Q3 2021 digital health funding: To $20B and beyond!

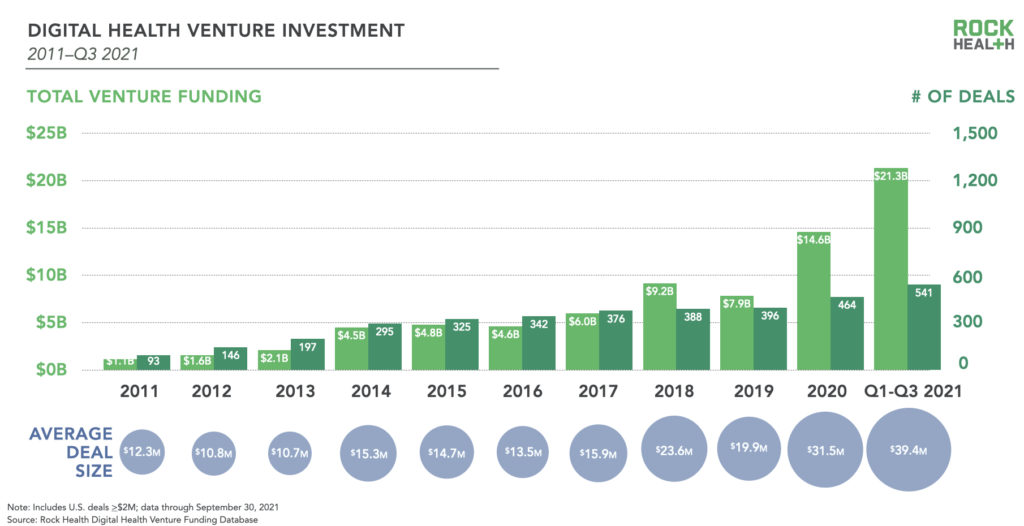

We closed out 2020 announcing that it was the first year digital health passed $10B in total funding, finishing at $14.6B.1 Not to be outdone, 2021 has already surpassed the $20B mark with three months left in the year. Between Q1-Q3, 2021’s total funding amounted to $21.3B across 541 deals, with an average deal size of $39.4M.

In this digital health funding recap, we analyze how 2021’s funding swell is changing market expectations and empowering investors to “venture” outside of historical funding patterns, with more dollars going toward women-led companies, women+ digital health,2 and health equity solutions. In light of Q3, we’ll also take a critical look at how entrepreneurs and investors can contextualize today’s opportunities and understand consolidation moves that are reshaping the sector.

