Q3 2022 digital health funding: The market isn’t the same as it was

Given the year’s choppy venture waters and public market correction, investors are holding back from the market, waiting to strike once things stabilize. Q3’s low funding numbers—the lowest quarterly funding total in the past 11 quarters—reflect that sentiment. Yet, even though the market isn’t the same as it was, this quarter has featured some standout digital health activity, including major acquisitions by Amazon and CVS, and Akili’s SPAC close, this year’s first digital health public exit.

As we enter the last 90 days of 2022, a few key themes have emerged throughout Q3: 1) smaller checks across the board, 2) a focus on early-stage funding, 3) reprioritization of technology investments, and 4) an exit market that’s beginning to thaw. Each hints at the type of activity we may see in Q4 and the early days of 2023. In this piece, we’ll recap Q3’s venture funding and public market activity, with an eye toward what these movements signal for the last quarter of the year.

So down and under pressure

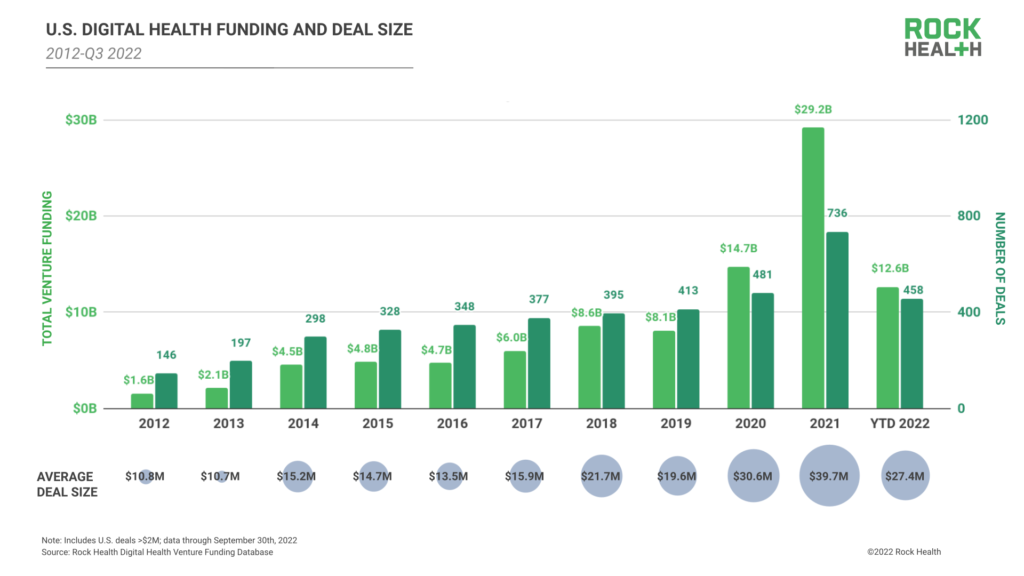

With $2.2B raised across 125 deals, Q3 takes the title of the smallest funding quarter in the sector for all of 2022—in fact, it’s the lowest quarter by dollars raised in digital health since Q4 2019 ($2.1B). With Q3 included, 2022 year-to-date funding totals $12.6B across 458 deals, raising doubts that this year’s digital health pot will reach even half of last year’s $29.2B haul.

Q3’s lack of funding isn’t altogether surprising. Earlier this year, we discussed funding froth drying up in digital health and in VC more broadly in response to macroeconomic forces (inflation, interest rates, supply chain woes) as well as a shift in investor mindset from the high times of 2021. However, the sharp decline in funding reflects a deeper underlying change: this quarter’s near-complete absence of late-stage digital health investments.

As a backdrop, overall funding plummeted 48% between Q2 ($4.2B) and Q3 2022 ($2.2B). However, deal count fell less sharply, by 14 percent. Analysis of Rock Health’s funding database suggests that the number of smaller and generally earlier-stage deals remained relatively stable. Our analysis further suggests that smaller deal size—rather than fewer deals—pushed down the overall quarterly total.

Meanwhile, Q3 recorded only six funding raises of Series C or higher, accounting for less than 5% of the quarter’s total deal volume—a marked departure from Q2’s 19 Series C+ raises and Q1’s thirty-two. And, most notably, Q3 logged just two digital health mega raises totalling $100M or more: one from heart attack prediction app Cleerly ($223M) and another from mental health provider support toolkit Alma ($130M). By comparison, the quarterly average number of megadeals across 2021 was 22 deals, totalling 88 megadeals through the year. While 2021’s trend of $100M+ raises held somewhat steady throughout Q1 of 2022 (18 megadeals), the pace of megadeal funding started to fall in Q2 (11 megadeals) before nose diving in Q3.

