Amidst a record $3.1B funding in Q1 2020, digital health braces for COVID-19 impact

Digital health funding was on a tear in early Q1—before the COVID-19 pandemic rattled the US economy

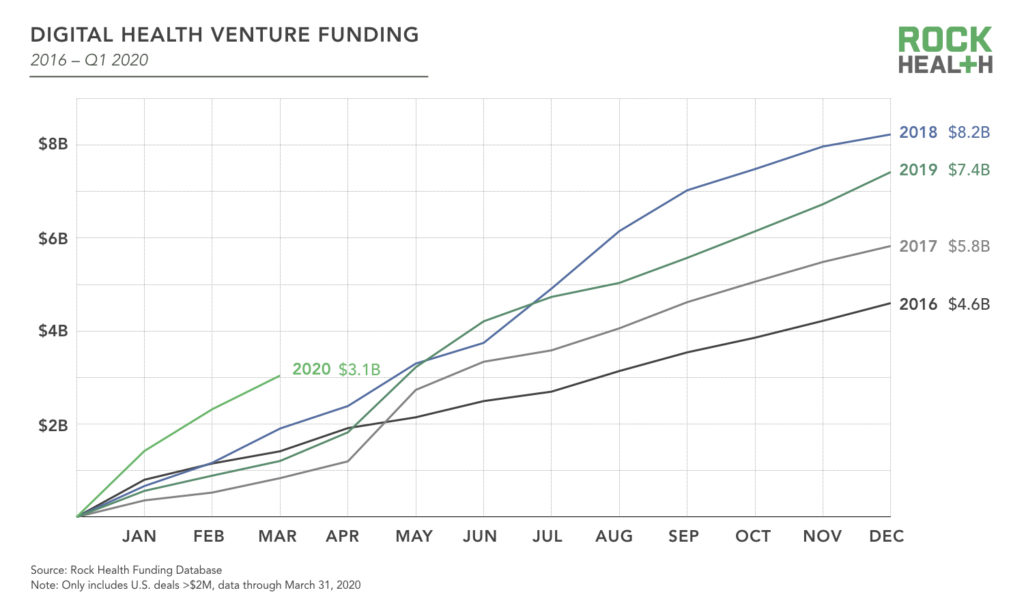

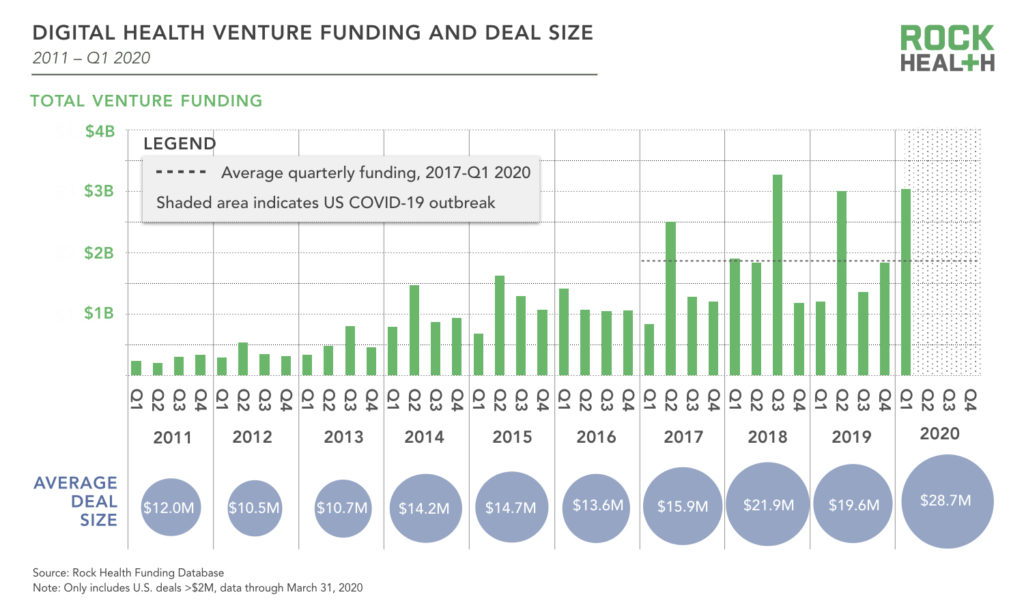

Digital health venture funding was off to the races in Q1 of 2020, following a moderation in investment between 2018 and 2019. Though a broad pullback in venture investing was likely under way at the start of 2020, US digital health companies nonetheless raised a whopping $3.1B across 107 deals—more than 1.5X the total funding in Q1 of any previous year. In fact, Q1 2020 was the second largest quarter in terms of total funding, and 57% greater than the average quarterly funding across 2018-2019. This caps off the largest ever twelve month funding period (TTM) for digital health, with $9.3B invested across Q2 2019-Q1 2020.

