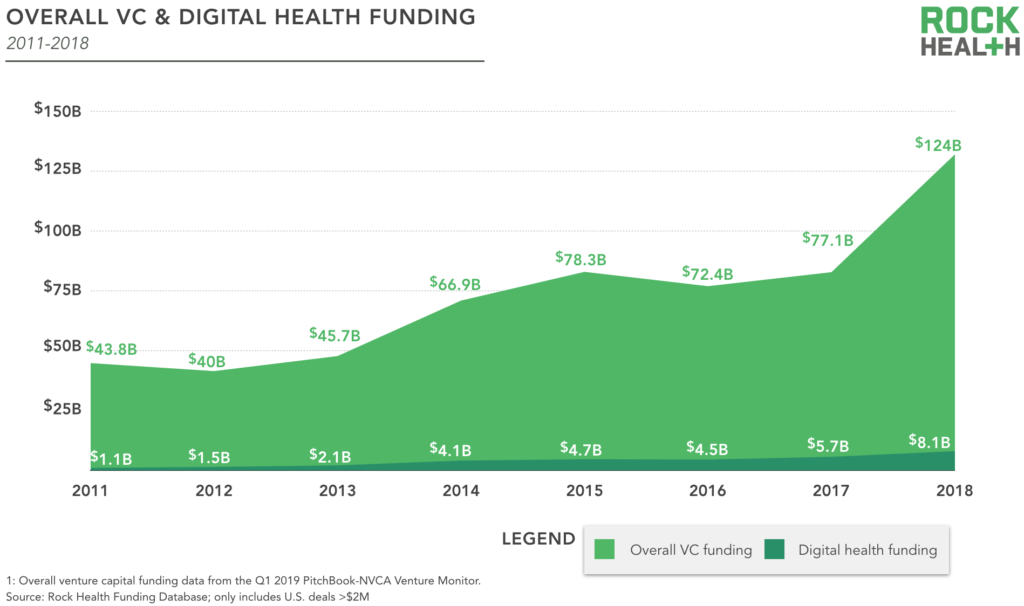

Though digital health remains a small portion of the overall venture investment ecosystem, its share has grown substantially over the past eight years. In 2011, the $1.1B invested in US-based digital health companies represented just 2% of venture capital dollars deployed into all US-based startups, according to data from the National Venture Capital Association (NVCA). Since then, digital health’s share of VC investment has grown between three- and four-fold, depending on how you measure things1. Either way, the story remains the same: Digital health is on the rise.

We reported on these trends in January and were spurred to reflect further when our good friend Michael Greeley, cofounder and General Partner at Flare Capital Partners, recently penned an insightful analysis that included a look at overall VC funding, outside of digital health. He went a level deeper, exploring the broader trend toward capital concentration, toward bigger venture capital funds and outsized investment in a small number of startup companies. Given that digital health represents a growing segment of the full VC market, we wondered if the broader market trends outlined by Greeley also represent the story within digital health.

To find out, we ran a similar analysis on digital health investments. We wondered, do the data show fewer companies capturing a larger percentage of investment dollars? Is capital concentrated similarly across investment stages (with, for example, a small number of companies accounting for a large percentage of all investment dollars)? Likewise, to what extent is capital concentrated within each investment stage (i.e., to what extent do the top few deals in a given stage account for the total dollars invested in that stage?)? We’ve lined up our analysis with excerpts from Greeley’s blog post to compare and contrast digital health funding with broader VC trends.

TL;DR

Our analysis shows that, like the broader VC industry outside digital health, digital health venture capital is, by some measures, concentrated in a relatively small number of companies. Since Q1 2018, the top five deals each quarter account for about one third of total digital health funding in that quarter. But the distribution of capital concentration does differ in some ways from the broader market. For example, while the bulk of overall VC dollars is concentrated in late stage investments, in the digital health sector less than half of invested capital went to late stage companies.

Greeley Insight #1: Evidence of continued concentration of capital, by company and by venture capital fund, persists. The top ten deals [in Q1 2019] accounted for $10.3 billion of the quarter’s activity (0.5% of the deals represented 32% of the capital).

Similarly, capital is concentrated in a small number of digital health companies. A total of $534M was invested in the top ten digital health deals of Q1 2019, representing 55% of all digital health VC dollars invested in that quarter. One third of the capital was raised across just four deals, representing 6% of the 64 Q1 deals.