Looking for the late-stage deals

We believe there are three likely explanations for the pullback in late-stage digital health funding:

- A portion of the “missing deals” already happened, pulled forward to 2021 in order take advantage of last year’s funding-friendly climate

- Another portion of deals are in fact happening, but behind closed doors via arrangements like round extensions and venture debt

- A final portion of deals are simply not taking place

Let’s unpack the first one—that many late-stage deals were raised early to strike while the iron was hot in 2021. Seeing money on the table (meaning cash was cheap and readily available), many founders were chomping at the bit to secure investment at strong valuations. Together with high market interest (i.e., investors were eager to get on the cap tables of digital health startups) and an understanding that this “free lunch” wouldn’t last forever, a number of companies chose to accelerate rounds into 2021 that may otherwise have been offered in 2022. Our data supports this hypothesis: 64 companies raised twice in 2021—36% more than 2020, and 113% more than 2018.

“Part of our strategic calculus is that it’s always best to raise when you’re in a position of choosing to raise, rather than needing to raise.”

— Steve Gutentag, Co-Founder and CEO, Thirty Madison

Second, we hypothesize that some of the “missing” late-stage digital health deals have taken place this year, but without the usual fanfare typical of a boom cycle. At some point in 2022, it’s likely that growth-stage digital health startups in need of additional cash turned to investors already on their cap tables for quiet cash infusions (inside rounds), or pursued extension rounds, bridge rounds, or venture debt to raise new capital without otherwise impacting their share price. While not all extension rounds reflect a cash need (some extensions focus on bringing in high-value investors—just ask Biofourmis), founders may shy away from publicizing these activities as they can be perceived by the market as negative signals. While publicly-sourced datasets like Rock Health’s Venture Funding Database1 can’t capture the delicate sound of these capitalizations, that doesn’t mean they’re not happening.

Lastly, given 2022’s tighter capital markets, it’s possible that some late stage raises slated for 2022 simply didn’t happen, and that these digital health startups are making do by running leaner businesses. Whether avoiding a dreaded down round or delaying until the IPO market reopens, late-stage players are forced to stretch existing cash reserves by streamlining operations, adopting measures such as cutting customer acquisition spend or reducing workforce (2022 has seen a steady trickle of digital health layoffs). Navigating layoffs and frustration by delayed exits, we expect some of today’s digital health talent to migrate from late-stage players to up-and-coming digital health startups for greater upside opportunity, or to head over to enterprise healthcare teams in search of stability—though these companies too have not been immune to budget cuts and layoffs.

“In today’s environment, many companies are going to need to think about how to get ahead of liquidity issues including pursuing down rounds or some other form of more dilutive financing. On the other hand, there continues to be capital available at attractive valuations for best-in-class companies with defensible business models and compelling unit economics.”

— T.J. Carella, Managing Director, Warburg Pincus LLC

For startups that are making do, there’s a good chance they won’t need to be running up that hill much longer. Dry powder has grown amid 2022’s investment pullback, and investors will need to deploy capital to match LP expectations. Plus, signals of a revived IPO market and a flurry of digital health acquisition activity—a topic Rock Health will be diving into in early November—suggest that paths are reopening for late-stage startups to receive their golden tickets.

Shifts in funding allocation: Emptying the bank account

With Q3’s dearth of late-stage deal opportunities, we see investors on the hunt for early-stage, complementary businesses to round out their portfolios. As such, 2022’s funding data to date offers a unique opportunity to examine investment patterns by value proposition, therapeutic area, and technology type as bellwethers of digital health growth areas for quarters to come.