A record-breaking year continues

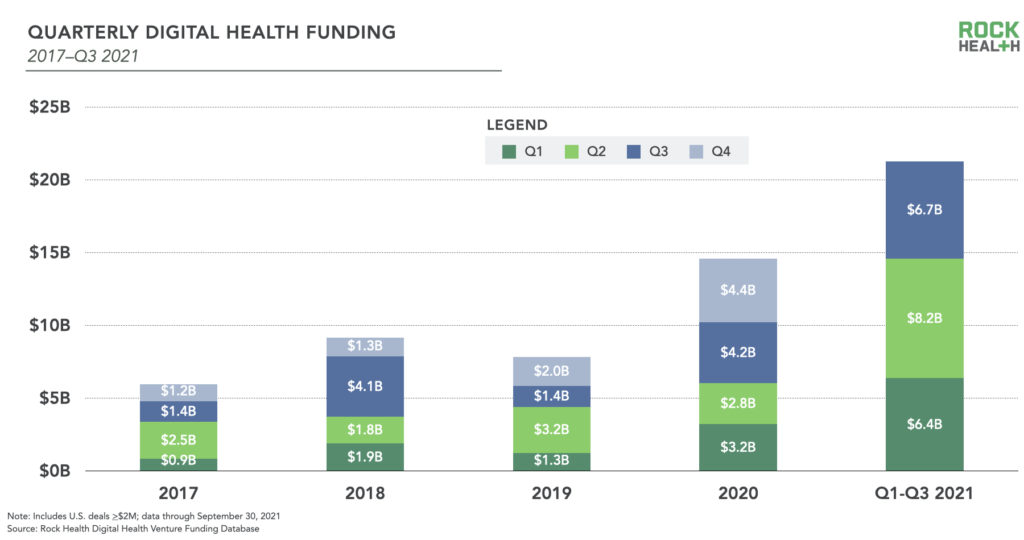

Digital health funding continues to break records during 2021’s blockbuster year, with the three highest-funded quarters ever. After the impressive sprint of Q2’s $8.2B (a quarter that outpaced 2019’s entire annual funding), Q3 experienced a slight funding slowdown that more closely resembled Q1. Q3 2021 secured $6.7B across 169 deals, just beating out Q1 ($6.4B)3 to be the second-highest quarter of digital health funding ever, surpassed only by its immediate predecessor Q2 ($8.2B).

A main driver of Q3 2021’s slow down relative to Q2? Overall deal volume decreased in Q3 (169) compared to the funding blitz of Q2 (223). Additionally, while Q1 and Q2 had their funding driven by approximately two dozen $100M mega deals each (22 in Q1 and 25 in Q2), Q3 only clocked in 15 mega deals. These deals added $3.1B to Q3’s funding pot, compared to mega deal totals of $4.1B and $4.5B in Q1 and Q2.

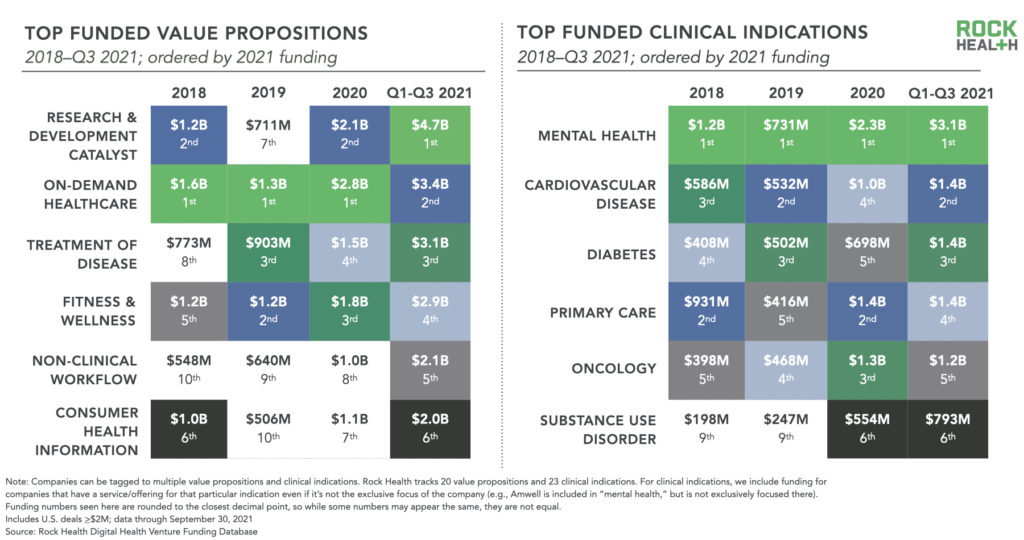

Across Q1-Q3 2021, digital health investors did not depart thematically from prior years, and the most-funded types of companies remained relatively consistent. Digital health companies using software to accelerate research and development, delivering on-demand healthcare services, and supporting treatment of disease continue to reign in the top funded value propositions,4 similar to 2020. For research and development catalysts in particular, funding was buoyed by Q3 mega rounds from XtalPi ($400M), Reify Health ($220M), and TrialSpark ($156M). This quarter’s deals from Maven ($110M) and Pager ($70M) supported on-demand healthcare, while InBrace ($102M) and Woebot ($90M) bolstered this quarter’s treatment of disease funding.