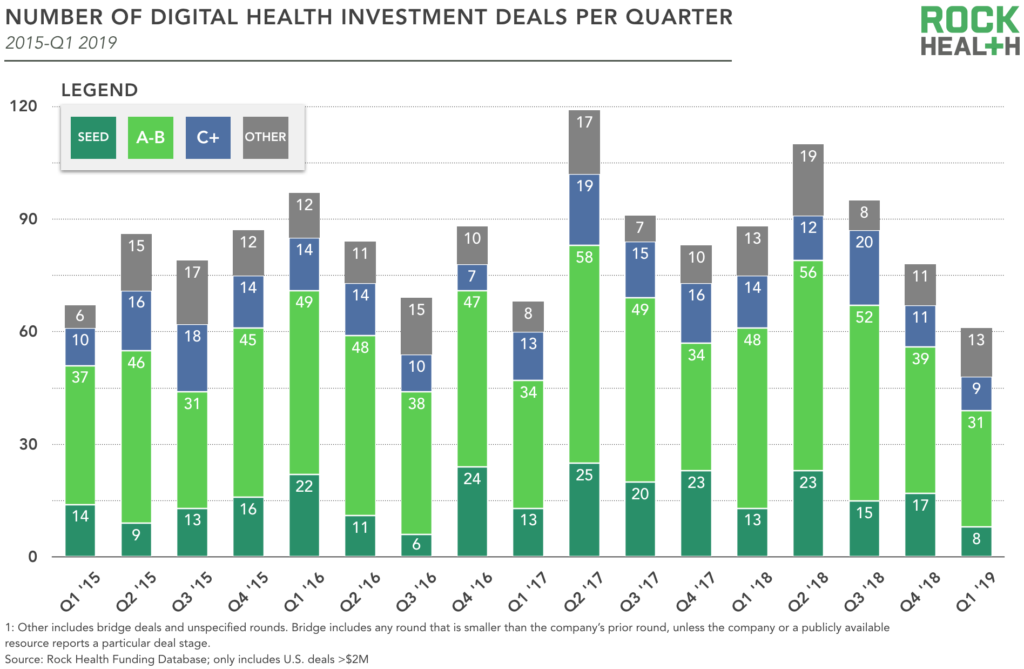

The concentration of capital in digital health in the first quarter of 2019 is not an outlier in recent history. On average, five deals accounted for about one third of total funding across each quarter of 2018. In Q3 2018, digital health’s largest ever with $3.3B invested, four deals—Peloton, 23andMe, American Well, and Butterfly Network—brought in $1.4B, or 42% of the quarter’s total capital.

Greeley insight #2: Even more notable was the decline in the number of early stage financings (Series A and B) from 1,013 to 828 quarter-over-quarter. Might this suggest increased investor aversion to early stage risk?

The number of early stage2 (Series A and B) digital health deals fell slightly from 39 in Q4 2018 to 31 in Q1 2019, a 21% drop that aligns with the 21% fall in total quarterly digital health deals across that time range. The steady decline in the number of early stage funding deals tracks with a slowdown in total number of digital health deals over the past four quarters.

Through a wider aperture, Q1 2019 had the lowest total number of early stage deals since Q3 2015. But those early stage deals have consistently accounted for around half of all digital health deals each quarter since 2015, and Q1 2019 was no different, at 51%. Rather than losing their appetite for early stage risk, digital health investors continue to deploy capital at a consistent pace into companies raising Series A and B rounds.

Greeley insight #3: If investors were nervous, they certainly seemed to be at risk of over-capitalizing companies at historically high prices. Nearly 42% of all early stage financings were greater than $10.0 million in size, accounting for almost 90% of all the capital invested. There were 15 “early stage” rounds greater than $100 million. Quite clearly concentrated investments around fewer, presumably, very high potential opportunities.

Capital concentration within early stage financings has been increasing over time. Seventeen Series A and B digital health rounds were greater than $10M in Q1 2019—that represents 55% of the 31 early stage deals, a higher percentage than VC overall in the same timeframe. In 2018, 58% of early stage digital health deals were greater than $10M—up from 40% in 2015.

It’s likely that recent record levels of capital raised by VC funds has contributed to greater funding round sizes. The $30B+ raised annually3 from 2014-2018 means investors have more capital (and competition) to finance the most promising companies, assuming the number of promising companies holds relatively constant.

Unlike the broader venture market, however, Q1 2019 didn’t include any $100M+ investments in early stage digital health companies, although Calm’s $88M Series B round came close. Since 2014, four Series B deals have been greater than $100M:

Corporate VCs (CVC) participated in rounds for all four of these highly capitalized companies. Roche, an investor in Flatiron Health, ultimately acquired the company for $1.9B in 2018. Digital health investments are a means for corporates to support promising sources of external innovation. As discussed in our Q1 2019 funding recap, CVCs participate in about one third of all digital health funding deals. That’s twice the rate of participation of corporates in VC rounds overall.

Greeley insight #4: Nearly $21.4 billion was invested in late stage opportunities (Series C and D) in 1Q19 which was two-thirds of all capital deployed in the quarter. Of the 538 late stage investments, 62% of them were greater than $100 million in size. Another sign of capital concentration.

There were just six Series C and D digital health deals in Q1 2019, totalling $175M—18% of all capital deployed in the quarter. Including rounds C-F and Growth rounds, Q1 2019 had nine late stage funding rounds with an average size of $41M, comprising 38% of funding that quarter. Across 2018, $4.1B was invested in deals Series C+, accounting for 51% of the year’s record-setting $8.1B total. Rather than focusing on select, late-stage companies, investors are still actively placing bets on the long-term prospects for the sector. Half of invested dollars were invested in early-stage rounds in 2018, and the other half invested in late stage rounds.

By these measures, venture capital in late stage digital health companies is less concentrated than in venture-backed companies overall. This aligns with the relatively young age of digital health when compared to other market segments.

Nonetheless, several late stage companies have raised large rounds in advance of anticipated liquidity events. Health Catalyst’s $100M Series F funding round was the largest in Q1 2019. It joins Peloton and Livongo, both of which raised $100M+ rounds in the past 12 months, as companies expected to IPO in 2019.

What we’ll be keeping an eye on for the rest of Q2 2019:

As we prepare for our midyear funding report release in July, we are watching to see if the dollar amounts of early stage financings will continue to grow. We are also keeping an eye on the planned 2019 IPOs of Health Catalyst, Livongo, Peloton, and Change Health. Strong early performances on the public market may boost investor confidence in late stage opportunities and pave the way for more liquidity events. As always, we’ll also be watching for Michael’s next market redux. He never disappoints!

Footnotes

1Using NVCA data alongside Rock Health’s 2018 YE funding report, digital health now represents 6% of overall VC. PwC MoneyTree reports slightly different data for total venture dollars invested, and when these numbers are used, digital health funding grows from 3% to 8% across 2011-2018.

2“Early stage” in this analysis refers to Series A and B deals. Seed stage deals are excluded to align with NVCA’s data and Michael Greeley’s analysis.

3Source: Pitchbook-NVCA Venture Monitor, Q1 2019 report