Of course, this is not a post about historic funding levels—it is a story of healthy funding momentum cut off at the knees by a global pandemic. Though some of the economic blow will be tempered by demand for connected healthcare, we do not anticipate investment activity to keep pace with Q1 levels in the coming months.

Today, roughly four months after the first case of COVID-19 was detected in China, we are living through a historic global health crisis. Unprecedented public market volatility signals a capital market that is actively pricing in the expectation of a sharp economic downturn driven by multiple factors: quarantine-driven shocks to both supply and demand; a sharp increase in unemployment; an unrelated but ill-timed oil price war; and new patterns of remote work, education, and physical distancing—all changes to culture that may persist even after the crisis has passed. Forecasting the spread of SARS-CoV-2 and the road to recovery remains a guessing game due to the persistent absence of systematic, widespread epidemiological surveillance. Venture investors have sounded the alarm for startups—many of whom have already taken a huge hit to revenue, and are making deep cuts. To take an initial pulse of this new reality, we surveyed a dozen leading healthcare investors between March 16 and March 20 about the outlook for digital health venture funding in the coming months. We share their perspectives below.

We’ll dig deeper into digital health investment in the shadow of a downturn at our ninth annual Rock Health Summit on September 22-23 in San Francisco. Get your early bird ticket here.

Our TL;DR take on COVID-19’s impact on digital health funding

Our last report anticipated a more challenging fundraising environment in 2020. But we could not have predicted the altogether new territory we’ve entered. A COVID-19-induced economic downturn is under way, but the differential impact across sectors of the economy has yet to play out. The healthcare industry is hardly immune to the financial stresses of the economy at large and although digital health startups are at the center of the response to COVID-19, they’re no exception. Yet two important factors may buffer a contraction in digital health venture funding.

First, venture capital firms are still sitting on record levels of dry powder. Because venture fund partnership agreements make it difficult for limited partners (LPs, who supply the capital) to back away, “defaults” are a rare event. Add to this the fact that venture investors are typically obliged to deploy LPs’ committed capital in a fixed time frame. While some investors may “take a breather” as valuations reset, they can’t sit on the sidelines forever.

Second, digital health startups are, in some cases, uniquely positioned to play both an outsized role in ameliorating the immediate effects of the crisis and in driving sustained, positive changes in its aftermath. While other industries (or other segments within healthcare) must simply cope, some digital health companies are in the drivers’ seat.

Faster down than back up again

The scale and speed of COVID-19’s economic impact is unlike anything the US has seen in decades. The stock market began a rapid decline in mid-February. On March 16, 2020 the DOW plunged almost 3,000 points, the largest drop since 1987. As of April 3, 2020, the S&P 500 is down more than 25% from its February high and still reeling from the fastest 30% decline ever. After setting the record for all-time low volatility just over two years ago, public markets have entered a period of selloff and record high volatility—the US economy appears set to enter a recession, if it hasn’t entered one already. Notably, of the twelve investors we surveyed two weeks ago, ten “strongly agree” that a “recession is either already underway or will occur in 2020.”

Governments worldwide have intervened in an unprecedented and necessary (if imperfect) manner to create liquidity within the financial system and directly support individuals and businesses. On March 27, the US federal government passed the largest stimulus bill in history. Among other measures, it includes expanded unemployment benefits, $500B to support corporations, and $1,200 in direct payments for most American taxpayers. The Fed is also taking dramatic actions unlike any since the financial crisis of 2008-2009, including plans to purchase an unlimited number of Treasuries, dropping interest rates to zero, and for the first time ever, purchasing corporate bonds and corporate bond ETFs.