When it comes to particular clinical or disease areas, investors continue to finance opportunities in mental health, the top-funded therapeutic focus so far in 2021 with $3.1B raised. Digital mental health funding was boosted by Q3 deals from behavioral health provider marketplace SonderMind ($150M) in July and mental health unicorn Spring Health, which received a $2B valuation after a $190M Series C in September.

As digital mental health companies compete in an increasingly crowded space, we’re seeing more startups differentiate by focusing on complex mental and behavioral health support, including serious mental illness and substance use disorders. Recent investments include Quit Genius’s $64M in July, Lucid Lane’s $16M in August, and NOCD’s $33M in September. Q3 also saw behavioral health incumbents expanding into these complex care needs. In August, mental health benefits provider Lyra Health rolled out technology-integrated care solutions addressing alcohol use disorder and suicidality, and in September, insurer Highmark announced a partnership with Ria, a digital care platform for alcohol use disorder. In the substance use disorder support space, digital health companies have raised $793M so far in 2021—already a 4x increase from 2018’s $198M.

Alongside these dominant investment themes, 2021’s digital health’s cash infusion is also distributing dollars to emerging areas within the marketplace, including women-led digital health teams, women+ digital health solutions, and digital health companies addressing equity gaps.

Women CEOs make headway

Women CEOs5 are closing more private market digital health deals than ever before, with $3.0B raised across 103 deals so far in 2021. Overall, women CEOs closed 19% of 2021’s digital health deals through Q3, the highest percentage we’ve ever seen. For comparison, we reported women CEOs raising 11% of all digital health deals in 2017, and the number has been increasing each year since: last year, women CEOs raised 16% of digital health deals. However, women-led companies are raising, on average, less money relative to their men-led counterparts. Despite raising 19% of rounds, women-led companies accounted for just 14% of 2021’s digital health total funding pot to date, with a $29M average check size for women-led rounds, compared to $42M for men-led rounds.

This funding statistic is related, in part, to the age of today’s women-led digital companies: 59% of digital health deals raised by women CEOs so far in 2021 are Seed or Series A, compared to 40% of deals for men-led companies. Given this early-stage activity, we anticipate a cohort of women-led digital health startups raising later-stage rounds over the next few years, and we’re already seeing first movers take center stage. Maven ($110M), Modern Health ($74M), and Evidation Health ($153M) reached unicorn status this year after large funding raises, and in September, Spring Health’s CEO April Koh made headlines when she became the youngest woman currently running a unicorn at 29 years old.

Funding boosts for women+ digital health

Funding women+ digital healthcare companies is no longer a novel move, and we’ll say it again: women+ health isn’t a niche market. 2021 continues to spotlight opportunities within this segment as the COVID-19 pandemic exacerbates care gaps and disparities for women+. 2021 women+ digital health funding through Q3 is already 2.3x larger than the amount raised in the same time period in 2020, bolstered by Q3 deals from Maven ($110M), TMRW ($105M), and Woebot ($90M).6 Q3 was the second-highest funded quarter for women+ health ever with $443M raised, following Q1 2021 ($631M).7 In fact, Q3 accounted for 33% of total women+ digital health funding ($1.3B) in 2021 so far. We expect there’s more to come for this space as attention and dollars are funneled to previously-overlooked areas for women+, including tailored behavioral healthcare, menopause support, and digital therapeutics.

Interest in women+ digital health reinforces the broader trend that segment-specific care offerings, such as specialized care for particular populations, are priority areas for digital health companies looking to build comprehensive care platforms. Particularly when selling to large enterprise buyers, telehealth and platform companies are learning that offering tailored service for key populations grants them a competitive edge for now, though may eventually become table stakes.

Health equity efforts gain momentum

Disparities laid bare by the pandemic and national movements for justice have created a crescendo for greater equity in all digital health products, and several early-stage digital health solutions centered on equity raised capital this past quarter. To name a few, Soda Health secured $6M to launch a social determinants of health benefits platform, MiSalud added $5M for its health and wellness app for the Latinx community, Alkeme Health raised $3.5M for its digital mental health platform that centers the Black experience, and Cayaba Care announced $3.2M to build out digital care offerings for underserved mothers.

