Q1 2024 digital health funding: Great (reset) expectations

Q1 2024 moved us from times of transition to full entrenchment in a new digital health funding cycle. The quarter’s $2.7B across 133 digital health deals demonstrated higher deal volume at lower check sizes. In the private markets, creative financing measures were the name of the game, while AI drove investment energy and attention refocused on startups’ abilities to demonstrate outcomes. In the public markets, stock delistings continued to change the makeup of digital health’s publicly-traded cohort, impacting how digital health players and investors think about exit potential.

Expectations are resetting for digital health players both private and public, pushing them to align to different paradigms of success (strong outcomes and healthy margins instead of high projected growth rates) and change their practices (structuring deals differently, forecasting conservatively). Read on for a breakdown of Q1’s digital health funding landscape, and how startups, investors, and innovation leaders are orienting for the year ahead.

Clipping along in a smaller funding market

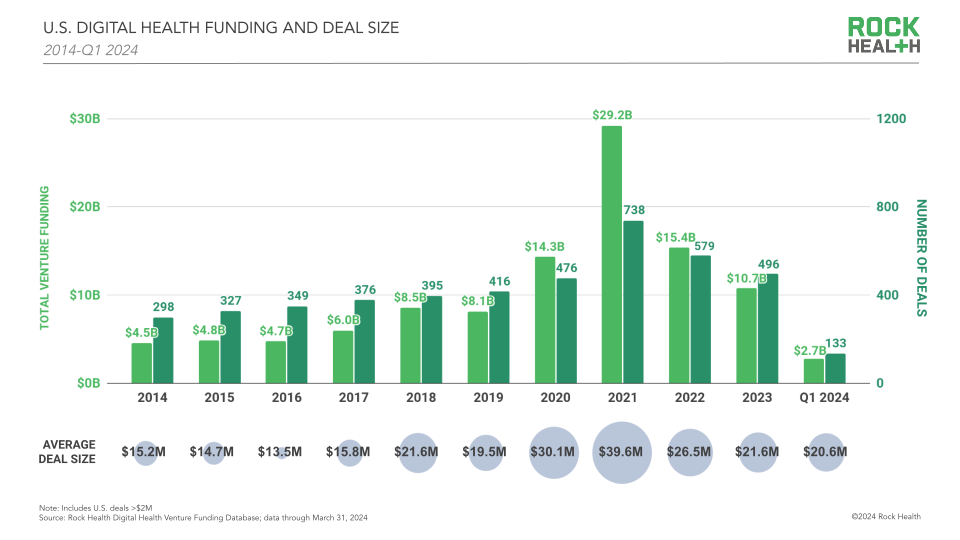

In Q1 2024, U.S. digital health funding closed with $2.7B across 133 deals, with an average deal size of $20.6M.

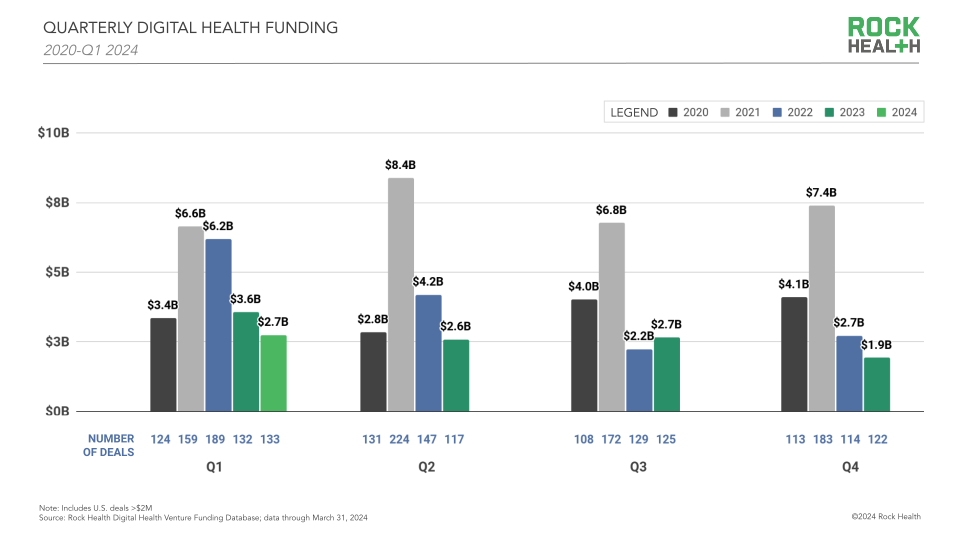

Q1 2024 was the lowest first quarter by sector funding since 2019, noteworthy given that Q1 was the top-funded quarter of the entire year in 2022 and 2023. However, the pace of deal making is strong, even with lower overall funding dollars. Q1 2024 logged 133 fundraises for digital health companies, beating out each of the past six quarters though just edging out Q1 2023’s 132. Investors and founders are finding their stride and closing deals at more measured check sizes than in previous quarters.