Access to capital will tighten

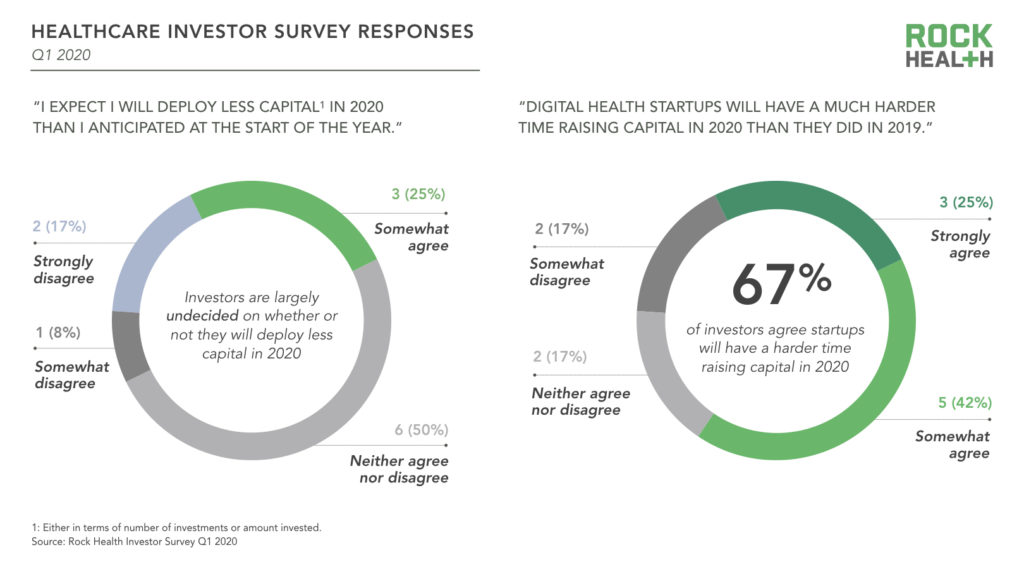

There is every reason to believe that the dual supply and demand shocks will be a significant event for all companies, and startups are no less vulnerable. As Sequoia Capital noted, the novel coronavirus has and will undoubtedly cause supply chain disruptions, reductions in growth forecasts, and changes in hiring plans. Eight of the twelve investors we surveyed felt that digital health startups will have a “much harder time” raising capital in 2020 than they did in 2019.

Access to private capital won’t contract as rapidly as public capital

The size and speed of the public markets’ selloff has been breathtaking. Private markets will likely not experience as dramatic of a downturn because private equity, of which venture capital is a subset, comes from capital committed by limited partners. Unless those commitments are unwound (a difficult process), PE and venture firms are obligated to continue investing the funds raised prior to the current crisis. Just three of the twelve surveyed healthcare investors “somewhat agreed”1 with the statement “I am concerned that LPs may default on capital calls” (i.e., may not have the funds or liquidity needed to meet their capital commitment).2

The upshot of several years of heightened VC and PE fund raising is that firms are collectively sitting on a record amount of dry powder—funds that have been raised but not yet deployed. This may, to some extent, help dampen the near term market shock on the availability of capital to entrepreneurs.

Surveyed investors are largely not reducing the amount of capital they plan to invest in 2020—only three “somewhat agreed” (and no one “strongly agreed”) with the statement “I expect I will deploy less capital3 in 2020 than I anticipated at the start of the year.” There is an apparent tension between respondents’ plans to maintain their investment activity this year and their expectation that startups will have a much harder time raising capital in 2020. The discrepancy may reflect a belief that in aggregate, digital health investors will deploy capital into new investments more cautiously during a recession while they simultaneously take action to support their existing portfolio companies. With that in mind, we expect to see a flight to quality with competition for the best deals—investors with capital to deploy will continue to invest in companies that are positioned to succeed in the rapidly evolving market for healthcare technology.

Our physical processes have forcibly changed but our activity has not–we are continuing to pursue investments in digital health, microbiome, biotech, and nutrition. In digital health, we see an urgency for investment as the current upheaval calls for an accelerated adoption, evolution, and creation of digital health solutions.

Isabelle de Cremoux, Managing Partner, Seventure

Digital health is uniquely suited to expand the capacity of our strained healthcare system

There is no silver lining to the SARS-CoV-2 pandemic and the economic downturn it portends. However, the digital health sector is uniquely positioned to tackle many current and upcoming challenges. We are witnessing a new set of healthcare needs emerge as health systems around the world respond to capacity constraints and restrictions on in-person interactions. Others are racing time to expand testing capacity, and develop a vaccine and cure. Digital health companies offer technologies that support the delivery of care virtually, scaling the medical workforce, and the acceleration of R&D for diagnostics and treatments.