We’re also seeing companies apply cash infusions to address remaining care barriers. For example, after being acquired by Headspace, Ginger announced that its digital mental health services would be made available in Spanish, with a full rollout in 2022. Following a $150M raise in March, Unite Us, a technology company focused on creating health and social service networks, acquired NowPow in September to expand its geographic footprint. Not to mention, Cityblock Health, which raised $192M back in Q1, grabbed $400M more this quarter in its continued effort to bring person-first healthcare to low-income patients at scale.8

While it’s encouraging to see increased investor attention and funding toward health equity efforts, it doesn’t guarantee that disparities will be meaningfully addressed. We’re eager to keep supporting innovators and companies on the path to demonstrating outcomes that move the needle in this moment and beyond.

Thinking critically about all the dry powder

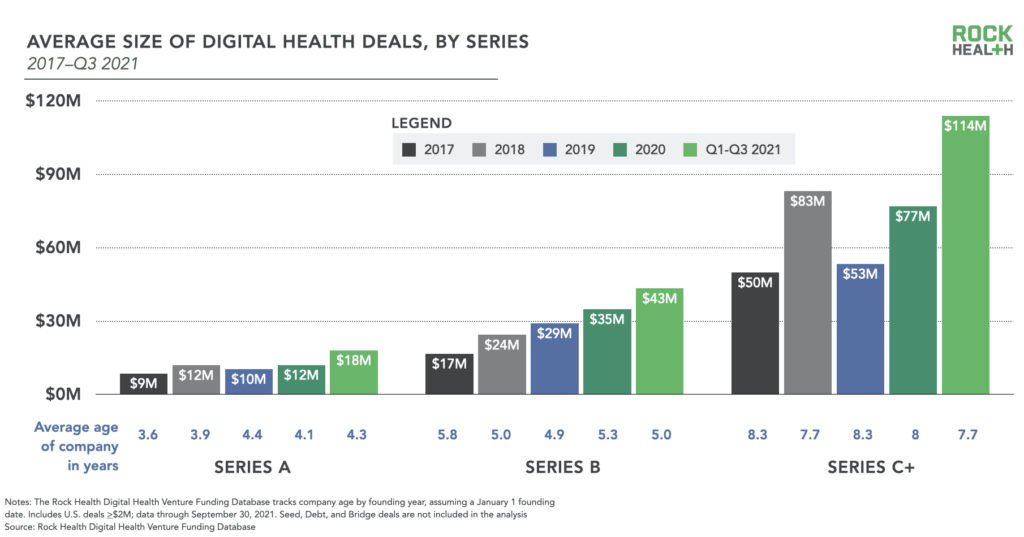

Digital health’s top three quarters of funding—all in 2021—signal that investors and entrepreneurs are betting on strong, consistent growth in the adoption of healthcare innovation, and these expectations are materializing in increased funding patterns across all stages. Average funding for 2021 Series A and B rounds grew 2.1x and 2.6x respectively since 2017. To put this in perspective, this year’s average digital health company’s Series A raise ($18M) exceeds the average Series B raise in 2017 ($17M). In other words, A is the new B.

Today’s funding growth isn’t limited to early-stage deals. The average funding amount for Series C+ rounds in 2021 is 2.3x what it was in 2017. And in terms of overall deal count, 59% of digital health deals in Q1-Q3 2021 were early to mid-stage (Seed, Series A, Series B) compared to 70% in 2017. This suggests that 2021’s growing Series A and B round averages don’t reflect investors shifting investments to earlier stages; rather, their growth is a reflection of the market’s overall funding swells.

Digital health companies aren’t just raising more money per round; they’re also raising early-stage rounds more quickly. In 2017, the group of digital health companies that raised their respective Series As were, on average, 3.6 years old, and the group that raised Series Bs were 5.8 years old.9 In 2021, this shifted to 4.3 and 5.0 years respectively, narrowing the gap between the cohorts. While there are some key limitations to this analysis—mainly that it does not track the same companies over time—it approximates the broad trend we’re seeing of reduced times between A and B raises for digital health companies.