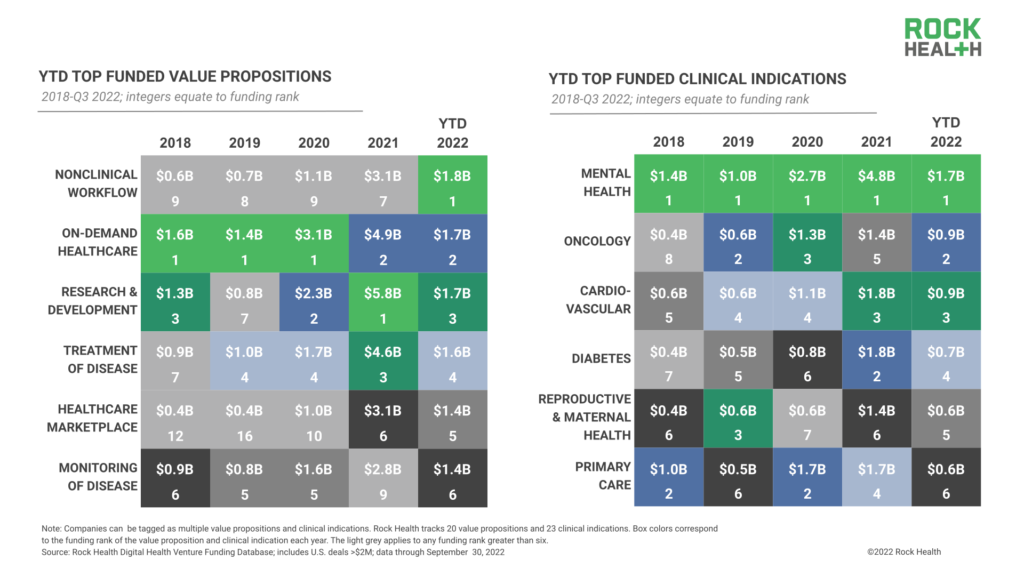

Looking closer, Q3’s funding allocations certainly hint at sector shifts. Digital health startups catalyzing R&D for biopharma and medtech fell from first place to third place with $1.7B raised so far in 2022, while digital health players specializing in nonclinical workflow solutions jumped to first place with $1.8B in funding, led by Alma’s megadeal, Grow Therapy’s $75M haul, and a $72M check for practice management suite Tebra. To us, strong funding flows to workflow tools mean that addressing healthcare staff shortages and employee burnout remain top priorities. This trend is also reflected in funding for healthcare marketplaces, the fifth most-funded value proposition, led by nurse staffing platform Incredible Health’s $80M raise in August.

While funding for digital mental health startups continues to lead investment activity by therapeutic area, focus on complex disease states is growing. Funding for digital health startups addressing oncology care came in second place with $946M, with Q3 raises from startups like Faeth Therapeutics ($47M), which designs precision nutrition programs for cancer patients. However, with investment totals similar across clinical indications, funding rankings could shift significantly before the year closes.

Funding shake ups are also happening on the technology front. While startups incorporating telemedicine components retained the second-top spot in investment activity—a position held since 2015, just behind funding for startups incorporating artificial intelligence—an oversupplied market, declining yields on direct-to-consumer advertising, virtual prescribing scrutiny, and difficult trajectories of public telemedicine leaders like Teladoc have increased investor skepticism toward telemedicine’s cash crop of virtual care providers, raising only $2B so far this year. Ultimately, if funding pace holds steady, investment in telemedicine startups will close 2022 with $2.7B—just over one-third of the category’s 2021 total and its lowest funding pot since 2019.

With investor interest in telemedicine startups waning, attention is turning to immersive and decentralized health-tech enablers. Catalyzed by FDA approvals for immersive physician tools and digital therapeutics in late 2021, this year’s funding for digital health startups applying augmented and virtual reality (AR/VR) technologies reached a new high, logging $239M through Q3 2022 compared to $198M in all of 2021. And while deal sizes for AR/VR digital health startups remain relatively small (reflective of early-stage investments), average deal size has doubled from $18M in 2021 to $34.2M through Q3 2022, bolstered by rounds like Apprentice.io’s $100M in January. Again, because small funding pots are more sensitive to individual deals, we may see rankings shift by the end of the year based on Q4 activity—but watching out for immersive digital health applications seems like a safe bet.

“Science and technology have been coming together in unprecedented ways, and there’s a growing opportunity for startups to deploy emerging tech to address healthcare challenges.”

— Jim Tananbaum, MD, Founder and CEO, Foresite Capital

Akili’s patience was waning

Digital health’s almost-yearlong public exit silence broke this quarter with August’s SPAC merger between digital therapeutics maker Akili Interactive and Chamath Palihapitiya’s Social Capital Suvretta Holdings Corp I. Akili is best known for developing EndeavorRx, an FDA-approved video game-based digital therapy addressing ADHD in children. Akili disclosed that funds raised from the public exit would be used to support EndeavorRx’s broader commercial launch.