Continued creative fundraising

Even with more pep in dealmakers’ steps, some of 2023’s transitory funding measures have stuck around in early 2024—one of which is creative deal structuring. Creative deal structures, like the unlabeled rounds we talked about a lot in 2023, can be used to extend capital to companies that aren’t ready to raise a new round. This trend has continued into Q1; 48% of the Q1’s deals were unlabeled, compared to 44% of all digital health funding deals in 2023.

Founders are also exploring creative deal structures to lock in investor participation. Medication management player DecisionRx secured $100M as a debt facility from investment firm Carlyle; as part of the investment, Carlyle received the option to acquire 25% of the outstanding equity of DecisionRx. Meanwhile, late-stage player Transcarent is structuring terms of their $125M Series D to offer funders 2.5x their investment should the company M&A or IPO. Each approach is designed to entice investors—one with potential upside and the other with protection from downside risk.

AI investment trends upward

Beyond deal structure, Q1’s investments signaled digital health’s priority areas, with AI naturally rising to the top. 40% of Q1’s funding total went to AI-enabled companies ($1.1B across 45 deals), rising from 33% of 2023 digital health funding, and 29% of 2022’s funding pot. AI-enabled clinician scribe software Abridge raised a $150M Series C in February, just four months after raising their Series B, and AI precision health company Zephyr AI announced a $111M Series A in March. They led the cohort of AI-enabled digital health startups that raised in Q1, including Ambience Healthcare ($70M), Fabric Labs ($60M), Codametrix ($40M), Limbic ($14M), and Milu Health ($5M).

AI is a bright light in today’s funding environment, with multiple fundraises, partnerships, and acquisitions attracting investors to the space and energizing startup teams. Model evolutions, large scale rollouts, and new coalitions remind us that we’re building the infrastructure of AI-enabled healthcare in real time.

Real conversations about outcomes

Historically, outcomes reporting practices have not been consistent across digital health players, and we’ve previously noted that strong outcomes data would become more important to startup success. In Q1, significant energy was aimed at assessing the outcomes of digital health solutions. From these conversations came some important takeaways. Testing digital health solutions and comparing outcomes between solutions remains hard, especially when those solutions serve patients with multiple conditions and equity considerations. This makes it even more important to recognize players1 that continue to lead with evidence-based outcomes research. Crowded digital solution spaces are pushing enterprise buyers to seek out outcomes data as a way to differentiate players in the market and evaluate value-for-investment. As outcomes data becomes a moat and a customer draw-in, investors are seeking out companies that can demonstrate efficacy early. This makes outcomes data more central to fundraising conversations—and at earlier stages.

“There will soon be a time where the question sequence [to digital health companies] is, ‘What is your solution?’ and ‘Is there evidence showing it works?’ instead of, ‘How many customers do you have?’”

– Jared Dashevsky, Co-Founder, Healthcare Huddle

Creative deal structuring, AI excitement, and attention to outcomes are features we expect to see in this digital health funding cycle for quite a while longer. The stakes are rising for technology innovation in service of better care, and the pressure’s on digital health companies to demonstrate their contributions and validate their path forward each time they seek out new customers, users, and investment from funders.