Additional analyses point to higher velocity funding: of the 81 companies that raised a Series B between Q1-Q3 2021, 40% (31 companies) raised their Series A less than 20 months prior in either 2020 or 2021. Comparatively, only 22% of 2020’s Series B startups raised their A rounds in either 2019 or 2020, and 24% of 2019’s Series Bs raised their As in 2018 or 2019.

From our vantage point, there are a few key factors crunching average time between early-stage rounds. First, there’s unprecedented capital in healthcare and beyond, brought on by mega investors such as SoftBank and Tiger Global and catalyzed by broader market conditions including low interest rates and a healthy stock market. With capital flowing, startups feel motivated to carpe diem and raise rounds quickly while the market is hot.

Faster raises are also likely influenced by startups today having the advantage of learning from go-to-market strategies (successful and not) implemented by mature digital health companies in their earlier years, creating a knowledge infrastructure that can be leveraged as a guidebook for new entrants or as an evaluatory de-risking tool for investors.

Startups also benefit from another kind of infrastructure—software. Q3 2021 featured funding for startups Commure, Xealth, and Rock Health port co Zus Health, which create platforms and programming interfaces that other digital health companies can build upon. Once startups have funding available to leverage the knowledge and API infrastructures at their disposal, they can devote less time to standing up their products and focus on UX, design, sales, and proving out their impact to the broader market.

“Today, we have a running start in digital health innovation. Playbooks that didn’t exist years ago have now been written by category-defining companies.”

– Lynne Chou O’Keefe (she/her), Founder and Managing Partner, Define Ventures

So, will we continue to see the same degree of fast-paced, large rounds, or is there already some evidence of a slowdown in the making? And, with sources like Fenwick & West’s venture capital survey showing valuations rising at a faster pace than at any time in the past 17 years,10 we wonder, can company valuations continue to rise at the same pace much longer?

The answer rests in the tug of war between opposing forces. Some investors look at the vast frontier of healthcare industry opportunity—which digital health startups are still just beginning to explore—and predict the current course and speed of industry funding will continue. Other investors, however, point to pockets of froth in the market and foresee potential disaster. We believe that the overall picture is a blend of both these perspectives.

Though the macro opportunity for healthcare transformation is as big as ever, we believe that near-term investment market trends will moderate in the coming 12 to 18 months. If individual company valuations outpace their fundamentals, the risk of down-rounds for these companies rises; at the very least, pressure grows on teams to quickly “grow into” investor expectations. Plus, we’ve been around long enough to know that good times come and go. While today’s deal terms may be skewing heavily to favor entrepreneurs, the tables will turn. Relationships built (or fractured) now will be considered—on both sides—if there are tougher times ahead. We counsel the middle way: make smart use of today’s bountiful capital but strengthen fundamentals to weather any forthcoming storms.