The most significant problem facing healthcare is a historic mismatch between supply and demand. This was true before the onset of the pandemic and it will remain true after COVID-19 peaks. The human capital (MDs and nurses) mismatch is most acute today, hence the lift off for telemedicine and remote patient monitoring solutions. If there is one thing I am confident in predicting, it is that overcoming COVID-19 will reinforce that healthcare cannot go back to a time when virtual or automated care was not normal operating procedure.

Tom Cassels, President, Rock Health Inc.

We at Rock Health are fortunate to support and work alongside many digital health companies rising to the occasion by working long hours, accelerating project timelines, and providing their services and technology in new ways (and sometimes at no cost) to combat this public health crisis.

Telemedicine, in particular, is deployed at the front lines of the pandemic. Although there have been some reports of growing pains as telemedicine providers adjust to a rapid uptick in demand, telemedicine startups are rapidly responding to the escalating health crisis:

- Doctor on Demand launched an online assessment to evaluate COVID-19 risk

- MDLIVE is offering appointments for individuals with coronavirus symptoms as well as pandemic-related mental health issues

- 98point6 announced plans to triple its physician workforce over a month-long period in response to surging demand

- PlushCare has been ramping up its physician hiring plans by 50% to 100%

Federal and state governments are also clearing regulatory barriers to telemedicine adoption, opening the door for virtual care to be the new normal for the healthcare industry:

- Medicare announced it would temporarily cover telemedicine for its beneficiaries for services provided during the pandemic

- HHS announced it would waive HIPAA penalties for good faith use of telehealth during the COVID-19 pandemic, allowing providers to use tools like FaceTime during their appointments

- Vice President Pence announced potential plans to allow physicians to practice across state lines without state-specific licenses

This is undoubtedly a tipping point for telemedicine adoption, which has been rising steadily for several years. The use of live video telemedicine has increased 4.5X since 2015—to 32% of respondents in 2019—in Rock Health’s annual Digital Health Consumer Adoption Survey. We expect adoption to tick up significantly this year, and are cautiously optimistic that consumers and providers who use telemedicine for the first time will remain long-term users. The investors we surveyed also expect virtual care to gain traction: 100% of respondents agree telemedicine is positioned for greater growth in 2020 than originally anticipated because of the pandemic.

While telemedicine has earned the spotlight these past few weeks, countless other digital health innovations are supporting the response to the pandemic. In particular, surveyed investors anticipate growth in remote monitoring, symptom checkers, and triage tools. For more on digital health companies’ pandemic responses, check out this list from Catalyst @ Health 2.0.

The onslaught of COVID-19 belies a Q1 surge in late-stage funding rounds

The digital health funding environment in Q1 is not a good bellwether for the remainder of 2020. But two Q1 trends stand out:

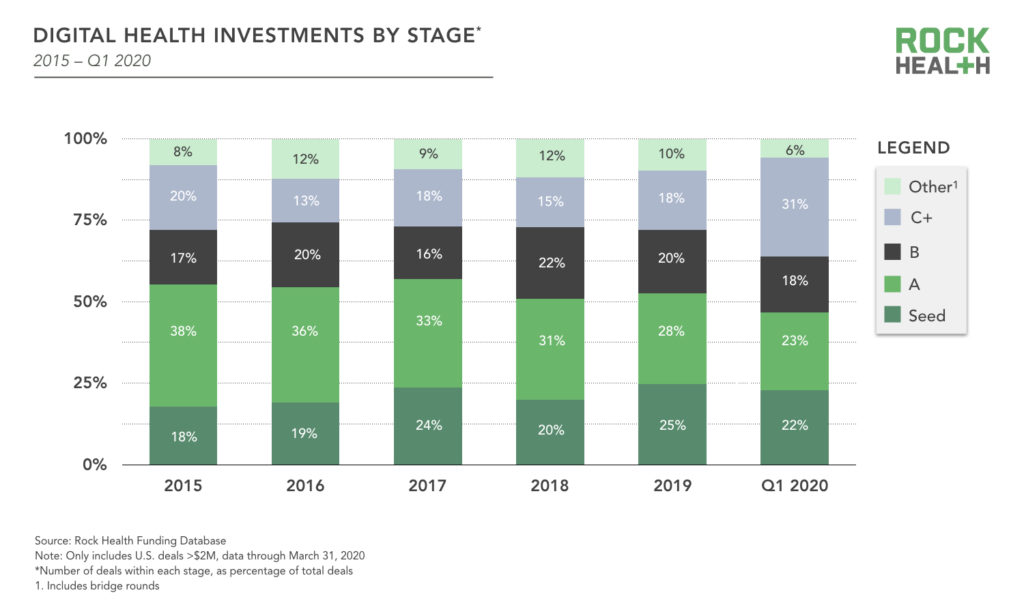

- Thirty-one percent (31%) of deals in Q1 2020 were Series C or later—1.8X the average annual proportion of C+ stage deals across 2015-2019

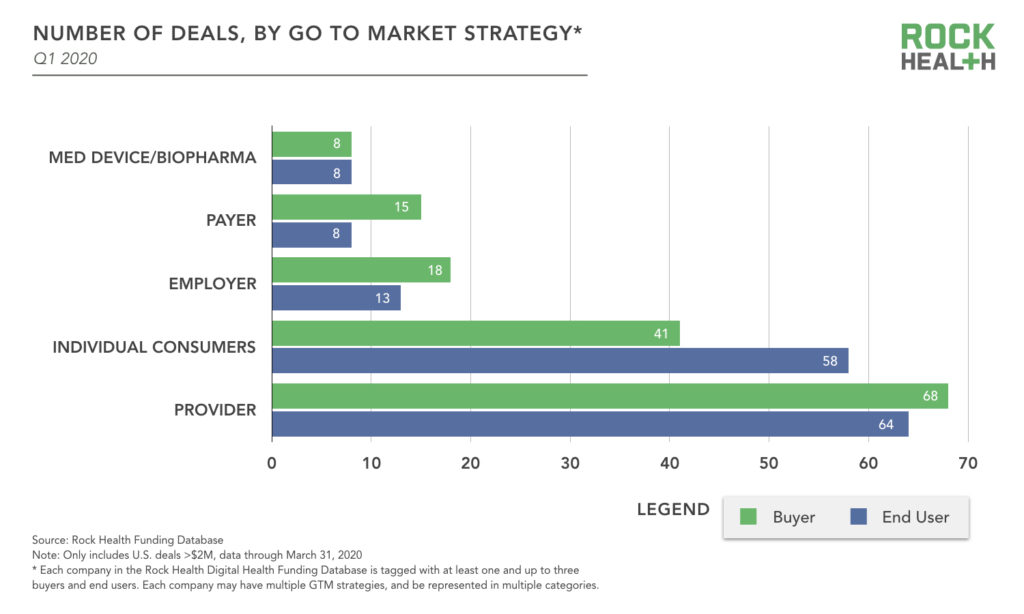

- Sixty-three percent (63%) of all funded companies in Q1 2020 sell to providers—far more than are selling to any other buyer group in digital health

Large, late stage deals accounted for a significant portion of Q1 2020 funding

Average deal size spiked in Q1 2020 at $29M—compared to $19.5M in 2019 and $21.5M in 2018. This follows naturally from the notable shift in funding toward later stage deals as the digital health market has matured.