Resets in public cohorts and exit mindsets

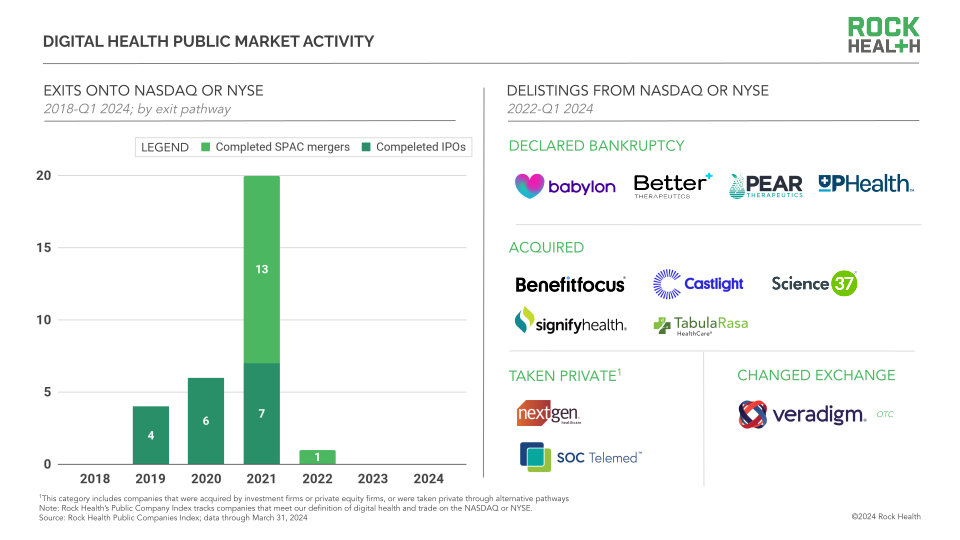

If expectations and practices feel like they’re resetting in the startup market, life on the public markets feels like a whole new ballgame. The most notable change is the shakeup in digital health’s publicly-traded class. Q1 2024 saw three digital health companies, Science 37, Better Therapeutics, and Veradigm, delist from the NASDAQ or NYSE—joining nine companies that did so since 2022 and bringing digital health’s publicly-traded cohort to 43, down from its 2021 peak of 54.2 With six other digital health stocks ending the quarter at risk of delisting, it’s possible we’ll see the sector’s publicly-traded cohort change even further in the near future.3

While some digital health companies shut down and sell their assets after delisting, going private could lead to longer-term stability for others. Development and growth planning are easier without the pressure of reporting quarterly to shareholders and market analysts, and the process of going private can be a good reset point in itself—offering a chance to restructure, shuffle assets, and make other operational changes that ultimately set an organization up for long-term success. This dynamic helps explain why companies like Veradigm might navigate delisting from the Nasdaq and acquiring another company simultaneously.

Delistings offer another important value—they recalibrate expectations for startups on the path to public exit. Startup valuations stem from expected investor returns at exit, and funders often use comps from publicly-traded players’ market capitalizations to triangulate company potential. In this way, public market delistings have a direct relationship to downshifts in startup valuations, which we see as an important reset in this market cycle. The publicly-traded players that remain, especially those that model margin management and revenue visibility, set a clear path toward success for others to follow in their footsteps.

Come on in, the water’s warm(ing up)

For digital health companies eyeing the thawing IPO market—and even those who just have a public exit on their roadmap—expectations for exit have probably never felt as real…or harrowing. As a result, some companies that previously had eyes set on Wall Street may embark on dual-track processes, pursuing IPO and M&A exit pathways concurrently to keep options open. But fear can be combated with preparation. We expect that more late-stage digital health startups will build habits of budgeting and forecasting their finances as if they were publicly-traded, even if an IPO isn’t on the immediate horizon. Shifting from growth-minded forecasting, common in venture capital, to more conservative market guidance can help to iron out kinks and set a company up for public or private exit success.

“Late-stage digital health companies are evolving from growth-oriented forecast mindsets (what if everything goes right?) to more conservative mindsets (what if some things go wrong?). This shift can strengthen a company’s financial position and increase optionality down the road, including opportunities for a potential exit.”

– Sasha Kelemen, Director of Healthcare Investment Banking, Leerink Partners

Writing new chapters

It’s a tougher, more scrutinizing climate for digital health companies on the private and public markets. Expectations around company and solution performance are rising—but great expectations are healthy for the sector to mature and evolve, and the necessary pressure will make diamonds of companies and leaders.

“Innovating in healthcare is hard, but hard can be your moat”

– Halle Tecco, Startup Founder and Investor, Founder of Rock Health

Tap into insights and strategic guidance for enterprise companies with Rock Health Advisory.

Get in touch with the venture team at Rock Health Capital.

Join us in building a more equitable future at RockHealth.org.

And last but not least, stay plugged into the Rock Health community and all things digital health with the Rock Weekly.

Footnotes

- Virta Health and Omada are Rock Health portfolio companies.

- Rock Health’s Public Company Index tracks companies that meet our definition of digital health and trade on the NASDAQ or NYSE.

- If a company’s stock trades under $1.00 for a certain consecutive period, the security may become noncompliant with exchange requirements and be required to delist; publicly traded digital health companies that ended Q1 2024 trading under $1.00 include Streamline Health Solutions, American Well Corporation (Amwell), Movano Inc., 23andMe, ShareCare Inc., and Vicarious Surgical.