The future is ripe for consolidation

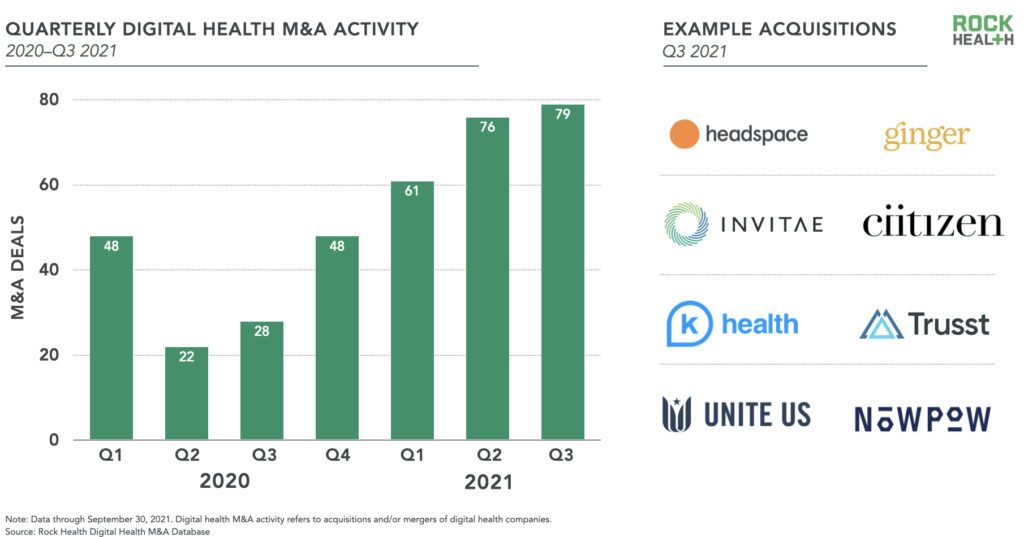

Venture funding isn’t the only metric off the charts; one year after the market-shaking $18.5B acquisition of Livongo by Teladoc, digital health M&A activity has evolved from breaking news to near-daily occurrence. Digital health companies matured quickly during the pandemic, and many are now turning to M&A as a way to scale their product development and client growth.

Overall, Q3 2021 was the largest quarter to date for digital health M&A activity with 79 deals in which a digital health company was acquired or underwent a merger. August alone logged 33 deals—the biggest digital health M&A month ever. Below, we dig deeper into recent M&A activity, shout out a few of the quarter’s serial acquirers (hello Commure and Invitae), and review what Q3 tells us about the consolidation strategies digital health players are adopting to meet market demands.

2021’s M&A boom was spearheaded by several repeat acquirers. Digital healthcare operations leader symplr acquired three companies in just this past quarter: HealthcareSource, SpinFusion, and Halo Health. Meanwhile, health software company Commure announced acquisition to be its primary driver of growth and backed up its claim with no less than three acquisitions in 2021, including Patient Keeper from HCA, Merlin, and Karuna. But no digital health acquirer may be more active than genetic information hub Invitae, which acquired an astounding 14 companies in the past five years. In September, Invitae acquired Ciitizen, a consumer health platform that allows patients to access their medical records.

We’re also seeing a trend of companies raising funding and quickly putting their new capital to work by acquiring smaller players. Unite Us raised its $150M Series C in March and then snagged two companies in Q3—Carrot Health and NowPow. Another example of the funding-acquisition one-two punch is Genome Medical, which simultaneously raised a $60M Series C round and acquired GeneMatters in August to accelerate the company’s growth into virtual genetic counseling.

One key driver of digital health’s acquisition wave is the need to deliver more streamlined offerings and experiences for customers. Customers—patients, providers, and employers alike—are all feeling overwhelmed by different digital health options in the market and are pushing for more unified offerings. In response, digital health companies are using M&A to drive strategies such as vertical integration, horizontal integration, and competitive acquisitions.

“We’re on the threshold of pretty dramatic consolidation. Many companies have either too narrow of a market or a customer concentration issue. As these startups get ready for their Series C and above, many will likely pursue private-to-private consolidation. This will be a great catalyst in bringing comprehensive solutions to market.”

– Michael Greeley (he/him), Cofounder and General Partner, Flare Capital Partners11

Diving first into vertical integration, we see digital health players consolidating different steps of patients’ total care journeys. In August, Headspace and Ginger announced plans to combine to form Headspace Health, offering a full spectrum of mental wellness and care solutions ranging from meditation support to clinical referrals and licensed therapist visits. Vertical integration approaches like these are designed to help patients funnel from broad “front door” wellness exploration to clinical health support, working across all stages of consumers’ needs on their own unique timelines. Another example of vertical integration is combining technology infrastructure components into one seamless care journey. In September, virtual MSK clinic Hinge Health acquired computer vision technology wrnch to help evolve its own product offering.

On the horizontal integration front, virtual chat-based primary care provider K Health announced its acquisition of Trusst in August, a behavioral health app focused on text-based therapy. K Health’s acquisition looks like the beginnings of a strategy to serve multiple clinical service lines with a common tech interface—chat. Horizontal integration allows companies like K Health to expand in size, diversify product offerings, and expand into new markets, all while refining their core chat experience.