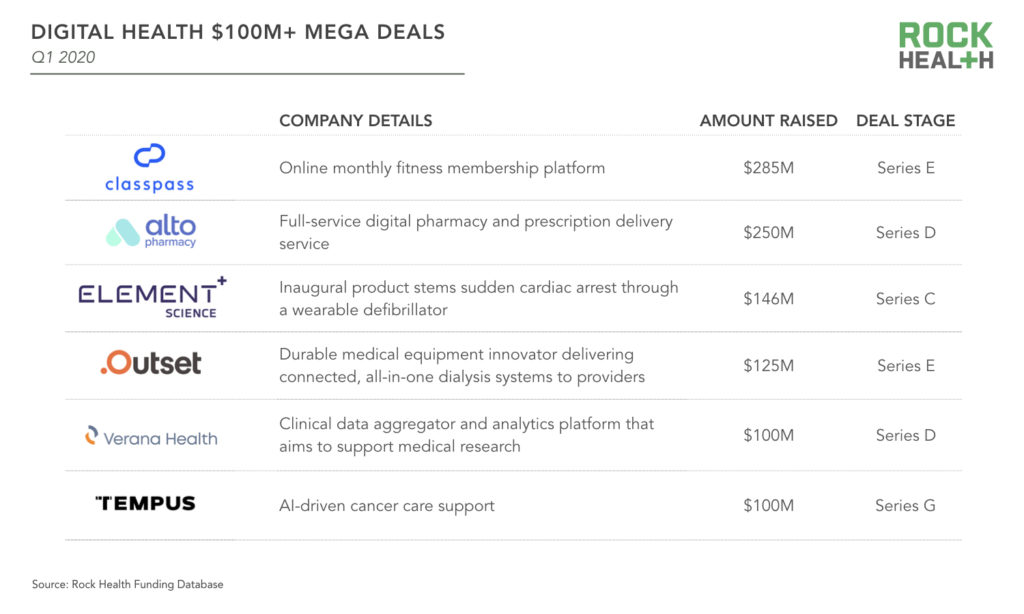

Six “mega deals”—funding rounds of $100M or more—accounted for 33% of total digital health funding in Q1:

Exits: A diminished outlook for IPOs and M&A in 2020

A shift in digital health capital allocation towards late-stage (Series C+) deals would normally signal a pipeline of companies gearing up for exit. However, an impending recession will diminish public investor appetite for IPOs. Eleven of the twelve investors we surveyed felt that the digital health IPO window is shut for 2020 (respondents either “disagreed” or “disagreed strongly” with the statement “digital health companies who were anticipating an IPO in 2020 will go public in 2020 as planned”). However, those same investors were slightly less aligned in their predictions about the M&A market. Eight of the twelve respondents believe “market volatility will significantly slow down digital health M&A activity” (seven “somewhat agreed” and one “strongly agreed”).

Investors bet big on provider-focused innovation even before COVID-19 hit the US

A significant proportion of startups funded in Q1 2020 develop solutions for providers seeking to improve efficacy, capacity, and workflows with technology. Sixty-eight startups serving providers raised rounds in Q1 2019. As providers are now consumed by COVID-19, we’ll be keeping an eye on this trend and whether startups face challenges selling to this group—or if they see sales cycles shortened given the urgency for connected care.

In Q1 of 2020, investors backed a wide variety of solutions for providers, clinics, and health systems, with the largest rounds focusing on data collection, clinical workflow, and health system administration:

- Innovaccer, a population health management platform that supports pay-for-performance solutions and SDOH management, raised $70M in a Series C.

- Komodo Health raised $50M in a Series C to continue building out its data set of longitudinal healthcare experiences used to inform and improve clinical decision-making.

- IntelyCare offers a “smart” nurse staffing solution to optimize system capacity needs and employment flexibility and raised $45M in a Series B in February.

Two of the six previously mentioned mega deals—Outset Medical and Tempus—sell directly to providers.

Innovation that scales the capacity of healthcare providers will be critical to the national response to COVID-19. We are hopeful to see how startups will work alongside their healthcare system partners to adjust to this new imperative.

As always, Rock Health remains committed to investing in the entrepreneurs bringing life-saving technology to healthcare. We’re continuing to meet with companies (virtually) and would love to hear from you—get in touch.

Thank you to to our contributors

This report would not have been possible without the help of a number of healthcare investors representing the following firms who graciously participated in our COVID-19 Digital Health Impact Survey:

- Andreessen Horowitz

- DigiTx Partners

- FCA Venture Partners

- Lifeforce Capital

- NEA

- Refactor Capital

- Rock Health

- Seventure

- Venrock

For access to Rock Health’s investment databases, get in touch about becoming a Rock Health partner.

Stay up to date with the latest headlines in healthcare technology and new Rock Health research. Subscribe to the Rock Weekly.

Footnotes

1None “strongly agreed” with the statement “I am concerned that LPs may default on capital calls”

2Notably, the survey went out before the stimulus bill passed and before most of the terms of the bill were public. Unfortunately, we did not have time to ask respondents if their level of concern changed after seeing the scope of the bill’s support for the financial system.

3Either in terms of number of investments or amount invested