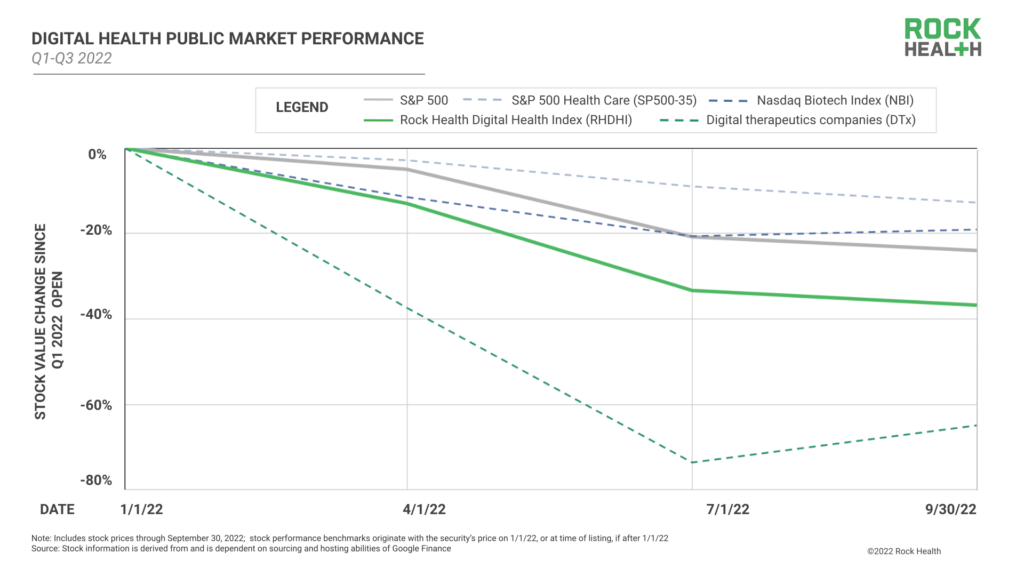

Despite generating excitement as 2022’s first digital health exit, Akili Interactive suffered a rocky lurch onto the markets. The company’s stock price, which opened its first day trading as high as $36.06 per share, fell to $7.15 within the first 24 hours, and finished the quarter near $2.26. Why the drop? While Akili might just be suffering the growing pains of entering onto the public market, it’s also worth noting that since the start of 2022, the three publicly-traded DTx manufacturers—Better Therapeutics, Pear Therapeutics, and Akili—significantly underperformed the Rock Health Digital Health Index (RHDHI). At the start of Q3 2022 (July 1, 2022), Better and Pear’s stock prices averaged just $1.52, together averaging a 74% drop from their 2022 open prices and underperforming the RHDHI by 40 percentage points. Akili’s listing brought the DTx cohort’s average stock price up to $2.02 at the end of Q3 2022 (September 30, 2022), clocking in 28 percentage points below the RHDHI.

One possible explanation for digital therapeutics companies’ poor market performance may lie in a “revenue penalty”—meaning that stock price is being driven down by investors’ concerns regarding the companies’ abilities to drive recurring revenue. For example, Akili and Pear first gained revenue traction via strategic development or licensing contracts with pharmaceutical manufacturers to bring digital therapeutics to new patient communities or geographic regions. However, as these contracts ended, Pear and Akili both faced roadblocks transitioning to commercial sales via provider or pharmaceutical business models—with some of the biggest challenges being reimbursement pathways and provider adoption hurdles. In an S-4 amendment issued in July, Akili reported just $6K in revenue for Q1 2022 and $538K in revenue for all of 2021—down from its licensing heydays of 2020, when annual revenue totalled closer to $4M.

While our hypothesis around DTx’s “revenue penalty” requires some more digging (e.g., comparing Akili’s company data and stock performance to other recently-exited digital health players, which is difficult to do during an IPO dryspell) we’re interested if and how the DTx cohort continues to perform relative to non-DTx digital health securities. While DTx players may be feeling stretched thin—Pear underwent a restructuring in July, inclusive of layoffs—market signals such as Evernorth’s digital formulary expansion and recent DTx-provider partnerships may indicate better days ahead.

Ain’t worried ‘bout it (right now)

While Q1 and Q2 2022 may have read as adjustment periods coming off of 2021, Q3 represented a clear departure from the COVID-driven digital health financial market, including changed market dynamics, shifts in investor focus to prioritize workflow support and complex diseases, and growing excitement for new technologies and immersive solutions. Significantly, as investors at Rock Health Capital, we’ve seen a gradual return to pre-pandemic asset pricing in the pre-Seed through Series A deal flow. Rational prices promote long-term market health and, if anything, diminish near-term worries. Nonetheless, we’ll be watching Q4 closely to see which of these trends take hold to shape the market going into 2023. Small ripples can lead to big waves—and we’re curious to see where these directional turns lead.

A big thank you to our friends and thought partners at Flare Capital Partners. All quotes featured in this report were collected from the Flare Capital Partners Expert Roundtable Series: Fundraising in a Turbulent Capital Market, held on September 27, 2022.

Rock Health Capital continues to invest in entrepreneurs bringing unique and innovative technology to healthcare. We would love to hear from you. Get in touch!

Rock Health Advisory provides guidance on digital health strategy, access to proprietary funding databases, and in-depth perspectives on the digital health market. For digital health insights targeted to your needs, drop us a note.

Finally, stay up to date with the latest headlines in healthcare technology and Rock Health news by subscribing to the Rock Weekly.