Lastly, companies’ focus on ramping up size and entering new markets means we’ll continue to see digital health players acquire competitors. In September, Flywheel, a platform that helps researchers process imaging data, leveraged its recently-raised $22M Series C to acquire Radiologics, a competing medical data processor.

In contrast to its swell of M&A activity, Q3 saw a slowdown in digital health companies exiting via SPAC and IPO. In Q3 2021, there were three completed SPAC mergers (Sharecare, Owlet, Sema4) and two IPOs (Definitive Healthcare and Cue Health), alongside one announced SPAC and two announced IPOs. This is a departure from the frenzy of Q2, which had four completed SPACs, four IPOs, and seven announced SPACs. While Q3’s public exit slowdown is certainly influenced by heightened regulatory scrutiny and a general cooling of the SPAC investor craze, we’re interested to see how public exit activity continues into the final quarter of the year.

Onward we go

2021’s breakout funding is evidence of an unprecedented mandate for change, across all aspects of healthcare. After all the movement in the market so far this year, we’re curious to see what Q4 holds; historically, the final quarter of the year hasn’t been the biggest for funding, but all that changed when Q4 2020’s funding surpassed all preceding quarters that year. With that in mind, we’ll catch you again soon for more funding analysis once 2021 wraps.

Rock Health Capital invests in Seed and Series A stage entrepreneurs bringing unique and innovative technology to healthcare. We would love to hear from you. Get in touch!

Rock Health Advisory provides guidance on digital health strategy, access to proprietary funding databases, and in-depth perspectives on the digital health market. For digital health insights targeted to your needs, drop us a note.

Finally, stay up to date with the latest headlines in healthcare technology and Rock Health news by subscribing to the Rock Weekly.

Footnotes

- The Rock Health Venture Funding Database is constantly refreshed with new information and SEC filings, including deals closed in the prior year. This accounts for an increase in 2020 funding relative to our EOY 2020 reporting.

- Rock Health defines women+ health as encompassing digital health solutions that work within or across the full spectrum of health needs experienced by cisgender women, as well as others whose health needs relate to those of cisgender women but identify as transgender or nonbinary. This category encompasses menstruation and menopause care, pregnancy and postpartum care, sexual and reproductive health, and fertility support (egg freezing and IVF), as well as behavioral health, exercise and nutrition, cancer prevention, and other health services delivered specifically for this population.

- The Rock Health Venture Funding Database is constantly refreshed with new information and SEC filings. This accounted for a change in Q1 2021 funding relative to our Q1 2021 reporting.

- Each company in the Rock Health Funding Database is tagged with at least one and up to three “value propositions.” Since each company may fall into multiple value propositions, the sum of funds raised across value propositions does not sum to the total funds raised.

- The Rock Health Digital Health Venture Funding Database tracks each company’s CEO and assumes gender based on LinkedIn photos and public pronouns. This measure only accounts for one CEO and assigns one of two options: man or woman.

- Rock Health’s women+ funding analyses include companies that exclusively address women+ care needs (such as Maven and TMRW) as well as companies that support women+ health in addition to other communities (e.g., Woebot, Hims&Hers, Ro).

- Q1’s $631M in women+ digital health funding consisted of six deals, including Ro’s $500M Series D.

- Cityblock Health’s rounds are not represented in Rock Health’s Venture Funding Database and funding figures due to their clinic-based model. Learn more about how Rock Health defines digital health here.

- The Rock Health Digital Health Venture Funding Database tracks company age by founding year and assigns a January 1 founding date.

- According to pages 6-8 of the Fenwick & West report, the average price change of venture capital financings in Q2 2021 was 186%, compared to the 17-year average price change of 65%. The median price change in Q2 2021 was 140%, compared to a median price change over the past 17 of 35%.

- Michael Greeley shared this insight during a MedCity INVEST Digital Health webinar titled, “The Next Phase of Digital Health Investment.”